Circle’s blockbuster IPO saw the company surge in value, bringing an end to a multi-year journey to public listing. But what are its main priorities as a public company?

Last week saw Circle finally make its public market debut in an upsized 5 June IPO on the New York Stock Exchange.

It follows multiple previous attempts at listing, first with a failed SPAC in 2021 and later in 2022 with a private IPO filing. In April, the company announced a new IPO and filed its S-1 publicly but was forced to delay as the US tariffs plunged markets into turmoil shortly after. However, it returned with an amended prospectus in late May before its public listing just over a week later.

The IPO saw Circle make its stock market debut at a $6.9bn valuation, with its share price quickly skyrocketing. At the close of the week, its market cap stood at $18.5bn and has risen further since. By the close of Wednesday 12 June, it had risen to $25.8bn

As the only publicly traded stablecoin issuer, the company is becoming something of a proxy in the wider market. However, there are some high-priority areas it will need to focus on if it wants to maintain its strong market position.

In this short report, we look at some of the key areas where Circle will need to prioritise its efforts if it is to maintain its current market strength.

Circle’s post-IPO revenue mix

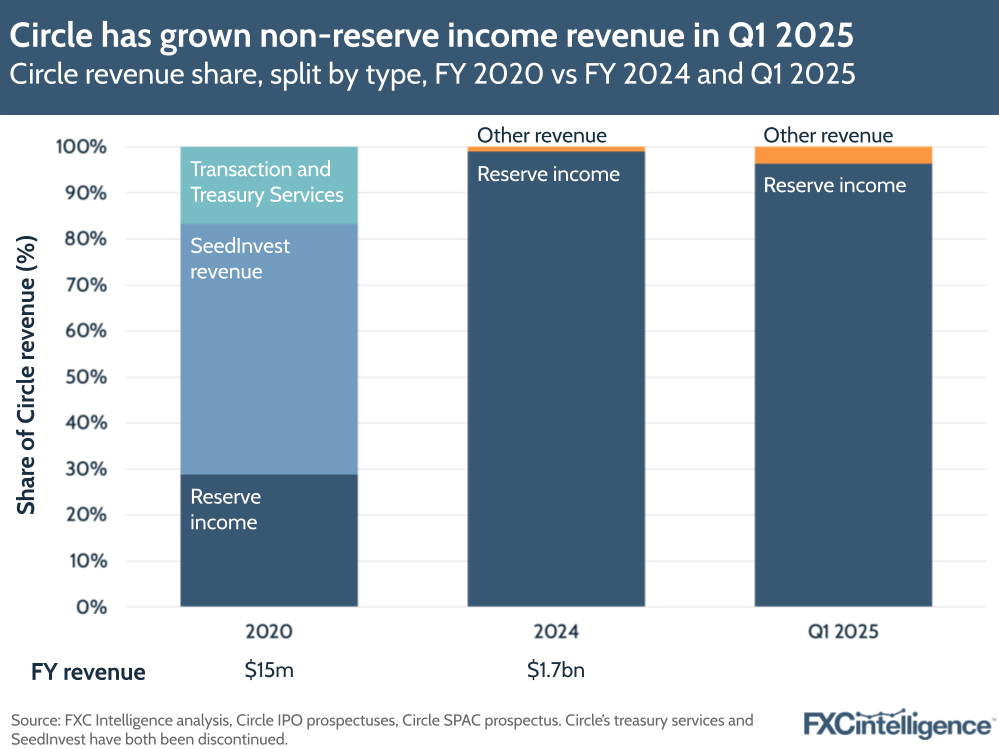

Circle’s revenue mix has evolved significantly over the past few years. In 2020, the year before its failed SPAC listing, Circle gained much of its revenue from its then-share of crowdfunding platform SeedInvest, as well as its since-closed treasury services business line.

However, the 2024 numbers shared in its S-1 document earlier this year showed this had changed significantly, with 99% of its income coming from reserve income. This is the interest income it makes on the reserves it holds to back its stablecoins, which are a mix of cash, short-dated US Treasuries and overnight US Treasury repurchase agreements. As a result, the greater the number of stablecoins issued by Circle – primarily US dollar-backed USDC – the higher its revenue.

However, this does make the company highly sensitive to interest rate changes, which is a particular challenge in the current macro environment, and also means it is very exposed if there is a sudden sell-off of its stablecoins. In light of the current interest rate uncertainty, Circle’s S-1 gave reserve income guidance for FY 2025 that varied by more than $1bn depending on the change in interest rates.

However, Circle has indicated that it plans to diversify its revenue through additional services related to its broader business areas. These include liquidity services product Circle Mint, its developer services solutions and its tokenised funds offering.

Q1 2025 numbers indicate that the company is beginning to see some results from these efforts, with non-reserve income revenue increasing to 4% of total revenue for the quarter, up from 1% a year earlier. Nevertheless, there is a significant way to go before Circle’s revenue mix meaningfully changes, and this may create challenges for the company in its upcoming quarterly earnings calls.

Growing USDC circulation

The primary way Circle can grow its revenue at present is by increasing the number of its stablecoins in circulation, making this a primary goal for the company simply from a revenue generation point alone. However, it also is critical to broadening its utility in the payments space, particularly if efforts to use USDC for cross-border payments continue to gain momentum.

Some companies offering stablecoin-based cross-border payments that we have spoken to have reported the market cap for USDC being a limiting factor in its use for cross-border payments, particularly for high-value transactions. As a result, some players have opted to use USDT instead of or in addition to USDC due to the greater market liquidity.

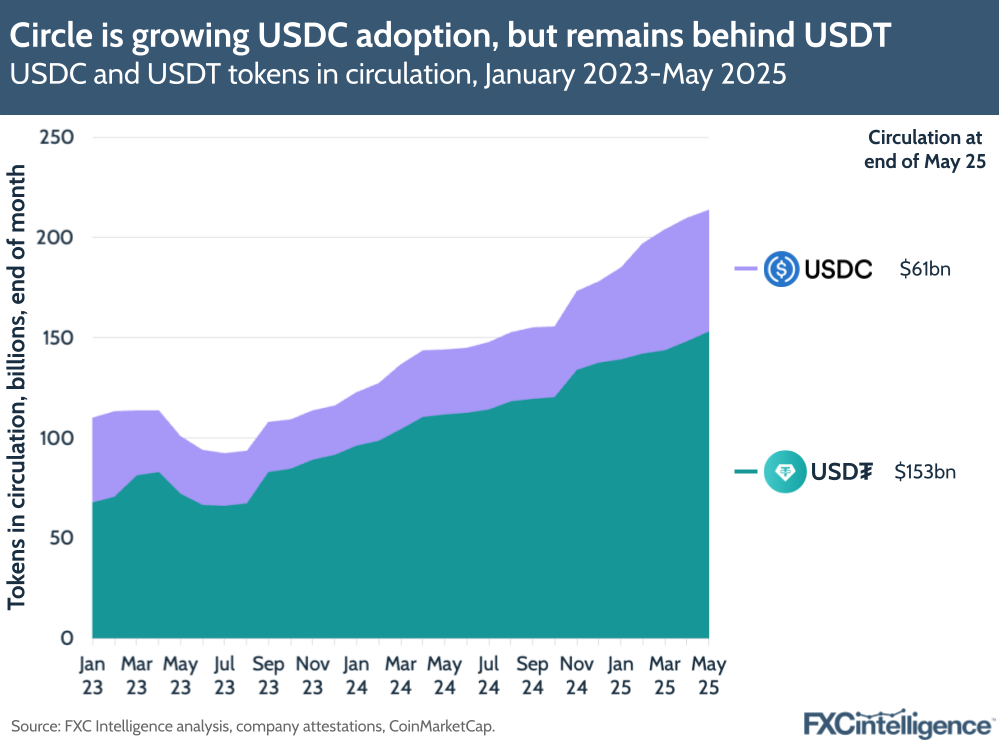

While USDC had a $61bn market cap at the end of May, USDT, which is issued by rival Tether, had a market cap almost three times higher, at $153bn. Given differences in the way the two companies back their stablecoins, and where they are based, there are those in the financial industry that are far more comfortable using US-headquartered Circle’s stablecoin, however the greater liquidity offered by USDT gives it inevitable additional benefits for some applications.

While Circle has some way to go if it is to grow USDC to the circulation of USDT and beyond, it is seeing some progress, with a significant increase in recent months. USDC’s market cap has increased by around $20bn since the start of the year and almost doubled from a year ago, when its market cap stood at $32.3bn at the end of May 2024.

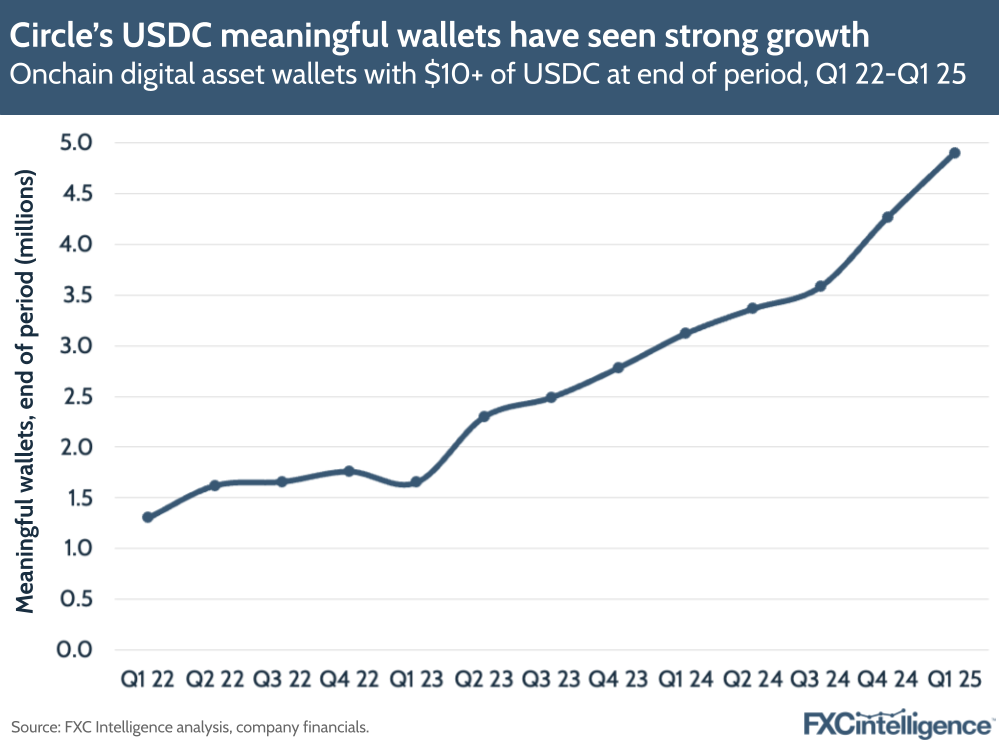

Circle is also seeing success in growing the number of users of USDC. Meaningful wallets – blockchain-based digital wallets holding $10 or more in USDC – have grown significantly in recent months, climbing 15% quarter-on-quarter and 57% year-on-year to 4.9 million in Q1 2025.

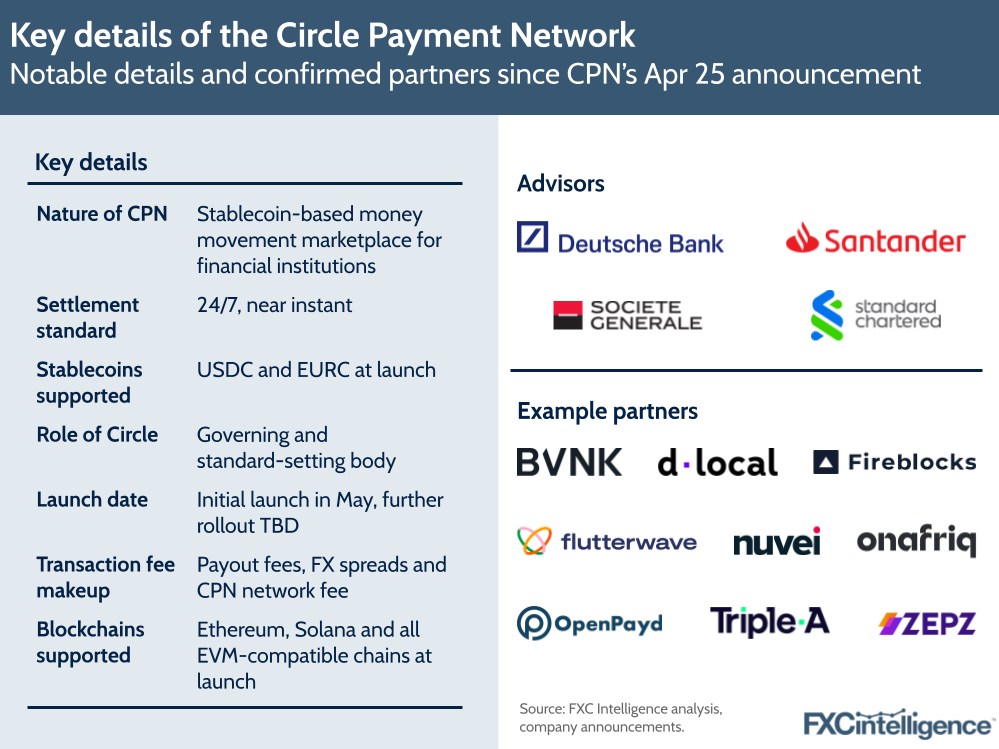

Circle Payments Network clarity

Another area that Circle is presenting as a future source of revenue is its Circle Payments Network (CPN) project. Announced in April shortly after the company published its S-1, this is a proposed stablecoin-based alternative to Swift that Circle would act as the governing and standard-setting body for.

While Circle would not facilitate the movement of money itself, CPN would act as a marketplace between financial institutions, enabling 24/7, near-instant transfers using stablecoins across several major payments-friendly blockchains. Under the system, Circle would take a fee for each transaction, which would apply alongside the usual transaction fees and FX margins.

The project was developed with Deutsche Bank, Santander, Societe Generale and Standard Chartered acting as advisors, with a wide variety of companies named as initial partners, including BVNK, dLocal, Flutterwace and Zepz. Circle has also indicated that it could be used for a wide variety of institutional, business and consumer payments.

However, there are still many questions that remain unanswered, particularly when it comes to its rollout and cost.

While Circle did announce an initial launch in May, we have yet to get further clarity on this or the timeline for the project. There is also not yet a clear sense of the volume of transactions that the network can support, its cost or how it will be used alongside other networks by the participating financial institutions.

While the project is in its early stages, Circle will need to provide further details and clarity on launch plans to convince the industry that CPN can provide a meaningful improvement on network solutions already in place.

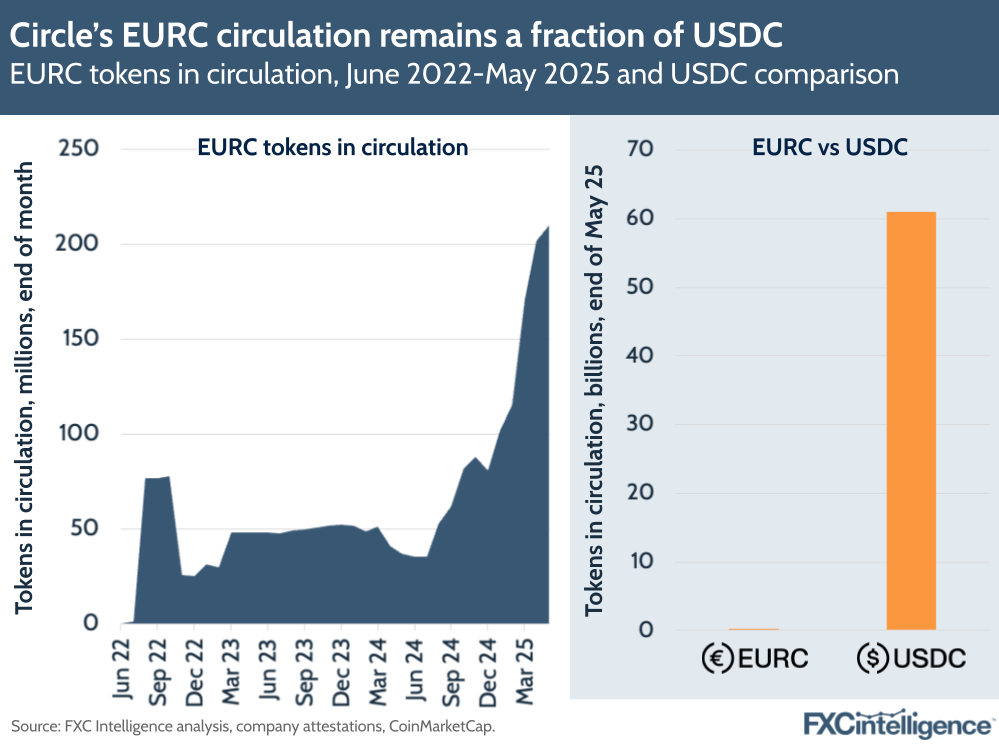

Stablecoin sovereignty and EURC growth

The final area is not just an issue for Circle, but for the stablecoin industry as a whole. In some areas of the world, such as Europe, there are increasing concerns about stablecoins not due to the technology, but because of the ubiquity of US dollar-backed stablecoins. As stablecoins grow in use, there are concerns that they are bringing a creeping dollarisation in the process, raising concerns about monetary sovereignty that have become particularly pronounced in light of the US trade tariffs.

There are therefore increasing calls for non-USD alternatives, with Europe in particular seeing growing demands for euro-denominated stablecoins. As the issuer of one of the most popular US-backed stablecoins, Circle is a focus for this, which may be why it has increasingly focused its euro-backed stablecoin EURC in recent marketing activity in the region. At Money20/20 Europe last week, for example, EURC was a central focus for the company on its stand.

However, having been launched just three years ago, EURC’s market cap remains a small fraction of USDC, and while it has seen strong recent growth, particularly since the start of 2025, it still has some way to go in this area.

If Circle is to build a presence as the stablecoin of choice in many regions, it will need to be mindful of sovereignty concerns, and may even see challenges of a regulatory variety if the issue becomes more pronounced.