Circle’s Q2 2025 results, its first earnings as a public company, demonstrate both growth and broadening plans for the cross-border payments space.

Stablecoin major Circle has published its Q2 2025 earnings, its first set of numbers as a public company following its blockbuster IPO in early June. With strong top-line growth, the company’s results have been met with a strong response from investors, with its share price jumping on the publication of the numbers.

However, the earnings call also saw the company provide updates on a number of cross-border payments-focused solutions, primarily the Circle Payments Network, as well as launching a blockchain specifically designed for the financial services industry that is set to have several highly beneficial features for cross-border transactions in particular.

In this report we dig into Circle’s latest numbers, as well as consider how its evolving product set is catering to the cross-border payments industry.

Circle’s top-line Q2 2025 results

Q2 2025 saw Circle report a 53% rise in total revenue and reserve income to $658m, largely aided by the growth of the amount of its primary stablecoin USDC in circulation. The second largest stablecoin in the world by circulation, USDC saw a 90% increase in circulation between the end of Q2 2024 and the end of Q2 2025 – to $61.3bn. This has continued to grow since, reaching $65.2bn as of 10 August.

The volume of on-chain transactions using USDC, which covers all transactions on public blockchains using the stablecoin, including buying cryptocurrency and sending payments, has climbed even further, rising 436% YoY to $5.9tn.

The number of holders of USDC has also increased, with meaningful wallets, defined as those holding at least $10 of USDC, increasing 68% YoY, and 16% quarter-on-quarter, to 5.7 million.

This growth has helped drive a 52% YoY increase in adjusted EBITDA to $126m. This translates into an adjusted EBITDA margin, when defined as a margin of total revenue, of 19% for Q2 – slightly down on Q1’s 21% but in line with Q2 24. However, Circle defines adjusted EBITDA margin as a margin of total revenue less distribution, transaction and other costs, and reports this metric as 50%. This is slightly down on Q1’s 53% but up from 45% in Q2 2024.

Circle also reported a $482m net loss for the quarter, which it attributed to IPO-related non-cash charges, namely stock-based compensation from IPO-related vesting conditions and an increase in the fair value of convertible debt as a result of its climb in share price. This follows Q1 seeing positive net income, and there is currently no indication of negative income in future quarters being likely.

In addition to sharing numbers, the company highlighted growing use of USDC across a wide variety of use cases, including many in cross-border payments, spurred on by the passing of the Genius Act. These included Remitly, MoneyGram, Stripe and Zepz under payments and remittances, as well as Fiserv, FIS and Corpay under core banking and treasury management.

Potential revenue challenges: From Coinbase to reserve income

While Circle’s revenue performance is strong, there are some areas that present potential challenges for the company. One area, which we first highlighted in our teardown of the company’s IPO prospectus, is the share of USDC held on Coinbase’s platform. As USDC was originally co-owned by Circle and Coinbase, the two companies have had a Collaboration Agreement since 2023 that sees Circle incur distribution costs when USDC is held on Coinbase’s platform.

As a result, increases on Coinbase’s platform come with increased costs, which is reflected in a rise in Circle’s overall distribution costs. The company reported that its distribution and transaction costs across H1 2025 climbed by 68% YoY to $304m, which was largely driven by $192m in transaction costs paid to Coinbase. Other partnerships also have incurred costs for Circle, with the company attributing $111m of its H1 distribution costs to payments to other partners.

For Circle, it is therefore more desirable to increase the share of USDC held on its own platform, and here the company has made significant gains. While its share still remains small, it has reached double figures for the first time, climbing from 2% in Q2 2024 to 10% in Q2 2025.

Meanwhile, Circle remains highly reliant on reserve income, the interest income it receives from the reserves it holds to back the USDC in circulation. As of Q2 2025, this accounted for over 96% of its overall revenue, and means the company is highly exposed to changes in interest rates, which has led it to previously provide very broad guidance for its FY performance based on different moves in interest rates.

In recognition of this, Circle has been making moves to diversify its revenue, including through the Circle Payments Network (CPN) as well as trading-related products. In Q2 2025 the company saw growth in other revenue outpace the growth of reserve income revenue, at 253% YoY, and further rollout of CPN, as well as the launch of Arc, a new blockchain tailored to stablecoins, is set to grow this further.

With the interest rate environment having been less favourable in the last few quarters, Circle has seen its reserve return rate drop from the levels it saw in H1 2024. However, this drop has been offset by significant growth in USDC in circulation, which has meant that reserve income has nonetheless climbed.

Circle Payment Network: Initial insights and strategy

In May this year, halfway through the quarter, the company launched its stablecoin-based cross-border payments network Circle Payments Network, and this earnings call provided a key opportunity for the company to update the market on CPN.

While the company did not share financial metrics, it did report that CPN now has four active partners – RedotPay, Conduit, Tazapay and Alfred – and that there were a further 100+ in the pipeline. On this, the company said that it is currently seeing greater demand for onboarding than it has capacity for, and so is working to improve this with the rollout of self-service tools.

Circle also reported that CPN is initially active on only four corridors – Hong Kong, Brazil, Mexico and Nigeria – although the company plans to roll out support for significantly more in the latter half of this year. It expects to see this, along with the increased number of partners, drive accelerated growth across H2 2025.

Speaking during the earnings call, Circle CEO Jeremy Allaire said the company wanted to enable money flows on CPN to “work seamlessly across major developed markets and more emerging and developing markets”, which made “activation of corridors” a key priority.

“Our ultimate ambition is that thousands of members will join CPN and participate in a wide array of payment flows,” he added.

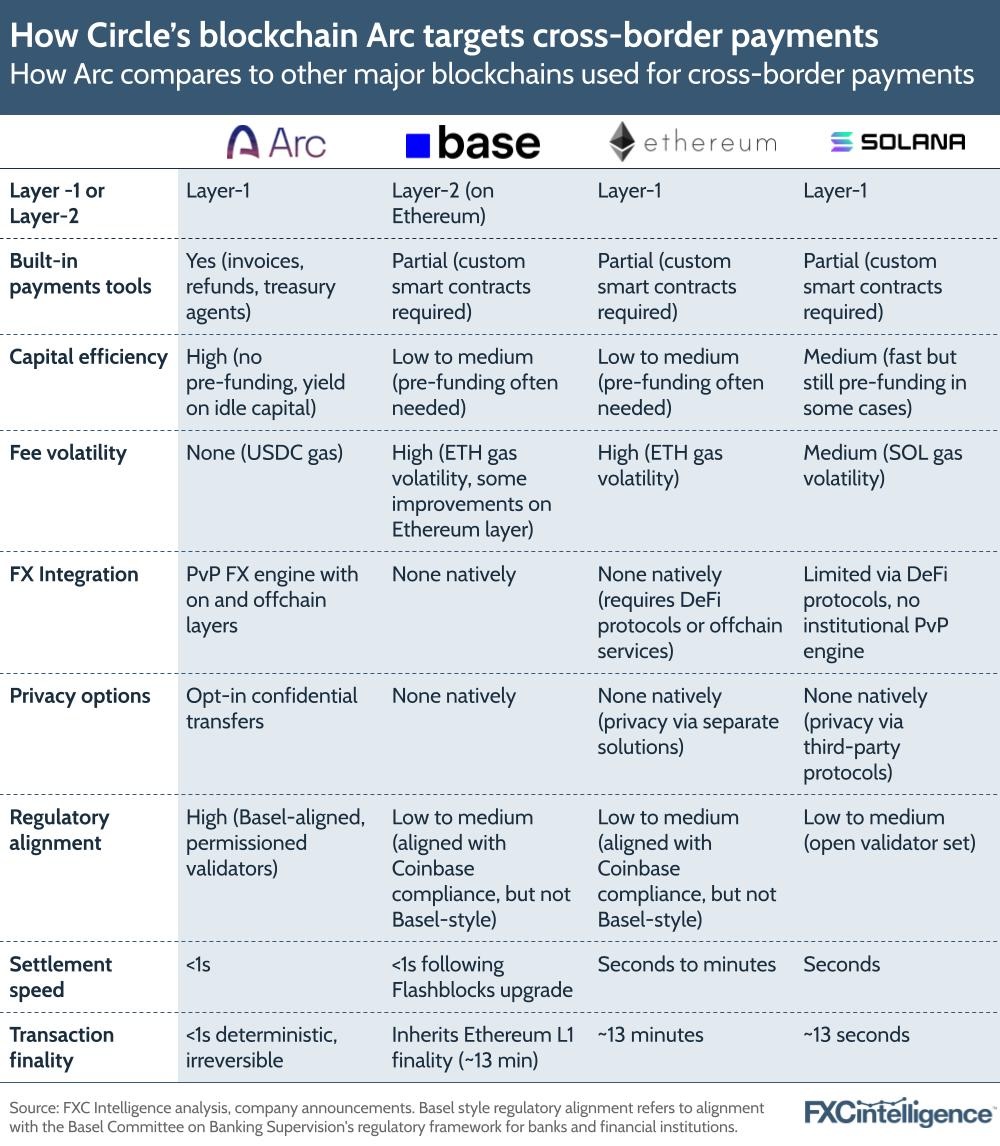

Introducing Arc: Circle launches cross-border payments-focused blockchain

Alongside providing an update on CPN, Circle also announced the launch of Arc, a planned blockchain that has been tailored to the needs of financial institutions moving money using stablecoins.

Described by Allaire as “a purpose-built blockchain for stablecoin finance for payments, FX and capital markets”, Arc will initially see a private testnet launch within the next month, with details of its design currently available via a litepaper on Arc’s dedicated website, although there is not yet a date for its full-scale launch.

However, the blockchain includes features that could prove to be extremely powerful for the cross-border payments industry in particular. An open Layer-1 blockchain, as opposed to a Layer-2 blockchain built on top of another existing blockchain, Arc is designed to be enterprise-grade, complying with the Basel Committee on Banking Supervision’s regulatory framework for banks and financial institutions, and includes sub-second settlement finality.

It also contains a number of features that are extremely rare natively on payments-focused blockchains, but which combat areas where blockchains’ typical operational structure creates friction with how the financial industry operates.

The first of these is how gas fees, the fees charged to deliver a transaction on a blockchain, are charged. On other chains, these vary in price depending on the level of the traffic on the network, and in some cases can at times jump to prohibitively high levels, as well as being incurred in the native token, which is typically a non-fiat currency pegged cryptocurrency. Arc charges gas fees in USDC, meaning they are charged in dollars, and crucially are designed to be fixed so that they can be accurately predicted as part of financial models.

Second is the ability to make transfers confidential, which is necessary for some regulatory requirements but is not possible natively within most major blockchains, particularly Ethereum, Solana and Base, the three biggest blockchains for USDC in terms of value held onchain.

Finally, Arc also features a built-in FX engine, which is designed to bring institutional-grade foreign exchange trading and settlement onchain. This is achieved through a dual-layer approach, with an on-chain settlement layer and an off-chain request-for-quote layer that allows institutional takers to request FX prices from a network of vetted market makers, with sub-section completion.

At launch, Arc’s FX engine will support both USDC and EURC, Circle’s US dollar and euro-denominated stablecoins, but over time the company plans to add wider multicurrency support.

The blockchain has the potential to combat key frictions for cross-border payments amid rapidly rising interest in stablecoins within the space, but it also has the potential to significantly benefit Circle and its wider strategy. It is set to underpin Circle Payments Network once it launches, helping to drive adoption, and has the potential to be a significant source of non-reserve revenue through its gas fees.

FY projections and future growth

During the earnings call, Circle highlighted the recent passing of the GENIUS Act in the US, which has been central to increased financial industry interest in stablecoins, with Allaire saying that the company was “uniquely positioned to lead in the mainstream adoption of blockchain and stablecoins”.

This approach has seen the company provide strong full-year projections, which include an expected 40% YoY rise in USDC in circulation that would see it achieve average USDC in circulation of $47bn and year-end circulation of $62bn.

If the company’s reserve return rate remains at its H1 2025 average, this would see reserve income climb 17% YoY to around $1.9bn. The company also projects other revenue to reach $75-85m for the year, which would see other revenue at a similar rate or slightly lower in H2 than that generated in H1.

Combined, this would see its FY 2025 revenue reach around $2bn, at the upper middle end of the previous FY projections it shared that were based on interest rate changes, despite interest rates being lower than those seen in FY 2024.