Visa and Mastercard have shared their latest earnings for calendar Q3 2025 – Visa refers to this as Q4 2025 as part of its financial year – with cross-border volume continuing to be a key driver for both businesses.

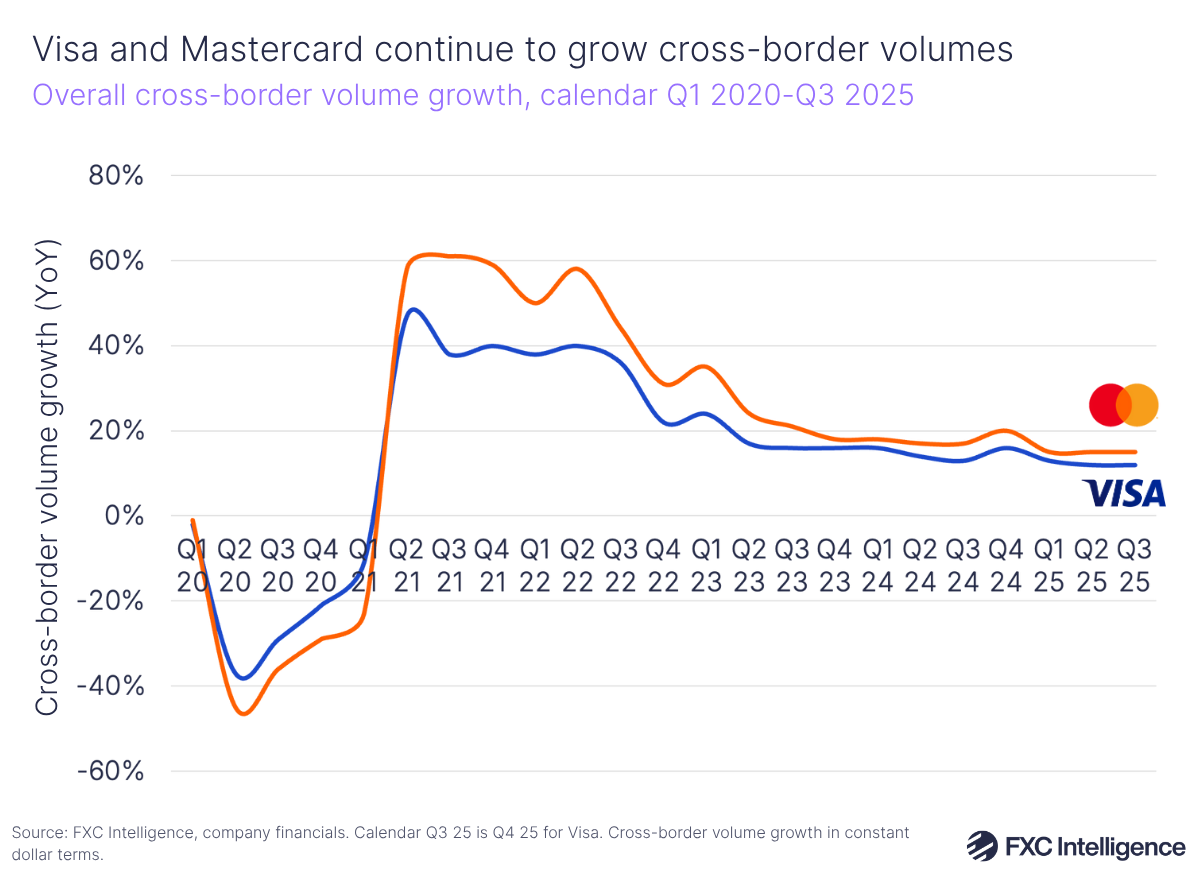

While neither company reports its cross-border volumes directly, Visa said that total cross-border volumes rose by 12% in financial Q4 2025 in constant currency terms, while for its full financial year (spanning calendar Q4 2024 to Q3 2025), cross-border volumes rose by 13%. By comparison, Mastercard’s quarterly cross-border volumes grew slightly faster in Q3 2025 at 15%.

Growth in cross-border ecommerce, as well as sustained post-pandemic travel, is propelling both companies, with a key theme in the calls being the ability for them to serve a higher number of endpoints, in turn driving transactions not just across cross-border card spending but also through money movement for businesses and consumers via the company’s B2B2X platforms Visa Direct and Mastercard Move. Stablecoins and AI – two of the top trends of the moment – are also driving actionable growth for the companies.

Visa Q4 2025 earnings highlights

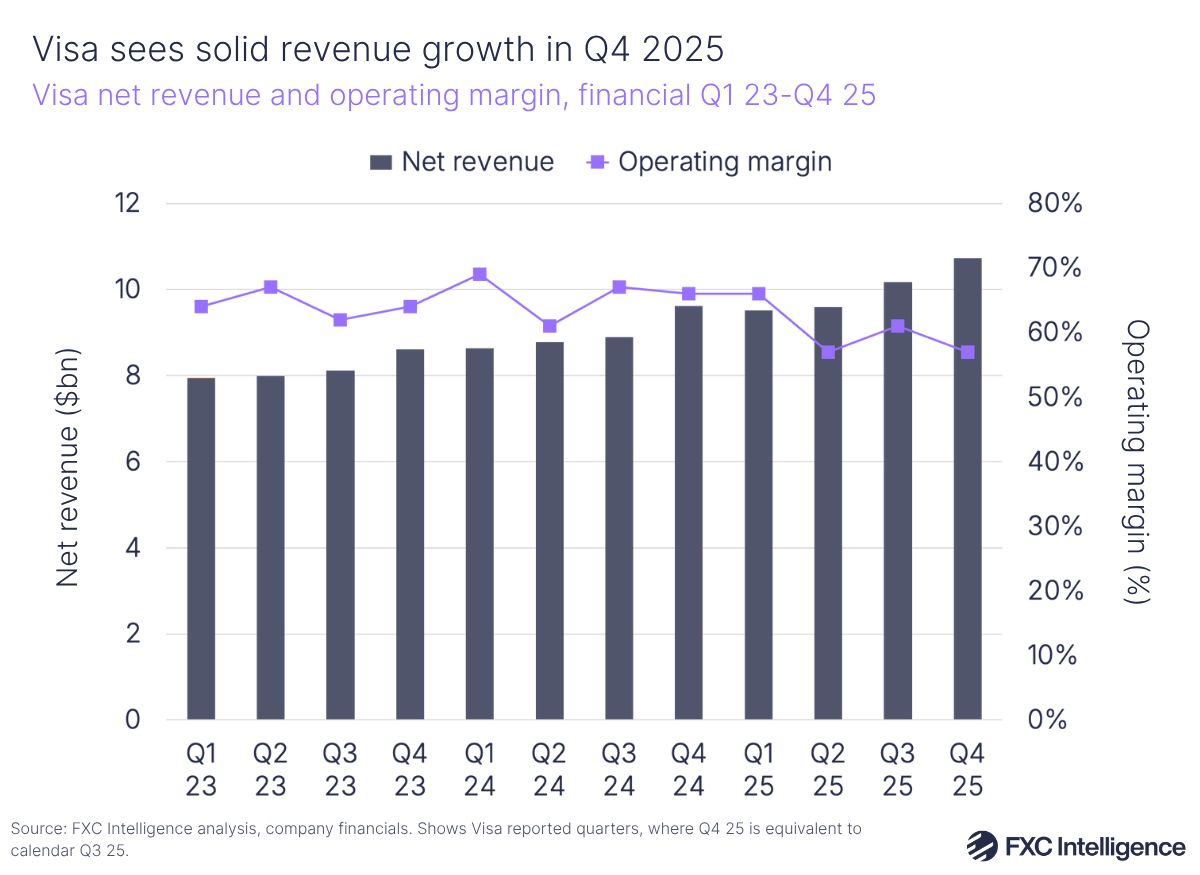

Visa reported continued solid growth in its financial Q4 2025 results (calendar Q3 2025), with CEO Ryan McInerney noting that “continued healthy consumer spending” drove net revenues to rise 12% YoY to $10.7bn during the quarter. However, a 40% rise in operating expenses to $4.6bn drove an overall operating margin of 57%, down from 66% in Q4 2024.

Cross-border volume growth continues to be a key growth driver, rising 12% in constant dollars YoY (11% excluding intra-Europe) in Q4 2025, which was faster than 9% growth for Visa’s overall payments volume. Processed transactions grew by 10% to 67.7 billion, driving processed transactions for the full financial year up 10% to 257.5 billion, in line with previous years.

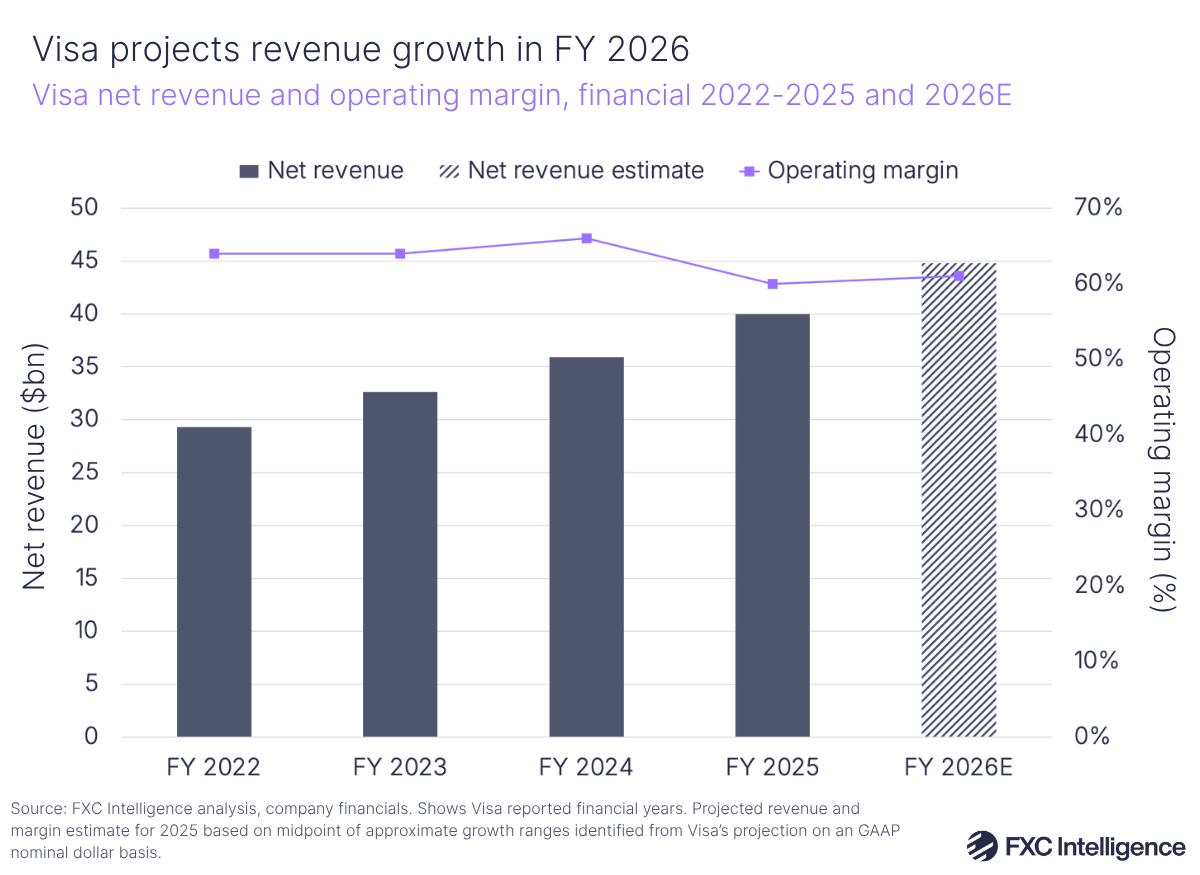

For its full financial year, Visa saw an 11% rise in net revenues to $40bn, with payments volume rising 8% while cross-border volume rose 13% both overall and excluding intra-Europe. On an annual basis, cross-border volume growth was slightly down from financial 2024’s 15% while the overall payments volume growth figure remained the same at 8%.

Guiding for FY 2026, the company expects net revenue to grow in low double-digits and operating expenses to grow at high single digits on a GAAP nominal-dollar basis. Based on our estimates, this would see revenue surpassing $44bn and the company’s operating margin reach around 61%.

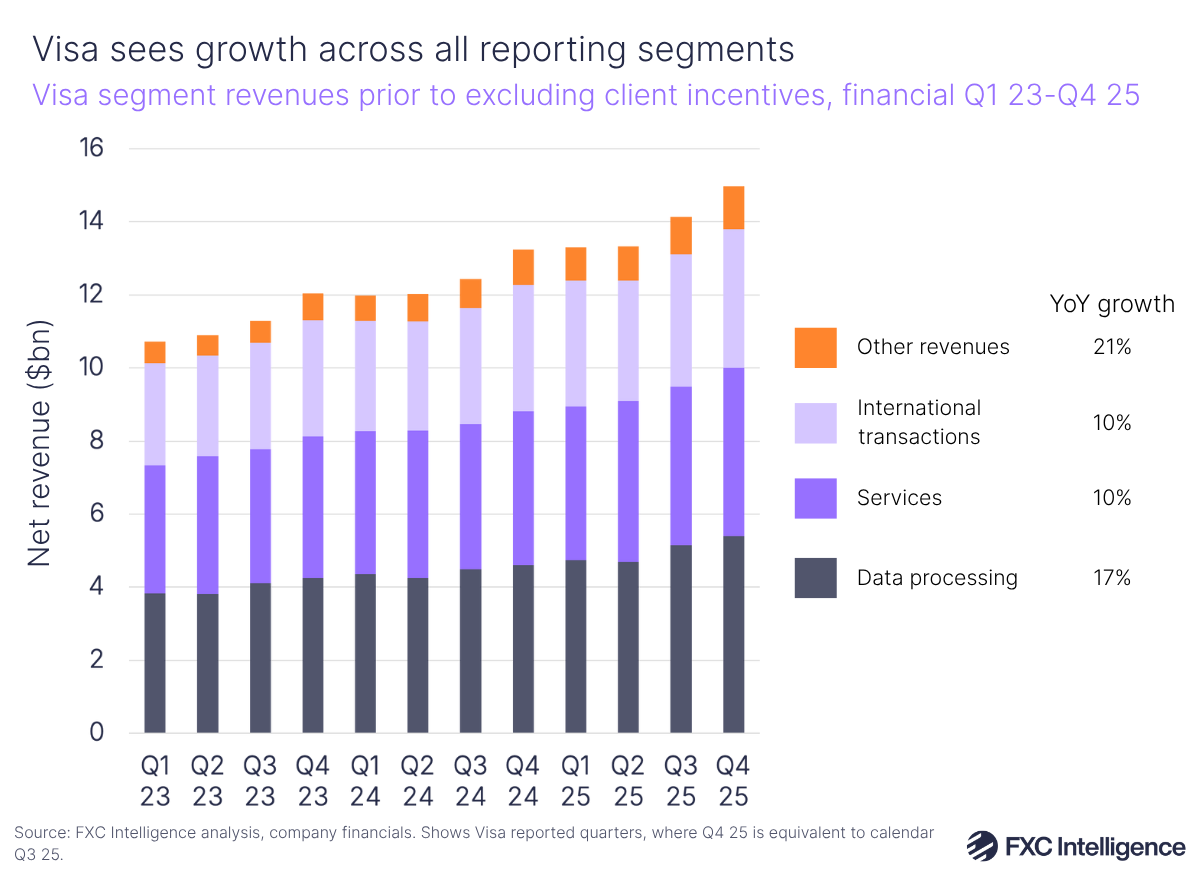

Visa’s international transaction revenues – largely driven by its cross-border volumes excluding transactions within Europe – grew by 10% to around $3.8bn in Q4 2024, meaning they continue to make up around a quarter of the company’s overall revenues. By comparison, data processing revenues grew 17% to $5.4bn, though the company noted that this was accelerating specifically in higher-yielding cross-border regions. Services revenues grew 10% to $4.6bn, while Other revenues grew at the fastest pace, seeing 21% growth to account for $1.2bn of Visa’s total.

Visa noted the particular impact that ecommerce (card not present ex travel) was having on cross-border volumes. Cross-border ecommerce rose 13%, having remained strong for the last eight quarters, and now accounts for 40% of the company’s total cross-border volume, with this expected to grow at a faster rate than cross-border travel.

Having said this, the company noted that the rate of cross-border travel spending improved sequentially to 10%, continuing to grow above pre-Covid-19 levels. Linked to cross-border growth were a number of factors, including rising commercial volumes aided by Visa’s efforts around virtual cards and improvement in outbound flows across Central and Eastern Europe, Middle East and Africa.

Cross-border is forming a focal point of Visa’s strategy, particularly around Visa Commercial & Money Movement Solutions (CMS) – its suite of services enabling businesses to move money globally. CMS revenue grew by 15% in Visa’s FY 2025, spurred by its Commercial Solutions business. The company is looking to bolster this further by investing in “specific commercial vertical opportunities” and building out cross-border capabilities through Visa Direct, its B2B2X platform enabling money movement for banks and other financial institutions.

Visa Direct transactions rise as network grows

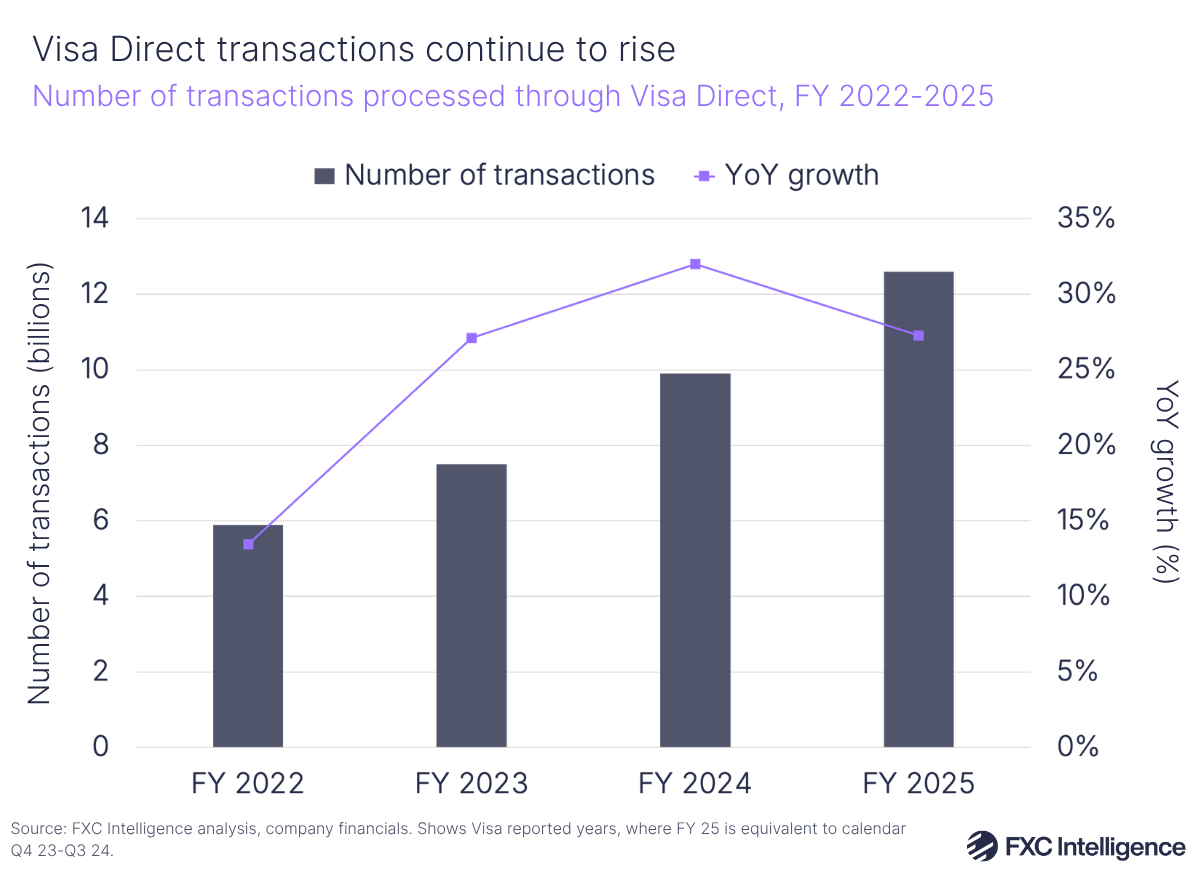

Visa Direct saw transactions rose by 23% to 3.4 billion during financial Q4 2025, bringing the total for the company’s financial year to 12.6 billion, a 27% rise.

Similar to the previous quarter, this means that Visa Direct transactions continue to account for around 5% of Visa’s transactions overall, though this share is gradually growing as transactions via the platform grow faster than Visa’s overall payments transactions growth.

Though the growth in Direct transactions for the full year was slightly lower than FY 2024’s 32%, Visa has continued to expand its network, serving payouts to approximately 12 billion endpoints in FY 2025, up from 11 billion the previous year.

Visa also called out a number of significant partnerships signed during the quarter, including signing with East African bank KCB, Saudi Arabian bank Al Rahji and Malaysia’s largest e-wallet Touch ‘n Go.

Finally, Visa referenced its recent announcement that it was launching a stablecoin pilot through Visa Direct, which will allow businesses to prefund transfers with stablecoins to help them reduce exposure to local currency volatility. Overall, the company is making progress in its pursuit of an $80tn opportunity for domestic and cross-border flows, as we discussed recently with newly appointed Global Head Vira Platonova.

Mastercard Q3 2025 earnings

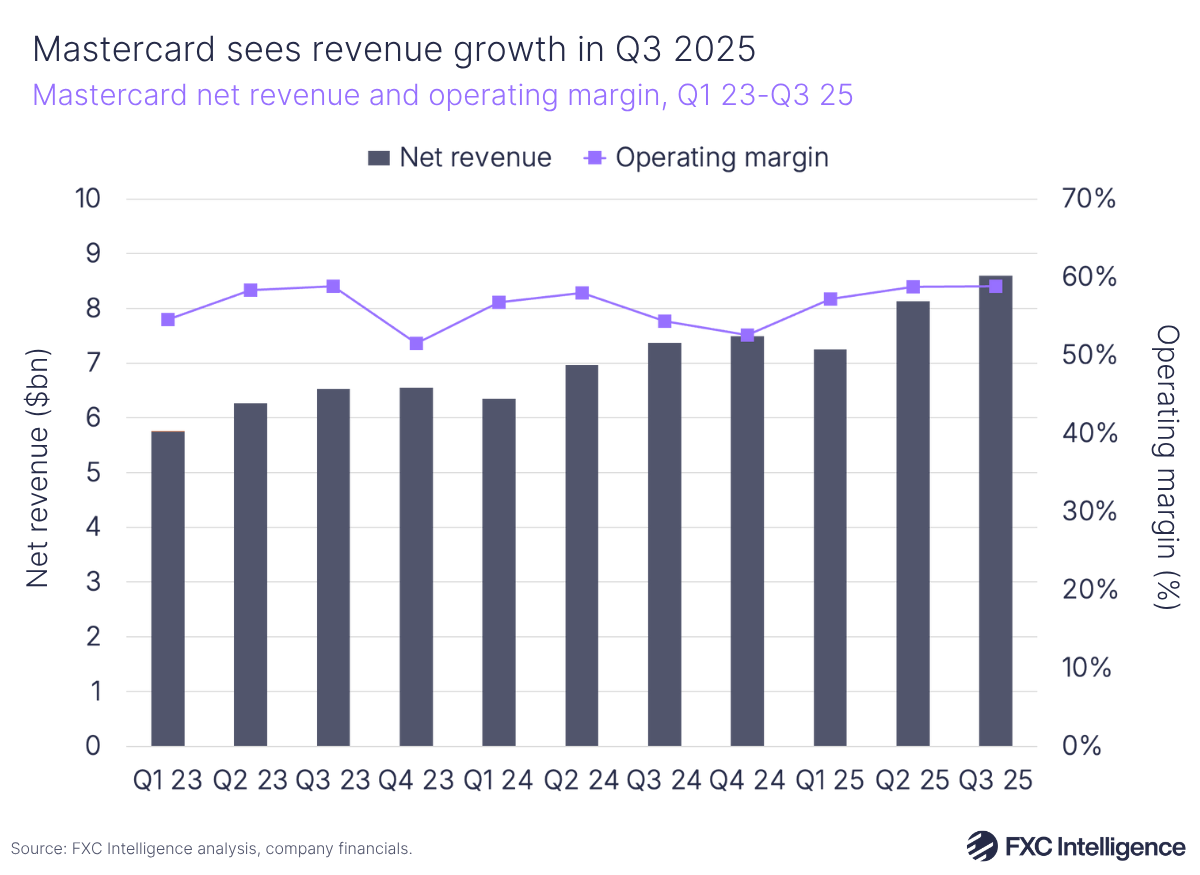

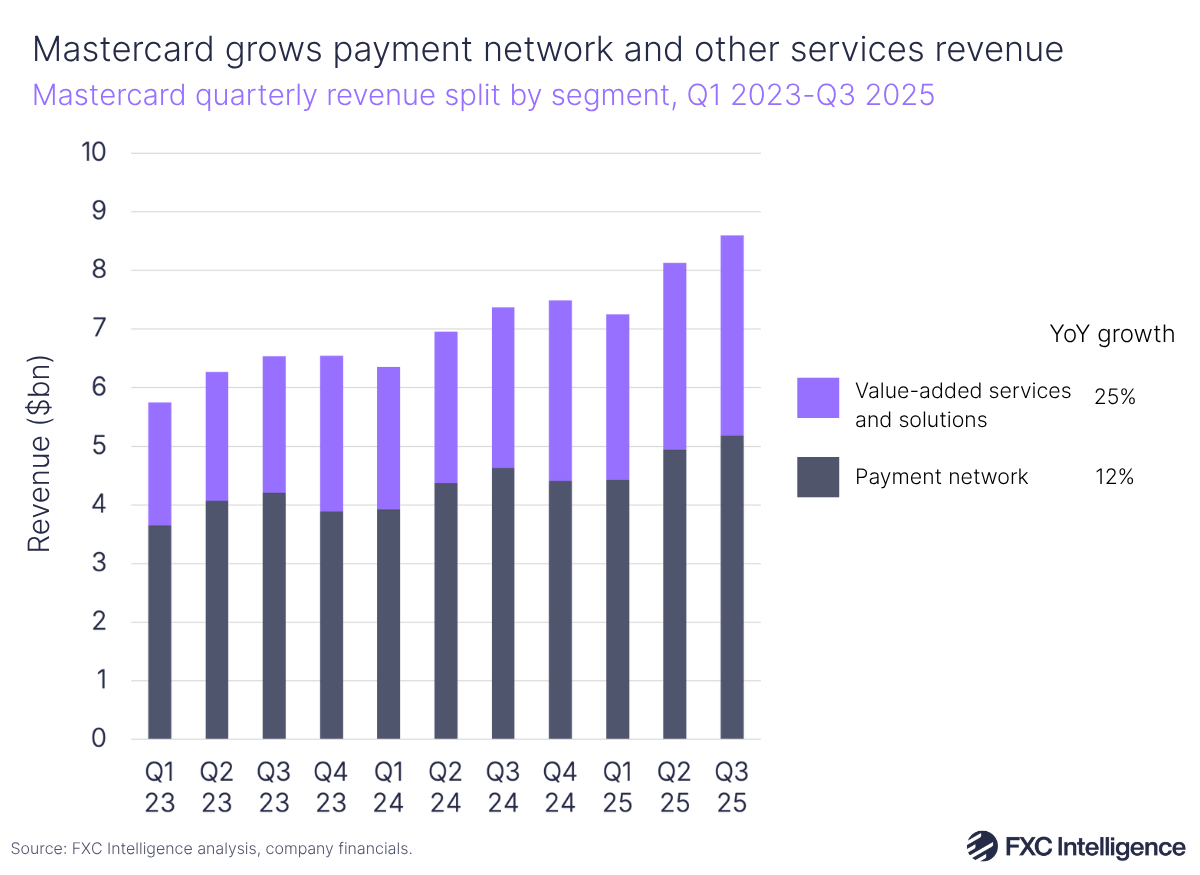

Mastercard reported that its net revenue rose 17% (or 15% on a currency-neutral basis) to $8.6bn in Q3 2025, with CEO Michael Miebach referencing “healthy consumer and business spending” in the quarter, with a supportive macro environment. Combined with a 26% rise in operating income, this gave the company an operating margin of 59% for the quarter.

The company’s payment network net revenue rose 12% YoY (10% on a currency neutral basis) to $5.2bn, accounting for 60% of Mastercard’s overall revenue share, on the back of growing transaction and volume growth. Having said this, the company’s value-added services and solutions segment continued to grow faster than network revenue in Q3 2025, at a rate of 25% to $3.4bn.

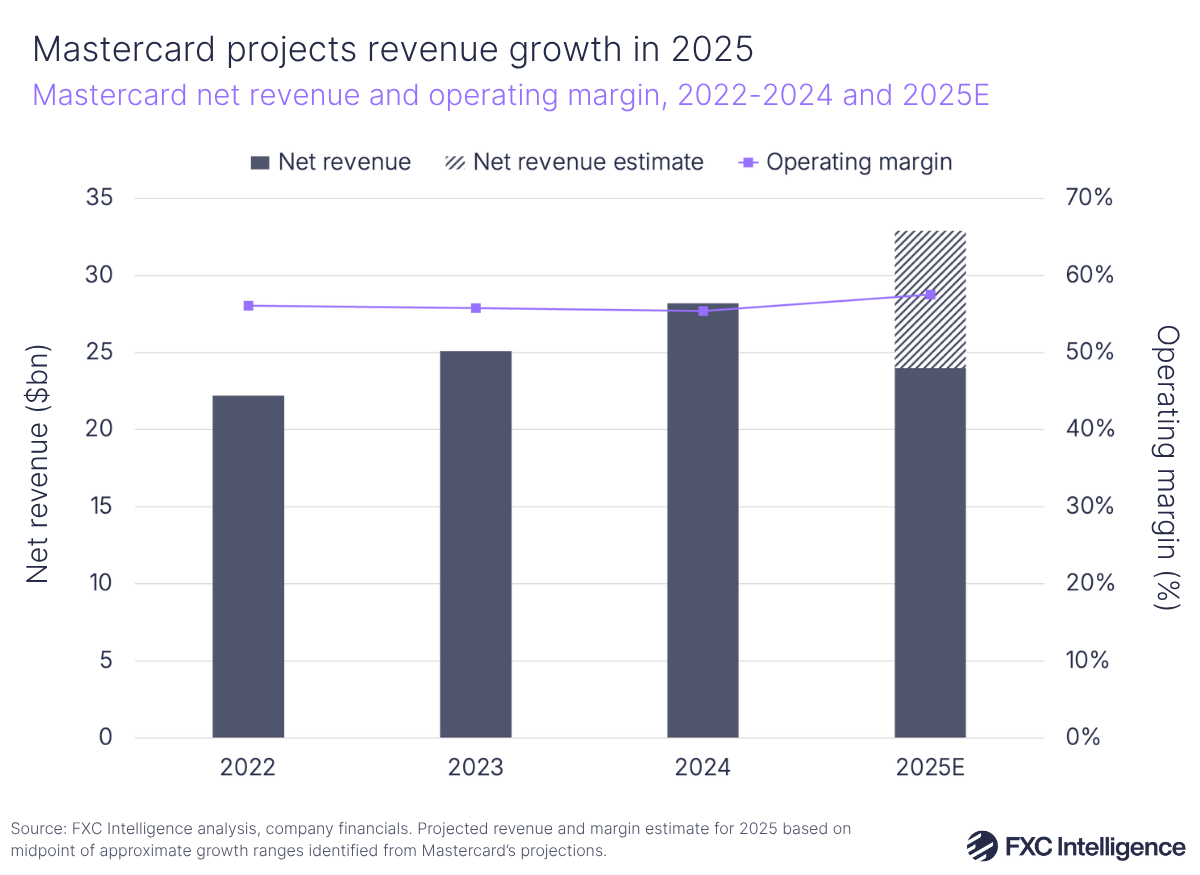

For its full-year results, Mastercard is forecasting GAAP growth at the high end of mid-teens and operating expenses to rise at the low end of low-double digits. Based on our estimates, this would see it surpassing $32bn in revenues and provide an operating margin at around 57-58%.

For Mastercard, 15% cross-border volume growth reflected continued growth in travel and non-travel related cross-border spending. Cross-border assessments – charges based on transactions through Mastercard-branded cards where the merchant country and issuing country are different – rose 18% to $3.3bn. This metric continues to grow faster than domestic assessments, which rose 6% and accounted for $2.8bn.

Intra-Europe cross-border volume grew 16% during the quarter, faster than 13% growth for other cross-border volumes. Meanwhile the company continues to see faster growth in its cross-border card not present volumes, which exclude travel, at 21%, while cross-border travel (i.e. card present plus card not present travel) rose by 11%.

During the company’s earnings call, Mastercard CFO Sachin Mehra said that “winning the right portfolios” was helping drive Mastercard’s sustained cross-border growth. In particular, he referred to affluent, travel-oriented companies – including a recent co-branding deal with Japan Airlines – which is helping embed cross-border usage into cardholders’ everyday travel. He also said that the company has a team spending time putting effort into “pulling the right levers” to direct the optimisation of cross-border flows, while Mastercard branded products being used in the on-ramp for stablecoins and crypto are now helping drive card not present ex travel volumes.

Responding to a question about how Mastercard is building out a competitive moat, Miebach said that building a network is complex as it requires Mastercard to “be a global player and act local”, and that the company is continuing to build out partnerships to enable the last mile of payments, citing Alipay+ as an example. Mehra added that the company is not aiming specifically at building out cross-border acceptance, but both domestic and cross-border together, as this is enabling it to grow its global footprint in a way that is increasingly serving cross-border too.

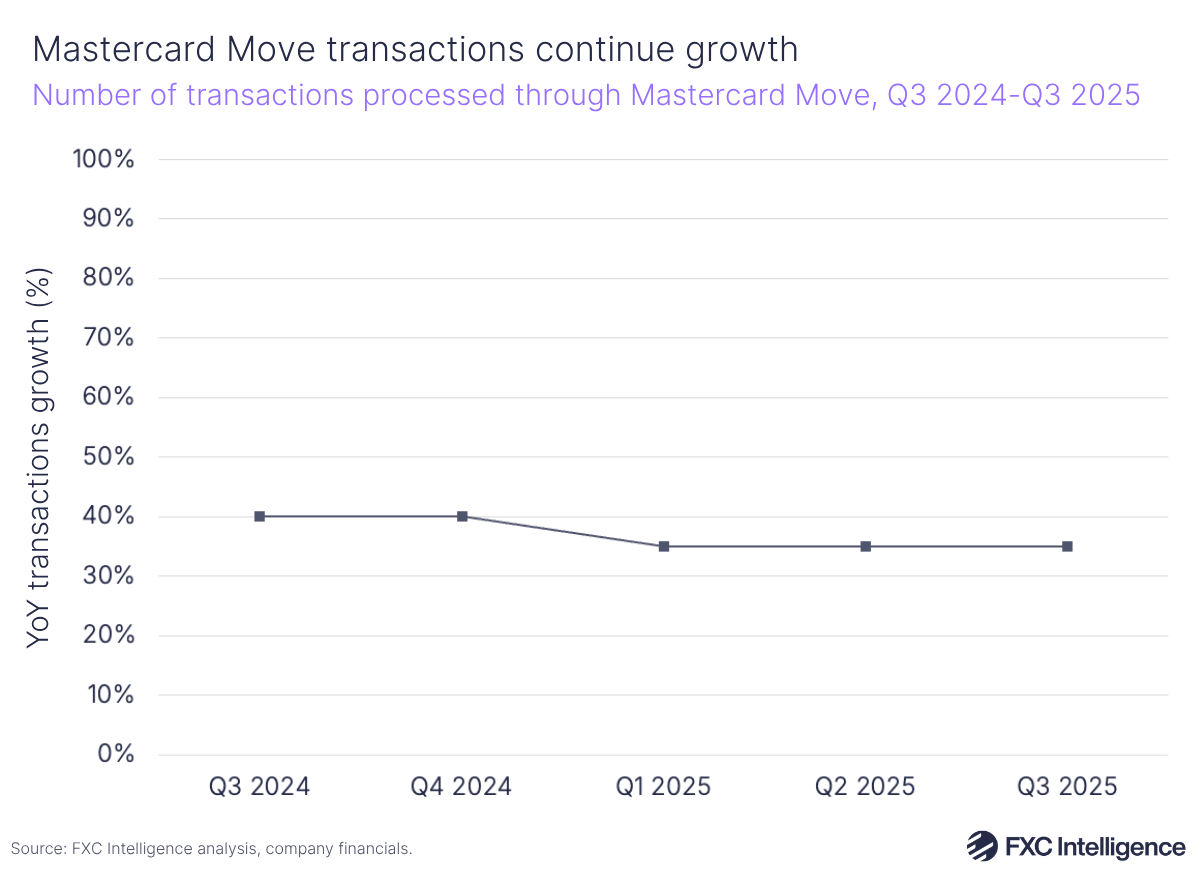

Mastercard Move sees globally driven growth

Mastercard Move – Mastercard’s disbursement and remittances platform for processing cross-border transactions, gig and real-time payouts – saw transactions grow by 35% during the quarter.

Miebach said that the company is integrating the product into core banking platforms, adding InfoSys during Q3, while in China it is enabling consumers to make outbound remittances through “billions of endpoints”. The product is also growing its presence in Europe, the Middle East and Africa (EMEA) through partnerships with Worldpay and Saudi-Arabia based STC Bank.

Similar to Visa, Mastercard recently announced it was embedding stablecoins into Mastercard Move across disbursements, remittances and B2B, with clients now able to pre-fund transfers with digital currencies. Prefunding capabilities are now live with customers in EMEA, including the addition of Paysend during the quarter.

Stablecoins continue to drive volumes for Visa and Mastercard

On stablecoins, Visa’s McInerney said during the earnings call that the company had facilitated over $140bn in crypto and stablecoin for users since 2020, with the majority of this (more than $100bn) being in purchasing crypto and stablecoin through Visa and $35bn being through spending using stablecoins and crypto assets. It also said that stablecoin-linked Visa card spending has quadrupled versus a year ago.

McInerney also said that Visa was adding support for four stablecoins running on four blockchains, which represented two currencies that could be accepted and converted to more than 25 fiat currencies. Overall, the monthly volume of stablecoin flows passing through Visa’s platform has surpassed an annualised run rate of $2.5bn. Finally, Visa is now enabling banks to mint and burn their own stablecoins through Visa Tokenized Asset Platform, which it launched around a year ago.

Mastercard similarly had more to say on stablecoins besides Mastercard Move, with Miebach saying that it continues to see them as an attractive and growing opportunity for Mastercard’s network. The company is seeing volumes and transactions grow across approximately 130 crypto co-branded card programs, with Q3 year-to-date transactions up over 25% with spending at crypto merchants.

Separately, Fortune reported this week that Mastercard was in late-stage talks about a potential deal to acquire crypto and stablecoin infrastructure provider Zero Hash for $1.5bn-2bn. In response to a question around Mastercard’s interest in crypto infrastructure, Miebach said the company would not comment on “market rumours”.

AI and agentic commerce open new expansion opportunities

Agentic commerce – payments facilitated by AI-driven bots or software agents – also cropped up across both earnings calls. Mastercard gave an update on Mastercard Agent Pay, its agentic commerce program launched in April. U.S. Bank and Citibank cardholders are already able to use AgentPay, with other US issuers expecting to be enabled in November and a global rollout to follow next year.

Partnerships here will be key, with Miebach saying that its system will be able to provide agents with predictive insights to help drive smarter decisionmaking and recommendations. Separately, the company said that it was continuing to work with key players such as OpenAI, Google and Cloudflare to set industry standards for agentic commerce.

Part of the call revolved around the unique threat or potential issues surrounding payments made through AI agents. Miebach acknowledged that there are complexities, including, for example, if transactions are challenged by the consumer and proving who might win a potential dispute. While he expects the regulatory framework on this to evolve over time, he said the company’s Agent Pay already works to establish the veracity of AI bots, and the company has already previously acquired a company (Ethoca) that helps provide an audit trail for transactions. Going forward, he said, a host of services – including identity solutions and merchant services – will help make agentic commerce a “safe and secure ecosystem”, creating an environment that could also see opportunity in the B2B context.

On Visa’s side, McInerney said that the company saw “considerable opportunity” in the agentic commerce space, having long been a proponent and actively leading product development in the space. He clarified that the company’s Visa Intelligent Commerce solution – launched in June to enable AI agents to securely transact on users behalf – is now powering live agentic transactions. He also gave an update on Visa Trusted Agent Protocol, launched two weeks ago to help merchants verify agents, saying that the system being an open set of standards was “critical to drive mass adoption in a way that’s needed for agentic commerce”.

McInerney added that he sees agentic accelerating the adoption of ecommerce and mobile commerce, saying that it could drive users to buy from a larger, more diverse set of merchants than they do today with traditional ecommerce, which ultimately leads to more transactions for Visa.

Finally, McInerney argued that tokenisation – i.e. replacing sensitive card details with unique tokens – would be the “critical building block” for agentic commerce, with the company looking to leverage its 16 billion Visa tokens across the ecosystem to help drive this forward. However, he said that collaboration in the industry will be key for the success of the technology.