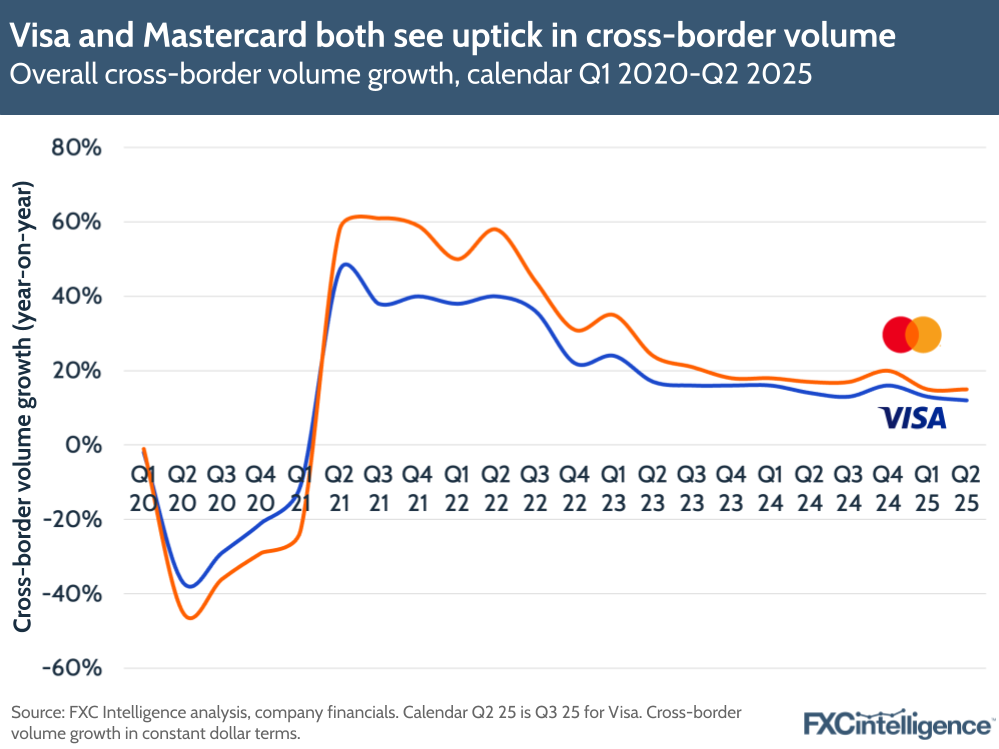

Visa and Mastercard have announced their calendar Q2 2025 results (reported as Q3 2025 for Visa), with both continuing to highlight cross-border as a major driver to their businesses. Despite volatility and some headwinds in core markets, transactions and volumes processed are on the rise for both companies and in many cases outpacing general volume growth metrics.

Both companies also saw rises across their network platform products Visa Direct and Mastercard Move and discussed the potential impact of stablecoins and AI on their businesses.

Visa’s Q3 2025 results highlights

Visa surpassed $10bn in quarterly revenue for the first time, with net revenue rising 14% to $10.2bn. This was the fastest revenue growth the company has seen since Q4 2022, driven by cross-border volume rising 12% (11% excluding intra-Europe) while overall payments volume grew 8%.

International transaction revenue rose 14% YoY to $3.6bn, benefitting directly from cross-border growth. The company saw processed transactions grow 10% to over 65 billion, with cross-border ecommerce rising 13%. Cross-border travel-related flows grew 9%, despite the company noting persistent FX volatility and headwinds in key corridors that were affecting inbound travel from the US to Canada.

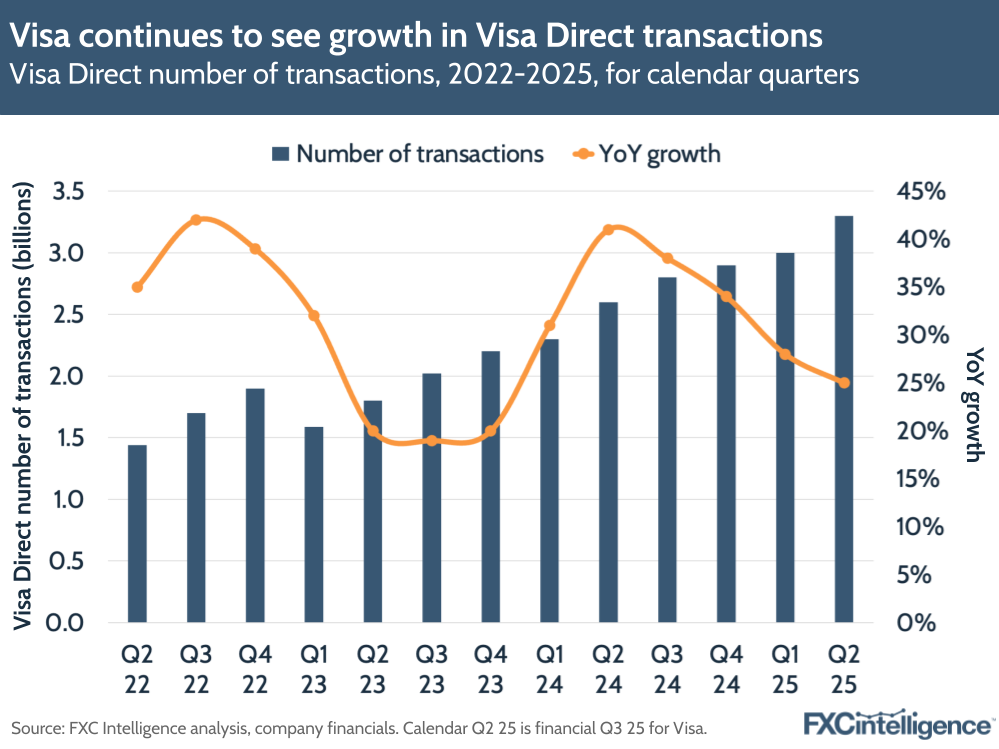

Transactions across Visa Direct – Visa’s B2B2X remittance network – continue to outpace overall transaction growth at 25%, rising to 3.3 billion transactions during the quarter. This amounts to around 5% of the company’s transactions overall.

The service could grow further with new clients onboarded, including one of the biggest banks in the UAE, ADIB, which is using it to power a new remittances programmes, alongside four Bangladeshi banks using Visa Direct for outbound payments. Money transfer provider Paysend, meanwhile, is expanding its use of Visa Direct to other cross-border use cases including gig worker and payroll disbursements.

Mastercard Q2 2025 results highlights

Mastercard’s net revenue grew 17% – its fastest growth since Q2 2022 – to $8.1bn. It saw cross-border volume rise by 15%, contributing to 13% growth in the company’s Payment Network net revenue.

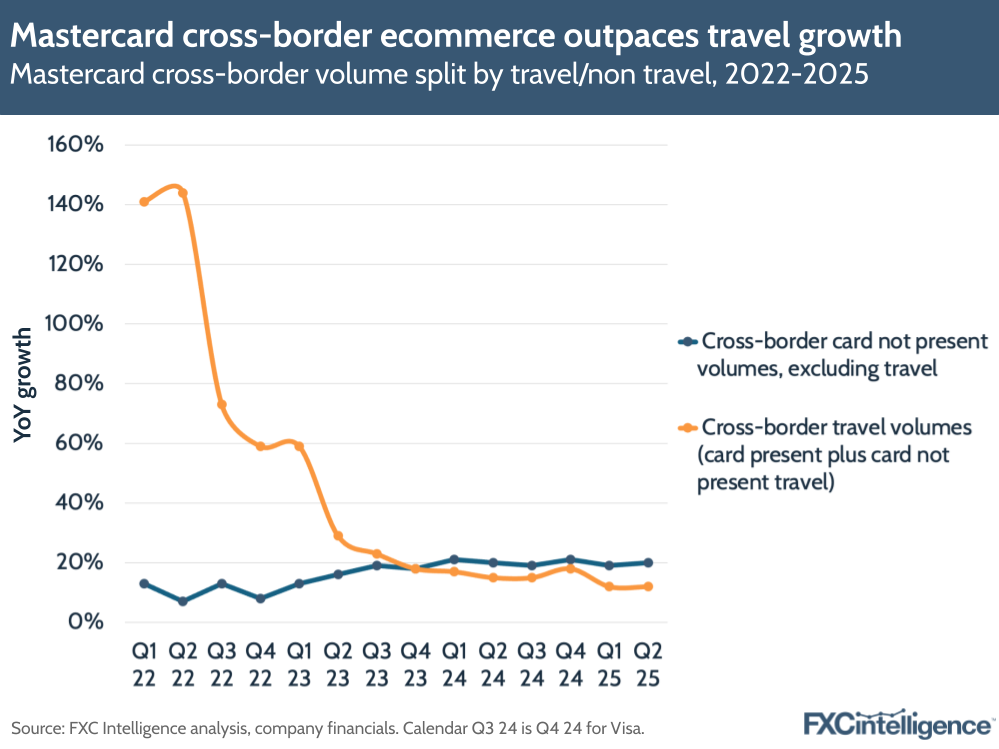

Cross-border volumes were driven by travel and non-travel related spending, though there has been a continued shift over time in how fast these are growing. Non-travel cross-border card-not present volumes grew 20% while cross-border travel rose 12% in Q2 2025, reflecting an ongoing trend in recent quarters where the former has outpaced the latter.

Mastercard CFO Sachin Mehra said during the earnings call that travel volumes have moderated in some Middle East and Africa markets due to tougher comparisons, new rules being enforced and geopolitical conflict, as well as the timing of Easter. However, he reiterated that the cross-border business is highly diversified, with no single cross-border corridor pair accounting for more than 3% of cross-border volume in 2024.

Cross-border travel volumes account for roughly 60% of Mastercard’s total cross-border volumes, versus 40% for cross-border non travel. Strong consumer spending is driving resilience, with affluent cardholders spending twice as much overall and three times more on cross-border. Added to this, cross-border assessments – the income Mastercard gets from cross-border-associated fees on its network – rose 15%, faster than domestic assessments growth and gross dollar volume growth, both 9%.

Mastercard Move is also on the rise, having seen 35% transaction growth and particular strength in Canada through a new partnership with Nuvei to enable instant payouts to cards, as well as BMO Canada expanding use of Mastercard Move across 20 more corridors.

The impact of stablecoins on Visa and Mastercard

On stablecoins, Visa CEO Ryan McInerney said during the call that the company sees two key areas for the technology – the first being in emerging markets where fiat currency is volatile or banking infrastructure is limited and the second being in cross-border money movement for both B2B payments and consumer remittances. The company has begun piloting stablecoin-based treasury operations and cross-border transactions by partnering with stablecoin payment infrastructure provider Yellow Card in Sub-Saharan Africa.

Visa also gave an update on its Visa Tokenized Asset Platform, which allows banks to issue and transfer fiat-backed tokens over blockchain networks. Visa has added support for three stablecoins – Circle’s EURC, Paxos’s USDG and PayPal’s PYUSD – and also added support for two more blockchains, Stellar and Avalanche, in addition to existing supported blockchains Ethereum and Solana. Through the company’s network, it is able to accept and convert the coins to over 25 traditional fiat currencies worldwide.

Mastercard didn’t go in-depth on stablecoins during the earnings call but re-emphasised its vision to support stablecoin on/off ramps, interoperability and compliance tools through partners and wallets. Mastercard CEO Michael Miebach said that the company sees stablecoins as “just another currency”, with the potential to be “additive” to its network.

Earlier in July, Mastercard held a special call about stablecoins in which it highlighted three opportunities for the technology, including enabling fiat-to-stablecoin and stablecoin-to fiat transactions; allowing financial institutions and wallets to issue or distribute stablecoins; and expanding its B2B services and cross-border money movement to include digital currencies. It confirmed that Mastercard Move has been expanded to include stablecoin-based cross-border transfers.

As Visa and Mastercard both make money from being intermediaries charging transaction fees for payments, it is unsurprising that both companies are increasingly talking about stablecoins, as it has been suggested they could bypass traditional payment rails to reduce fees and enable faster, more seamless cross-border payments. However, there are a number of complexities and challenges involved in this, as we highlighted in our comprehensive industry primer on stablecoins last month.

How can I compare the cost of cross-border payments transactions worldwide?