UniCredit has partnered with Wise Platform to launch a brand new international payments service focusing on the retail/low-value payments segment of its business. To explore the bank’s ongoing cross-border payments strategy, we spoke to Raphael Barisaac, Global Head of Payments & Cash Management at UniCredit, and Steve Naudé, Global Managing Director at Wise Platform.

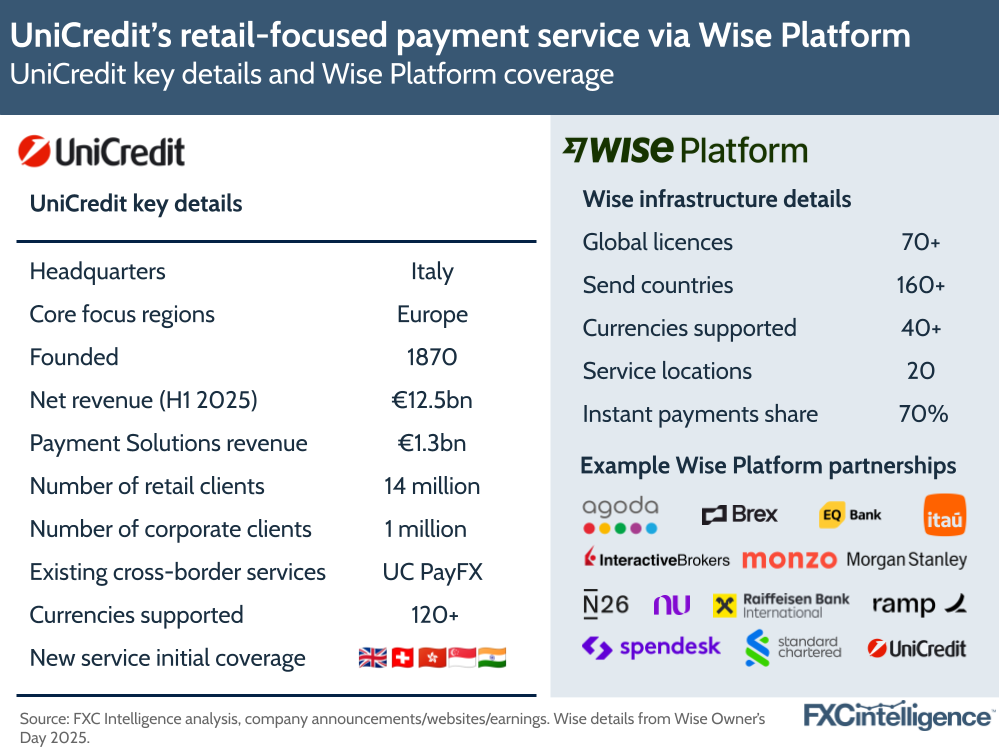

Earlier this month, UniCredit became the first major Italian bank to launch a new international payment service for its retail customers in partnership with Wise Platform – Wise’s payments infrastructure product. Italian UniCredit customers can now use the service to send and receive payments from a number of selected countries, including the UK, Switzerland, Hong Kong, Singapore and India, with more currencies to come.

UniCredit positions itself as a leading bank for payments and cash management in Europe. Through its Payments Solutions division, it helps clients to manage cross-border payments and end-to-end services, with its existing UC PayFX service enabling automated conversion in over 120 currencies. Last year, UniCredit also enhanced its cross-border payments services for retail clients, SMEs and corporates through the addition of Swift GPI, which allowed them to track the status of international payments in progress.

Having seen success with corporate clients, the bank is focusing specifically on retail and low-value payments through the latest deal. Partnering with Wise Platform allows UniCredit to quickly enable access to its on-the ground presence and connections to local payment systems. Meanwhile, Wise hopes that partnering with banks will allow it to tap into a massive cross-border payments TAM (for the non-wholesale market, we estimated this to be worth $40tn in 2024), and expects to grow Platform to one day account for roughly half of its cross-border volumes.

One of the unique assets Wise Platform can really leverage versus competing infrastructure players is the payment patterns and issues it sees from its own customers (totalling 15.6 million in FY 2025, according to the company’s most recent annual report). It uses this data, for example, to estimate to a high degree of accuracy the speed of a payment from the sender to the end beneficiary (not just the beneficiary bank), leveraging customer feedback from its large payments dataset.

To explore this ongoing shift and what UniCredit and Wise will get out of the latest deal, we spoke to Raphael Barisaac, Global Head of Payments & Cash Management at UniCredit, and Steve Naudé, Global Managing Director at Wise Platform.

Inside UniCredit’s cross-border payments strategy

Barisaac says that the bank has made significant progress for corporate and SME clients. However, it now wants to provide a product to its individual clients that replicates what Wise and similar companies are offering today and move away from the traditional correspondent banking model.

“When we talk about cross-border, it is not really one-size-fits-all,” Barisaac says. “When we talk about low-value payments, this segment requires specific things. They want to have transparency about how much is going to be credited, they want to know when it is going to be credited and they want to know how much they’re paying for everything, the FX and the fees.

“The traditional correspondent banking model does not provide that for various reasons. It’s a fantastic model for many other things, but for individuals today, it just doesn’t provide that.”

UniCredit is using Wise to connect different domestic payment schemes globally, but also to enable it to provide a superior end-to-end product for its customers that give the bank a “superior” offering, one that Barisaac claims has become the “standard today in the market”. The bank has carried out studies internally, using client feedback to find out where to improve its service and update its pricing model for clients.

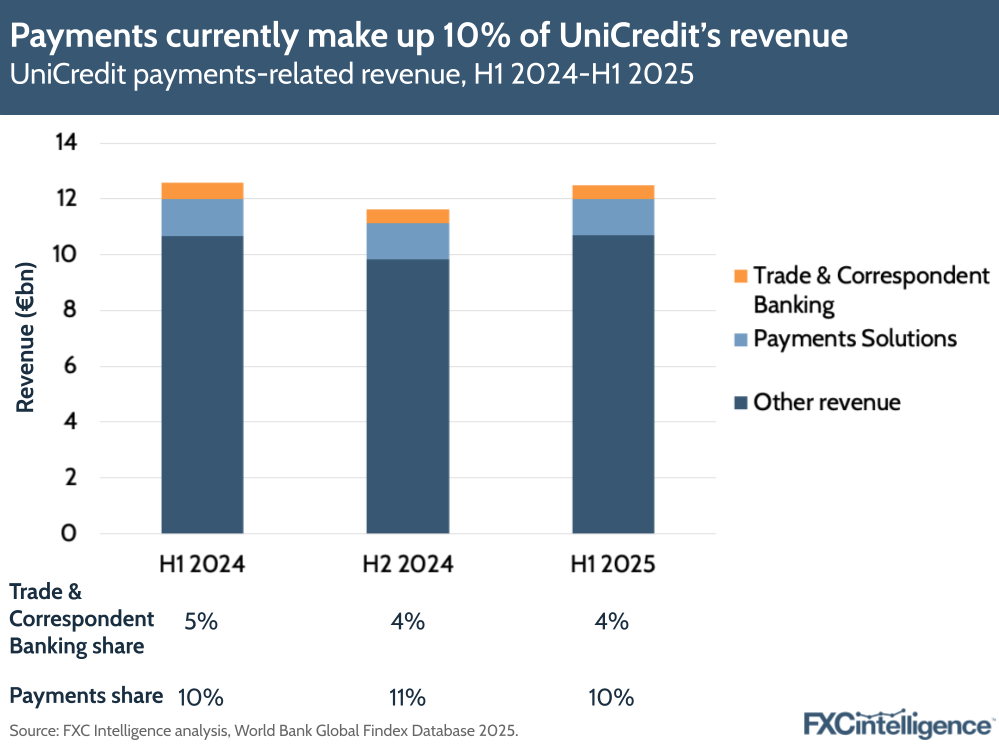

Similar to other major global banks, payments currently form a small but not insignificant part of UniCredit’s overall revenue. The company’s Payments Solutions arm (under its Client Solutions segment) produced around €1.3bn ($1.4bn) in revenue in H1 2025, around 10% of UniCredit’s overall revenue for the half. Separately, Trade & Correspondent Banking falls under the bank’s Corporate Solutions segment, and accounted for around 4% of UniCredit’s total revenue during the same period.

Navigating the competitor-to-partner relationship

A consistent theme in cross-border payments has been banks either partnering with other businesses specialising in the space – many of which may be competitors – in order to quickly expand cross-border capabilities or gain access to payment rails into other countries.

Barisaac explains that for banks of UniCredit’s size, partnering with other players to enhance its services makes sense. UniCredit serves millions of retail customers worldwide, with international payments being just one of many services offered through its mobile banking, making it difficult to invest the same amount that a specialist provider could in just that one service.

“In this industry, the business is going to develop by having services provided by others,” Barisaac states. “You cannot do it by yourself. And since the industry as a whole is not moving jointly in a common direction, you need to decide where you want to be.

“For UniCredit, we decided we still want to be a relevant player in this field a couple of years down the road. That means you have to take action.”

From Wise’s perspective, Naudé says that the banks like UniCredit who are looking to use Wise’s infrastructure transform their payments service into a full end-to-end experience, and not just make incremental savings in certain areas, are a real draw for the business.

“Banks like UniCredit realise that it’s not just about the rails,” explains Naudé. “It’s about that real end-to-end offering that you give to a customer. You need to be able to move money in seconds, with no deductions and at a low cost with full transparency.

“It’s the experience, the UX, the UI, the servicing, the ops, the compliance and the treasury. And if you get all of this to come together, you can build an amazing product for retail customers.”

Why banks are upgrading their cross-border payments offerings

Naudé posits that banks are picking up on what customers expect from low-value payments, which he says is changing “faster than ever before”. Driving this are significant improvements in domestic payments in countries such as the UK, which enable instant P2P transfers, bill or invoice payments. Increasingly, this expectation is being translated to cross-border.

“You’ve seen this change in the market happen very quickly,” says Naudé. “And therefore more and more banks and other institutions are saying, ‘If we want to remain relevant in this space to our customers, we are going to have to deliver a cross-border payments experience that looks something like this’.”

Wise has found that customers in Europe – where UniCredit is focused – have similar high expectations to other areas in the world. “Maybe Europe is a market of itself, but there’s still many neighbouring countries in many parts of the world that Europe trades with, or people have moved to or from, that are non-same currency payments,” he says. “A lot of the dynamics there are the same and a lot of the conversations we have are very similar.”

Why Wise Platform is winning business from banks

The deal is one of several high-profile wins for Wise Platform. Several other big banks have partnered with Wise to launch new products, including Morgan Stanley, Raiffeisen Bank and Standard Chartered, with the platform having surpassed 100 customers according to Wise’s recent Owner’s Day figures.

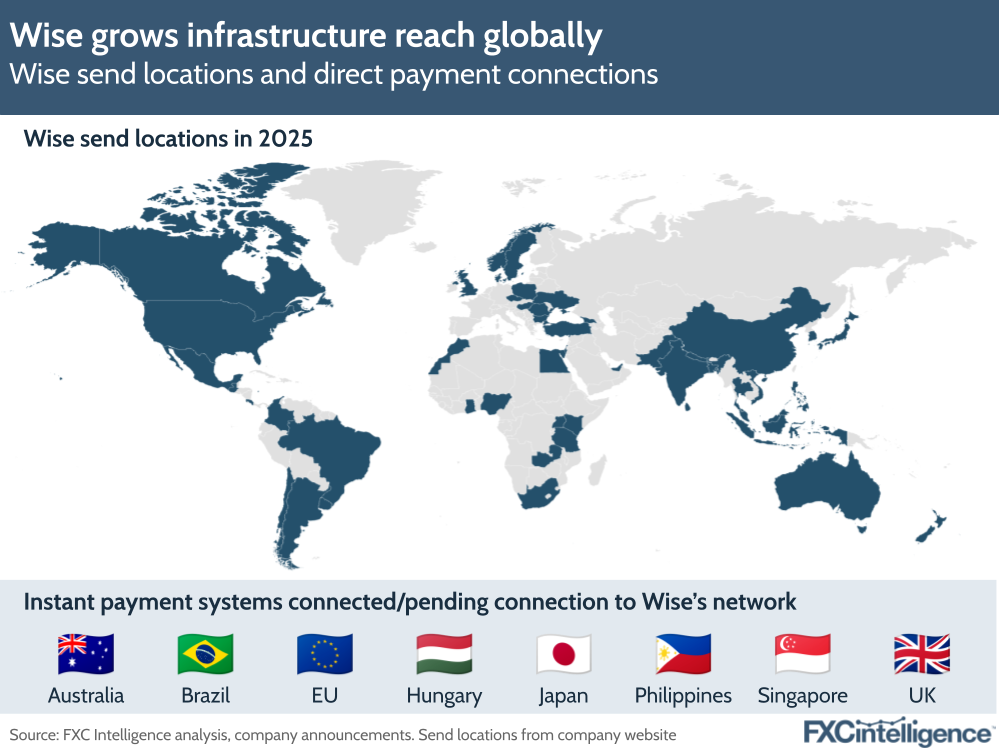

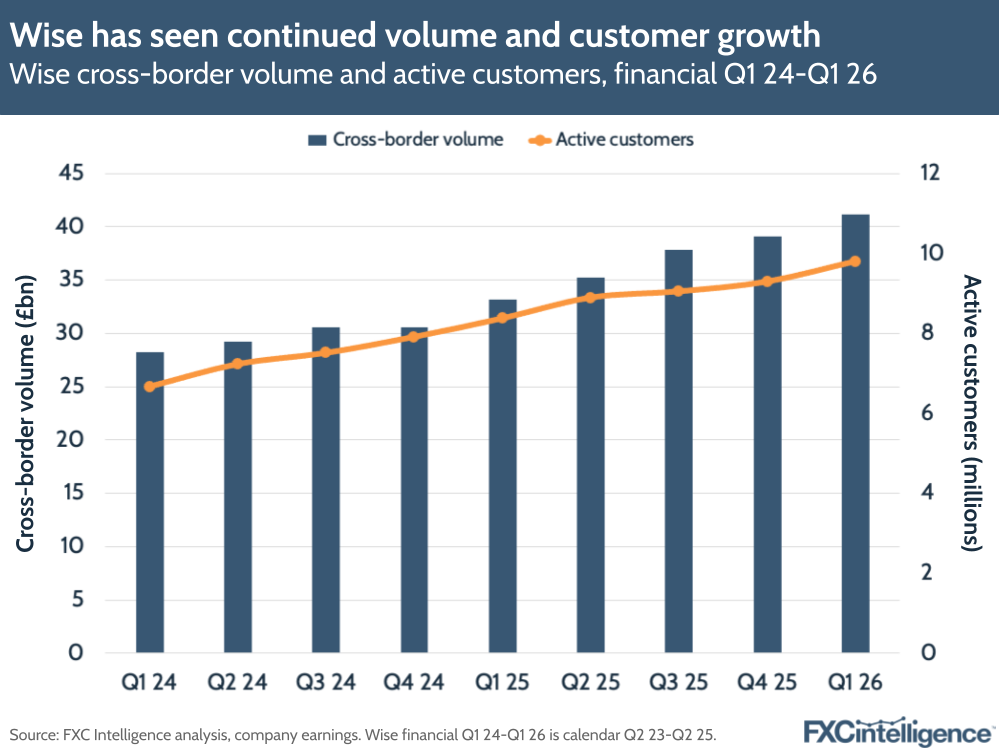

Since its founding in 2011, Wise has grown to become one of the world’s leading players in global money movement. In its most recent trading update for Q1 2026 (calendar Q2 2025), the company saw cross-border volumes rise 24% to £41.2bn, with 9.8 million active customers holding £22.9bn on the platform. This drove the company’s underlying income to increase 11% to £362m in the quarter.

Earlier, in its FY 2025 results, Wise announced that it would dual-list its shares in the US and the UK with a primary listing in the US, partly to grow capital but also to help promote Wise Platform to a wide base of banks across the country.

For Naudé, Wise’s established customer base is what gives Wise Platform a unique advantage over other competitors. The company has used data from its customers to optimise each part of its network – from knowing when money will arrive, to minimising failures across certain payment flows and improving its straight-through processing rate.

For example, Wise Platform is able to tell users accurately when money will arrive within one hour, based on customer feedback, tests and “reverse engineering” the world’s payment schemes so that the company knows exactly which banks use which cutoffs and how long it takes them to credit their end customers’ accounts. In another example, Naudé says that Wise saw a double-digit percentage conversion increase from customers in Morocco after changing the terminology used in its transfer documentation based on customer feedback.

All these “little details”, in addition to wide-ranging investment in Platform, make Wise stand out in the market. “Being able to take this very optimised piece of infrastructure and then work with banks to help them build these world-class experiences is really where we’re quite unique,” Naudé says.

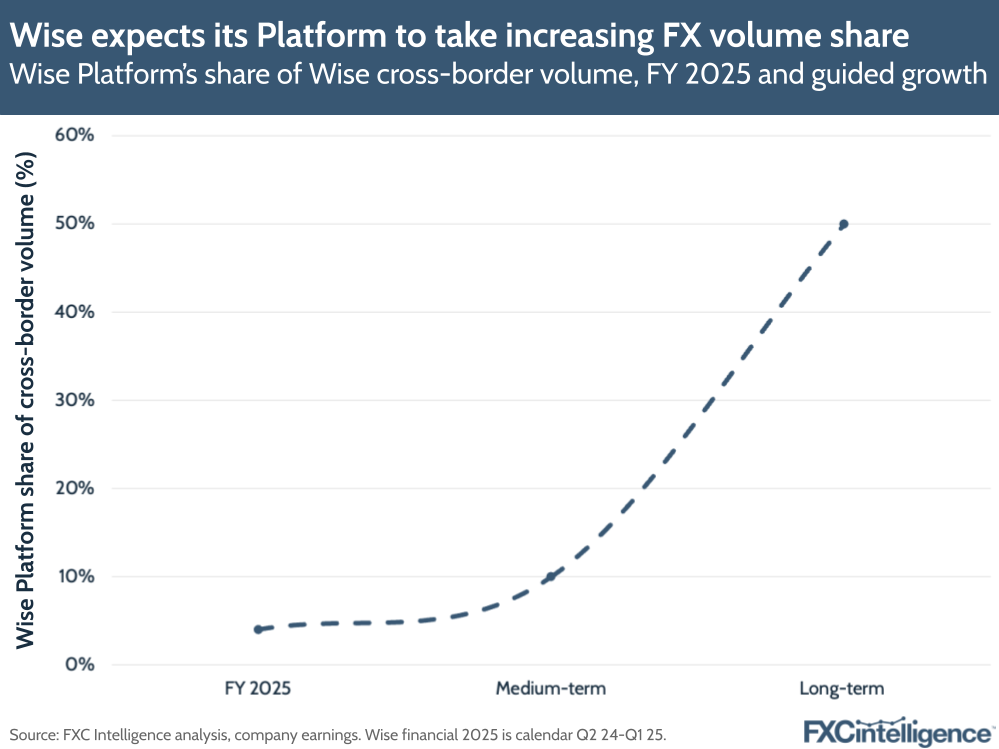

As of Wise’s most recent discussion of its Platform product in its earnings results, it currently accounts for 3-4% of Wise’s cross-border volume, but Wise expects that this could move to 10% in the medium term and rise to 50% in the long term. This is part of the company’s ongoing shift in its mix, away from purely providing money transfers to diversify its business streams; Card and Other Revenues accounted for 29% of its underlying income in Q1 2026, up from 25% in Q1 2025 and 19% in Q1 2024.

Wise Platform, however, will be the key to Wise accessing the trillion-dollar cross-border opportunity. Naudé says the focus is on building stronger, more resilient, more reliable, faster, lower-cost infrastructure that more and more banks and global players start using.

“At the core is going directly to payment schemes and continuing to invest in our treasury, our compliance and our operations,” Naudé says. “We’re planning to invest about £2bn in the next two years in this infrastructure and we expect to see all these investments pay off and have a stronger offering for UniCredit, their customers and many other banks as well.”

The impact of future innovations on cross-border payments

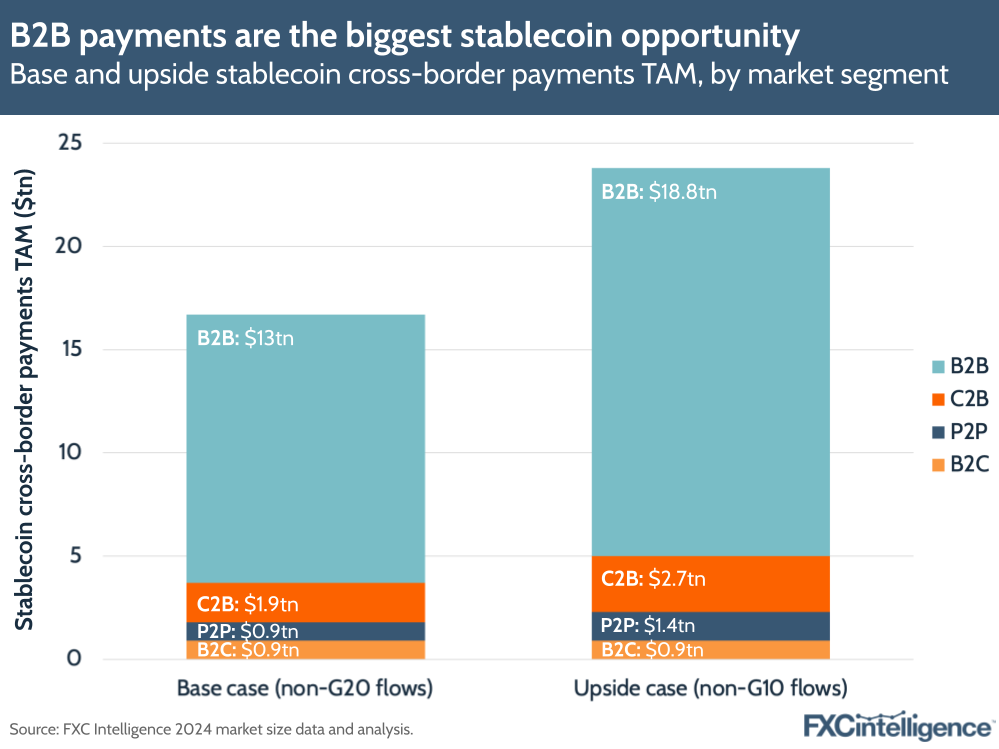

When it comes to enabling faster payments across borders, one topic that banks and cross-border players can no longer avoid is stablecoins. Our recent industry primer on the technology found that the base stablecoin cross-border payments TAM currently sits at $16.5tn across all verticals. Of this, B2B payments currently make up a significantly larger opportunity compared to C2B, P2P and B2C payments.

Barisaac says that UniCredit has been following what’s been happening in the market, but that he doesn’t currently see the use case for stablecoins in low-value individual payments. “Maybe in the future, but right now when we look at the use cases that are in the different types of industries, I don’t think that it will make a big impact on low-value payments for individuals,” he clarifies.

Similarly, Naudé says that Wise is “interested” in the fast-evolving stablecoins space, and as a “rails-neutral” company is primarily focused on moving money in the fastest, lowest-cost and most reliable way – but he says this isn’t stablecoins yet.

“Our job is to move money for customers in those criteria – the speed, the price, the secureness, the reliability – and in reality, today in most cases, it’s not able to help us do those things better.”

Another key trend for many industries is AI, which has been increasingly mentioned across banks’ earnings reports. Our industry analysis shows that cross-border players are discussing its use across three key areas: fraud protection and compliance, transaction/treasury optimisation and customer service and experience.

Naudé lists a number of opportunities for improvements in automation that could make payments more efficient and effective, such as answering customer queries, building machine learning models for preventing fraud, enhancing day-to-day payment operations and monitoring transactions.

“We’re seeing a whole number of interesting use cases crop up where technologies like AI could help solve that automation problem faster,” Naudé relates. “But it’s also what we’ve been doing for many years in terms of automation. Can it help unlock new things or make those things move faster? Potentially, yes.”

Barisaac, meanwhile, argues that opportunities for AI currently are being seen in “back office” and “middle office” activities (i.e. playing a supporting role) for financial institutions, with the expectation this will remain the same in the short to medium-term future. This is because applying such technology across the highly complex cross-border payments system will not be easy – particularly when considering different countries with different regulations.

“What I can tell you about this business is that there is not any magic solution,” Barisaac states. “This is a very complex business that has a lot of components provided by different types of providers in the value chain.

“You cannot really industrialise the value chain. You can make improvements in part of it, but if, for example, I want to transfer money to Brazil, I still need to provide certain types of details, and that would not be the case if I transfer to another place.”

Within the wider context of the cross-border industry, the global impact of innovations such as stablecoins and AI is still an ongoing story, and in many ways the true impact of these on payments is yet to be seen in the space.

In the here and now, it is significant that money transfer providers have scaled their networks to the point that banks are now tapping into their services to enable faster and speedier transactions than the traditional correspondent banking network can sustain.

For the moment, Barisaac is looking forward to seeing the impact of the bank’s new service after a successful pilot period.

“We have to see how this is going to evolve,” he concludes. “And to be honest, we are really, really excited about that.”