How did B2B2X players and cross-border payment networks providers perform in 2025? We take a look at the trends which have shaped the space in the last year.

Infrastructure firms that enable other businesses and platforms to move money internationally for business or consumer clients, known as B2B2X players, reported strong performances across the board in 2025.

B2B2X networks expanded rapidly throughout the year as firms engaged in more partnerships and integrations, while a large number of real-time payments systems across the globe linked to improve interoperability. Stablecoins also continue to have an increasing impact on the space and look set to have an even greater influence over the coming year.

In this report, we take a look back at some of the key moments and trends that occurred in 2025 for B2B2X and consider what the future holds for the industry.

Partnerships drove network expansions

In 2025, countless partnerships were agreed involving B2B2X players to ease and improve cross-border money transfers. Many of these partnerships involved banks, which looked to improve the speed and cost surrounding cross-border payments.

In September, global bank Citi teamed up with cross-border payments network provider Dandelion to integrate its WorldLink cross-border payment system with Dandelion’s digital wallet network. The move looked to enable Citi clients to deliver near-instant payments into digital wallets across the globe, with a specific focus on meeting a need for B2C payments into wallets for refunds, payroll, payouts and other use cases.

Earlier this year, executives at Euronet said they believed its B2B2X platform Dandelion could help it capture an industry “nearly 20 times the size of the remittance market”. In an attempt to take advantage of this opportunity, Dandelion engaged in a number of partnerships to extend its network. One of the most notable was a collaboration with Visa Direct, via which Euronet’s Dandelion was able to expand its network to include four billion Visa debit cards.

More recently, First National Bank (FNB) joined forces with Mastercard to launch a new cross-border payments solution dubbed Globba. The offering leverages B2B2X platform Mastercard Move to enable South Africans to send international payments to more than 120 countries. The partnership also has plans to gradually expand to other parts of FNB’s network across Africa.

In Asia, Thunes joined forces with WeChat Pay HK, a Hong Kong dollar-denominated e-wallet. By leveraging Thunes’ Direct Global Network, WeChat Pay HK plans to support real-time outbound money transfers to billions of endpoints worldwide.

Payment infrastructure interlinking and expansion

Domestic payment infrastructure played a role in not only improving financial access and speed, but also in increasing the number of endpoints for cross-border payments networks to connect to.

In July, India’s UPI significantly expanded its link with Singapore’s instant retail payment system PayNow – adding 13 more banks to the connection to further enable the sending and receiving of money across the two countries.

In September, Chinese state-owned financial services provider UnionPay International initiated a pilot for cross-border QR payments between China and Indonesia, following the launch of Indonesian QR code payment acceptance in Japan.

In October, the European Central Bank began exploring interlinking its TARGET Instant Payment Settlement system with the Swiss Interbank Clearing Instant Payments system as part of efforts to enable faster, cheaper and more transparent access to cross-border payments in the region.

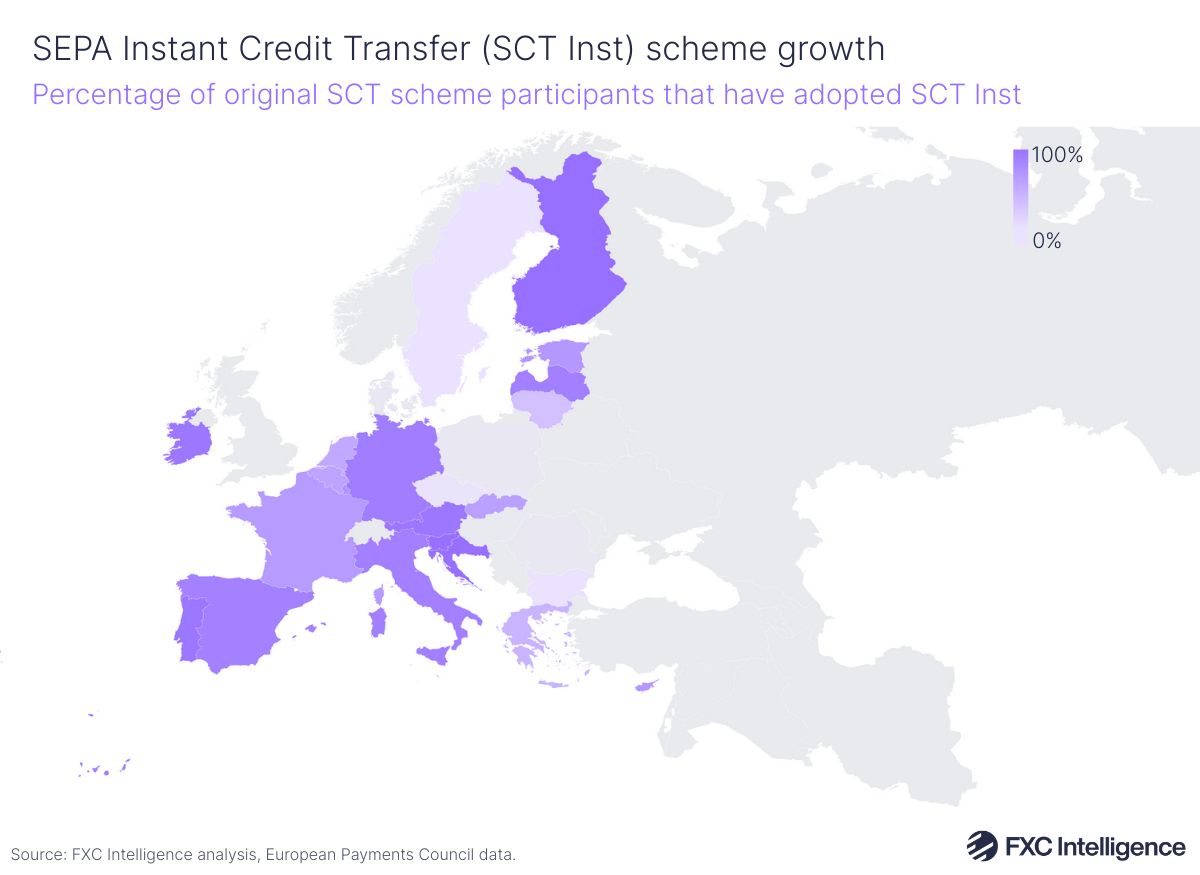

At the time, we looked at the progress of the European Payments Council’s SEPA Instant Credit Transfer (SCT Inst) scheme, which enables real-time euro payments across Europe. According to a 2025 status update, SCT Inst adoption has surged since its launch in 2017 – with 91% of euro-using participants of the original SCT scheme having already adopted the instant payment scheme. However, uptake hasn’t reached the same level in EU countries that do not primarily use the euro, highlighting the need for interlinking initiatives.

The Pan-African Payment and Settlement System (PAPSS) also continued to expand its coverage in 2025, officially launching in four new countries in 2025, namely Kenya, Rwanda, Morocco and Algeria – bringing its total to 18 countries. PAPSS now boasts connection to over 100 commercial banks, while a large number of African countries have made bilateral currency agreements with other countries to enable trade directly in other currencies.

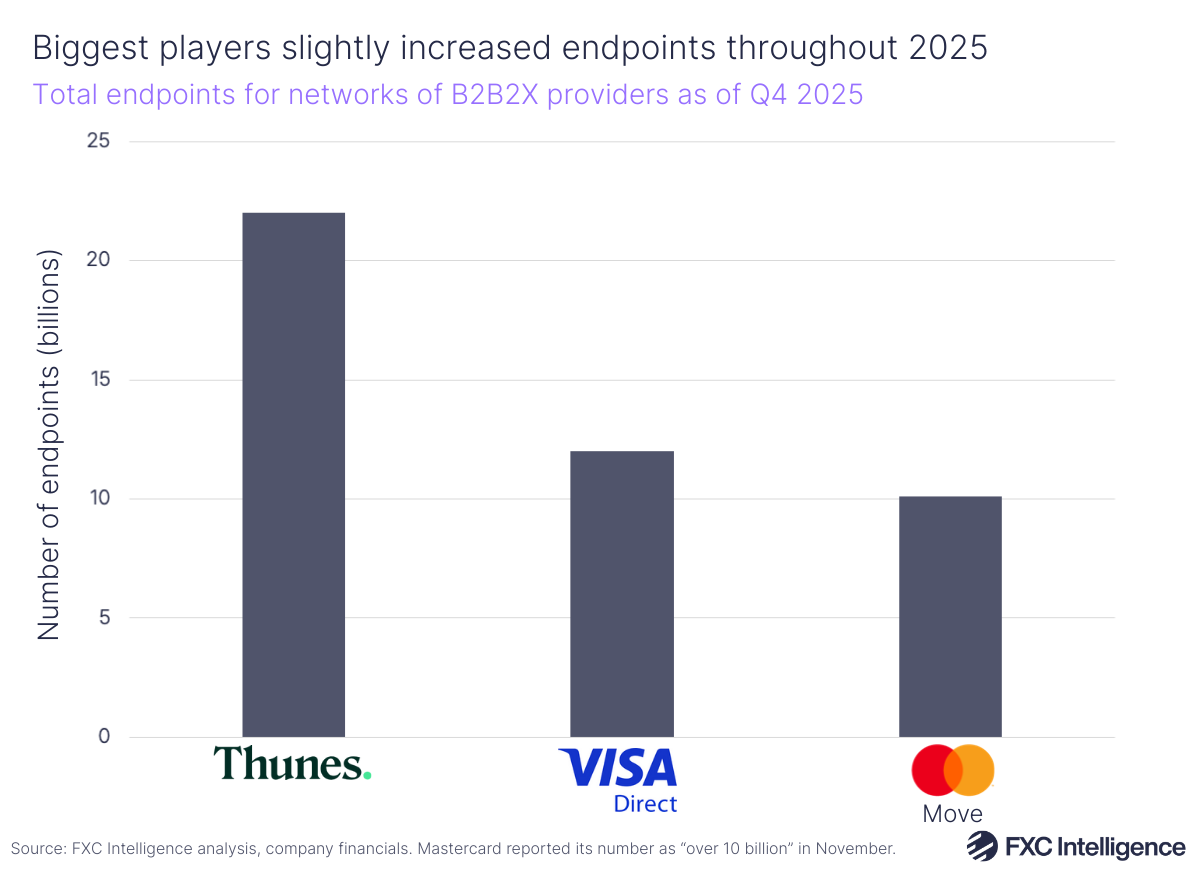

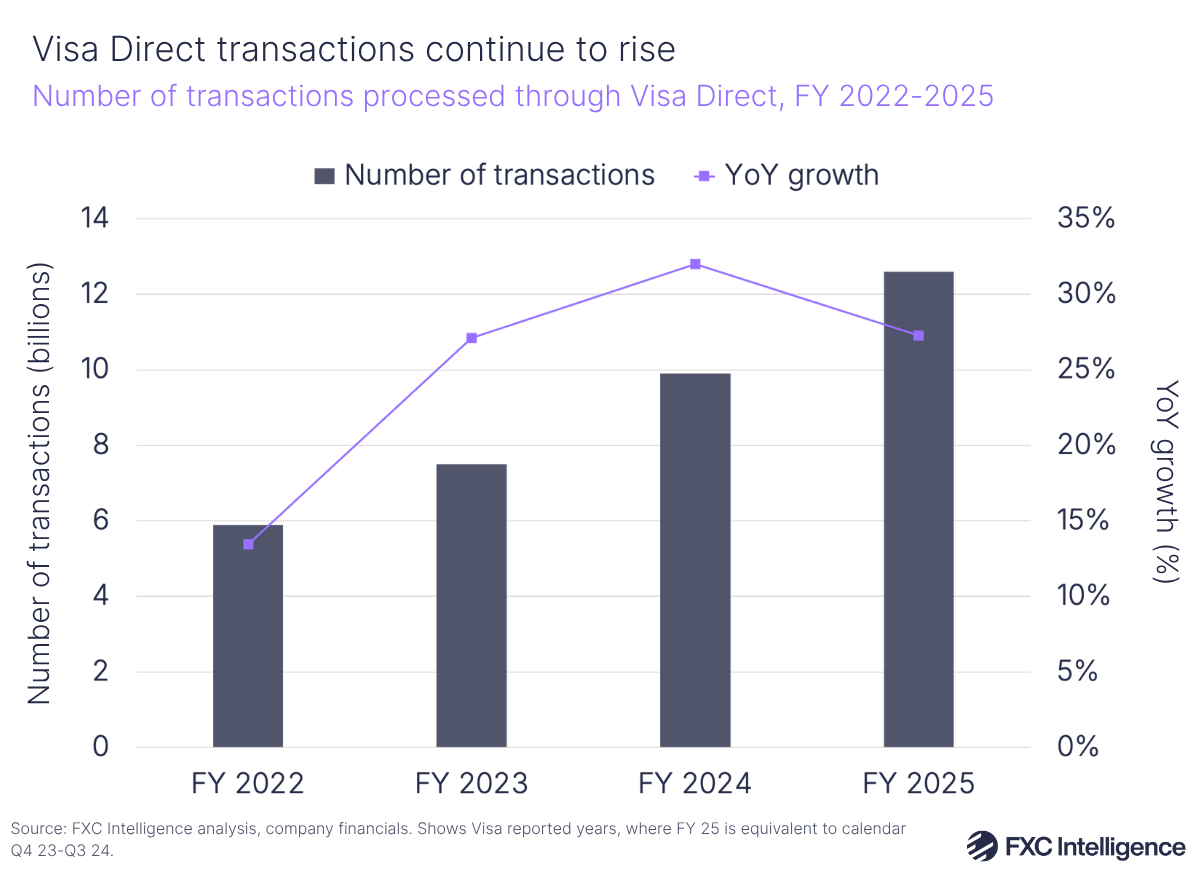

The biggest B2B2X providers also continued to expand or add to their own existing networks. In calendar Q3, Visa reported that its B2B2X platform Visa Direct grew to approximately 12 billion endpoints – up from 11 billion in 2024 – split roughly equally between cards, bank accounts and digital wallets, with around four billion each.

Mastercard went from reporting its total number of endpoints as “nearly 10 billion” in 2024 to “over 10 billion” in 2025, indicating a small YoY increase.

Despite launching its Pay-to-Banks solution through banks’ existing Swift connectivity in 2025 and expanding its Pay-to-Wallets solution the same way, Thunes still reports that its network has 22 billion endpoints – the same as in 2024. This year, the company expanded into Saudi Arabia and Morocco, whilst securing licences to operate in all 50 states of the US.

Mastercard Move and Visa Direct reported strong growth

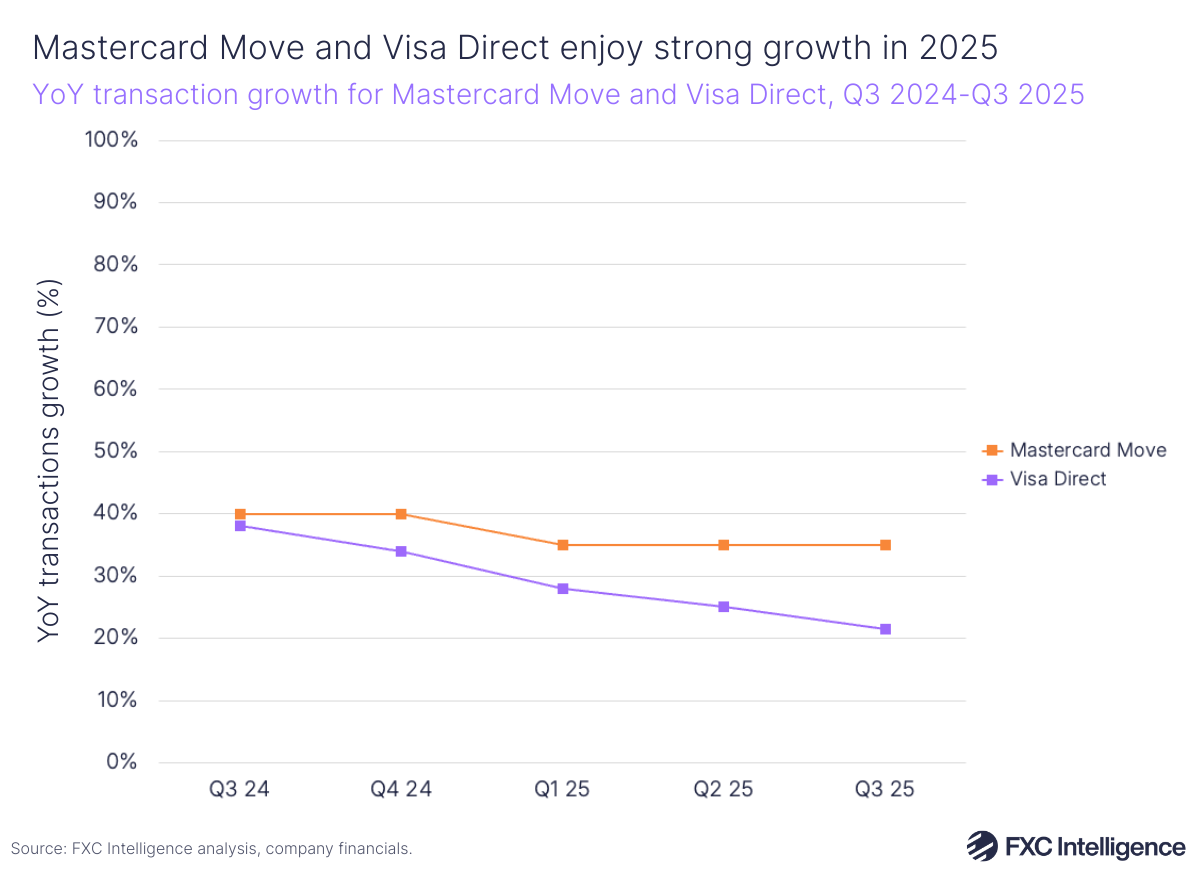

Endpoints aside, Visa and Mastercard saw their respective B2B2X network platform products perform strongly in 2025. In Q2 2025, Visa reported that transactions across Visa Direct outpaced overall transaction growth, rising to 3.3 billion transactions during the quarter – amounting to around 5% of the company’s overall transactions. In Q3, Visa Direct transactions rose 23% YoY to 3.4 billion, bringing the total for the company’s financial year to 12.6 billion, a 27% rise.

Mastercard Move also enjoyed strong growth in Q2 and Q3, seeing 35% transaction growth in both quarters. This success came as Mastercard integrated the product into core banking platforms, including InfoSys in Q3 – with CEO Michael Miebach explaining that it was enabling consumers to make outbound remittances through “billions of endpoints” in China.

Mastercard Move also grew its presence in Europe, the Middle East and Africa (EMEA) through partnerships with Worldpay and Saudi-Arabia based STC Bank. The product also saw faster growth in Canada, in part thanks to partnerships with Nuvei, which enabled instant payouts to cards, and BMO, which expanded the use of Mastercard Move across 20 more corridors.

Stablecoins became a key B2B2X focus

Unsurprisingly, stablecoins became a central part of many B2B2X strategies this year, as many players looked to expand their capabilities in line with increasing demand for the emerging technology.

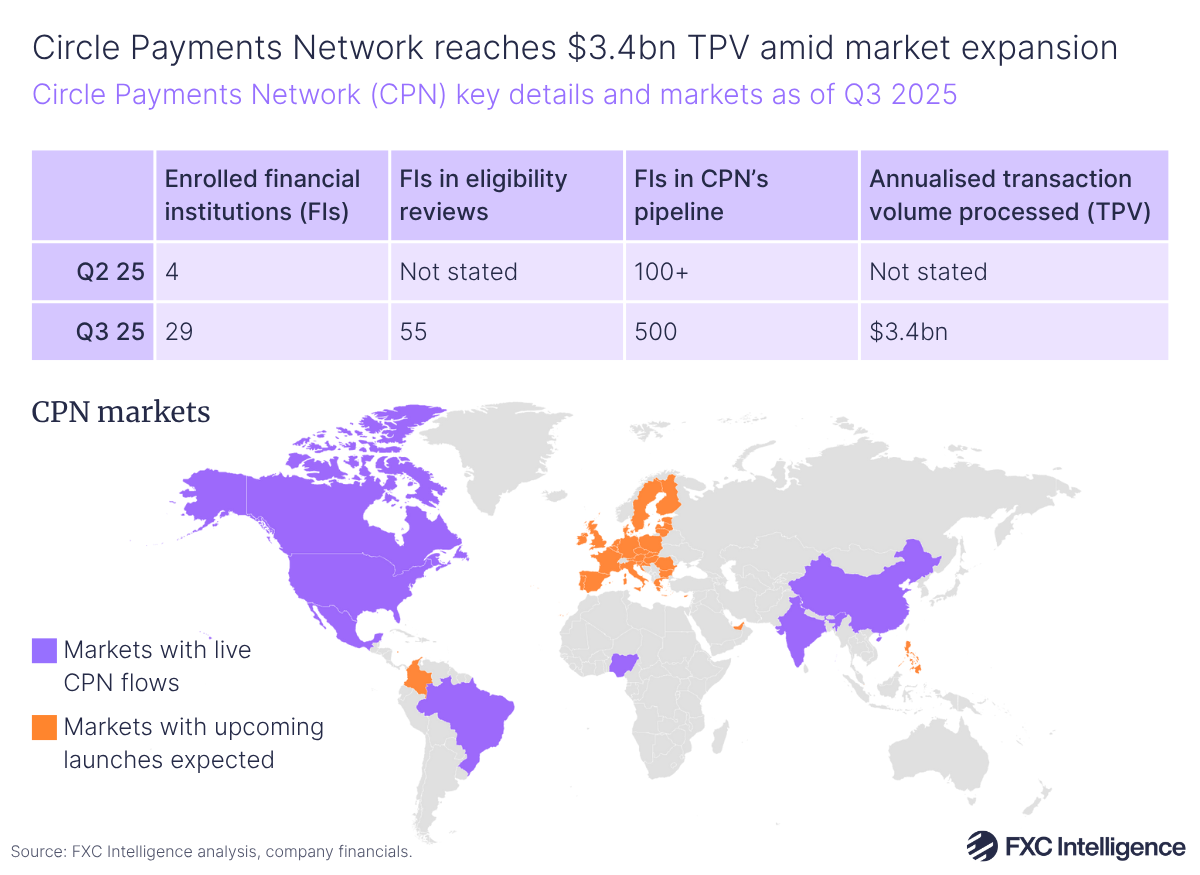

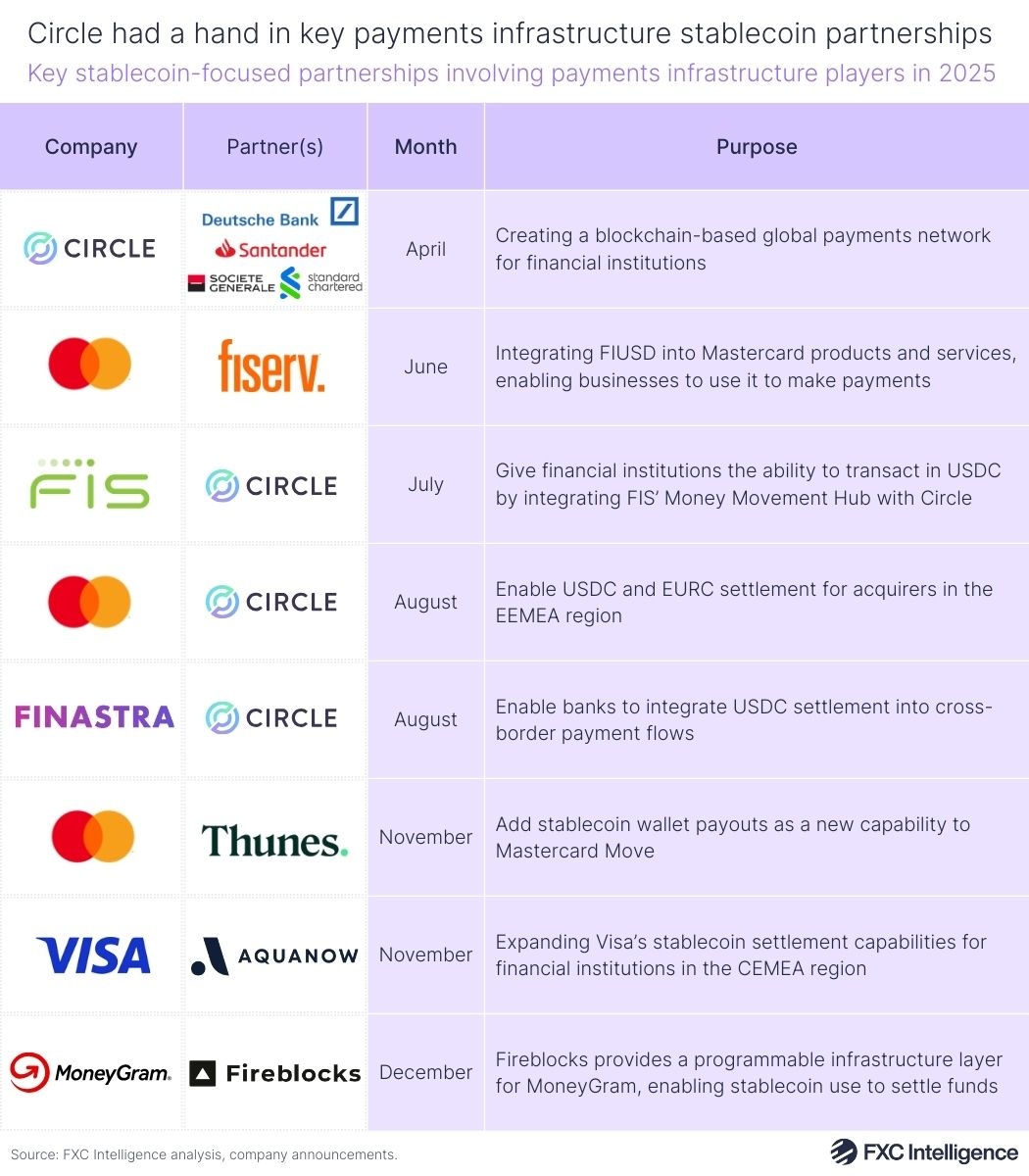

Circle, the stablecoin-powered payments infrastructure provider, launched its own B2B2X network in May dubbed the Circle Payments Network (CPN). CPN aims to become a global network of banks, payment service providers, virtual asset service providers and enterprises, which enables consumer, business, and institutional payments via stablecoins including USDC and EURC.

At Circle’s first earnings as a public company in Q2, it reported that CPN had four active partners, with 100+ in the pipeline – demand that exceeded its capability for onboarding. By the end of Q3, this number had risen to 29, while the number of companies in the pipeline had also grown to around 500. At this time, Circle also provided the network’s annualised transaction volume for the first time, at $3.4bn.

The largest players also appear to be taking note, as institutions increasingly demand faster and cheaper cross-border settlement. Visa began leveraging stablecoins including USDC for settlement in 2025 via an integration with digital asset platform Aquanow, which enables Visa’s partner banks and acquirers in Central and Eastern Europe, Middle East and Africa to access always-on, near-instant cross-border settlement while reducing reliance on correspondent banking systems.

Thunes also embraced stablecoins, launching a Pay-to-Stablecoin-Wallets solution that supports USDC and USDT in October, enabling banks, fintechs and other financial institutions to send and receive stablecoin payments.

During November’s Singapore FinTech Festival, Thunes also unveiled a collaboration with Mastercard that will see Mastercard Move facilitate real-time payouts to stablecoin wallets via Thunes’ Direct Global Network. The move represented a step towards a completely new endpoint for the B2B2X platform, giving banks and payment providers greater flexibility in delivering funds.

What’s next for B2B2X?

With the biggest B2B2X and payment infrastructure players making quick progress implementing and leveraging stablecoins to speed up cross-border settlement and keep costs competitive, it seems certain that focus on the technology is only set to increase.

Paired with the passing of the GENIUS Act in the US in July, as well as increasing clarity surrounding stablecoins elsewhere worldwide, confidence in utilising them appears to be on the rise. This should lead to further and increased adoption of stablecoins for settlement throughout 2026 and beyond.

Stablecoins may also have a hand in making cross-border transfers significantly faster and cheaper in emerging markets. African payments companies Onafriq, Flutterwave and Yellow Card joined Circle’s CPN in April 2025 to utilise the technology throughout the continent. Interoperability should also continue to improve across the globe, in the form of further partnerships between domestic real-time payments systems.

In the longer term, geopolitical shifts could also influence how payments infrastructure is used, with the likes of the BRICS group (including Brazil, Russia, China and India) and countries across Africa looking to reduce dependence on the US dollar – especially after President Trump rolled out tariffs earlier this year. This could see some countries increase focus and investment in local currency settlement without using the US dollar.

However these trends play out, it appears that partnerships will remain a key part in attempts to reduce the cost of cost-border transfers and expand the reach of banks and other financial institutions.