Money transfers with cash payouts have traditionally cost more than transfers to bank accounts, with FXC Intelligence data showing that this is still the case in 2026. However, there are signs that consumers are beginning to pay less of a premium on these transfers.

With the world continuing to increasingly embrace digital financial solutions, cash usage has declined significantly – particularly in developed countries.

As of 2025, 79% of adults worldwide had an account at a bank or similar financial institution, up from 74% in 2021. However, this isn’t equal worldwide: less than half of adults report having a bank account in countries like Lebanon, Morocco and Niger, while bank account access is practically universal in the likes of Canada, Denmark and Japan.

While internet access and smartphone ownership have also increased over the last decade, the World Bank reports that internet usage gaps still exist in some parts of the world, with poorer adults less likely to have access to the internet.

Some of the largest remittance providers in the world continue to focus on expanding their portfolio of digital money transfer offerings to compete with newer, digitally native companies.

However, many of these providers also continue to provide cash payouts to customers, recognising that this transfer method remains crucially important to some of the world’s poorest people. Despite this, according to our data, cash payouts remain one of the most expensive money transfer methods, with transfers sent to bank accounts remaining consistently cheaper worldwide.

In this report, we use FXC Intelligence’s FX Pricing Data to take a closer look at the cost of sending cash payouts compared to bank accounts, exploring how much of a premium they require and whether the difference in total costs and margins are decreasing over time.

How do cash payout premiums vary in 2026?

To understand the cost of cash payouts, we collected the median standard pricing (for returning customers) of major remittance providers when sending $500 across 10 corridors, all originating from the US, specifically in February 2026. Using this data, we calculated the average margins and average total cost for transfers to bank accounts and for cash payouts, using these values to find the premiums attached to the latter. We did not include promotional pricing that applies to new customers, which FXC Intelligence also collects real-time data on.

The 10 receiving countries focused on are Egypt, Guatemala, India, Mexico, Nepal, Nigeria, Pakistan, the Philippines, Thailand and Vietnam; these were selected to ensure a broad spread geographically, while only focusing on major recipients of remittances.

For each of these corridors, we collected pricing to send bank account-to-bank account and bank account-to-cash, finding the median FX margin, median fee margin and median total cost across selected providers that offer both methods of transfer. We used this information to calculate the difference between pricing for cash payouts and bank account payouts.

This research does not include providers that only offer one of the two selected methods of payouts for any specific corridor, or other forms of payouts including debit cards or mobile wallets – all of which are available within FXC Intelligence’s FX Pricing dataset.

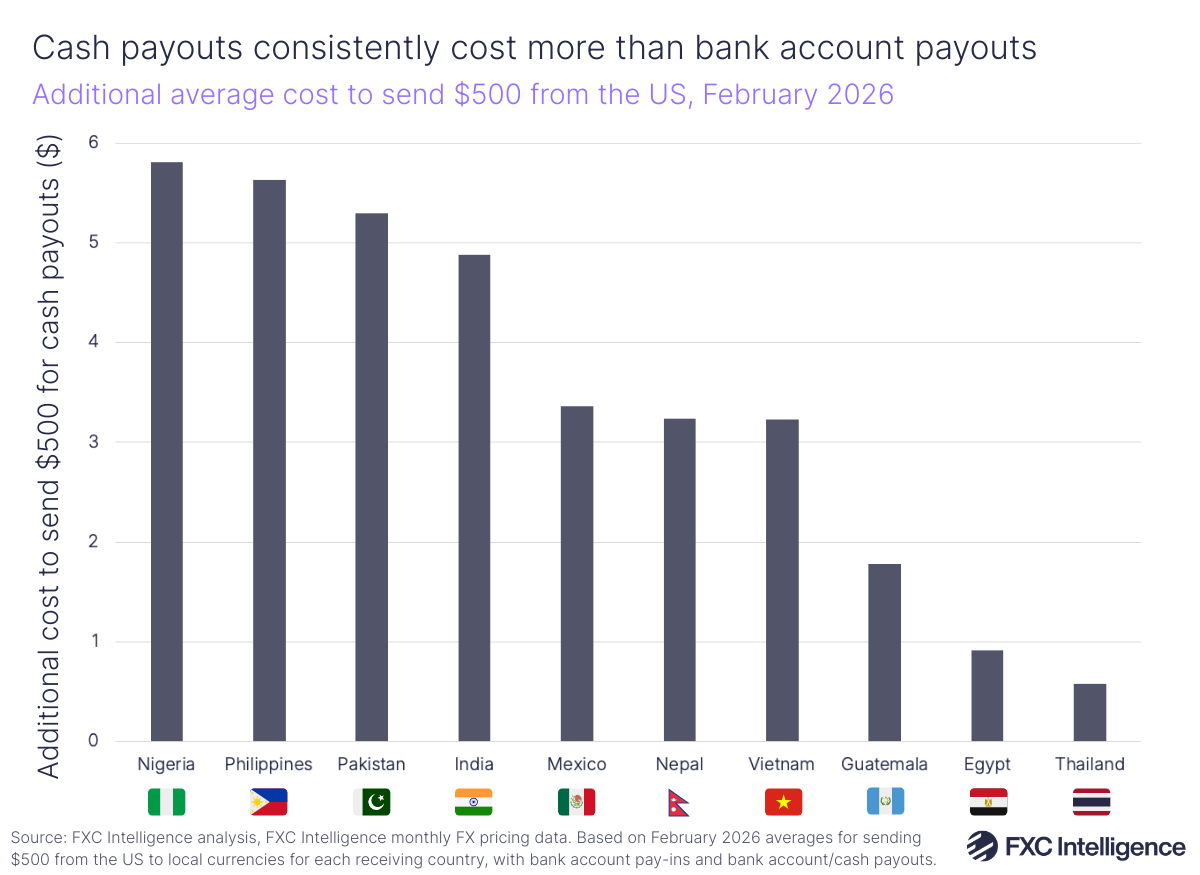

As we did in 2024, we found that the average total cost to send money from the US to each of the 10 receiving countries was higher for cash payouts than for bank accounts. Across the 10 corridors, the average cost to send $500 from the US was $3.47 more for cash payouts than those to bank accounts.

However, there has been improvement, with the difference in cost less pronounced than when we analysed this trend for the same 10 corridors in March 2024 – when cash payouts were $5.55 more expensive on average.

The cost difference when sending $500 from the US also varies considerably depending on the receiving country. Of the 10 corridors, two were less than $1 more expensive to send money for cash payouts than bank account payouts in February 2026 – the US to Egypt ($0.92 more expensive) and the US to Thailand ($0.58).

At the more expensive end of the spectrum sits the US to Nigeria ($5.81 more expensive), the US to the Philippines ($5.63) and the US to Pakistan ($5.29). The remaining corridors cost between $1 and $5 on average more for cash payouts than when sending $500 for bank account payouts.

Why do margins differ between corridors?

While the overall margins were consistently more expensive when sending money for cash payouts than for bank account payouts, this was not always true for two main components that make up the margins remittance providers charge on transfers – FX margin and fee margin.

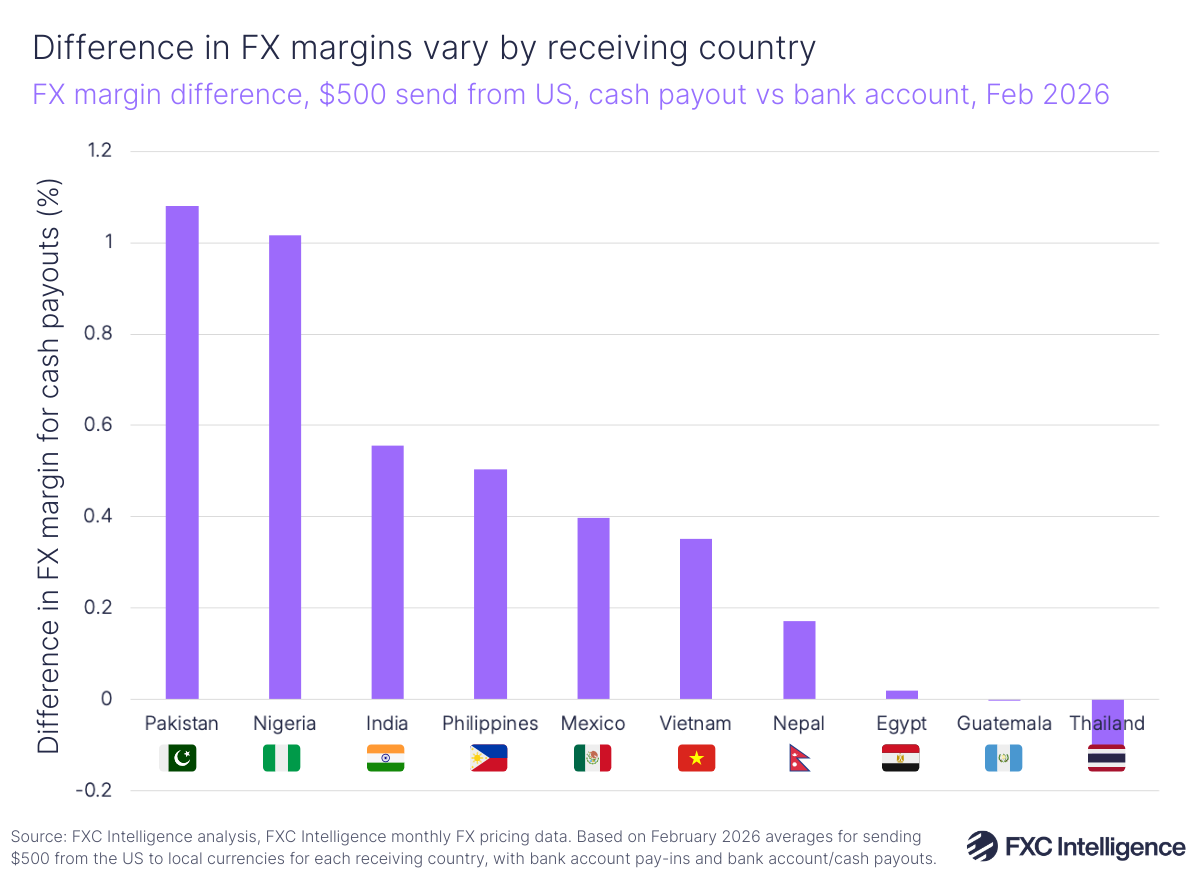

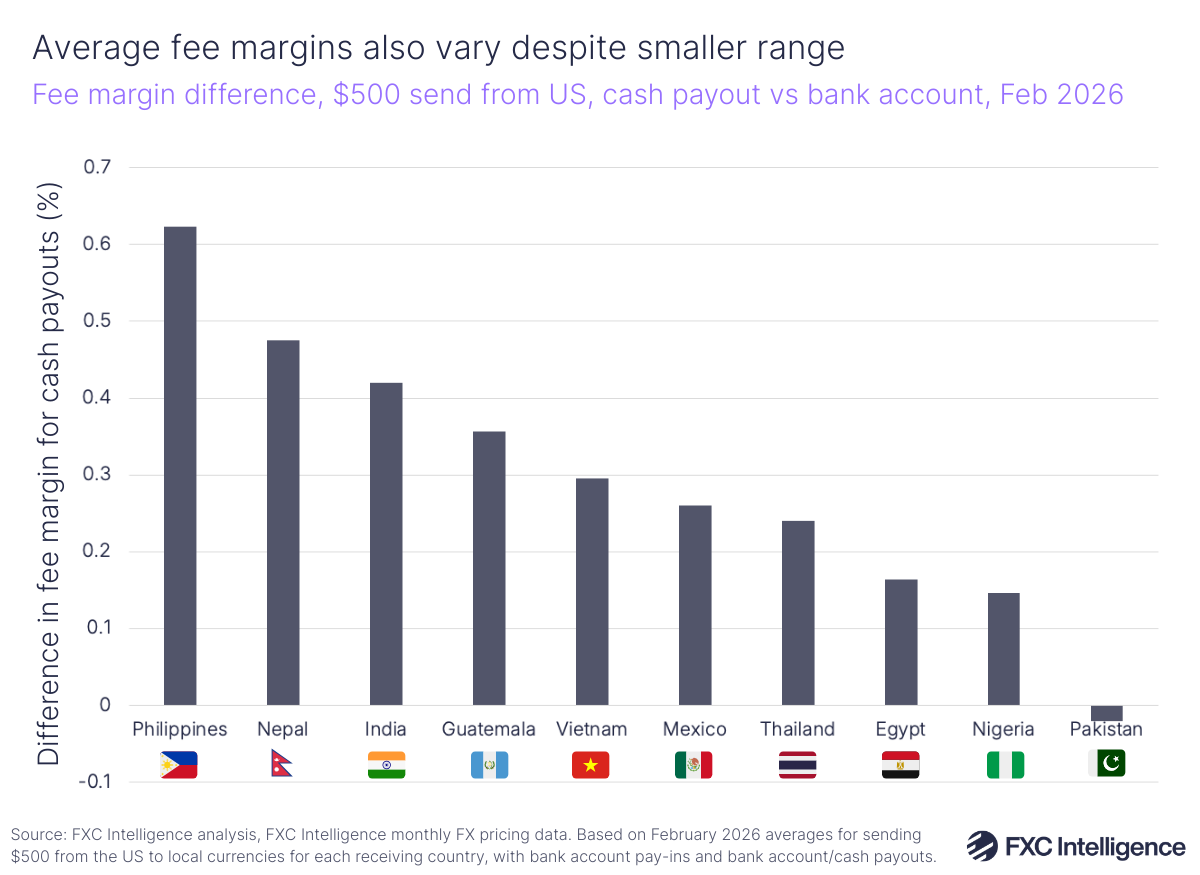

The total margin charged for cash payouts was 0.7% more on average than for bank payouts across the 10 corridors, although this varied corridor-to-corridor, as did the FX and fee margins. Of that 0.7%, FX margins – the percentage charged to cover the cost of converting the sending currency to the receiving currency – accounted for a larger share at 0.4%. Fee margins, the percentage remittance providers charge on top of each transaction to deliver the remittance to the recipient, made up the remaining 0.3%.

Notably, cash payout remittances to Thailand saw a lower FX margin than for those sent to bank accounts by 0.1%. All other corridors saw a higher FX margin for cash payouts than bank payouts or were effectively equal with the charges applied to transfers to bank accounts.

Remittances sent to Pakistan had the highest difference in FX margin attached to cash payouts compared to the FX margin attached to transfers to bank accounts, sitting significantly above the average at 1.1%. Meanwhile, Nigeria saw FX margins for cash payouts sit 1% higher than bank accounts.

When it came to fee margins, this once again varied depending on the receiving country. The Philippines saw the greatest difference in fee margin for cash vs bank payout, with the average fee margins on cash payouts being 0.6% higher than the same margin on bank account-to-bank account transfers.

Meanwhile, despite cash payout transfers sent from the US to Pakistan having the largest premium for FX margins, this corridor not only had the smallest difference between fee margins on cash and bank account payouts, but was the only one to have lower fee margins for cash transfers (at 0.02% cheaper).

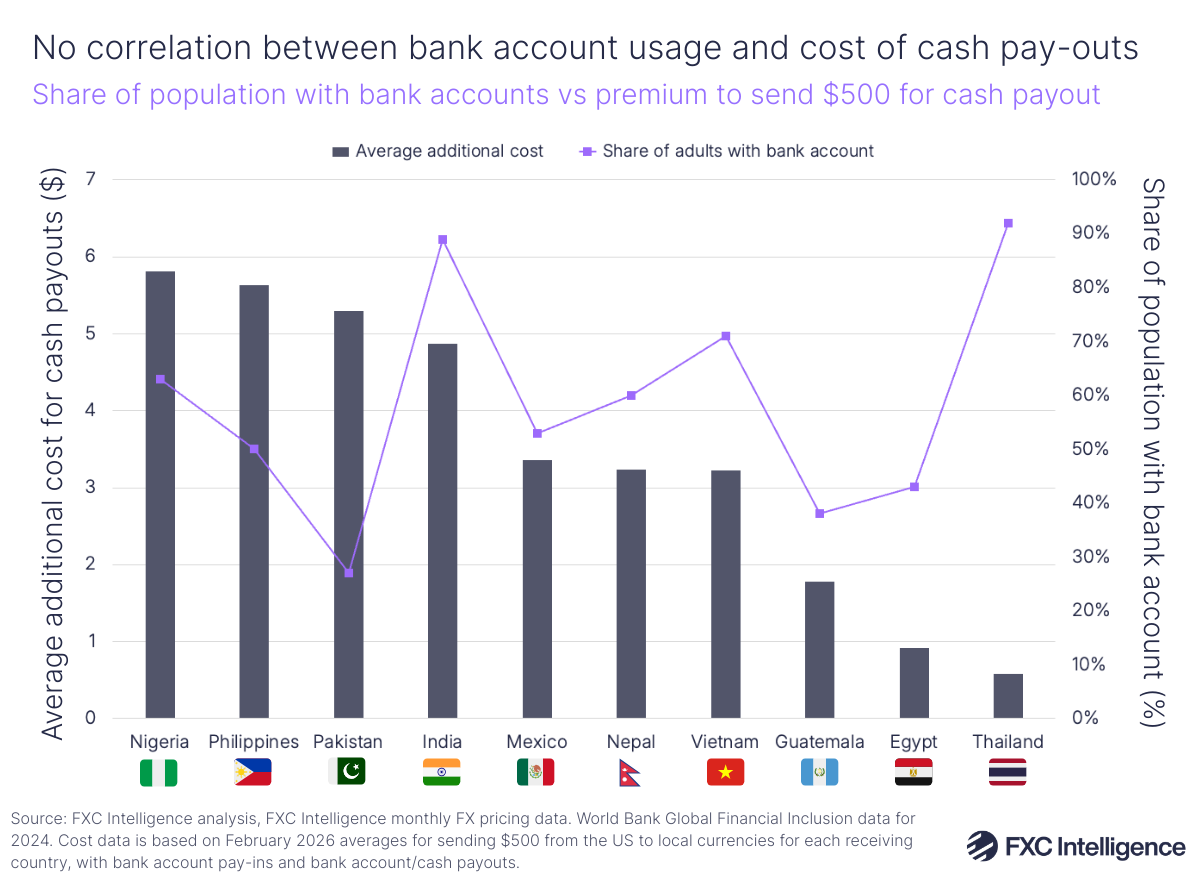

Are fees on cash payout remittances higher to countries with lower bank account access?

In 2025, the World Bank released the latest edition of its Global Financial Inclusion data, which details the percentage of adults (people aged 15 or over) that have a bank account.

Across the 10 receiving countries focused on in this report, an average of 59% of people have some form of account at a bank or similar financial institution. While this has risen from an average of 45% in 2017, this data suggests that there is still a significant number of people that currently do not have access to bank accounts.

Meanwhile, an average of just 22% of adults across these 10 receiving countries have a mobile money account, highlighting the importance of cash payouts to significant proportions of these populations.

Money transfers sent to countries with lower levels of account usage are more likely to be affected by premiums associated with sending cash payouts, as the sender has a smaller range of options to choose from when sending the money.

Despite this, there appears to be no correlation between the premiums applied to cash payouts and the share of adults with bank accounts in each receiving country. While 92% of adults have access to a bank account in Thailand and the additional cost to send these types of transfers is around $0.58 when sending $500, India has a similar share with 89% but the additional cost for cash payouts is over eight times more – at an average of $4.88 more than a bank to bank transfer. When looking at countries where less than half of the population has a bank account, such as Egypt, Guatemala and Pakistan, there is also no clear trend with cash payout premiums. Egypt has the second-lowest average additional cost for cash payouts with only 43% of adults having bank account access, but Pakistan, which has the lowest population share with bank account access at 27%, sees the third-highest premiums across the 10 corridors – around $5.30 more for cash payouts.

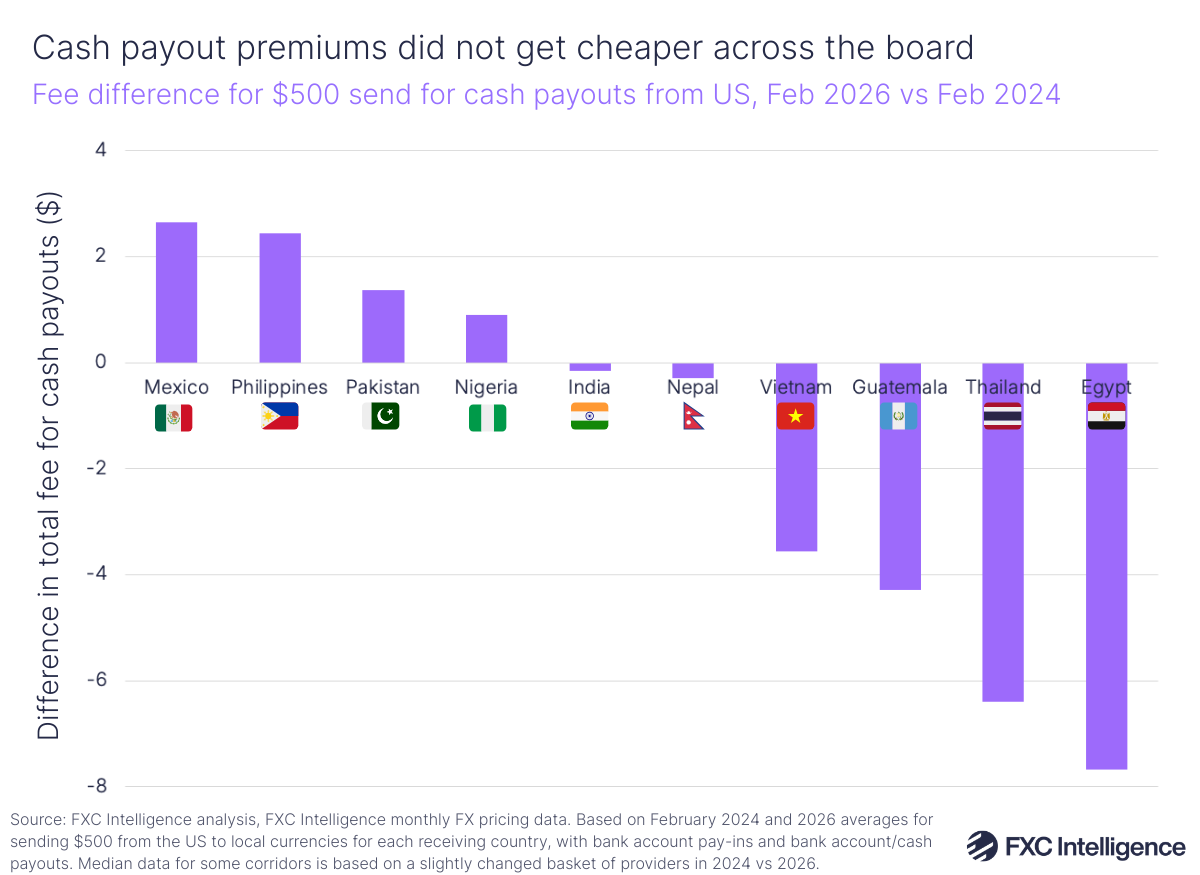

Are cash premiums getting cheaper over time?

Although premiums associated with cash payouts are clearly still present across every corridor analysed, several initiatives continue to focus on reducing the overall cost of remittances, including the G20 Roadmap for Enhancing Cross-border Payments and UN Sustainable Development Goal 10.c.

To find out if these efforts have helped close the gap between fees on bank and cash payouts, we also analysed median FX pricing data for February 2024 to see if there have been any major shifts in the difference in pricing between the two payout methods.

Overall, the average difference in the total cost of cash payouts versus bank account payouts fell by $1.50, while the difference in total margin also declined by 0.3%. The US to Egypt, Thailand, Guatemala and Vietnam were the key drivers of this downward trend, with each corridor seeing the difference fall a minimum of $3.56 regarding fees on $500 transfers from the US.

However, this trend did not occur across every corridor analysed. Although six of the corridors saw the average total difference of fees decline for cash payouts compared to bank account payouts, the difference increased on some of the largest remittance corridors.

For some time, the US to Mexico has been widely known as the single largest remittance corridor in the world. Despite bank account access in Mexico remaining a long way from universal and the county receiving well over 100 million remittance transactions each year from the US alone, the premiums associated with cash payouts increased more than any other corridor analysed. The Philippines, Pakistan and Nigeria also saw the average difference between cash and bank account payouts increased compared to February 2024.

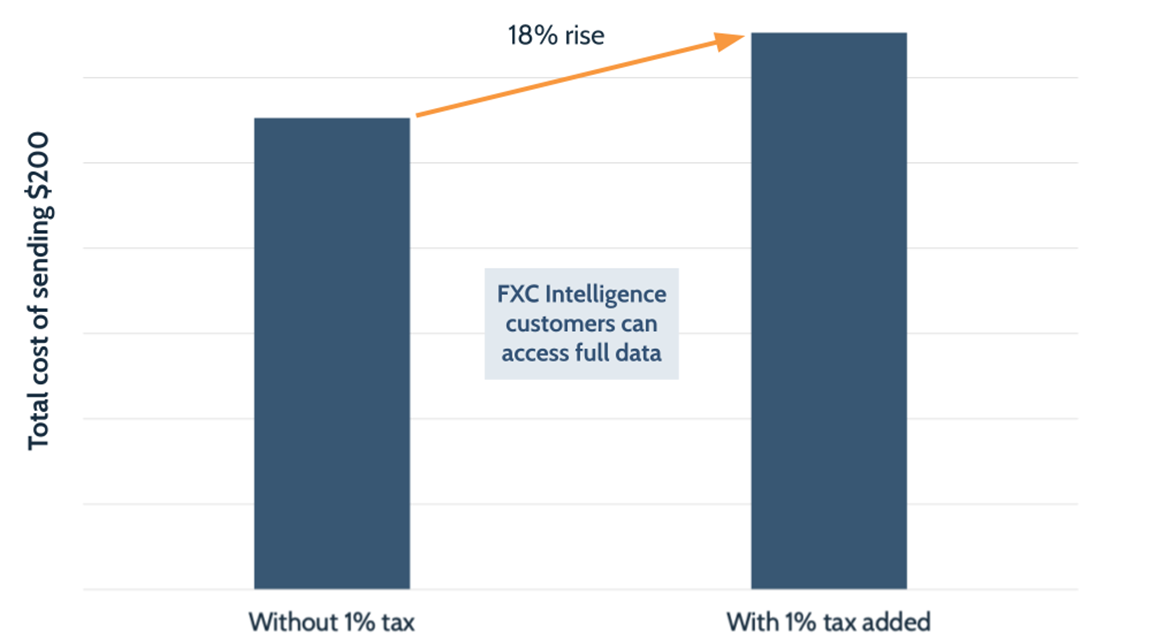

Although the US’s 1% federal tax on remittances only applies to transfers sent using cash from the US (rather than applying to cash payouts), this means that some remittances are seeing extra fees added at both ends of the transfer. In many cases, these fees continue to fall on the poorest and most vulnerable consumers, highlighting the need to keep premiums on cash payouts down wherever possible.