Following the publication of Flywire’s Q2 2022 earnings results, we caught up with CEO Mike Massaro to discuss the company’s latest strong quarter as part of our Post-Earnings Call Series.

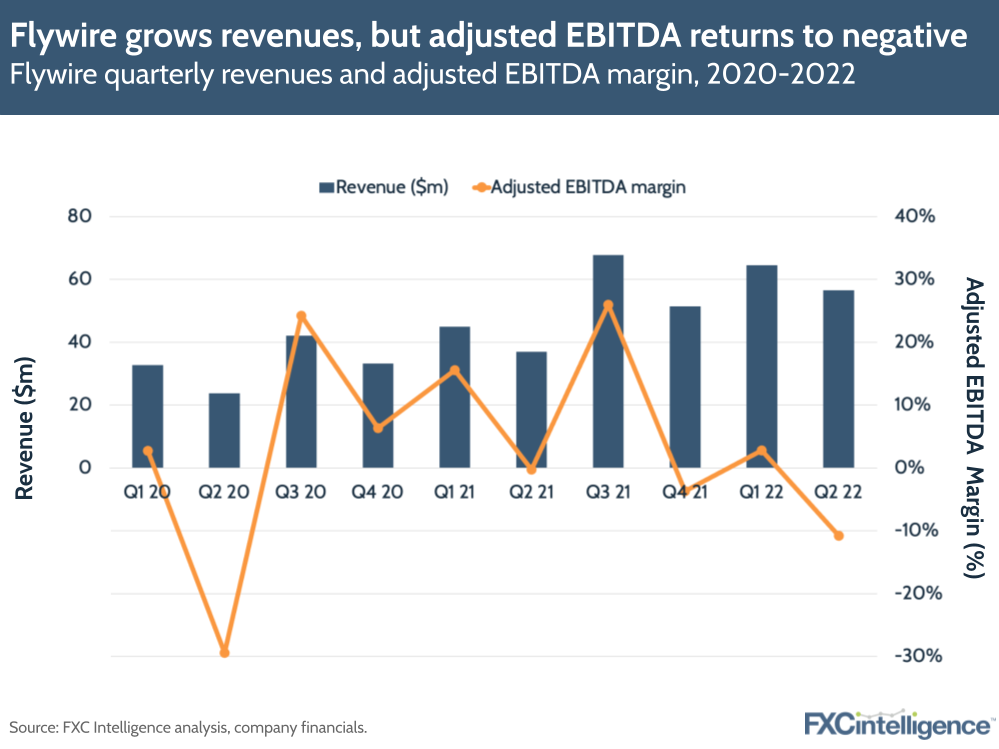

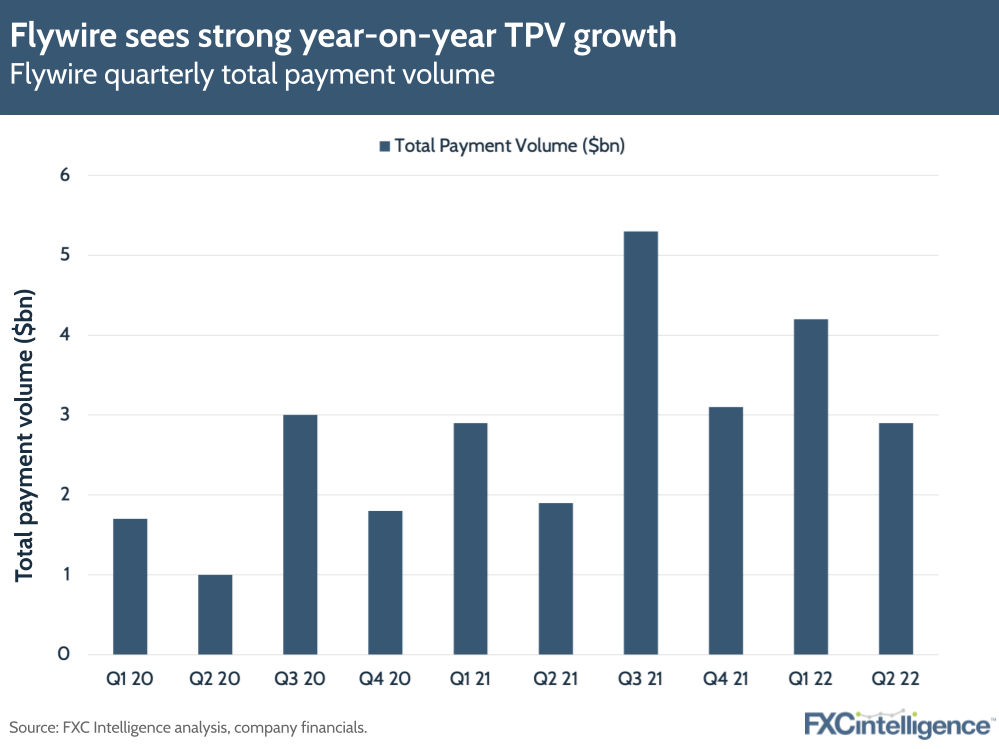

With 53% YoY revenue growth, to $56.5m, and total payment volume growing 49% over the same period, education, healthcare, travel and B2B-focused Flywire has reported a strong set of Q2 2022 results.

The company also reported adjusted gross profit of $33.2m – a 48% increase YoY. However, adjusted EBITDA dropped into negative, at -$6.1m,. This marked its second lowest quarter as a public company, although above internal expectations.

Flywire is building on plans laid out in its analyst day last quarter, prioritising go-to-market hiring and significantly increasing pipeline value in H1 22, which was twice that of H1 21. This has translated into a c.17% rise in customers compared to Q2 21.

The company has also increased its focus on international expansion, in particular increasing hiring in Australia, China, India and LatAm, as well as making key additions to its international network, including local payment methods.

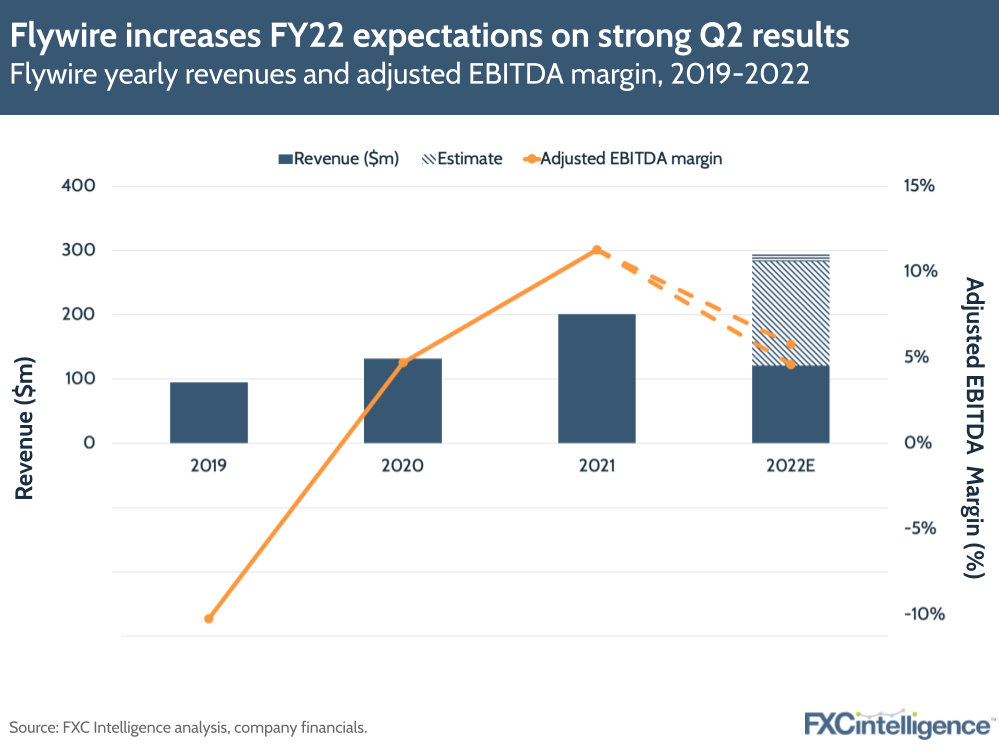

Flywire has raised its guidance for FY22 and remains positive about the resilience of its industry to economic uncertainty – particularly education and healthcare. However, how does it plan to keep building on its growth? I spoke to CEO Mike Massaro to find out more.

The drivers of Flywire’s profitable growth

Daniel Webber: Payment volume is up nearly 50% overall, revenue growth is at similar levels. Talk us through what’s driving that.

Mike Massaro:

A couple of the real highlights, obviously the travel sector. As you were off to Italy, and I was off to Italy, there’s a lot of people revisiting crossing borders, and travel, so we’ve seen really great growth in our travel business, which we called out in the earnings, and we also highlighted domestic education.

That continued ‘land and expand’ strategy that we’ve talked about before, where clients who had started using us for just cross-border really adopting more software, and using Flywire to digitise more of their payment volume. Those are two big call outs for Q2 that we highlighted in the earnings call.

Daniel Webber: Talk us through how you’re thinking about profitable growth.

Mike Massaro:

We’ve had this as a cornerstone, even in the pandemic, profitable EBIDTAs in ’20, ’21, and ’22, we’re guiding to ’22 as well. For us, we are actually in a bit of a different situation than most, where we actually had to really educate the market a lot on the investment thesis, and the fact that we were actually investing more in 2022.

It’s actually a record year of investment for us and yet, profitable EBIDTA is up. Part of the reason to do that was because we just felt like now’s the right time to continue to accelerate more investments. We wanted to do that, but at the same time, we wanted to make sure that we were still showing we could grow profitably.

That’s been a lot of the discussion with investors this year, and making sure people see us actually increase our guidance on profitable EBIDTA and revenue, which we did for the quarter, and we did for the full year on the last quarter call.

Again, hopefully people see that even in the headwinds and the macroeconomic climate. It’s quite an unusual time, we feel like it was a great showing of strength. Even with multiple headwinds around the world, we were able to increase both revenue and EBIDTA guidance for the year.

Figure 1

Flywire’s investment thesis

Daniel Webber: Where are you focusing investment?

Mike Massaro:

We always look at investment, core investment thesis, when we make any investment decision, but we’ve highlighted a few things. Increasing go-to-market teams, further geographic expansion, which not only means payment network enhancements but even just operationally, where we have FlyMates [Flywire’s employees] supporting the business and expanding geographically there. The third area is really product and payment innovation, think of that as product and engineering investment. Those are the three areas.

Some highlights, if you think of just geographic expansion, our ability to just add more FlyMates around the world. We’ve actually increased our team size in India, not only from an operational support perspective, but supporting the huge market of international students that originate out of India.

When you think about payment network, we highlighted on the call that we’re expanding some of the payment methods in Columbia; we’re also doing some improvements to the product work, from a payment collection perspective, in India, as there’s been a bunch of regulatory changes there that we wanted to make sure we were on the front end of supporting.

When you think of product and tech, we’re really just scaling up our engineering and product team so that we can do more not only at the platform level and the network level, which supports all the industries, but even within the vertical industry, so that those teams continue to be able to deliver more product to customers and add more value to the software. Those are really the investment areas. If you think about the IPO, I think we had just over 400 FlyMates then, and I think we’re over 900 now.

It’s been quite a 15 month, 16-month process of scaling the company.

Figure 2

Retention-focused hiring

Daniel Webber: How do you think about hiring?

Mike Massaro:

It starts with retention. Hiring becomes a lot harder if you have high attrition numbers. We’ve been fortunate for the last many years to have well below industry-average attrition numbers. FlyMates want to stay here, they want to grow their careers here.

We often talk about creating an environment that lets them create a career of a lifetime at Flywire. There’s a lot of internal mobility movement, a lot of upward mobility within our team. I think that’s part of what helps us. I think the average number in the industry, according to a Bain report last year, was 22% loss of teams.

Last year was an exceptionally high attrition year for many companies, and we were mid-low single digits. When you think of that, we’re really fortunate to have that and see that benefit of the culture we’ve created. When it comes to hiring, I would say, not only are we trying to hire record numbers, but we’re fortunate because we have a geographic footprint that many companies don’t have.

There are 12 major Flywire offices around the world, there are FlyMates in many more countries than even that. Because of the pandemic, it actually gave us more flexibility to recruit more geographies, because that’s just inherent in how the business works.

I talk to a lot of tech companies who have an office in Boston, and they’re going to go international to Ireland, or they’re going to go to the UK; they build a second hub and they’re now between two locations. For us, we’ve got 40 nationalities inside the company. There are people that are notoriously used to working virtually and remotely. We actually have a whole global talent pool that I think a lot of companies don’t benefit from having.

We’ve also been very fortunate to have two acquisitions that we completed – WPM in December and Cohort Go in July – and that added probably 90 FlyMates between the two of them as well, which again, is another great way to help accelerate the size of our team, getting people that know the industries that we’re in, they know the pain points and that are also a culture fit. That’s helped us scale as well.

Figure 3

Flywire’s approach to acquisitions

Daniel Webber: How are you thinking about acquisitions in this market?

Mike Massaro:

We continue to look for something that fits into three buckets for us. What can help us accelerate a given industry or a geography that we’re already in? What could add additional capabilities that we can offer our clients and drive additional revenue, or find an additional revenue stream within our industries? Is there a geography we’re not in, that we can get into through acquisition, or is there an industry we’re not in, that we can get in through acquisition?

WPM fit that first category of accelerating an existing industry and geography, and Cohort Go fits number one and two, it has value in both those two pillars. Not only does it help us in Asia-Pacific, Australia in particular, it helps us actually accelerate some additional opportunities around the educational agents, who are a big part of the educational experience for many students who study abroad, and it’s bringing additional capabilities to help support those agents.

We actually think it fits those two pillars. Even after those two acquisitions, we’re still sitting on quite a sizeable war chest. We haven’t used up our IPO capital yet, and definitely intend to still be active, but we’re also not in a rush to do another deal too quickly.

I’ve said before, we’re quite picky on making sure we find not only the right tech, but also the right team, which we think fits into the culture that we have and helps us accelerate. We’re not looking to just be a PE firm, and do roll-ups or anything like that. We really want to find the right asset, and the right team.

I would say too, to handle the scale in which our business continues to scale, you can’t just have five, six or seven different platforms. You have to really invest in core tech, or you just start managing technical debt all the time. Anybody that’s tried one of those roll-ups, or looks to bundle stuff on, oftentimes, they’re dealing with multiple tech stacks underneath the covers, which is tough.

Empowering clients for overdue collections

Daniel Webber: You’ve been adding clients and seeing results with cross-selling. Talk us through what that’s entailing.

Mike Massaro:

The first big area is just the domestic capability, and it sounds silly, because you would think having people solve that, but it’s a huge opportunity for our clients to just have Flywire process all their payments. Going from that cross-border payment vendor to being someone that can help them with all their receivables, domestic and cross border, you can imagine that’s a logical extension.

It does vary slightly by industry for us. In areas like healthcare, there’s a lot around omnichannel, where you’re putting payments in the flow of healthcare transactions, and user interactions. In education, there are things like payment plans, which are huge elements of the experience. We’ve also had a lot of success in this overdue receivables product that we have in the education sector.

Again, looking for areas in which our clients struggle to get paid. Once payments get into an overdue status, 60, 90 days post due, so many businesses, and so many universities, would just take that money and go to some type of debt firm or collection company and try and offload that, and get fifty cents on the dollar, or whatever they could, and have someone else chase the money.

What we’ve done with technology is just really empower the client to remind people that they have balances overdue. Just by having that simple layer of technology, it’s almost a re-bundling of the same capabilities we have in the domestic and cross-border product, but doing so focused on a different team within finance, that’s chasing overdue receivables. It really empowers them to get millions of dollars back that they would’ve handed off to a collection company.

Things like that are relatively small tech lifts for us, but deliver huge value to the customer. Obviously, the Cohort Go deal, plus our existing success in agent solutions and education, has been another capability we’ve added.

Agents aren’t really a customer of Flywire, but they’re a major stakeholder in the ecosystem, so we built a whole version of our software that gives a view into the agents as they help students make the payment. There’s a relationship building between the educational agents and the universities in the United States; we think that’s an interesting opportunity for future growth, too.

Daniel Webber: With overdue collections, is there often a cross-border element to that? Presumably the absence of normal models makes it more complicated.

Mike Massaro:

Yeah, there often is some cross border, but at the same time, it’s a very manual, inefficient process, even for domestic overdue payments.

Again, Flywire is not actually going and chasing or collecting, we’re enabling technology inside our clients to then go and automate the process, and empowering them with rules that they can configure as to how flexible they are on the payment terms that they’re offering. You can imagine, if someone has a student who’s enrolled but overdue, they can actually provide different terms. “Hey, you can make payments over the next three months to get back on track, and stay enrolled in school.”

Maybe somebody has graduated, and they forgot they had an overdue balance. Again, before handing it to a collection company, you should at least give them an opportunity to make that payment, and remind them and make it easy to make that payment. A lot of clients find value in just having the software to help automate that flow.

Flywire’s B2B payments solutions

Daniel Webber: Where in B2B are you really seeing growth?

Mike Massaro:

We continue to see clients who have some level of cross-border receivables that are quite challenging for them as they’re growing their business globally. They’re not experts in payments, nor do they want to go and build finance operations in different countries, or have three, four, or five different banking relationships in different markets and countries around the world.

The solution definitely hits a special need for those folks. Again, we called out some great case studies in the earnings call, but really just making sure that we’re providing great integrated solutions into products like NetSuite, which are huge, must-have integrations within B2B payments. Again, for us, I think everybody’s using B2B as a buzzword now.

Deals are getting done that are being branded as B2B, that I’m not sure are quite B2B. At the same time, we’re still in the really early innings of that digitisation. My belief is that it’s going to take at least a decade to see any type of real, massive transformation of this industry.

You’re going to have people succeed at it just because its size is so large. Again, our focus is on that accounts receivable side. Our focus is on deeply integrated solutions, and leveraging our existing payment infrastructure to make it easier for our clients to get paid.

Daniel Webber: There are a lot of people going out to the SMB space, but you’re focused on the mid-size to institutional level, correct?

Mike Massaro:

Think of it as $30m of revenue to $1bn of revenue. If you get up to $1bn of revenue, typically, we’re even just working on one division, or one department of a company that large. Again, if you can just digitise one quarter, one piece, one subdivision, you often can find your way to other pockets of receivables that can extend your relationships.

Thinking about additional products, that’s great, but for us, we can even just add more payment volume with an existing product. We don’t have to win all the business in our first go with a client. You can start with maybe helping them get paid from Europe, or from Latin America, and build on that over time, as the client gets more confident that they can automate more of their receivable.

Reassuring investors through economic uncertainty

Daniel Webber: How are you talking investors through how Flywire sits within the current economy uncertainty?

Mike Massaro:

Obviously, we’ve seen the business, having run it for 11, 12 years, we’ve seen it through a couple of different market downturns. We definitely have seen the trend before, where, oftentimes in recessions, more people go back and get reeducated, and retooled up in their skill sets. Again, I think that’s something that is positive for us.

Even in an inflationary environment, things like education and healthcare are often more resilient. In essence, costs go up, and people end up bearing those costs, because they prioritise those as important things they want to invest in. That’s traditionally what we’ve seen. Even if you look at our travel business, a lot of people would look and say, “Travelling, consumer spending could easily be cut.”

Where we’re focused in travel is typically in the high end, more affluent travel. Those experiences, I think people have had a lot of pent up demand, and I think you’re going to see multi-year, people investing in trips, and experiences, and you’ve had companies like American Express say something similar.

We feel like that is a bit resilient, and when you think of the B2B market, you have a similar dynamic, where everybody’s being asked to do more with less, and you’ve got potentially less ability to hire folks in finance, and back-office staff. Where can you automate more? Where can you find a chance to use technology to make your business scale? I think that’s a positive trend for us.

Again, these are quite unique macroeconomic times. I don’t know that the world has seen quite anything like what we’re seeing right now, or knows how it’ll play out, but we feel pretty good about the headwinds we’ve already navigated in Q2 and how we’re positioned for the future.

Moving past the pandemic

Daniel Webber: Do you feel that you are mostly through the pandemic pressures and we’re onto different economic pressures now?

Mike Massaro:

We still have some. I had a few comments in my script on the earning side, which was around education. There’s still some return. Even since the IPO, we always talked about a rolling recovery that we expected to go through ’21, ’22 and even into ’23, and we still believe that. If you look at certain parts of education, Australia, New Zealand is one of the markets, Japan had tighter lockdowns, and those markets haven’t had a full year in recovery yet, and 2023 will hopefully be that full year.

Then, there’s different sub-segments, whether boarding, language programs, where people, because of Covid restrictions, didn’t really either send younger children overseas, or didn’t want to do a four week language program in London, when they had a 10 day quarantine requirement or something like that.

There’s certain sub-sectors of education that we believe still have some recovery left in ’23. Then, there’s obviously certain parts of travel. If you look at Q1 of ’22, although a great quarter for us in travel, you still had some parts of the world that were struggling with Omicron. I think you have different trends.

The winter season that’s upcoming in Q4, in Japan, is a big ski season. That’s going to be interesting to see. Does Japan continue to open for travellers coming into Japan for ski season, which is very popular there? Again, I think you’re going to see, if there are macro lockdowns, potentially there’s some more recovery ahead, but most of it is within certain geographies, or within certain sub-sectors.

Daniel Webber: Great. Mike, I think we’ve gone through things nicely.

Mike Massaro:

I appreciate all the great questions.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.