In our most recent piece in our Post-Earnings Call Series, we speak to Payoneer co-CEOs Scott Galit and John Caplan to discuss the company’s strong and increasingly diversified Q2 2022 results.

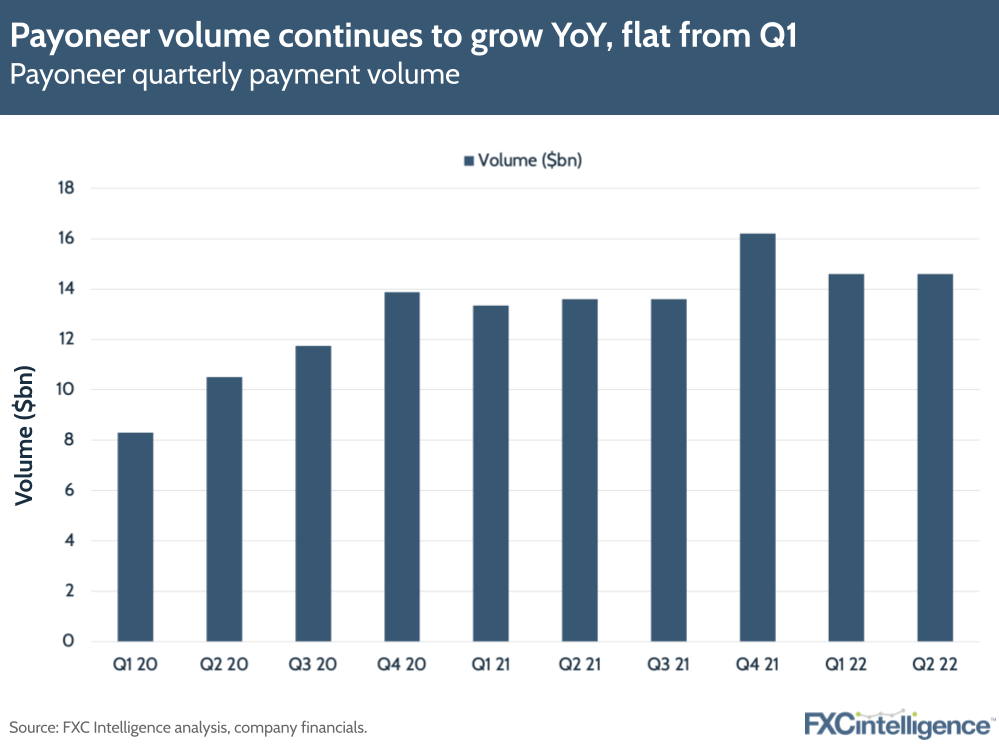

Ecommerce major Payoneer has had another strong quarter, delivering 34% YoY revenue growth in Q2 2022 to reach $148m, up 8% from Q1 2022. The company also delivered positive adjusted EBITDA of $15m, while volume climbed 8% YoY to $14.6bn.

The company’s regional diversity has enabled it to maintain strength during increasingly uncertain wider economic conditions. Some international regions have been particular contributors to the company’s rise in revenue: LatAm, South Asia and MENA all grew faster than the overall business.

Payoneer’s B2B accounts payable, accounts receivable (AP/AR) business has also grown faster than the overall business, seeing a 66% YoY volume growth that means it now accounts for 12% of the company’s total volume.

Other positive contributors include the company’s virtual card, as well as increased cross-border travel, although in Asia the pace of this growth still remains slow. Significantly, Payoneer has avoided some of the issues related to the strength of the US dollar (USD) that others have experienced as, while 60% of its operational expenses are paid in non-USD currencies, 85% of its revenue in Q2 2022 was USD denominated, protecting it from major FX risk.

To find out more, I caught up with Scott Galit and newly appointed co-CEO John Caplan to discuss the company’s results and future plans.

The drivers behind Payoneer’s Q2 22 revenue

Daniel Webber: Let’s start at the top line: really strong revenue growth. Talk us through what’s driving that; what’s the mix?

Scott Galit:

So this quarter was really a continuation of some of the important themes that we’ve been focused on and talking about for a little while now, which is the breadth and diversification of the geographies that we serve, the products that we offer and the vertical markets that we’re focused on. And that really creates a business model that is resilient and one that actually has multiple ways of driving increased revenue performance out of the flows that we get.

So, going through each of those dimensions with geographies, we’ve been increasing our investments in regions around the world that we see big opportunities in, and where we continue to see both growing opportunity as well as outperformance. So with areas like Latin America, South Asia and MENA, our growth rates continue to be very strong.

These are newer regions for us. We put in really strong leaders in those regions. Actually, even just this year, hiring a VP in the MENA region. And what happens when we do that is we then build a team around those people. And that team then starts to engage more actively in the market, building partnerships, building and developing our brand and increasing the acquisition of larger customers.

So that’s one theme and we’ve been executing on that for a while. Those regions also tend to have a higher take rate than the average take rate of the business overall, which will be another consistent theme across this. Second is the products, we’ve talked for a while about our higher value services. And so B2B, AP/AR for example, continues to grow strongly.

We really think we’re just seeing the tip of an iceberg here. AP/AR grew 66% in volume YoY and that accelerated from the first quarter. We really think this is just a super exciting and big opportunity, with long legs to it. And we’re investing appropriately behind that, so that was really exciting. And then also, the adoption of our virtual commercial card by customers around the world. It’s a great win-win value proposition.

It gives our customers more utility out of their Payoneer account. It saves them money and it actually generates a higher take rate for us than the average in the business. So an incredible win-win, more utility savings for our customers and actually improving take rate for us out of the same flow through our platform.

We are seeing some headwinds in general. Like many others in the market are expressing, the uncertainty around how things are developing is higher than it’s typically been. And so, we’re excited to have so many different ways of winning in the market. We continue to see strength in areas like services, social commerce, travel and remote work, and many of the other different market segments that we actually engage in. And so, we’re able to really ride things out and perform well even in more uncertain times.

Figure 1

Managing take rate intentionally

Daniel Webber: Let’s break down some of the mixes of the take rate. What’s driving it?

Scott Galit:

I’m going to focus first on the intentional part of how we’re managing the take rate in our business. The intentional part of take rate, there are a few things that are important themes for us. One, certain things are relatively harder to do and harder to deliver as services; either because there’s risk embedded in it, or there’s inherent complexity in it. And those are areas that we actually think there are opportunities to create more sustainable differentiation and sustainable value. And so we are intentionally focusing on service.

So B2B AP/AR, there’s actually a lot of complexity that comes along with that. And with that complexity, we believe there’s real, tangible, differentiated value that we have to provide for customers. It’s something that it’s harder for there to be easy “me too’s” on some of it. As a result, it’s not just a race to scale and margin.

In that way, there’s a real opportunity for us to create real value in a sustainable way. So that’s one, there’s services like that, which are positioned in big market segments. And that’s an area that we believe we can continue to drive increasing value.

Another example is the card. I think, as we show, that actually lowering the cost of ownership for a customer does not necessarily equal lower prices. So I’m not sure that everybody has understood that you could actually get to zero cost with a customer and actually make even more money than if you were charging them a fee. For anything that’s cardable, the actual opportunity is to reduce that cost that the customer pays and to generate attractive or premium value out of it, which is what we’re showing the ability to do.

As we continue to prove that out and further penetrate our base of customers with services like that, I think it actually helps bolster the value proposition.

And I think as we show, we’ve got a lot of additional exciting services that we believe can create some combination of sustainably differentiated value because of the complexity or extra value that we can create by just additional value, creating opportunities that layer on top. And then, when markets are competitive, we do think pricing will gradually decrease over time.

Our mix of larger customers is also increasing, and so that will also have the effect of gradually bringing the weighted average down as well a bit. But we think that we have sustainable, good take rate performance in the business because of these additional services that we’re investing in.

John Caplan:

So I would just add, different industries are in different geographies. And we have different costs in those geographies and can price differently for different customers types, different geographies, different industries, different bundles of our products. As our customers adopt bundles of the services we offer, we’re able to price the bundle.

And I think there’s some pricing power in the bundled services we offer. And then I think even more important, our customers are SMBs. And SMBs rely on us and trust us for having built the financial platform we’ve built, with the reliability it has, and they are not focused on the cheapest possible option all the time; what I think they’re focused on is a long-term relationship.

And you can see in our retention of our customers and net dollar retention, we see that our customers are loyal to a platform that’s providing value. And as we add additional products and services and bundle them together, we think our take rates will be stable.

The take rate also, or the loyalty, I would say also includes the high touch service that we provide in the markets around the globe. So our customers have a relationship with a member of the Payoneer team. Those relationships, I think, are highly valuable to our customers.

Figure 2

Building Payoneer’s business outside of China and the US

Daniel Webber: You’ve made the extra push into markets other than the US and China and those are thriving. What colour would you add to the geographical piece?

John Caplan:

In the World Bank, 90% of businesses around the globe are SMBs. They’re 50% of employer firms. If you’re an SMB in an emerging market, you need cross-border trade to be successful. There isn’t enough demand locally to be a business owner in Vietnam, or in Morocco, or in Argentina.

You have to export to grow your business. And what Payoneer has built is the core message about the next decade for the company. That growth you’re seeing in the business is because what we have is go-to market teams around the globe. In some of the markets, candidly, we’ve just begun.

We have a lot of runway in front of us on our go-to market initiatives, but we’re in these high growth, high export markets where they’re exporting goods, services, capability. So it’s not just the export of a pallet of eyeglasses, it’s a team of outsourced engineers that are working. It’s a stock photo agency that’s taking pictures of the beautiful sites around the world.

There’s outsourced accounting firms. I mean, you name it. There’s the breadth of businesses using our platform and all of those businesses, their customers are cross-border. And because of that, they’re not micro-businesses and they’re not big enterprises, they’re this very important part of the global economy, which are small, medium-sized franchises that are focused on providing their products and services to businesses around other businesses around the globe.

And one of the things we’re seeing is the network effects of the Payoneer population. So Daniel’s a wood table manufacturer in Vietnam, and Scott is a copywriter in Bangladesh, and John is an engineer in the Ukraine. We may all have Payoneer accounts, and we may buy and sell services from one another within the Payoneer network. And that network effect, that trust economy that we’re beginning to see be the fluid in our platform, is a really powerful dynamic.

When you think about the stability of our take rates, the additional services we’re offering and the community or ecosystem of our customers, it feels like there’s the very beginning of a multi-decade opportunity to provide sophisticated financial services and a network to the world’s exporting SMBs.

Figure 3

Driving customer acquisition through network effects

Daniel Webber: Let’s talk about the network effects. How do you measure improvement in network effects?

John Caplan:

I think the virality of our B2B, AP/AR platform is one thing where our product is driving our customer acquisition. That is one key driver. And then another driver is the trust and speed of the movement of funds.

Scott Galit:

So three things that I’ll zero in on. First, there are organic networks that exist in the world. And actually, part of what’s been beautiful about the internet from the beginning is that technology has now made it possible for networks of activity to find themselves and actually platform themselves in ways that really weren’t possible before.

The idea of Payoneer from the beginning was to plug into those networks, starting with marketplaces. And from the very beginning, we saw that oDesk connected to Elance, Elance connected to freelancer, freelancer connected to RentACoder and you could keep going. It’s the same thing that now, when we announced that we’re working with Walmart in the UK and in India to help them onboard merchants, it’s Amazon connects to eBay, connects to Walmart, connects to JD.com, and so on.

So, ultimately these ecosystems are all connected together as part of bigger networks of activity. And Payoneer has grown very, very successfully by amplifying those flywheel effects that exist naturally and organically and focusing on that. So that’s one, that we position ourselves in those networks of activity. Two is the products.

And we have multiple products that we intentionally introduce network effects into the products. So B2B AP/AR, we have an exporter that uses Payoneer to bill a buyer. That buyer then pays that supplier through Payoneer. On average, that buyer has more than one supplier internationally that they pay.

We then can engage with the buyer and say, “Actually, who else are you paying around the world?”. And we can help them now pay all of their suppliers, not just the one that actually introduced them to us. That then brings more suppliers, who often, if they’re selling to one buyer internationally, they’re selling to more than one, and those network effects continue.

And another product attribute, which is really easy for us to measure but we don’t report this out, we have in-network payments. So Payoneer account holders, anywhere in the world, can pay each other, essentially in real time, for free.

This is many billions of dollars a year of volume that we don’t report, that is just intra-network activity. And we get thousands of new customers a month that are signing up and getting paid for the first time by an existing Payoneer customer. And those network effects actually really do nurture and extend the ecosystem of activity that we have.

The place of credit in an uncertain market

Daniel Webber: Tell us where credit and working capital fits in because credit is increasing. Where does that fit into your thinking and mix?

John Caplan:

So credit’s important to us, it will be important to us. We have adjusted our risk appetite in the current climate to be moderate, given some uncertainties in the market. But long term, we believe credit is an essential tool for us and for our customers. And we’re uniquely positioned with the data we have on our customers and the relationships we see. Frankly, it’s similar to the network discussion that we just had.

We have exceptional data about who our customers do business with, the consistency of those relationships, the volumes of trade and their flow of funds. We see their volume coming in and out, so we feel good about our long-term prospects with working capital and credit. I do think we’re at the very beginning though, so it has not been the core focus for us. And I think you’ll understand, you can see why as we built the network, built the go-to market muscles, built the viral product suite, we then are in a position to layer in the credit as a loyalty program. And I think there’s opportunities there in front of us with that.

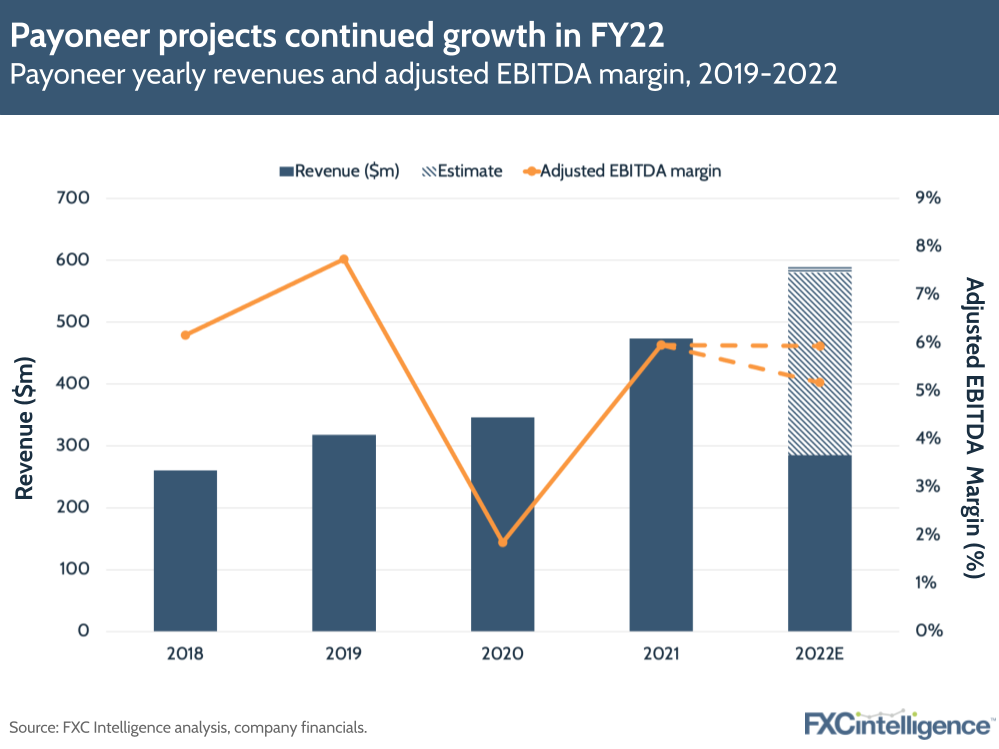

Payoneer’s journey to positive EBITDA

Daniel Webber: EBITDA and profitability is front and center for investment managers. Talk us through the EBITDA journey.

John Caplan:

We communicated yesterday that we intend to have positive EBITDA going forward. The firm has had 11 years of positive adjusted EBITDA, so we see good growth on the top line and good growth in our margins. And we feel comfortable with the forecast that we’ve communicated to the market about that.

Scott Galit:

The additional layer I’d add is we are continuing to invest. In particular, as interest rates have gone up, we’re able to pull forward our commitment to sustaining positive adjusted EBITDA. But you’ll also notice that our guidance for the second half of the year of adjusted EBITDA is lower than the first half. We’re continuing to focus on building for the long-term significant opportunity that we see but now, within the framework of sustained adjusted EBITDA and profitability.

Putting the customer first, building shareholder value

Daniel Webber: Is there anything else you want us to cover?

John Caplan:

What’s been exceptionally impressive to me joining Payoneer is the quality of the team and the engagement of our customers.

Scott Galit:

I’ll just say that I’m really, really thrilled to have most of a quarter under our belts together with John and I think we’re enjoying the process and enjoying the exercise of learning how to make the most of this really unique opportunity and set of capabilities, and a unique time in the market.

This whole process of communicating with the street feels like an interesting culmination of this introductory phase one and it’s really exciting. John’s done a great job and has really been diving into the deep end of the pool getting to know teams all over the world, as well as bringing his energy and excitement for the customer and the team that we have.

And it’s very clear, customer first and employee second. And for us, if we get those right, then the shareholder value will follow. We’re excited to be on the journey and there’s a lot of really good stuff to explore going forward.

Daniel Webber: Well, thank you both.

Scott Galit:

Good to see you.

John Caplan:

Thanks, everybody.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.