Western Union has held its investor day for 2025, in which the company outlined a three-year strategy to drive FY revenues to around $5bn at the midpoint in 2028, as well as giving an update on its recently announced stablecoin announcements.

Western Union’s 2025 investor day signalled a significant pivot for the world’s biggest consumer remittances provider.

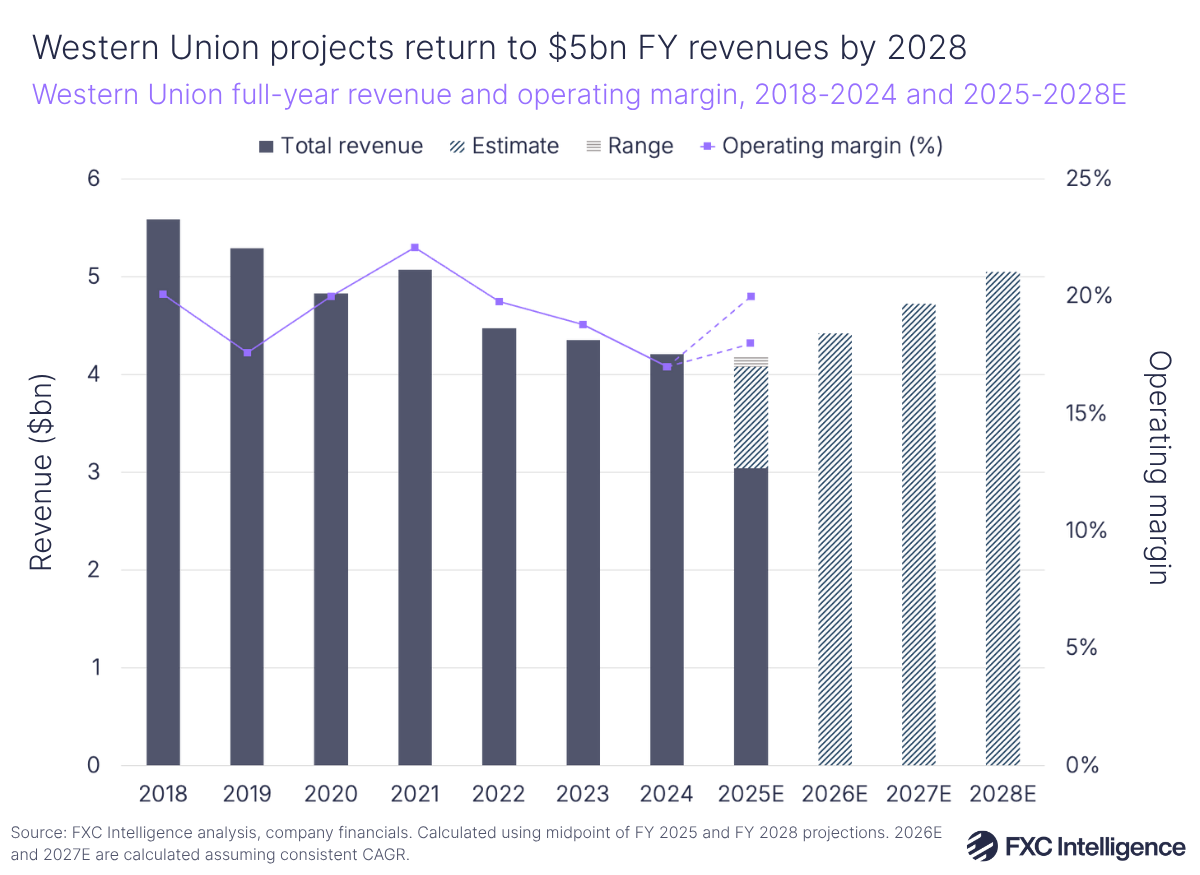

Following on from its Evolve strategy, laid out in 2022, the company has now launched Beyond – a three-year plan to drive its annual revenues to around $5bn at the midpoint by 2028 and reposition Western Union as a digital-first provider of remittances and other financial services.

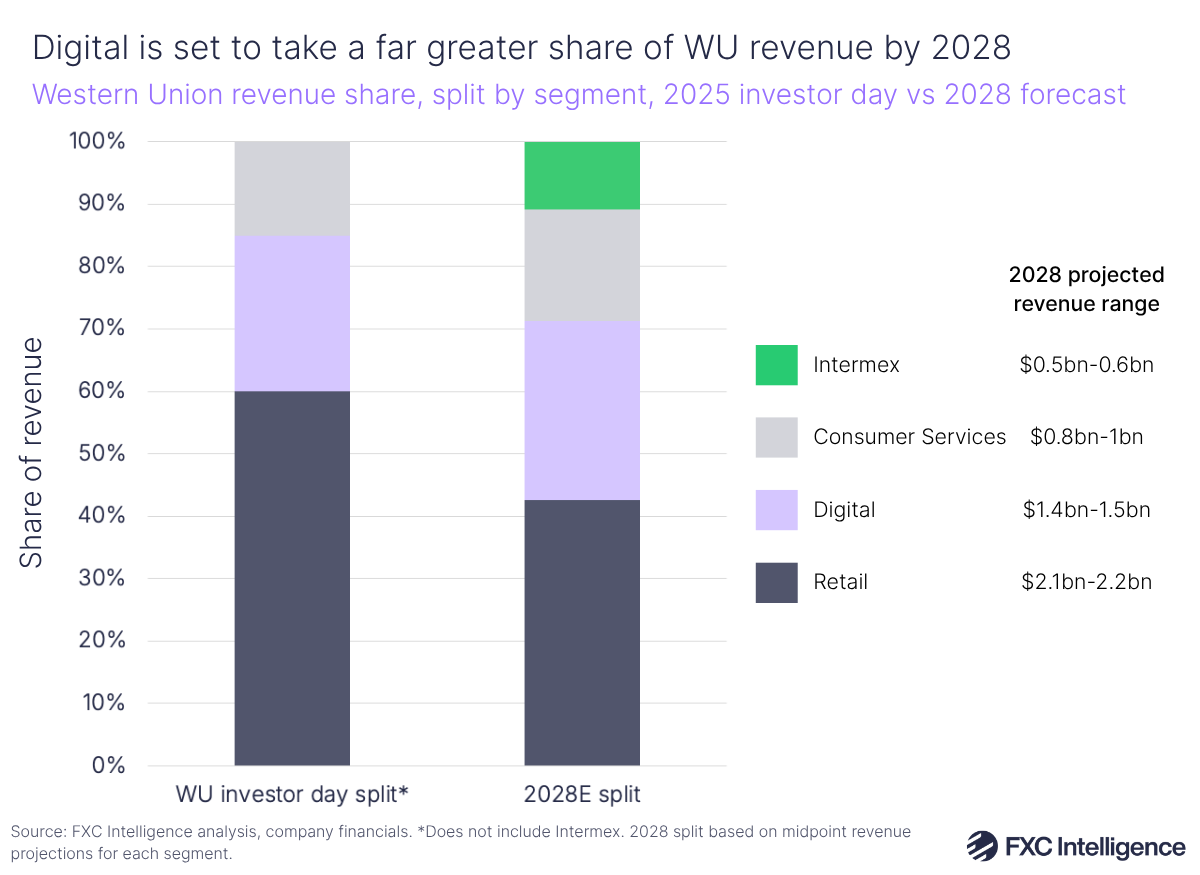

Central to this strategy is Western Union’s potential to use its retail network to catalyse growth of its digital services, spanning online and app-based transfers; digital wallets; and its Consumer Services segment. The latter of these – which includes online bill payments, travel money, insurance and prepaid cards – accounted for just 6% of the company’s revenue in 2022. It now makes up 15% of Western Union’s revenue and has grown by 80% over the last three years, with Western Union now pitching it as a potential $1bn business by 2028.

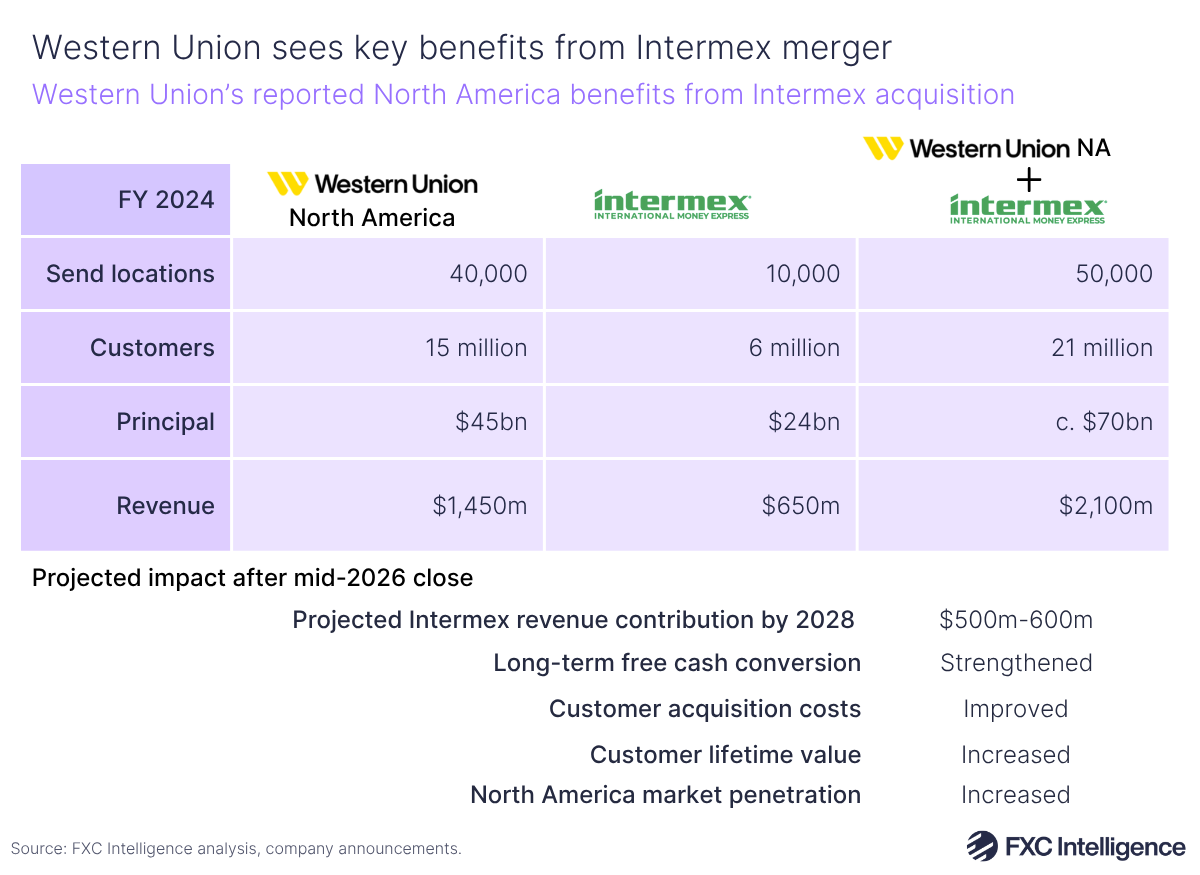

Based on its 2028 projections for each segment, the company expects to see Retail remittances account for between $2.1bn and $2.2bn of revenue, with Digital contributing $1.4bn-1.5bn, Consumer Services seeing $800m-1bn and Intermex accounting for $500m-600m.

Western Union also gave an update on its recently announced stablecoin USDPT and Digital Assets Network, through which it aims to allow customers to convert between stablecoins and fiat initially across high-volume corridors from H1 2026. It also sees a significant boost from its acquisition of LatAm-focused remittances player Intermex, adding to its other brands – P2P payments wallet Vigo in the US, UK travel money provider Eurochange and Argentinian wallet Pago Facil – and bolstering its US-LatAm money transfer network.

Below, we explore the key highlights from Western Union’s recent Q3 results and investor day, which FXC Intelligence CEO Daniel Webber attended, including the company’s digital strategy, stablecoins, network expansion as well as its Intermex acquisition.

Western Union’s Q3 2025 highlights

Released in late October, Western Union’s Q3 2025 earnings set the scene for its strategy going forward, in which it hopes to unlock greater growth and push beyond the retail remittances network.

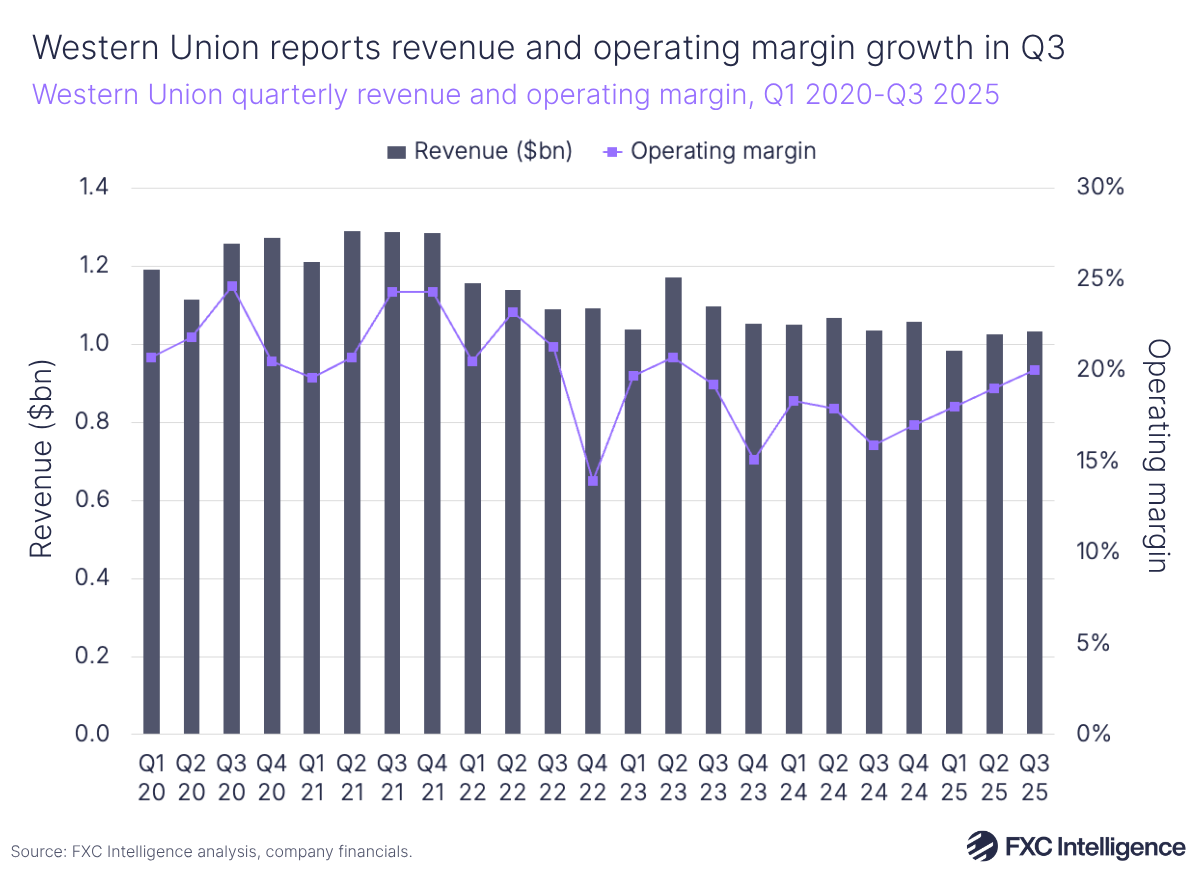

In its most recent earnings (Q3 2025), Western Union’s revenue remained flat on the previous year, at $1.03bn, with adjusted revenue excluding Iraq at -1% YoY. The company’s operating margin rose to 20% on a GAAP basis, up from 16% in Q3 2024, which the company attributed to its continued discipline around costs.

The company reaffirmed its full-year outlook for 2025, with GAAP revenue expected to be between $4.1bn and $4.2bn. Adjusted revenue (i.e. excluding the impact of currency translation, as well as Argentina hyperinflation) is expected to grow to $4.035bn-4.135bn, giving an adjusted margin of 19-21%.

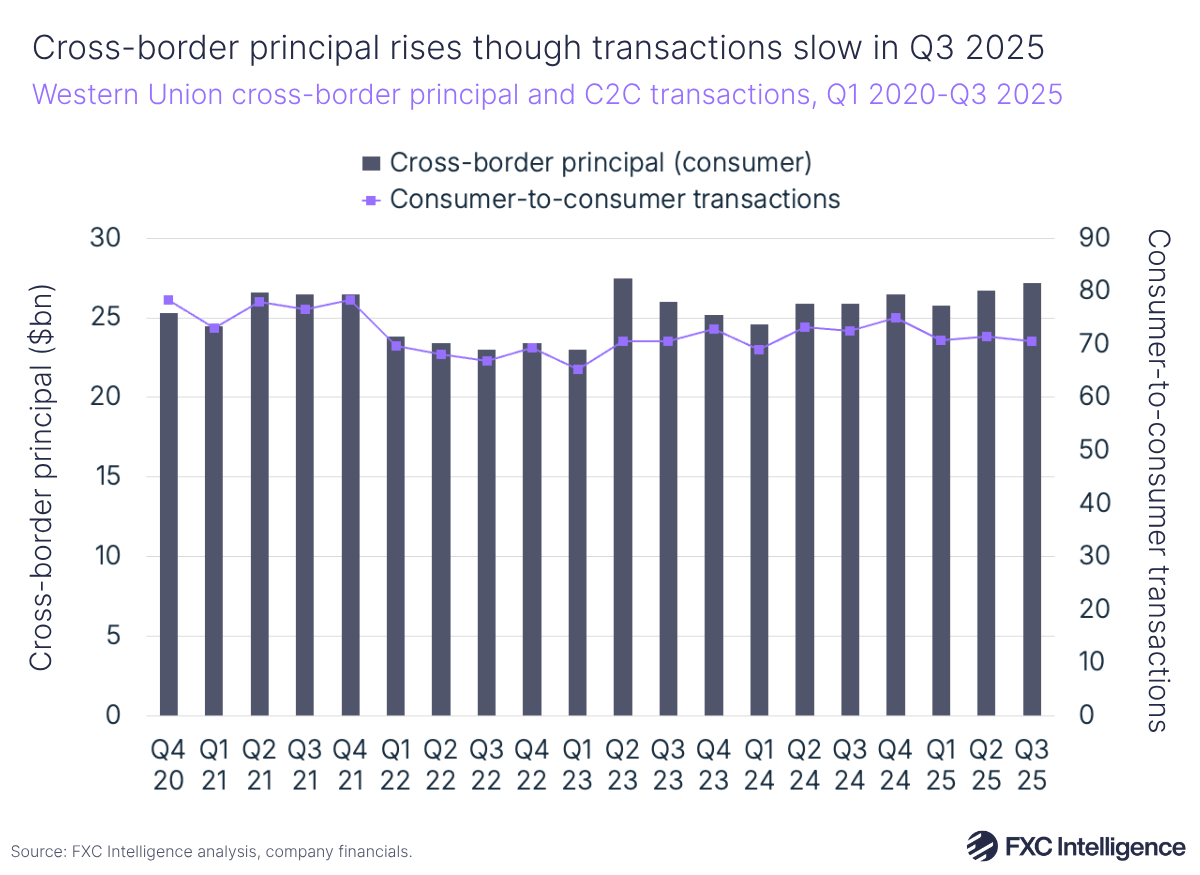

Western Union continued to see softness in its consumer money transfer (CMT) revenues during the quarter, which fell by 6% to $878m, while transactions declined by 3% to 71 million. However, the company continued to see its efforts rewarded on digital transformation, with branded digital revenues rising 7% and branded digital transactions growing by 12% during Q3 2025.

On the other end of the spectrum, Consumer Services revenue continued to see rapid growth, at 49% YoY to $154m – it now makes up around 15% of Western Union’s revenue, up from 10% in Q3 24. The company’s share price rose as a result of it beating market analyst estimates.

Western Union’s Beyond strategy: Growth projections to 2028

2025 saw the close of Western Union’s Evolve strategy, with the company saying it had achieved its financial outlook in “absolute terms”, though macroeconomic impacts – particularly in US retail – affected the company’s expectation of 2% revenue growth to 2025. Having said this, CFO Matthew Cagwin added that the company had not expected positive revenue growth until 2025 due to the “complexities of [Western Union]’s transformation”.

Western Union is now launching Beyond, through which it aims to see revenues improve by 20% to reach a range of $4.8bn-5.3bn (or $5bn at the midpoint) in 2028. Based on our calculations using the midpoint of Western Union’s 2025 and 2028 revenue projections, this would give the company a CAGR of 6.9% and see it return to revenue levels it previously saw in 2021.

The company noted that its outlook for the future – in particular its consumer money transfer revenues – is grounded in the expectation that remittances are resilient and continue to grow 3-4% per year.

CEO and President Devin McGranahan also spoke about how the company aims to continue work from its Evolve strategy to drive efficiency, having achieved its cost reallocation program two years early. He also said that the company has continued to scale its investment in AI and particularly generative AI, which it hopes will contribute to $150m cost savings in the next five years. This also spans areas such as account payout costs, fraud losses, productivity improvements and cost synergies associated with the company’s Intermex acquisition.

Shifting towards digital and consumer services

Across Western Union’s investor day, the word “digital” cropped up 161 times, versus 128 for “retail”. This is just one of many signals of how the company is aiming to move its retail channel into a digital-first channel.

Western Union sees its retail network as a “bridge” to its digital services. This means using its retail network as a low-cost way to acquire customers for its digital network, as well as increasingly expanding services such as bill payments, wallets, lending and travel money.

Digital services have become a bigger and bigger part of Western Union. Over the past three years, Western Union has grown its CMT business by 6%, a key part of which has been a 25% increase in branded digital customers. By introducing more competitive rates and enhancing services, the company says it has seen transactions per customer climb by around 10%, driving a 35% increase in branded digital transactions over the period.

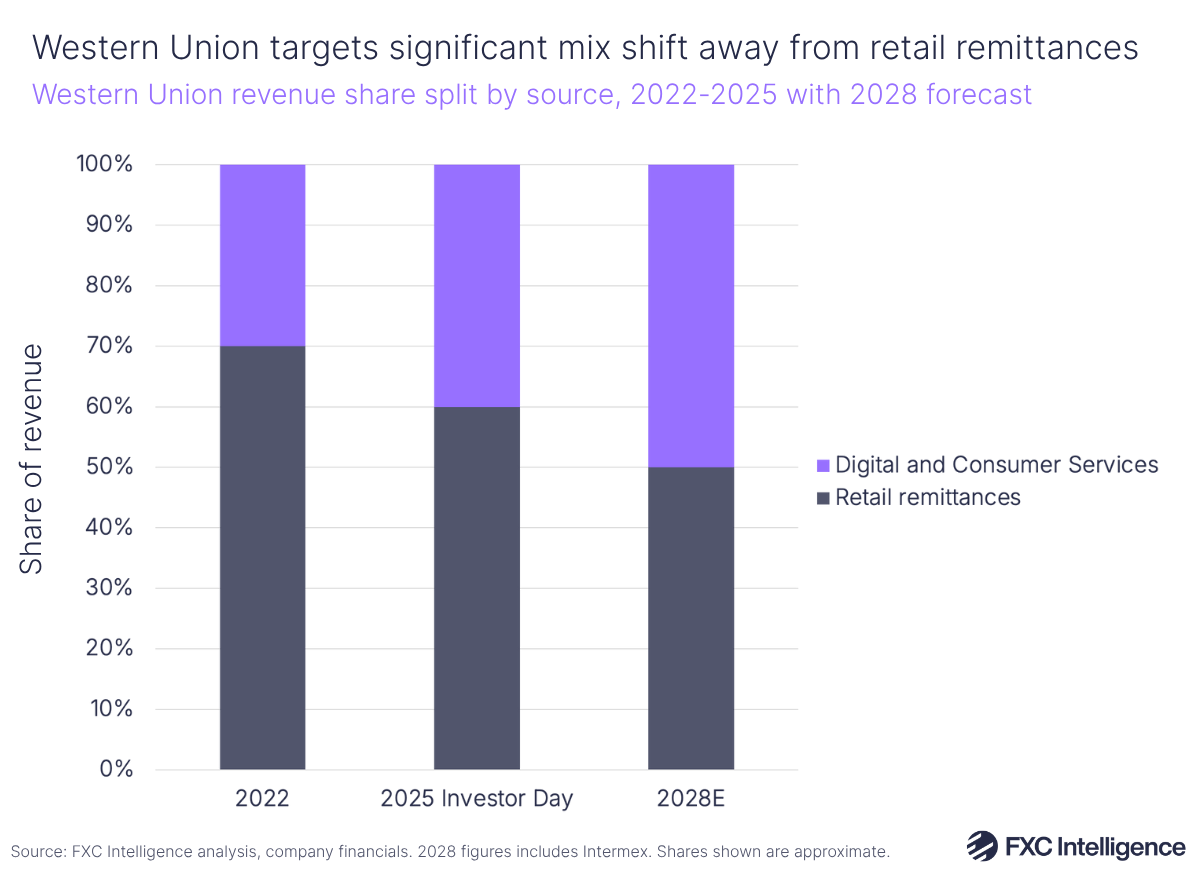

In 2022, Digital and Consumer Services accounted for around 30% of Western Union’s revenues; today this is around 40% and in 2028 the company expects that together they will account for around 50% of revenue. By comparison, Retail remittances, which today account for around 60% of revenue, are projected to only take around 50% of revenues in 2028 (including Intermex).

Assuming Western Union hits the midpoint across its full year and segment projections, Retail would still account for the highest share of revenue in 2028 at 43%, though this would be significantly lower than the 60% for FY 2025 assuming that the company’s mix as of its investor day holds true. Meanwhile, Digital would account for 29% of revenues, with Consumer Services contributing 18% and Intermex making up around 11%.

Western Union argues that strong brand recognition and trust is the key to keeping digital customer acquisition costs low – though it is also using other methods including localised marketing and precision pricing to do this. Having cut customer acquisition costs by 50% since 2022, it is targeting a digital customer acquisition cost target of less than $20, while continuing to cross-sell its services to its 80 million customer retail base and its 10 million customer digital base. The company also sees its strong retail presence as being a differentiator from other digital-only platforms that are in the money transfer space.

Notable in all this is Western Union’s growing focus on the receiver of consumer money transfers, and particularly those who receive through wallets. Not only will this allow the company to improve their relationship with the receiver and start to offer them financial services, but it also arguably improves the relationship with the sender, as it puts both the sender and receiver in the same money transfer system. “Our global platform of digital wallets integrated across our entire network will enable onboarding, payouts, digital asset off-ramps and, importantly, nonremittance financial services,” said McGranahan during the presentation. “This is what we mean by ‘powered by retail’.”

Stablecoins help drive next phase of growth

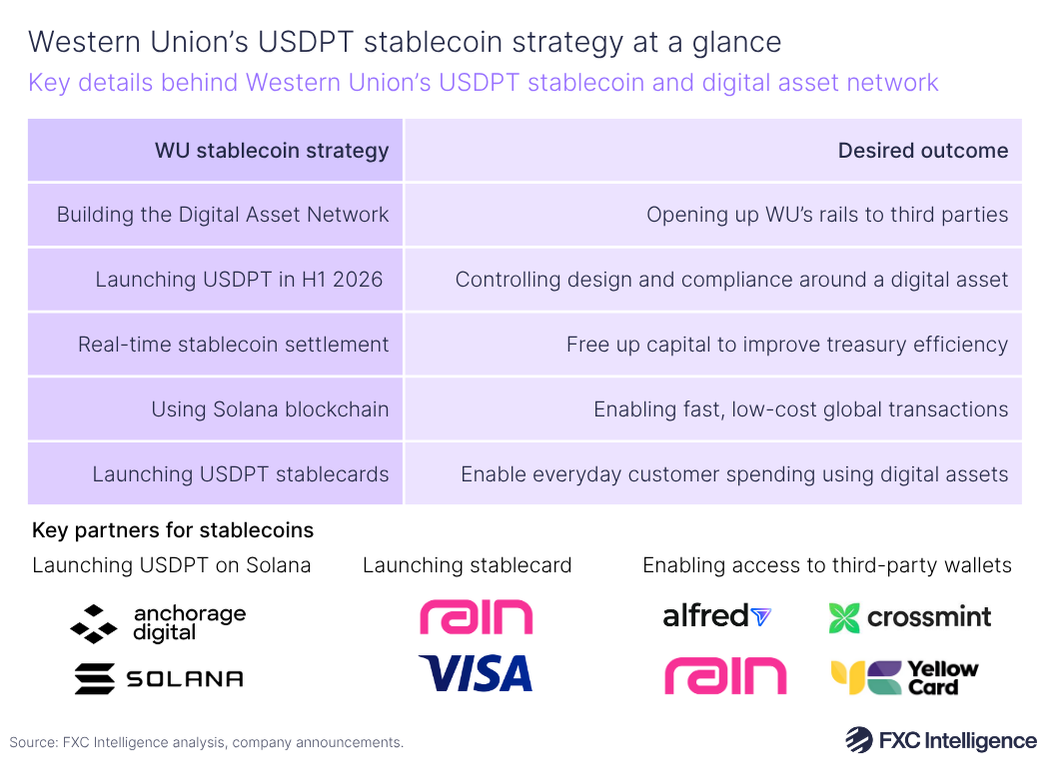

Western Union also gave a significant update on its upcoming stablecoin USDPT and the launch of its new Digital Asset Network, which it announced at the end of October, as well as other key aspects of its stablecoin strategies.

Chief Operating Officer Ben Hawksworth highlighted three key objectives for stablecoins at Western Union – helping move money more efficiently, opening up its network to third parties and helping create value for customers by enabling spending through USDPT.

On the first point, Western Union wants to use stablecoins to prefund transactions across its network through real-time settlement – reflecting a significant advantage that we have seen drive other cross-border payments launches.

On the second, it wants to build out its Digital Asset Network – creating the world’s largest on and off-ramp networks for digital assets that other digital wallets can tap into. Hawksworth said that the company is expecting to activate fund-out ramps in H1 2026, referencing four parties – Alfred, Crossmint, Rain and Yellow Card – through which it is aiming to extend its network across “hundreds of wallet ecosystems”.

Thirdly, through USDPT – the company’s stablecoin it is building with infrastructure provider Anchorage Digital and planning to issue on Solana – Western Union is targeting consumers directly, giving them the ability to hold, send and spend stablecoins. Alongside this, it has partnered with Rain and Visa to launch a physical and digital card that consumers can use to make payments with USDPT.

The company is issuing its own stablecoin so that it can have full control over the stablecoin’s design and how it is issued and circulated, but also because it sees itself having a “natural advantage” through its network to target stablecoin supply in high remittance-receiving countries.

The move is reflective of other players in the cross-border payments industry. For example, MoneyGram recently launched a new app enabling users to send and receive funds in USD stablecoins, while last year PayPal began enabling its disbursement partners to use PayPal USD (PYUSD) to settle cross-border money transfers.

Breaking down Western Union’s regional performance

Western Union has seen a mixed picture across regions and, aligning with its wider digital goal, the company is hoping strong performance in digital-heavy markets can help offset some of the softness it has seen in its core market of North America.

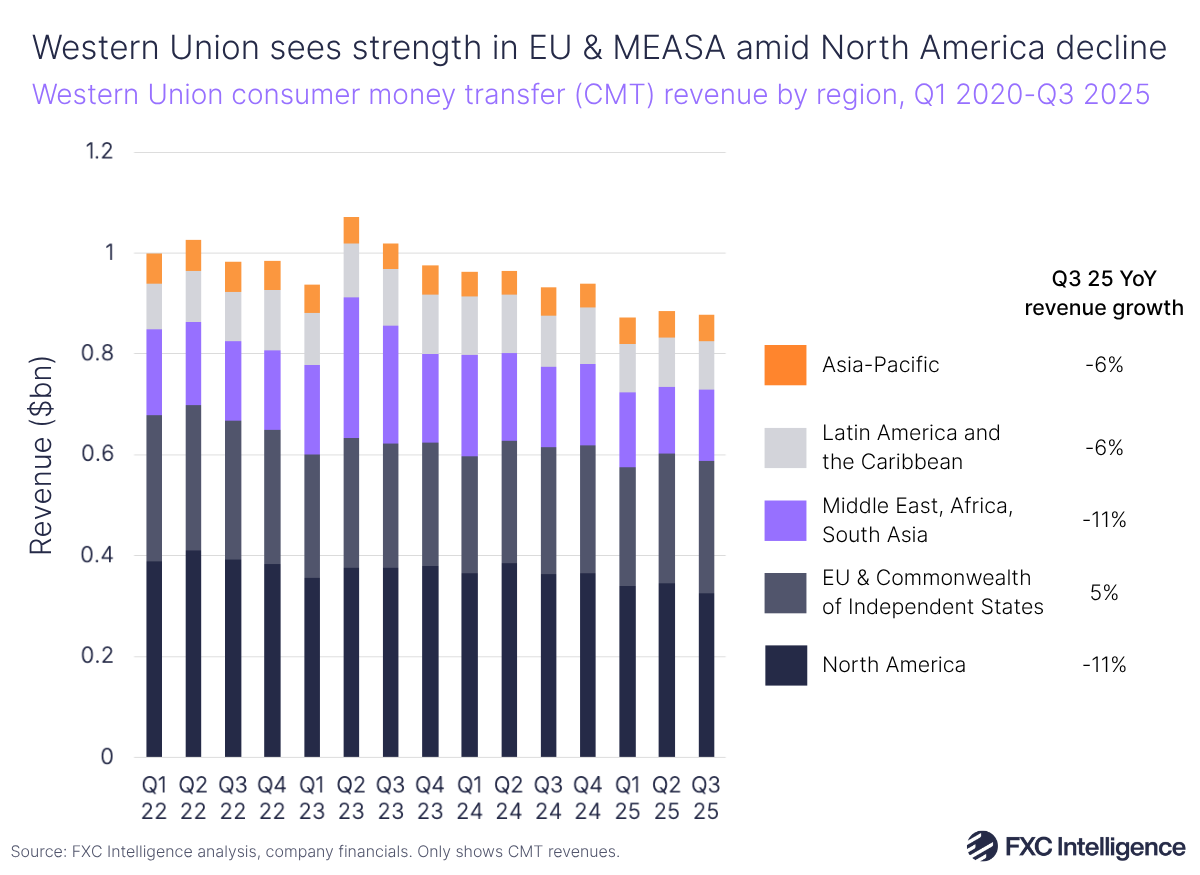

Digging into regional performance from its recent Q3 earnings, Western Union had noted a continued decline in North America – its largest market – where its share of remittance revenues had fallen from 39% to 37% between Q3 24 and Q3 25. By comparison, Europe and the Commonwealth of Independent States (EU & CIS) took a 30% share of revenues, with the Middle East, Africa and South Asia (MEASA) accounting for 16%, Latin America and the Caribbean (LACA) for 11% and Asia-Pacific (APAC) for 6%.

Taken against its C2C revenues figure, this means that EU & CIS revenues grew 5% YoY, while North America, LACA, MEASA and APAC all saw declines.

During the Q3 call, McGranahan noted “significant declines” to Mexico, El Salvador, Peru and Ecuador, as well as flat to negative change in corridors including the Philippines, Jamaica, Guatemala and Colombia. Recent policy changes in the US, which were leading to a decline in border crossings and more enforcement actions, are having an impact on consumers’ behaviour.

Having said this, McGranahan did note there had been “some recent improvements” on the US to Mexico corridor from lows seen in June, while macro changes had also led to stronger growth in outbound remittances in Argentina and growth in corridors such as Canada to India and Singapore to Indonesia.

Western Union is also factoring in its acquisition of LatAm-focused Intermex to future growth. Announced in August 2025 and expected to close in mid-2026, the acquisition should shore up Western Union’s North American retail operations and accelerate its digital transformation in key US-LatAm corridors.

As part of this, Western Union will add Intermex’s six million customers and around 10,000 agents across the US. This gives Western Union another large customer set to sell its digital services (e.g. its wallet), which was a key area that Intermex itself was trying to develop prior to selling.

LatAm is a region where Western Union continues to see strong opportunity amid current macro uncertainties. For example, it cited a large opportunity to target growth in underpenetrated routes such as the US to Guatemala, where digital adoption is rising but the company’s currency reach is “nascent”.

Strengthening Western Union’s hold in North America is key amid macro factors. On the US’s upcoming remittance tax, Cagwin said during the investor day that various solutions offered by Western Union – such as its Vigo wallet and prepaid card solutions – were potential tools for circumnavigating the tax and could see more monetisation as a result.

Looking at other regions presents a more positive story. McGranahan said during the call that Asia had become a “turnaround story”, while the Middle East “is rapidly investing and going digital”. In Europe, the company saw 13% YoY growth in its retail business as of the investor day, versus a 12% decline in 2023, through the implementation of a new operating model that it now aims to bring to its North American and global retail businesses.

Also in Europe, debit-funded send transactions accounted for 12% of retail transactions at retail locations in Europe, versus 4% in the US, highlighting this opportunity to scale up in North America as well as an overall customer demand for digital payment methods.

Building a bigger payments network opportunity

A key theme for Western Union’s strategy is the strength of its existing network – a driver of its “Beyond” ethos for remittances.

The company has more than 300 real-time payout options in more than 140 countries – including key corridors such as India, Mexico, the Philippines and Colombia – and has doubled the number of transactions delivered via account payouts over the last three years. Altogether, the goal is to eventually target a wide range of use cases beyond consumer-to-consumer payments.

“We envision a future, not too far away, where we can move money for others for B2C, C2B and maybe even B2B use cases,” McGranahan said.

Some major money transfer companies have been pushing selling their networks as a service to other financial institutions or payments companies, in particular Wise with its Wise Platform product and Ria with Dandelion. For Western Union, however, the current focus on investments into its infrastructure – i.e. through cloud migration, stablecoin payouts and real-time payments connections – appear to be mainly in serving its own business first.

“That real-time payments network, the ability to fund across geographies, across payment types and to pay out in real time is a strategic asset for us,” said McGranahan. “If there is market demand, we’re going to take advantage of it. But you didn’t see us come up here and say, ‘Hey, we see $1bn of revenue from opening it up’. What we said is we’re building a strategic asset that has utility Beyond and we’re going to see what that looks like.”

Looking at Western Union’s overall ambitions, its Beyond strategy captures a move other remittances companies appear to be making to extend the reach of their payments networks and shift solely from serving remittances to other financial products.

Though it hasn’t grown as fast as other digital challengers in recent years, it is worth remembering that the company remains the biggest player in terms of revenue compared to other consumer-focused money transfer players, with a projected annual revenue of over $4bn in 2025, and one of the world’s most trusted and established payments networks. This makes its moves to extend its non-remittances segments, as well as shore them up with stablecoins, particularly significant indicators to the industry as it redefines its position in payments.