The global economic downturn is affecting a wide range of industries, but the Q2 earnings have provided a first look at the ways it is impacting cross-border payments in particular.

Fallout from the Covid-19 pandemic, the ongoing war in Ukraine and skyrocketing inflation are all contributing to a global economic downturn in 2022. But how it is impacting cross-border payments?

This piece highlights four key areas that have had a significant impact, both positively and negatively, on cross-border payments companies based on their Q2 earnings results (or in the case of FX solutions provider Argentex, their full year results for the year ending 31 March 22). It also examines where companies have said they could see an impact moving forward.

The economic downturn and cross-border payments

While the economic downturn is being felt more acutely in some parts of the world than others, the vast majority of cross-border payments companies are seeing some form of impact, as a result of rising inflation, the Russia/Ukraine war and ongoing effects of Covid-19.

Significantly, our analysis of earnings reports has found that while not only has this not been felt equally across different companies, there are also signs that while some are set to see significant headwinds due to the downturn, others are benefitting from the changing economic landscape.

We have identified four key areas where companies are reporting particular impacts, which are FX volatility and the strength of the US dollar; inflation; the drop in crypto prices; and changes to consumer spending habits. While these are naturally interlinked, we found that different companies were seeing discrete impacts from these four, which we break down in more detail below.

FX volatility and the strength of the US dollar

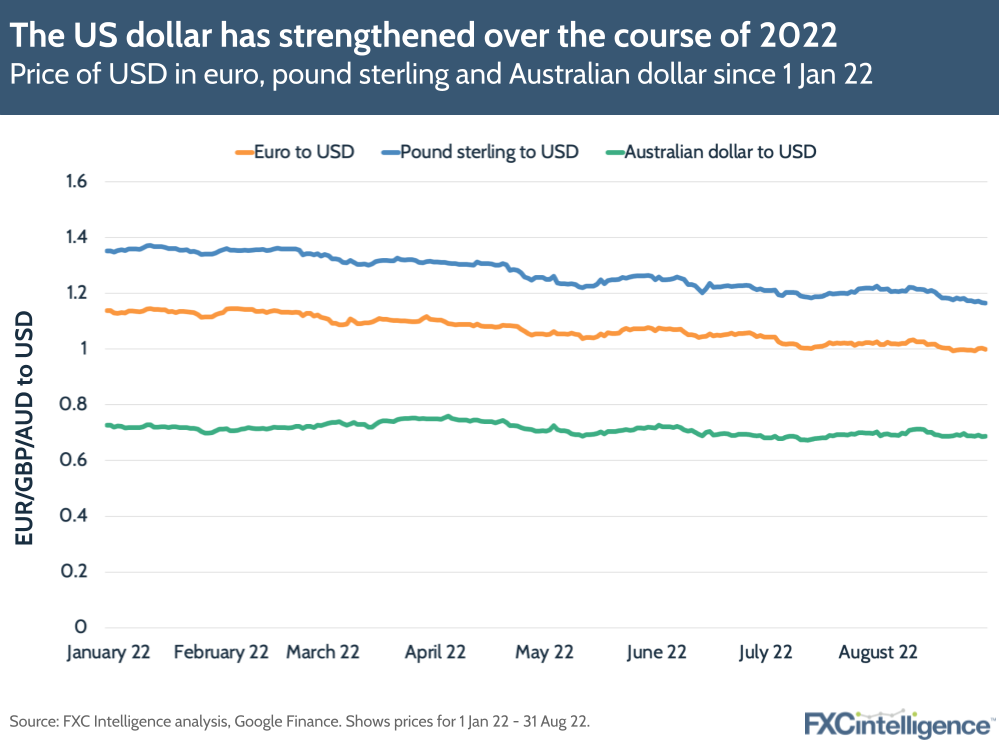

With investors flocking to the US dollar and selling off holdings in other currencies, the US dollar value has climbed in value substantially (as it often does in periods of downturn) while other currencies have depreciated. For cross-border payments companies, this has had mixed effects, with some companies seeing headwinds as a result of FX volatility and others benefitting from the stronger dollar.

Business payments specialist Paysafe has updated its FY22 revenue outlook to $1.47bn-$1.49bn (down from $1.54bn-$1.58bn) and adjusted EBITDA outlook to $400m-$415m to reflect FX headwinds. Meanwhile, B2B accounts receivable firm Flywire and ecommerce fintech Global Payments both mentioned they had seen negative impacts from FX volatility (although for Flywire, this was a nominal impact related to transactions settled in British pounds, euros and Canadian dollars).

Mastercard and Visa both said that they had seen cross-border volumes increase, but Mastercard also said that unfavourable FX activity had been a contributing factor to the 10% increase in its adjusted operating expenses. It’s expecting FX to create headwinds of 5-6% for the year, primarily due to the strengthening of the US dollar. On the other hand, Visa said that nominal operating expense growth would be around one and a half points lower due to the stronger dollar. Mastercard chief financial officer Sachin Mehra also mentioned that in a highly volatile FX environment, Mastercard delivers important switching and settlement services for all the transactions made, so it can actually work in the company’s favour.

Other companies have said that they actually stand to benefit from shifting currency values. In its FY22 results ending March 2022, FX specialist Argentex said that more volatility in markets led to clients trading more frequently and hedging for longer periods, and it expects this trend to continue.

Finally, Scott Galit and John Caplan, co-CEOs of US-based fintech Payoneer, spoke to FXC about how the company’s model of spending mainly in non-USD, and earning mainly in USD, means that it sees a slight improvement from the strong US dollar.

Inflation and rising interest rates

Macroeconomic factors, including rapidly increasing energy prices, are driving up the price of goods and services in many countries worldwide, which in turn is driving central banks to raise interest rates. On the one hand, some cross-border payments are seeing nominal or little impact from inflation, while others are seeing more sizeable impacts on their bottom lines. For some, it’s actually creating some benefits.

Fintech Fiserv, for example, says that inflation was one of the contributing factors to its adjusted operating margin slipping to 33.5% (down from 33.9% a year earlier), partly due to inflation. Despite inflation leading it to see revenue growth in some ways, the increased cost of labour and materials (such as in its PoS systems) affected its profitability. It did say it anticipated inflation and its effects to subside as the year continues.

Euronet, meanwhile, saw its average send amounts decreasing during the year. The company has reflected a 1% tempering of revenue growth in its H2 22 guidance for its Epay and Money Transfer segments to account for possible changes in consumer transactions as a result of inflation.

Money transfer player Wise said that it had to change its fees due to inflation in the Turkish lira, which has risen nearly 80% in July due to increased cost of living.

However, inflation has not been bad for everyone. Visa executives explained in their Q2 earnings call that inflation can actually increase the size of transactions made using their debit cards (with Visa being ‘stronger in debit’ as more people use debit during slowdowns). PayPal, meanwhile, said that cost-of-living related impacts due to inflation could actually prop up services like its PayPal Honey product, which provides coupons and rewards at checkout.

Western Union, which struggled in Q2, saw mixed impacts as a result of inflation. On the one hand, it said that inflation in Argentina had actually increased revenues by approximately 1%, but it also said that its retail business overall would be affected by macroeconomic headwinds, including inflation, moving forward. The money transfer giant is predicting a mid-single-digit decline in constant currency revenues for this year, but this does not include the impact of inflation in Argentina.

In that country, the central bank recently raised its main interest rate to 69.5% as it tries to contain inflation, which is currently at 70% and expected to go over 90% by the end of the year.

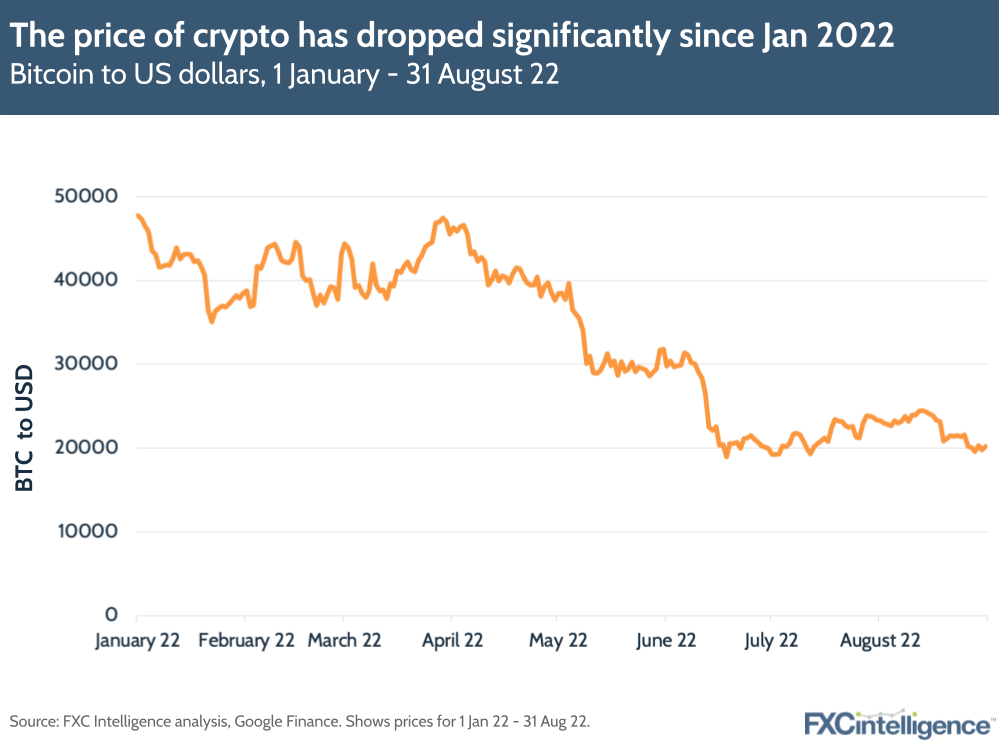

The crypto downturn

Crypto tanked in Q2 for a number of reasons. For one, the TerraUSD stablecoin lost its peg, causing a panic in the crypto market that led to a worldwide sell-off of cryptocurrencies (find out more in this report). The Ukraine war, lifting of Covid restrictions and rising cost of living are making it less likely for people to invest in crypto at the moment, perpetuating the downturn and leading to some significant risk cost-cutting initiatives.

Coinbase, which earlier this year launched a crypto remittances pilot programme to Mexico, saw its revenues decline 61% YoY while its adjusted EBITDA margin fell to -19%, primarily due to the decline in crypto assets. The company laid off 18% of its workforce (1,100 employees) and is now looking to push more into staking products in a bid to move away from trading revenues, which it sees as being more volatile, as well as introduce more strategies to reduce costs across its operations.

Then there’s Block, the Jack Dorsey-owned payments tech company formerly known as Square, which allows US users to send bitcoin to other accounts around the world via its Cash App offering.

Cash App saw Bitcoin revenue shrink 34% YoY, which is significant as the cryptocurrency accounted for 41% of Block’s overall revenues for the quarter. However, the company did argue that larger sellers (those with a gross payments volume of $125,000 or more) made up two thirds of the company’s volume in the Square business, and historically these companies have been more resilient to downturns.

On a more positive note, Moneygram CEO Alex Holmes told FXC that the global on and off ramp for crypto could be set to benefit from the downturn, as now more than ever people are looking for a solution that will allow them an accessible way to cash out without losing a significant amount to fees.

Changes in consumer spending

The way that consumers spend their money may change during an economic downturn as priorities shift away from unnecessary commerce – however, many companies in the cross-border space are likely to see varying impacts, with some saying that they don’t expect spending to change in industries relevant to them.

FIS and Fiserv, which together provide payments tech to millions of emerchants worldwide, said that they could see the effect of changing consumer spending habits in months to come. Fiserv executives said that in the event of a recession they would see a meaningful downturn affecting its merchant segment first, followed by payments and then fintech.

However, both companies did say they felt they would be resilient given their performance in the pandemic and subsequent recovery. Fiserv also said that spending across Latin America and the EMEA region had accelerated during Q2, driven by strength in the hospitality segment.

Visa said that the volume of spending might decrease, which would affect services, but spending would remain high. As one executive put it in the earnings call: “It’s possible that people are changing what they are buying but not how they are paying, and we fall into the latter category”.

Mastercard was also confident, saying that because the company has so many diversified options across card-based spending – from push payments into general payments for goods and services – it feels it can weather the storm of changing consumer spending habits.

Notably, ecommerce payments service provider dLocal’s adjustment for inflation was substantially higher in Q2 22 – $472,000 versus $7,000 in Q2 21 (this may, however, have been linked to an increase in revenues). Executives said they had not seen a big impact to their business from inflation, but it could end up being linked to lower ecommerce growth, which would have an impact.

Similarly, ecommerce player Adyen said that rising interests and inflation would be a challenge, but that the diversity of merchants across lots of verticals, geographies and products would make the company more resilient to this.

The future economic outlook

As we’ve seen over the course of this piece, many companies in the space have said that they will be resilient in the months to come, whether that’s because they believe inflation will have a nominal impact, or because their core customer spend will not be as badly affected as the need for their services won’t dissipate.

Much of this is to do with the target markets being addressed. LatAm-focused remittances player Intermex doesn’t believe inflation will cause a major change in principal amounts being sent. CEO Bob Lisy said that this was partly because the company does a lot of business in areas where primary industries have essential services that make them more resilient to the downturn, such as construction and agriculture.

Following its Q2 results, Flywire CEO Mike Massaro spoke to FXC about how education and healthcare – two of the company’s major segments – have tended to be more resilient historically, as people see them as being worthwhile investments than other areas such as travel.

Meanwhile, remittance players MoneyGram and Remitly both acknowledged that inflation will put pressure on people’s disposable incomes, but also argue that remittances become even more important during a downturn. As Remitly CEO Matt Oppenheimer told FXC recently: “Despite the macroeconomic environment, customers continue to prioritise remittances as they have in previous recessions.”

With the Ukraine-Russia war still ongoing, inflation still rising and the cost of living changing the way many consumers and businesses make payments, the future still looks uncertain for the industry, but many companies are confident they can ride out the wave. As the year continues, FXC Intelligence will be continuing to monitor how cross-border payments companies are performing.

How are major payment companies competing on cross-border pricing?