The World Bank has released its Global Findex report for 2025, giving a wealth of insights into account ownership and remittances globally. Below, we dig into the key insights from the report for cross-border payments providers.

Last week, the World Bank released its Global Findex Database for 2025, giving a comprehensive snapshot into how consumers around the world are using financial services.

Based on survey data covering more than 140,000 people in 141 economies, the report gives an update on everything from account ownership to mobile money use and digital payments, including some insights that are particularly relevant for cross-border payments providers operating in developing markets. Here are some of those insights below.

Populations in some developing markets rely more on remittances

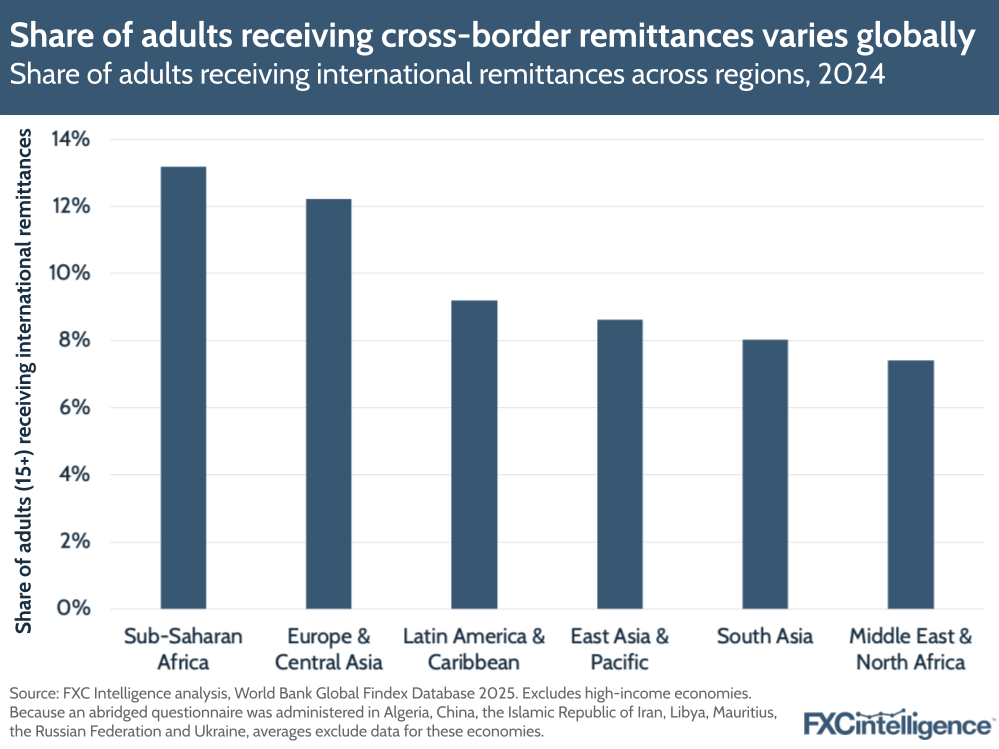

Though it has been historically focused on domestic remittances, the 2025 Global Findex report for the first time contains insights on the share of adults receiving international remittances. According to survey data, the share of adults who receive international remittances is less than 10% globally, though in 60 low- and middle-income countries (LMICs) included in the study 10% or more of adults receive international remittances.

Remittances figures from the study highlighted that a significant number of Sub-Saharan African populations continue to rely on remittances. Across LMICs included in the Global Findex 2025 (i.e. excluding high-income countries), 13% of adults in Sub-Saharan African countries received remittances in 2024, with this figure dropping to 12% of adults for Europe and Central Asia, 9% for both Latin America & Caribbean and East Asia & Pacific, 8% for South Asia and 7% for Middle East & North Africa.

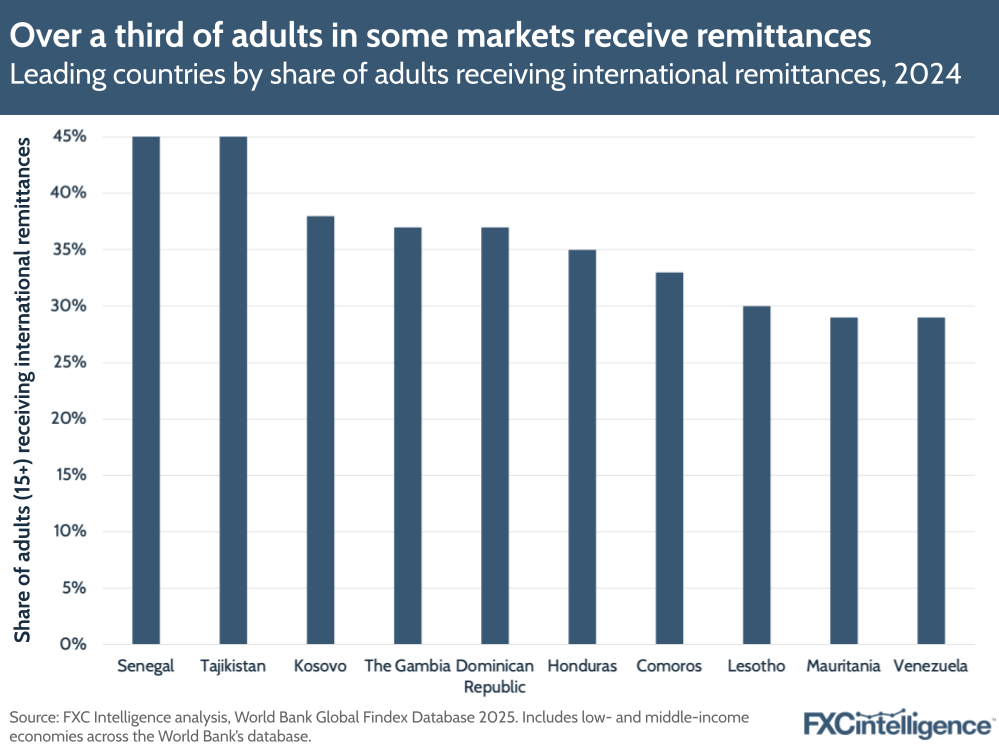

On an individual country basis, the figures varied widely across the study. The economies with the highest reported share of adults receiving international remittances were Senegal and Tajikistan, which both had 45% of adults report receiving international remittances, followed by Kosovo (38% of adults) and the Gambia (37%). Latin America was also represented across the economies with the highest shares, with 37% of adults in the Dominican Republic receiving remittances and 35% receiving them in Honduras.

Many of the countries with a high share of remittance receivers are small in terms of overall population but have large migrant diasporas. Across some of the world’s biggest remittance receivers in terms of volume, the share of adults receiving international remittances was lower, with 9% of adults in Mexico receiving international remittances, 8% in India and 6% in Pakistan. However, in terms of the overall population size of these countries, these figures still highlight a substantial market for remittances – for example, 8% of India’s current population (1.4 billion) would amount to roughly 112 million people.

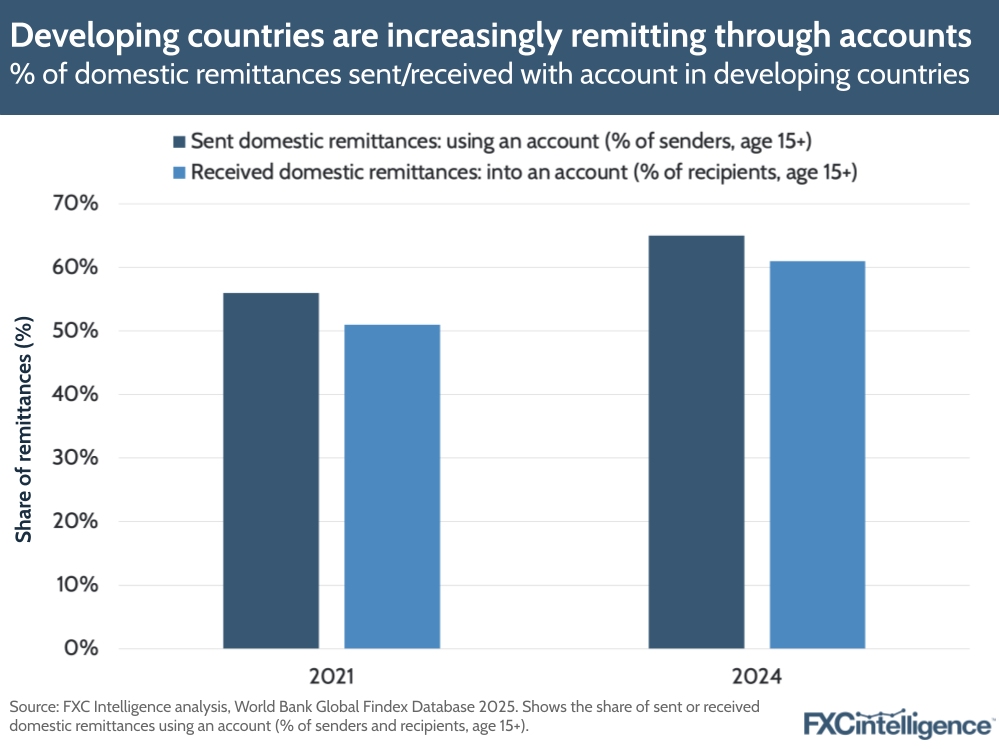

Across developing countries, the share of domestic remittances sent or received by adults using an account has grown from 36% in 2014 to 62% in 2024 (the year referenced in the 2025 report). However there also continues to be a gap between the share of remitters sending using an account in 2024 (65%) versus the number receiving (61%).

This shows that on a local level, the use case for digital in remittances is steadily increasing in these countries. With more people in developing economies growing their use of accounts to send money locally, the opportunity is also likely growing in these regions for digital and account-based cross-border remittances.

Aside from this, having an account to receive payments can increase the volume and frequency of remittances from family members and friends, according to a World Bank research paper cited by the Findex report.

Global account ownership continues to rise

Globally, the number of people who do not have access to a financial account has fallen from 2.5 billion in 2011 to 1.3 billion in 2024, though the rate at which this figure is falling has slowed over time. The biggest barriers to account ownership include not having enough money to open an account; fees for financial services; and the fact that many people are continuing to use a family member’s account. There is also still a notable gender gap in payments too, with adults without accounts in LMICs disproportionately being women and poor adults.

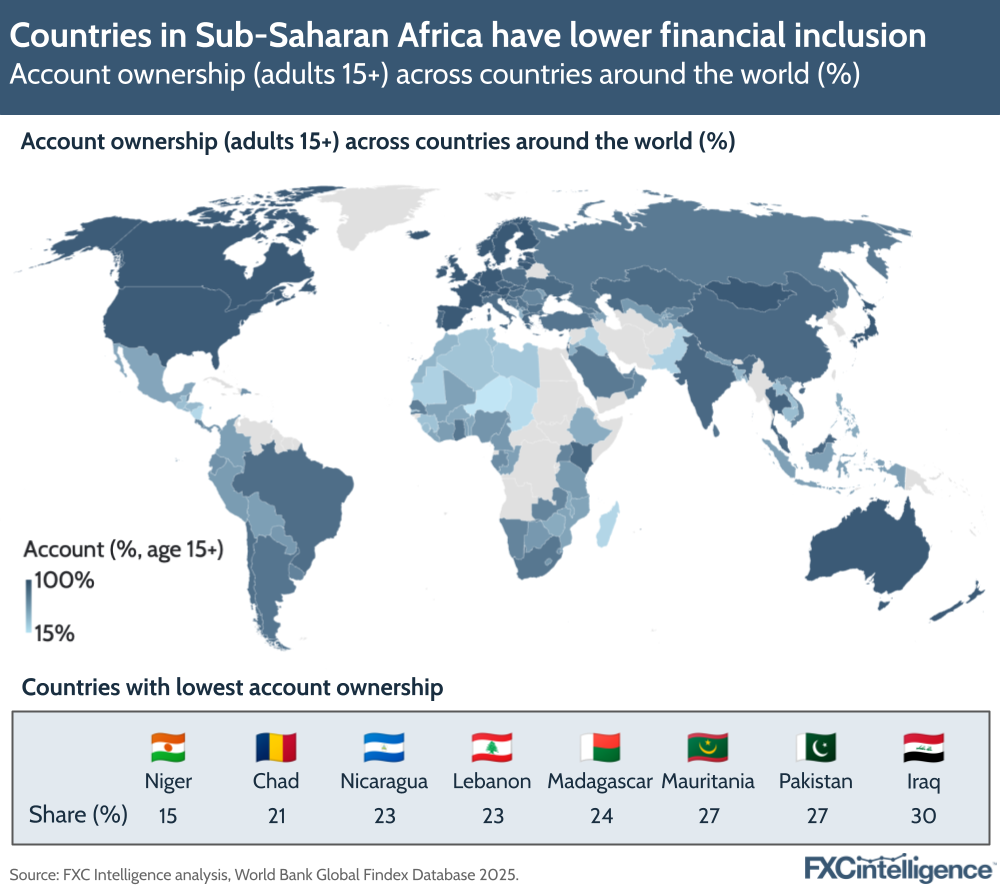

The share of people who owned an account in 2024 stood at 79% worldwide, up from 51% in 2011 and 74% in 2021. High-income countries continued to drive this figure overall, with 95% account adoption in 2024 versus 87% in 2011, though the share has actually gone down slightly from 96% in 2024. However, a significant change has come from developing economies, which have seen account adoption rise from 42% in 2011 to 75% in 2024.

On one side of the spectrum, high-income countries report near universal account coverage, with Iceland, Finland and Austria all seeing 100% account ownership. However, on the other end, a number of LMICs still face significant gaps when it comes to financial inclusion. Countries such as Niger (15%), Chad (21%), Nicaragua (23%) and Lebanon (23%) exhibit low account penetration, presenting both a challenge and opportunity for remittance providers.

A significant number of people remain unbanked globally, and many of them live in key remittance-receiving countries. More than 650 million adults without accounts (or 53% of all adults without accounts) currently reside in Bangladesh, China, Egypt, India, Indonesia, Mexico and Nigeria and Pakistan. Several of these are key remittance locations, with many people still relying on cash-based transfers, showing the need for providers to continue to blend digital and cash options to serve these areas effectively.

Mobile money account ownership outpacing bank account ownership in some countries

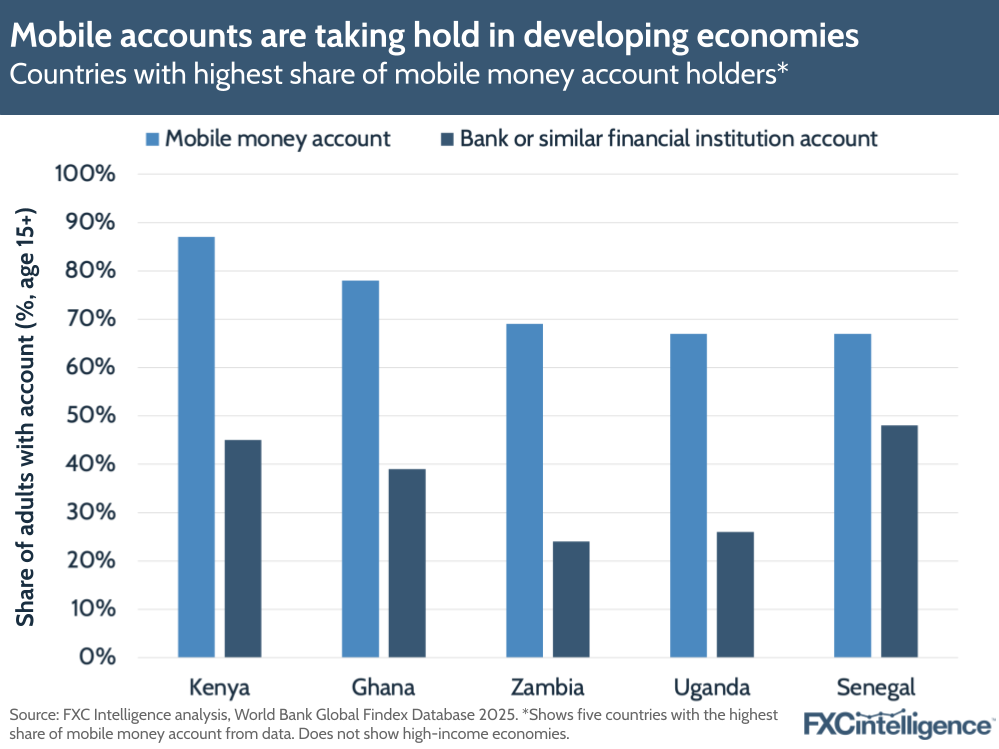

A key driver for rising account ownership overall has been the rise of mobile money, with 15% of all adults worldwide having a mobile money account, up from 2% in 2014. Over half of all adults in LMICs now make payments from an account using a mobile phone or card. There’s been particular growth in this area in Sub-Saharan Africa, where the share of mobile money account owners has grown from 11% in 2014 to 40% in 2024 and actually exceeded the share of bank account ownership (38%). Latin America, meanwhile, saw its share of mobile money account ownership rise from 2% to 37%.

The countries with the highest share of mobile money account ownership (excluding high income countries) include Kenya (87%), Ghana (78%), Zambia (69%), Uganda (68%) and Senegal (67%). Mobile money account ownership has grown significantly across these countries since 2014, when the World Bank first began collecting this data; for Senegal, as an example, mobile money account ownership has risen from just 6% in 2014.

Mobile accounts continue to be more dominant in lower-income countries, where traditional bank penetration is lower than in developed economies. For payment providers, this shows that mobile money rails remain extremely important for these regions, while also reflecting the continued need for cash-based agents.

However, the report also details that the opportunity to target mobile users with financial services persists. For example, there are currently 80 million adults in Sub-Saharan Africa who own a mobile phone, basic ID and a SIM card – the three digital prerequisites the World Bank identifies for account ownership – but still do not have a financial account of their own.

Digital payments continue to rise

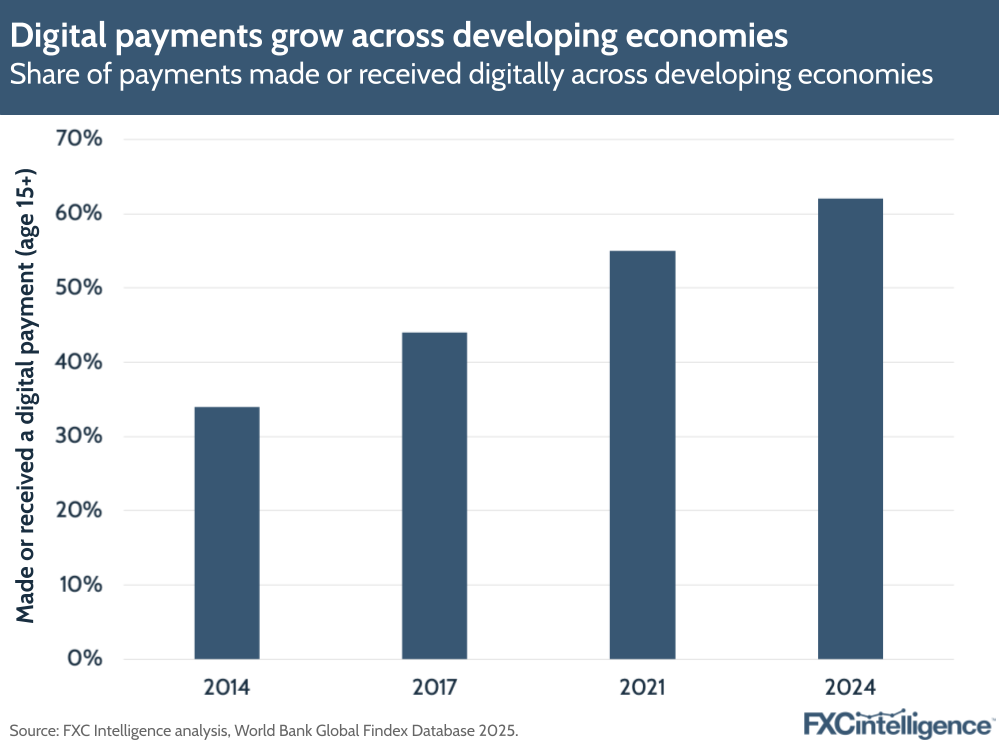

The Global Findex 2025 sees a digital payment as any payment sent directly from or received directly in an account at a bank or similar financial institution, or using a mobile money account.

As account ownership has grown, the share of adults in developing economies who make and receive digital payments has nearly doubled from 34% in 2014 to 62% in 2024. There have also been significant increases in digital merchant payment adoption across many countries, with 36% of adults in LMICs purchasing goods online in 2024. The growing popularity of digital payments highlights wider trends towards digitalisation in the industry, but also that the demands for these regions when it comes to cross-border ecommerce is likely continuing to grow.

While the Global Findex report points to progress in some areas, it continues to show that the world is not an equal place when it comes to financial inclusion. Growth in digital services is highlighting demand for seamless payments, yet significant barriers remain in some regions to onboard services. For cross-border payments, the opportunity remains in expanding access to underserved users while reflecting a growing demand for digital payments.