In what has now become an annual tradition, at the start of the year we published our 15 predictions for trends that we expected to shape cross-border payments across 2025. Now we’re closing in on the end of the year, how have they fared against reality?

Technology shapes cross-border payments in 2025

Grouped into three areas – technology-led, industry-wide and vertical-specific – our cross-border payments predictions for 2025 have for the most part been fairly accurate.

While 2024 saw longer term trends begin to establish themselves across areas as diverse as transparency and interoperability, both of which remained background themes this year, technology has undoubtedly been the critical shaper of this year.

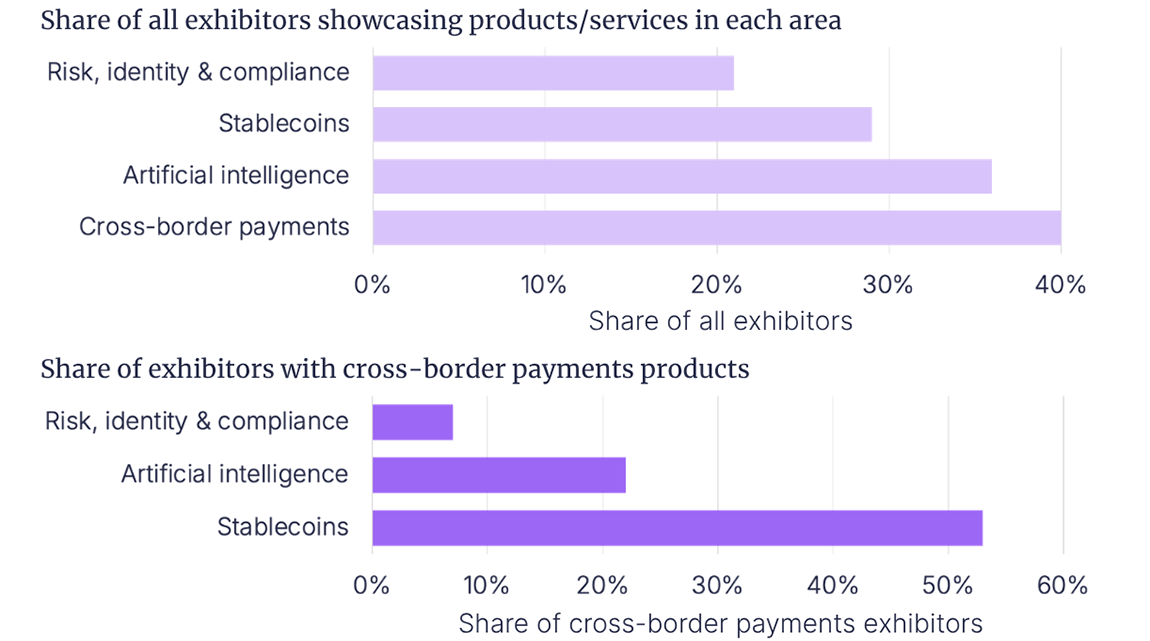

As predicted, this has undoubtedly been the year of stablecoins, which finally found mainstream acceptance in 2025 with a dramatic increase in discussion among public companies in Q2 as the passing of the GENIUS Act opened the floodgates for a variety of use cases. This has also prompted greater interest in wider blockchain technology, with tokenised deposits in particular seeing increased discussion and application.

Our expectations around AI have similarly borne out, with several companies including the technology in their financial reporting, particularly around customer service and in-house productivity in the most recent earnings period, although we did not foresee agentic AI in particular becoming as dominant in some discussions as it has.

Meanwhile, industry use of data has stepped up, albeit with some way to go yet, but our prediction around quantum computing was less accurate. There has been the occasional glimmer of interest in quantum computing, with the technology being the focus of a number of thinkpieces, but we haven’t seen any really meaningful movement on this in 2025.

Predictions in our ‘industry wide’ category were more focused on market moves and, as expected, there have been a number of companies to exit the public markets this year, although these have largely been the result of acquisitions by other payment companies, including the completion of Railsr’s acquisition of Equals, as well as Western Union’s Intermex acquisition and IFX’s purchase of Argentex.

As part of this, private equity players and related investment groups have continued to play a role, including funding the Railsr acquisition and making multiple investments in later stage private players, including Revolut’s most recent fundraise. There weren’t any industry-defining moves this year in this area, but investment remains key to even some of the sector’s biggest players, and that’s unlikely to change in the near future.

There are also signs that the environment is once again becoming more favourable to public market debuts, with Circle pulling off a blockbuster IPO on its third attempt at becoming a publicly traded company, while discussion of other players’ prospects is becoming more pronounced, particularly for Stripe.

On cross-border payments pricing, our speculation that the G20 targets would drive a big policymaker-led push has proved incorrect, with only minimal policy-led efforts and the chance of meeting the 2027 KPIs vanishing. However, focus on interchange fees was aided by regulatory efforts, particularly with a key ruling in the UK as well as Visa and Mastercard’s announcement of a settlement with US merchants, while blockchain-based solutions such as PayPal’s Pay with Crypto are presenting an alternative approach.

Turning to ‘vertical specific’ predictions, netting has seen increased interest for B2B payments and treasury solutions, with several announcements this year, although you wouldn’t know if you weren’t paying very close attention – stablecoin-based solutions provide an alternative approach and so have drawn considerable focus.

Banks, meanwhile, have seen continued specialisation from those focused on cross-border payments, with the topic being a key focus for Standard Chartered’s Corporate & Investment Banking investor day while Citi has seen increased cross-border growth. By contrast, others have continued to pay limited attention to the sector, while a growing number have opted to partner with B2B2X solutions, such as UniCredit, which this year partnered with Wise Platform.

Such B2B2X players have also continued to grow their networks this year, with Thunes among those to add stablecoin integrations alongside continuing to build their card and wallet endpoints, while there has also been increased efforts around interconnecting digital wallets, including via PayPal’s Alipay+ rival PayPal World.

Meanwhile, between Intermex’s sale to Western Union, the establishment of the US tax of cash remittances and MoneyGram’s refounding as a fintech, digital has become the primary driver for money transfers players across the industry.

Finally, ecommerce has continued to see some expansion of its localised payments support, although this has been overshadowed by agentic AI as a focus for many players.

In the new year we’ll be sharing our predictions for 2026, so stay tuned to see how we see the 12 months ahead shaping cross-border payments.