Money transfers and remittances continued the shift to digital in 2025 even as political moves in the US hampered transactions along one of the world’s most influential corridors. In this report, we’ve highlighted some of the key trends and takeaways from 2025.

This year has been a mixed year for the remittances and money transfer space. On the one hand, many players have noted continued revenue growth on the back of digital gains. On the other, various macroeconomic and political effects have shifted the balance across some corridors this year, leading some players to rethink their strategy and even a major acquisition in the form of Western Union’s takeover of Intermex.

Our most recent market sizing update puts the non-wholesale cross-border payments market at $40tn in 2024. While consumer-to-consumer payments made up a relatively small part of this, at $2tn, it is still a major opportunity for providers in the space, expected to grow to reach $3.1tn by 2032.

Below, we’ve explored some of the key trends and stories from 2025 in more detail, giving an insight into the year that was for cross-border consumer money transfers and remittances.

How have public consumer money transfer companies performed in 2025?

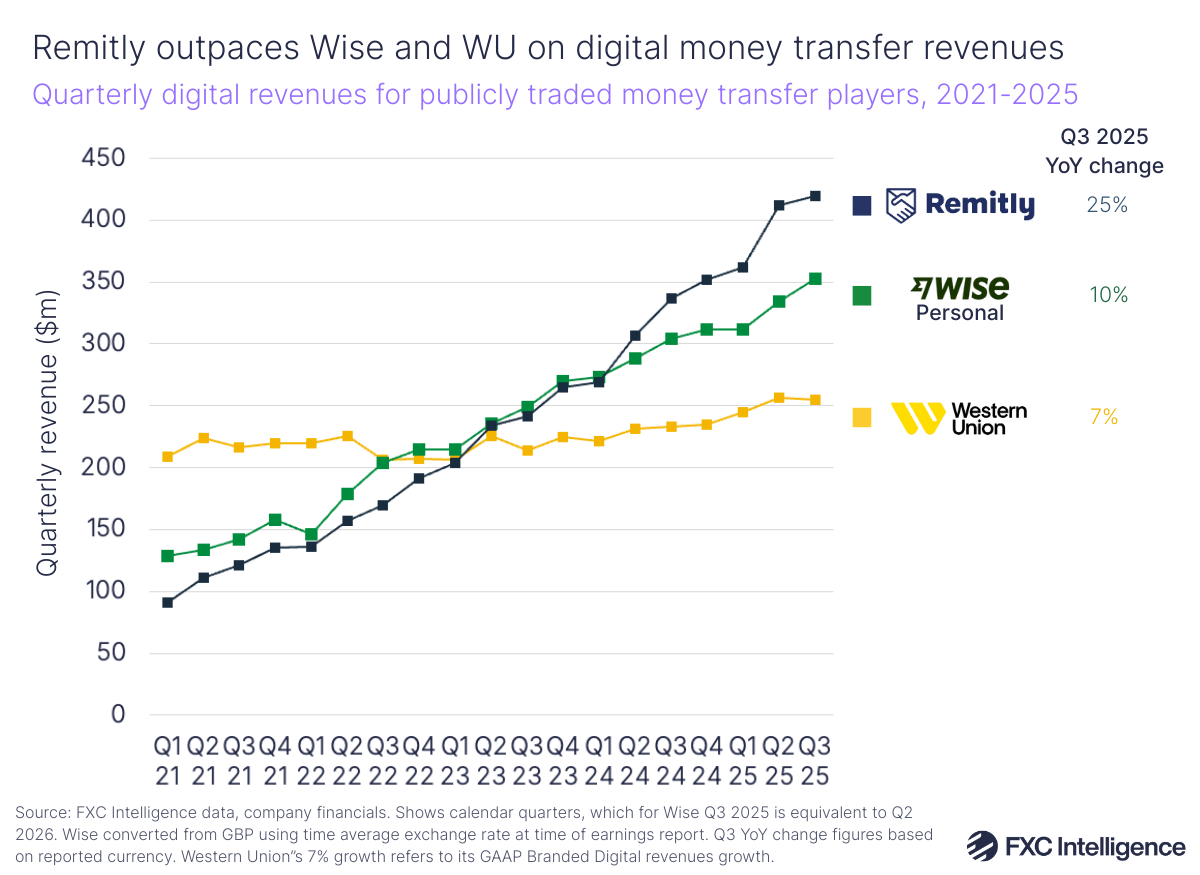

Among the four money transfer providers we track, Remitly remained the standout growth story in 2025, with double-digit YoY growth across every quarter this year outpacing other major players.

For example, in its Q3 2025 earnings, Remitly saw revenue rise 25% to $420m. It continued to grow faster than Wise’s Personal segment, which rose 10% to £261m ($352m), and Euronet, which posted a more modest 3% increase to $452m.

Western Union, by contrast, saw its Consumer Money Transfer (CMT) revenue fall 6% to $878m in Q3 2025 – but it still leads the C2C pack by revenue, retaining a sizeable share of the market.

Geopolitical impacts affect key corridors

Public companies in the money transfer and remittances space often mention the impact of macroeconomic factors on earnings, but this year has seen some particularly strong external influences on markets and corridors that have led to subsequent effects on companies serving the industry.

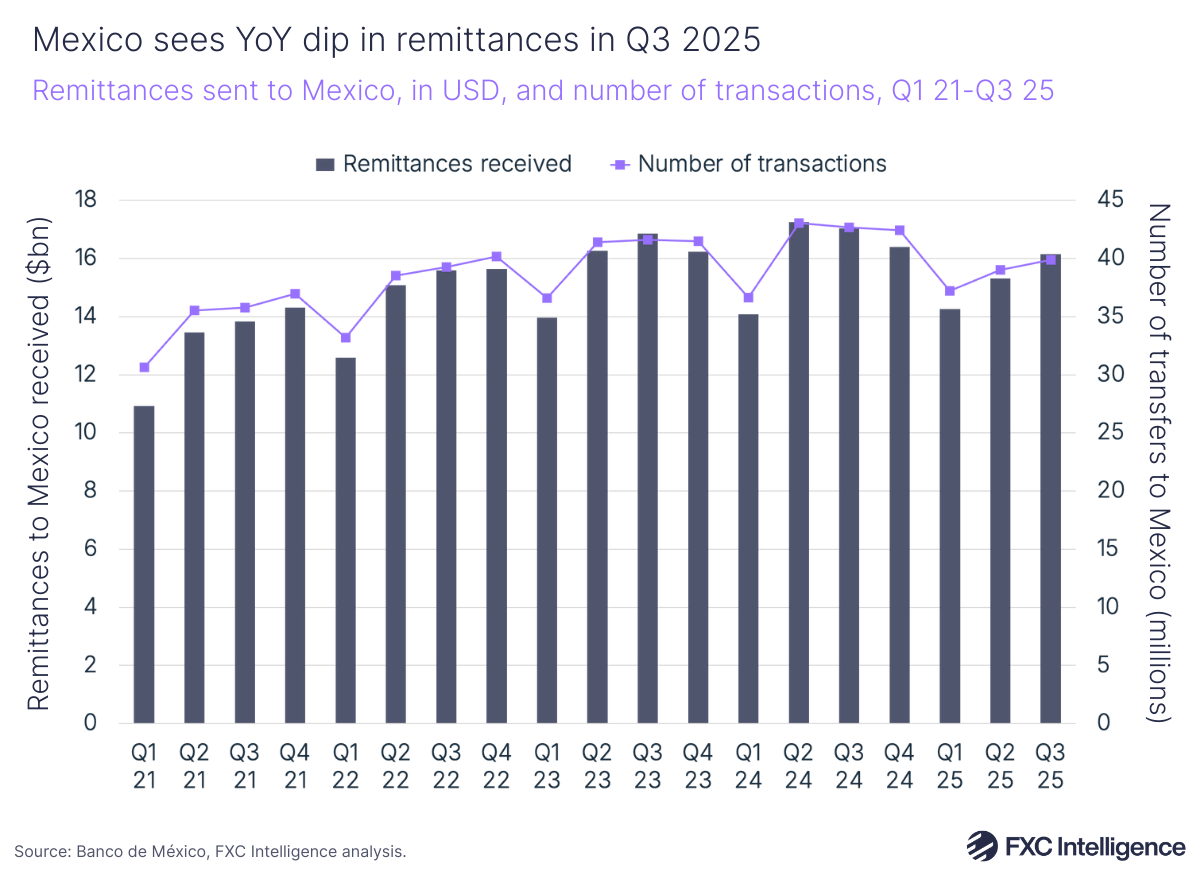

Changes in regulations in the US have led to a decline in border crossings and more enforcement on migrants to the country. This was linked with changing consumer behaviour when it comes to remittances, with fewer transfers sent across key corridors to Latin America – particularly US-Mexico, the world’s biggest money transfer corridor.

Inbound remittances from abroad to Mexico decreased by 16.2% YoY to $5.2bn in June 2025 – the steepest monthly decline the country has seen in this metric since 2012, according to data from Banxico. Though Western Union said in its latest earnings that the remittances situation was improving, the January-September figures for 2025 are significantly lower than 2024.

During its Q3 earnings call, Western Union noted “significant declines” to Mexico, El Salvador, Peru and Ecuador, as well as flat to negative change in corridors including the Philippines, Jamaica, Guatemala and Colombia.

Earlier this year, the company acquired Intermex, the LatAm-focused remittances provider that had seen quarterly decline for the four quarters leading up to Q2 2025 before being acquired. A big part of the reason for Intermex’s decline and subsequent share price fall was a continued decrease in cash-based remittances from US to LatAm.

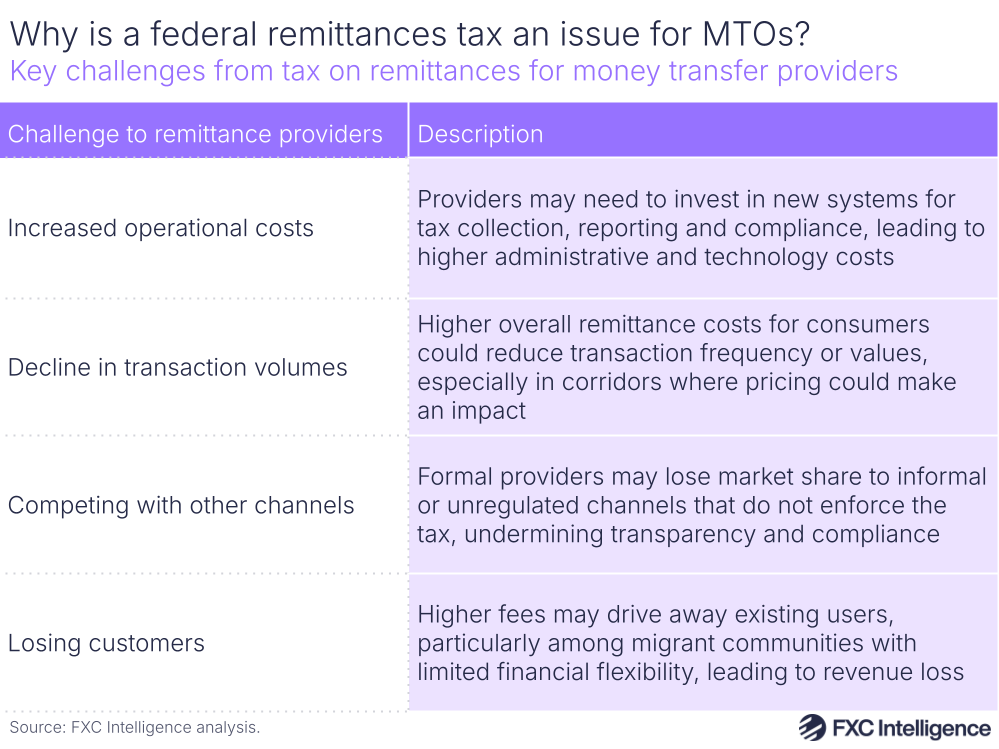

This region could see further change as a result of the US government’s incoming remittance regulations, introduced under its One Big Beautiful Bill act, under which a 1% tax will be applied to remittances from the US sent in cash. This could lead to a systematic shift in how consumer remittances are sent, with many favouring digital payment methods or some potentially shifting to other channels.

Digital drives money transfers

Movement towards digital transfers – apps, mobile wallets and online platforms – has persisted in 2025, with consumers increasingly wanting to send and receive money quickly.

On a wider level, this is aligning with a greater move towards digital financial inclusion globally. As per Global Findex report figures published in 2025, the share of people who owned a bank account in 2024 was 79%, up from 62% in 2014. Furthermore, 15% of adults worldwide now have a mobile money account, with particularly strong adoption in Sub-Saharan Africa and Latin America and the Caribbean. In Sub-Saharan Africa, 40% of adults had a mobile money account as of 2024, up from 11% in 2014, while for Latin America and the Caribbean, adoption rose from 2% in 2014 to 37% in 2024.

Alongside growing account ownership, digital payments are on the rise, with the share of adults in developing economies who make and receive digital payments nearly doubling – from 34% in 2014 to 62% in 2024.

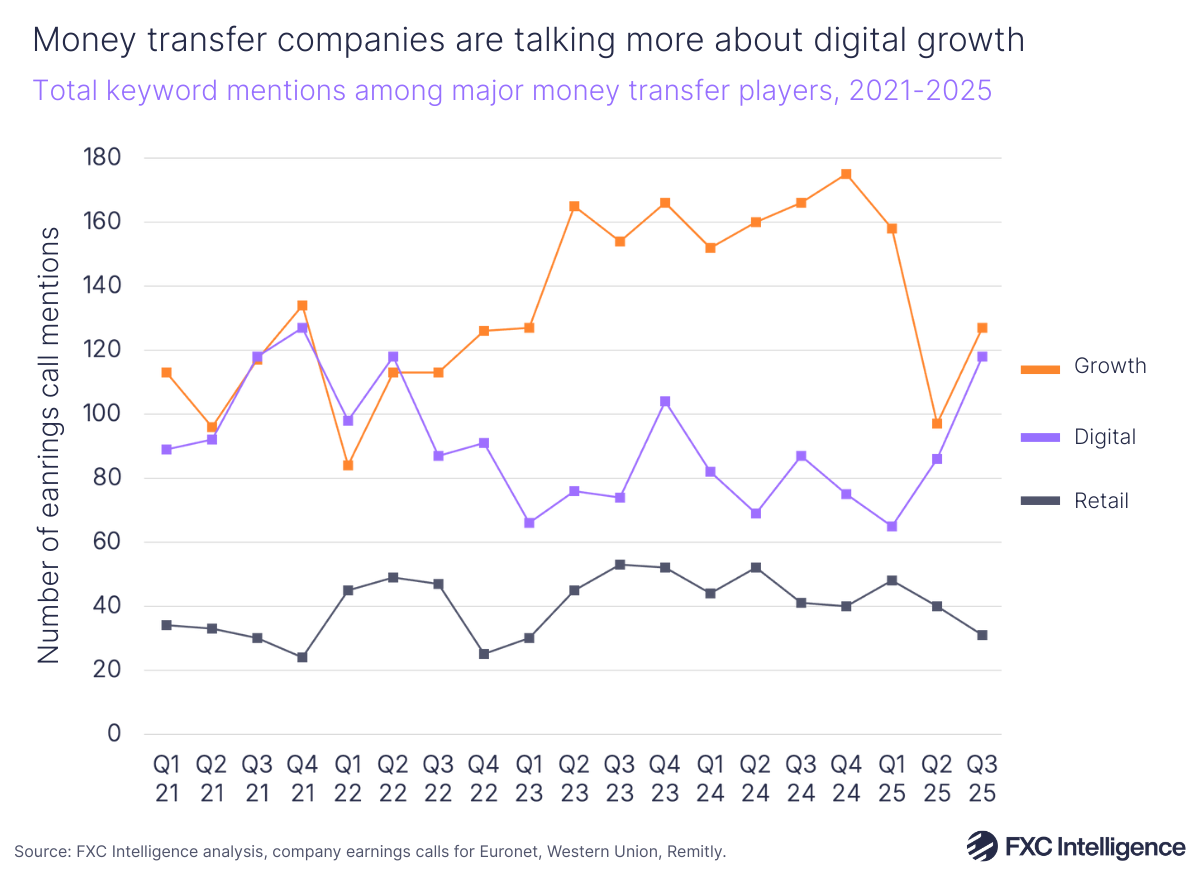

Amid macro challenges, public players in the space are continuing to note the significant impact that digital is having on their revenues. This is shown by companies like Remitly and Wise rising faster than the broader market, though the digital shift is being most aptly shown by the largest incumbent player – Western Union.

While Western Union’s number of transactions declined by 3% for the second quarter in a row in Q3 2025, its branded digital revenues rose in the mid-single-digits or better for the eighth consecutive quarter. The company’s efforts to boost its digital network are paying off, and as we saw in its investor day in November it remains fully focused on using its retail network to help catalyse growth of its digital services.

Separately, Euronet said that direct-to-consumer digital transactions accounted for 16% of its total money transactions in Q3 2025, but eventually it wants to grow digital transactions so they account for 30-35% of its transactions. In other words, major cash and over the counter providers are increasingly looking to serve digital needs in years to come.

Further backing this, digital continues to crop up more and more in earnings calls versus retail. Across the Q3 2025 earnings calls for Western Union, Remitly and Euronet, “digital” was mentioned 118 times, versus 31 for “retail”.

Pricing pressure continues to be key sticking point for money transfers

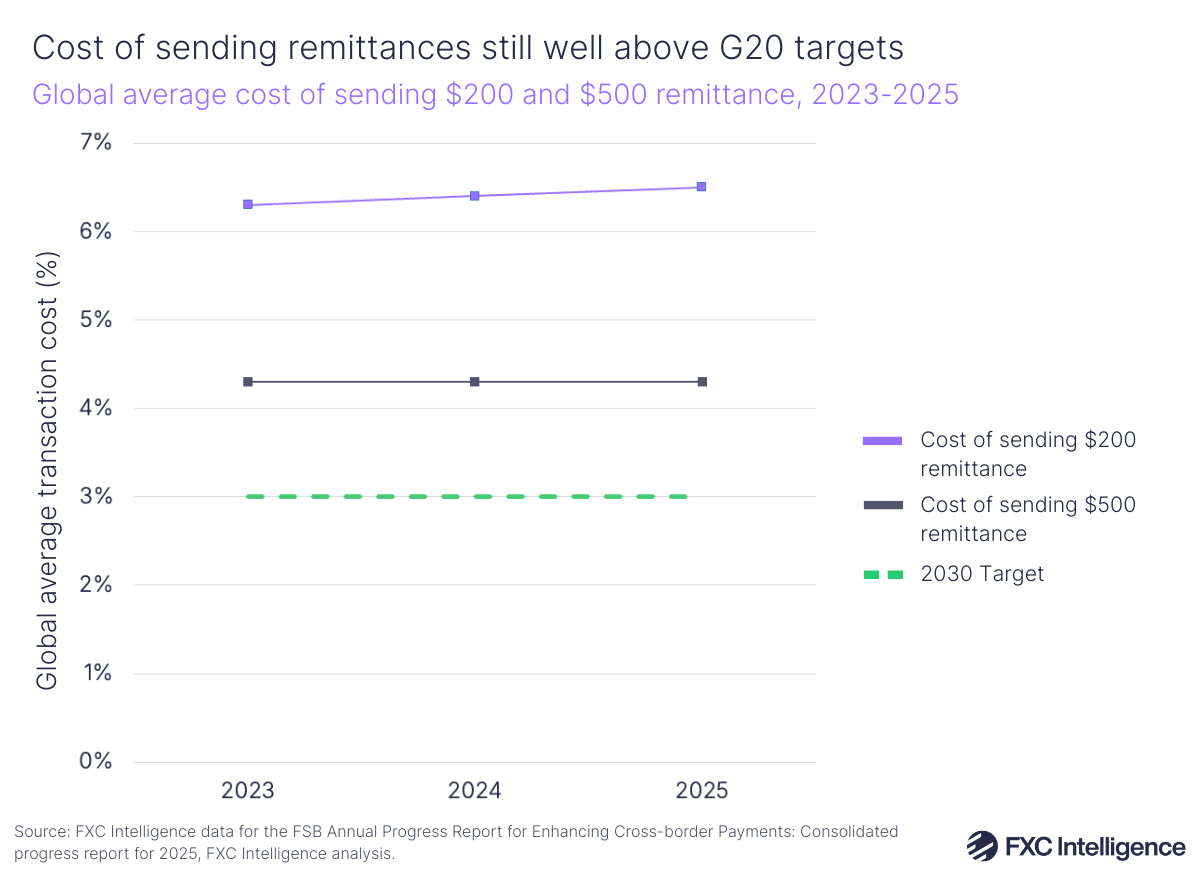

Pricing remains a key driver for competition in the money transfers space, both in remittances and higher–value money transfer sends. However, recent data from the FSB’s Annual Progress Report for Enhancing Cross-border Payments: Consolidated progress report for 2025 has shown that the industry is still far from achieving some of its goals in this area.

Under targets aligned with UN Sustainable Development Goals, the G20 is aiming to reduce the global average cost of a $200 remittance to be no more than 3% by 2030, while ensuring that no remittance corridor has an average cost above 5%. The FSB defines remittances specifically as low-value, high-volume payments primarily to receivers in emerging markets and developing economies.

As per the FSB report, the cost of sending remittances remained almost unchanged throughout 2023-25, with the global average cost of sending $200 actually increasing from 6.4% in 2024 to 6.5% in 2025, while the cost of sending $500 remained flat at 4.3%. This is based on data from the World Bank’s Remittance Prices Worldwide (RPW) dataset.

Although the average cost of the three cheapest qualifying services for each corridor remained relatively stable in 2025, the share of corridors with averages above 5% increased for sending both $200 and $500. This shows that pricing and competition are still crucially important in the space and will remain a key trend for the industry going forward.

The report presented several other findings around key influencing factors for pricing. Costs across all provider types (spanning banks, money transfer operators, post offices and mobile operators) increased from 2024, with the exception of money transfer operators. Mobile money was the lowest-cost instrument for funding remittances, while debit cards are the most affordable means of disbursing them.

Taken together, the pricing trends in the G20’s recent report often align with the trend towards digital. For example, analysis of a remittance corridor in sub-Saharan Africa found that higher costs were being driven by the administrative burdens of handling cash; taxes on digital financial transactions; weak competition amongst banks, many of which aren’t as interested in serving remittances; and a lack of direct access to payment systems from PSPs, which have to seek out more expensive financial arrangements to enable services as a result.

Despite little movement on pricing, the FSB report did note that the speed of remittances has improved globally, noting particular improvements in remittances being sent to the Middle East and North Africa, as well as Latin America and the Caribbean. In the last of these regions, for example, 60.6% of services delivered funds within one hour in 2025 (based on RPW data as of Q1 2025) an 8 percentage point improvement on Q1 2024.

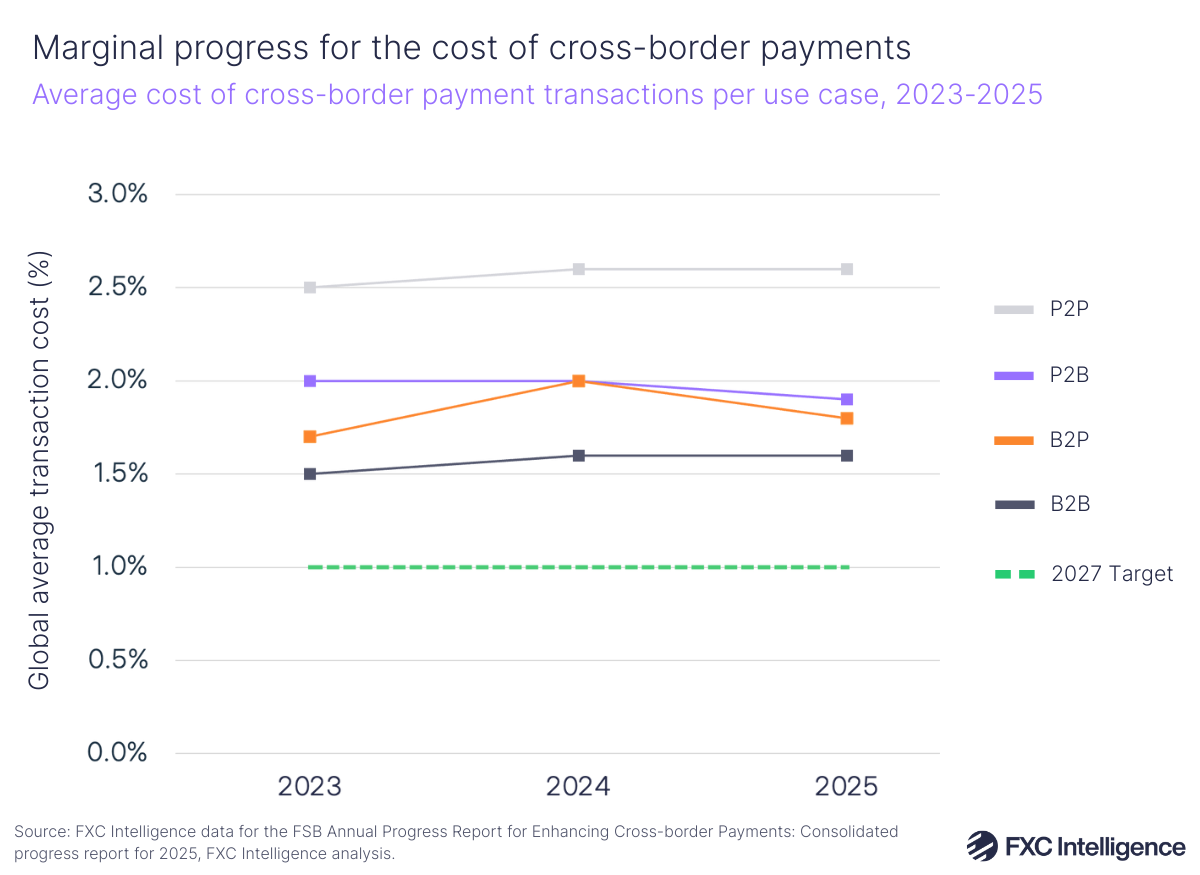

P2P payments are continuing to see slow progress on pricing, though these are defined slightly differently to consumer remittances in the FSB’s report and are tracked in relation to a different pricing target. In particular, the FSB’s P2P payments category is more digital-led and focuses more on use cases requiring higher send amounts, such as direct payments to other individuals for services or goods made online.

The G20 has set a target to see global average retail cross-border payments costs of no more than 1% by the end of 2027. In its 2025 report, the FSB defines retail payments as payments with a value of less than $100,000, not including remittances, and demarcates different single transfer amounts for each use case: $20,000 for B2B payments, $5,000 for B2P, $1,000 for P2P and $100 for P2B.

Based on this categorisation, P2P payments remained the most expensive cross-border use case in 2025 versus P2B, B2P and B2B payments. Average global costs for P2P payments of $1,000 held at 2.6% (a figure that is yet to drop below levels seen in 2023).

Sub-Saharan Africa was the most expensive region to send money from, with a weighted average total cost slightly above 4% and a YoY increase of 0.23 percentage points despite ongoing efforts to reduce cross-border payment costs. In contrast, Europe and Central Asia was the least expensive region for outbound retail payments, with the average cost of sending a $1,000 P2P transfer declining by 0.04 percentage points to 1.93%.

The crux of this is that pricing remains a competitive battleground for payments – particularly in developing regions, many of which contain key markets for remittances. However, progress towards reducing costs remains slow. While digitalisation offers opportunities to reduce costs, there are still major system hurdles to overcome.

Companies diversify offerings beyond transfers

This year, we’ve seen money transfer providers continue to widen their offering beyond remittances. Under its ‘Beyond’ strategy, launched this year, Western Union is aiming to frontload its consumer services segment more, including bill payments, wallets, lending and travel money, as it aims to expand away from retail remittances (though these will still remain core to its revenue mix).

Wise is another key example, having started out as a consumer money transfer company and now continuing to focus more on servicing SMEs and multicurrency accounts. It continues to grow its Wise Platform, through which it has turned its global money transfer infrastructure into a product to sell to banks, fintechs and large enterprises, and which it says could account for 50% of its volume in the long term.

This year, Remitly – another consumer-focused provider – also introduced membership service Remitly One in the US, enhancing its transfer offering with send now, pay later options. It also introduced Remitly Business to target transfers for small businesses, though CEO Matt Oppenheimer told us recently that this remains focused on micro businesses rather than medium and large-sized corporates.

Revolut, meanwhile, continues to apply for banking licences, having been granted a licence in the European Economic Area and more recently Mexico, while its UK licence is currently being delayed by various regulatory hurdles. These licences allow the company to accept deposits directly and use them in banking operations, expanding its role as a mobile bank and opening up new revenue streams.

Stablecoins power wallets, treasury and on/off-ramps

Stripe’s $1.1bn acquisition of Bridge earlier this year, as well as the US’s introduction of the GENIUS Act, have both ramped up interest in stablecoins from the cross-border payments space.

The hype around the technology for faster and less-costly cross-border settlement has been well reported (read our full industry primer on stablecoins). Within consumer money transfers the focus has been on a few key areas: enabling customers to hold and transfer coins across borders; adding on and off-ramping to networks; and speeding up treasury operations to move the company’s money around the world.

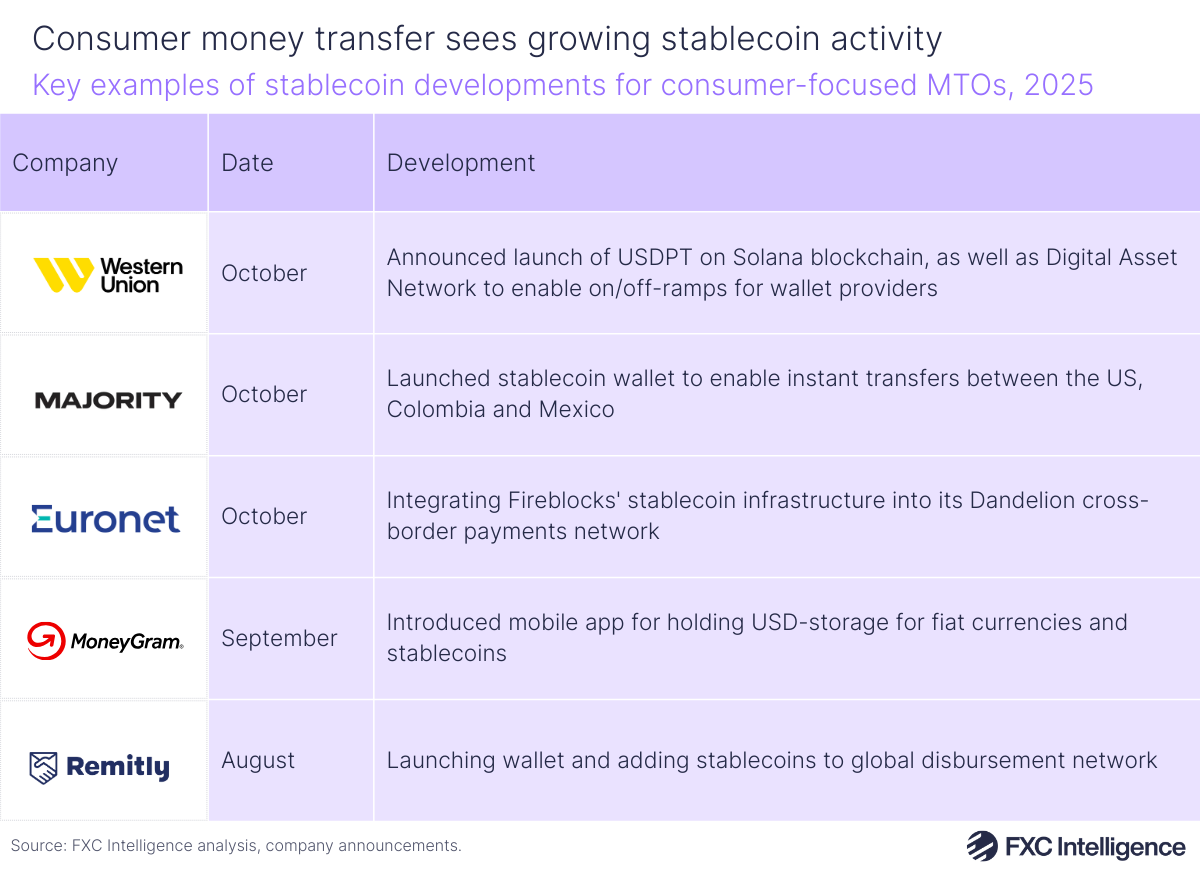

This year has seen particularly significant developments from consumer money transfers. For example, Western Union is launching its own stablecoin on the USDPT, a new stablecoin built on Solana. Remitly has launched a new wallet to support holding of fiat and stablecoins, and also adding stablecoin rails to its global disbursement network through a partnership with Bridge.

Digital bank Majority also launched its stablecoin transfer feature, enabling free and instant fund transfers, while MoneyGram, has launched a next-gen mobile app designed to work with fiat currencies and stablecoins. Euronet is planning to enable its first stablecoin-use cases in Q1 2026, including enabling cross-border transfers and consumer cash-out functionality in selected markets.

Aside from allowing customers to transfer and receive stablecoins, money transfer providers are also aiming to see benefits from stablecoins behind the scenes – for example, both Western Union and Euronet aim to use stablecoins within its treasury operations to move funds between accounts and jurisdictions faster and more efficiently.

Is AI making in-roads in money transfers?

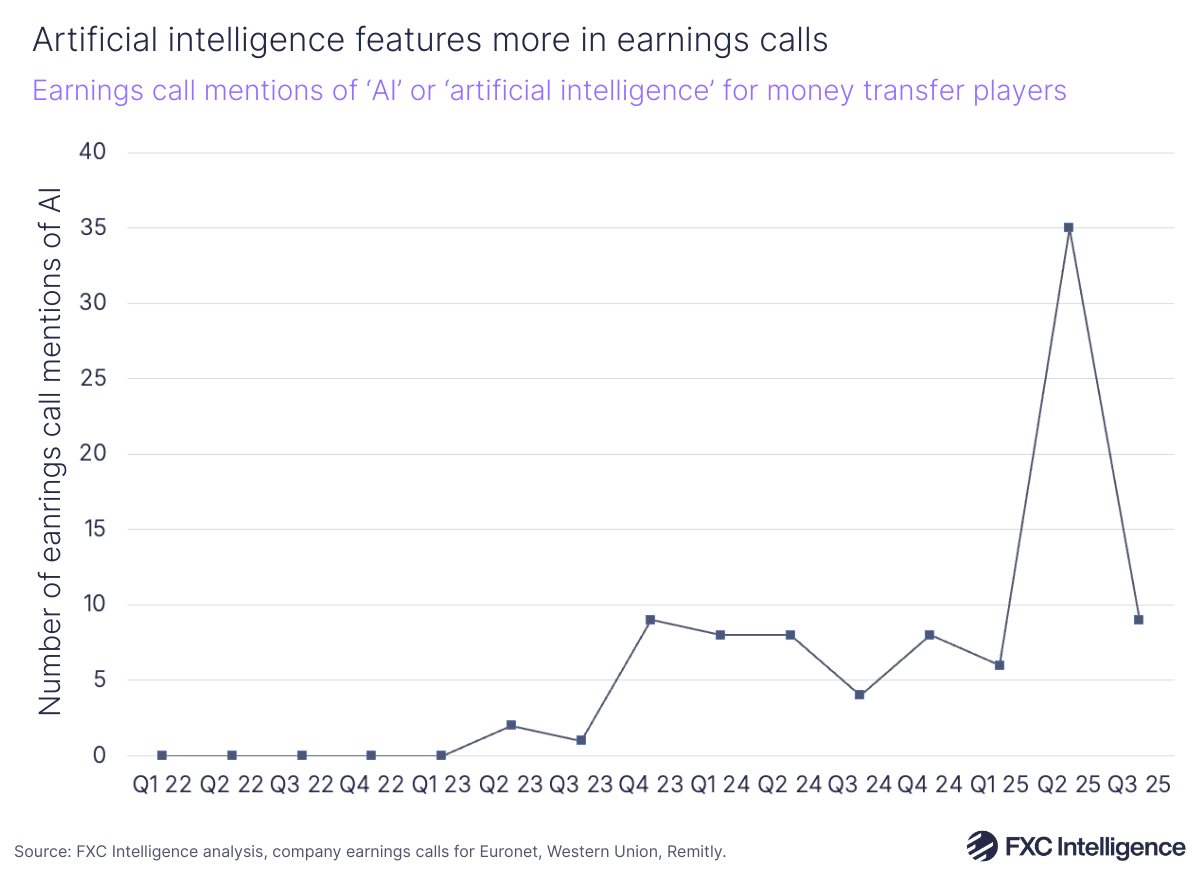

One trend that hasn’t seen as much traction on the consumer side has been artificial intelligence (AI), though this saw an uptick in 2025. In earnings calls for public money transfer providers (Western Union, Euronet, Remitly), AI was mentioned 50 times in 2025 versus 28 times in 2024.

For consumer money transfer providers, AI is having particular benefits in customer service, driving efficiency but also contributing to operational strategy. Remitly has implemented a virtual AI agent to improve customer service, as well as improving productivity across its marketing and engineering teams.

Meanwhile, Euronet is also harnessing AI in customer service and using it as a “strategic enabler” across its company, while Western Union is using AI models as part of its risk evaluation process.

Currently, the role of AI in consumer money transfers appears to be in driving productivity and enhancing customer service, rather than radically overhauling how the industry works. That being said, it is notable that companies are actively mentioning it more in their earnings in 2025.

Where will the consumer money transfers space go in 2026?

Next year, money transfers will increasingly move into the digital space as wallets continue to grow and major incumbent money transfer providers focus further on serving digitally originated transfers – though financial inclusion challenges in some regions will mean that cash remains important.

Stablecoins will continue to shift from theory to practice, and many companies could see the various plans they have put into action bear fruit. This includes forming partnerships and integrating stablecoin payments infrastructure to enable faster movement of treasury funds; supporting the transmission of funds across borders; and enabling on-ramping and off-ramping of stablecoins to wallets globally.

Depending on how new technologies such as stablecoins are adopted, these could generate more returns and efficiency gains for money transfer operators, which may contribute to more competitive pricing on some of the world’s most competitive corridors. As digital challengers continue to mature and add new services, consumer money transfers and remittances are becoming part of a larger financial scheme for these businesses, and we could see more bank licences being sought out and approved as these players seek to tap into a much wider cross-border payments TAM.