Last week, we launched The Cross-Border Payments 100 for 2026, our definitive listing of the 100 most important players in cross-border payments. Below, we break down some of the key data points about these companies to highlight ongoing trends in the industry.

FXC Intelligence has launched the eighth edition of its Cross-Border Payments 100 for 2026, which once again highlighted some of the key areas of the cross-border payments space.

Our list tracks key providers globally based on several criteria, including their significance as a company both globally and in a given market or segment, the extent to which cross-border payments is a key part of their business and how much they are growing.

Here’s another look at FXC Intelligence’s Cross-Border Payments 100 for 2026 below:

This year’s map saw many entrants return but some new additions continued to highlight the continued importance of blockchain and stablecoin infrastructure in the space, as well as significant growth in digital wallets and financial platforms in particular regions. Because these players carry so much influence, the data behind them holds a depth of insights about the space.

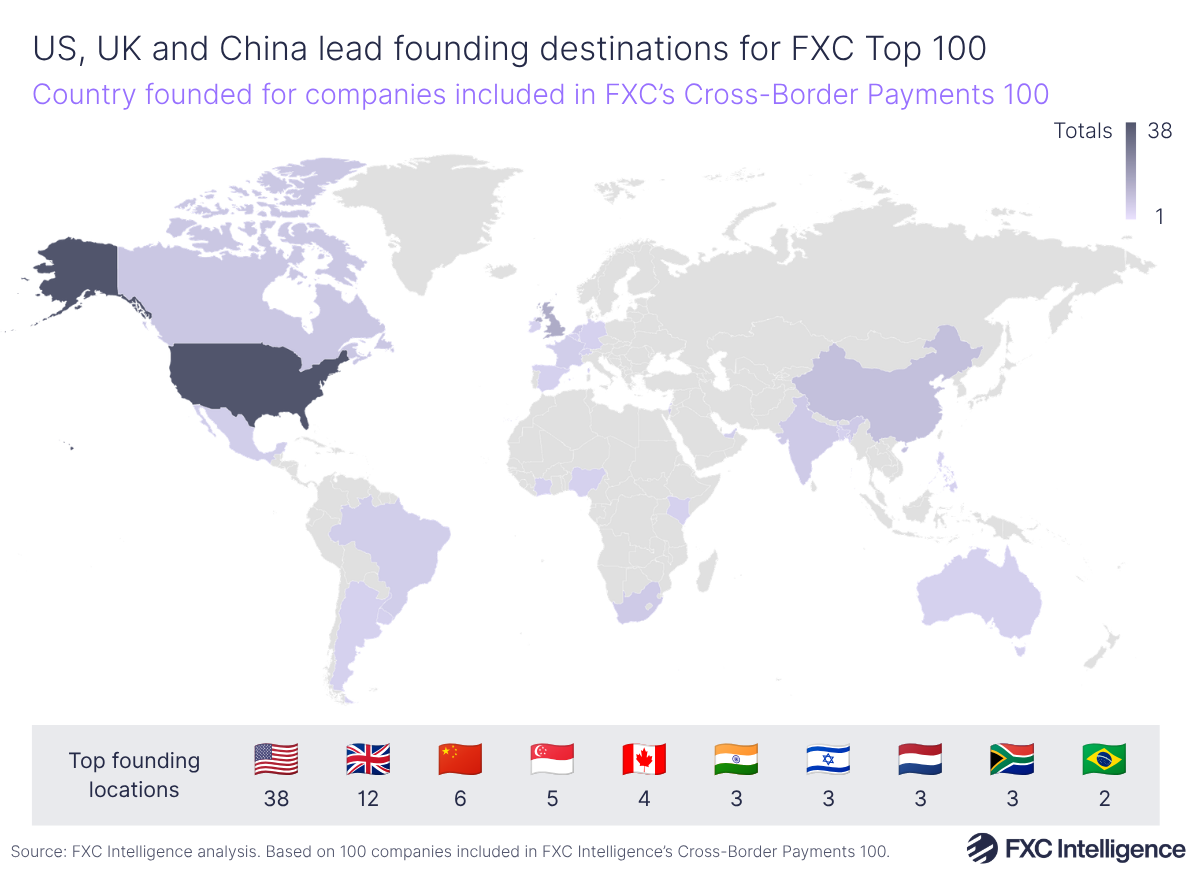

Cross-border payments companies span a variety of locations globally

Companies on the Top 100 were founded across 28 different countries and seven continents, with headquarters spanning 25 countries. Notably, 15 of the companies on the list were located in a different country to the one they were founded in, reflecting how players have often shifted their focus or business demands as they expand.

The US had the most companies founded there, followed by the UK, China, Singapore and Canada, with these same countries being the leaders for the number of companies headquartered there.

Nearly half of the companies were located in North America, with 22 founded in Europe and 17 in Asia, reflecting the extent of demand for cross-border payments into and out of these regions. However, companies also originated from Africa, the Middle East and Oceania, indicating the strong demand for remittances in these regions and aligning with significant developments, particularly in Africa and the Middle East, to fill an existing gap for better cross-border payment systems.

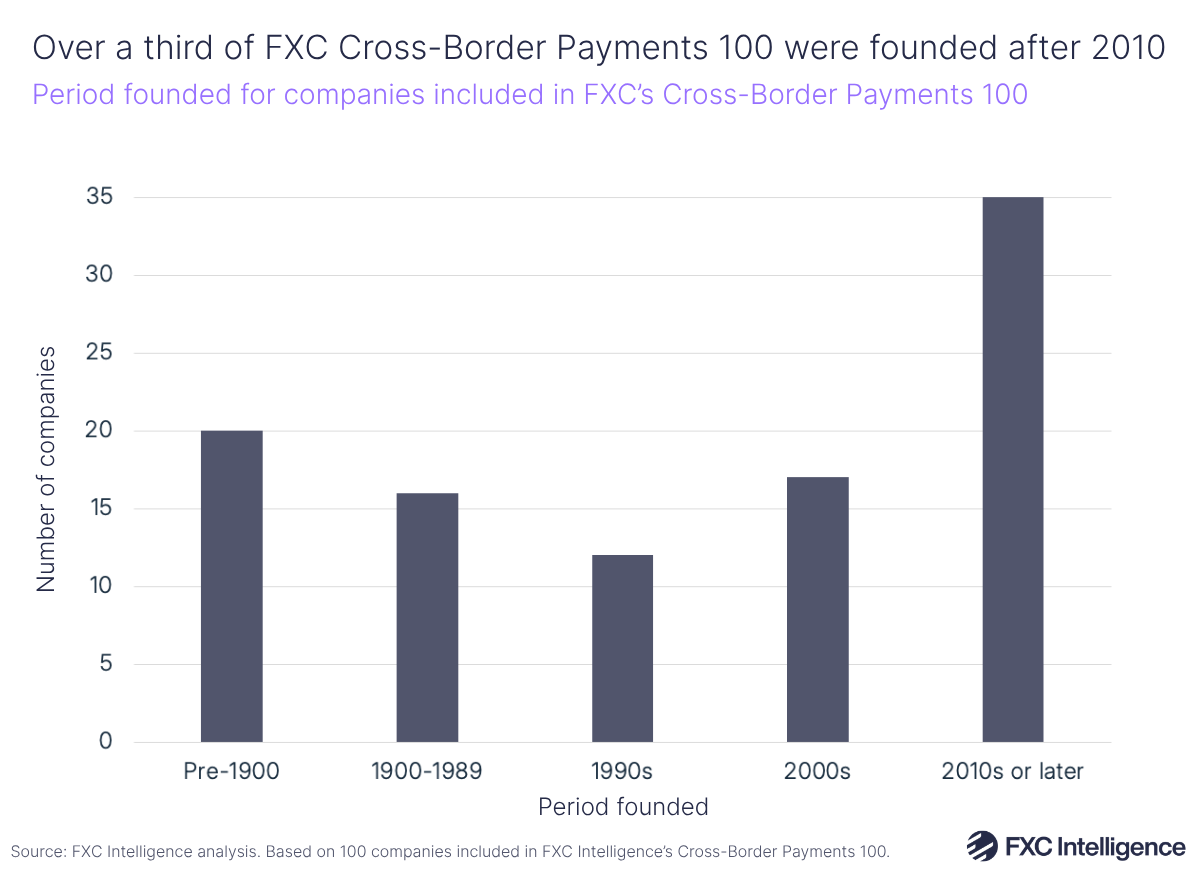

Leading players in the space continue to mature

Over a third of companies on the Cross-Border Payments 100 were founded in 2010 or later, though a significant portion (primarily banks) were founded either before 1900 or 1989.

This continues to highlight the global significance of established banking players, which according to our data account for the vast majority of B2B cross-border payments volume globally, as well as traditional P2P providers such as Western Union and MoneyGram, which have established roots in the space and remain dominant in their specific market.

Having said this, the fact that a large portion of the most significant players were founded in the 2010s or later speaks to the rapid rise of many companies on the list, particularly in areas such as blockchain and stablecoin services, consumer money transfers, mobile money and digital wallets and payments infrastructure.

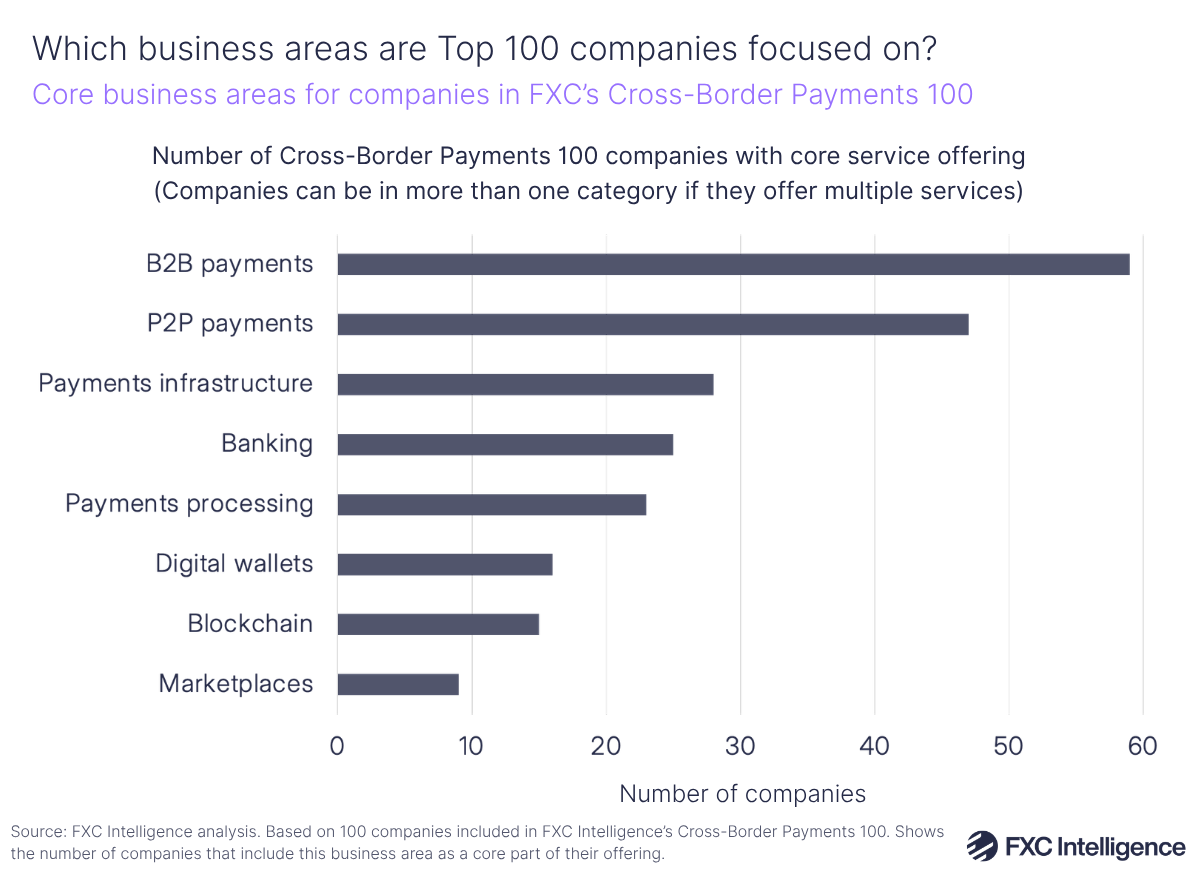

A significant proportion of leading cross-border players have B2B focus

We also explored where companies in the cross-border space have a specific cross-border focus across several categories, spanning B2B payments, P2P payments, payments infrastructure, banking, processing, digital wallets, blockchain services and marketplaces.

Companies on our Top 100 list often have a number of main business areas, and therefore were often added to more than one category on the list. Having said this, B2B payments stands out as a key core business offering across players in the list, applying to 58 companies, followed closely by P2P payments at 47. A large number of companies on the list had core business areas in payments infrastructure, banking and payments processing, with the number of blockchain-focused companies rising from last year – from 10 to 15.

Banks account for a significant portion of B2B payments players. However, our own analysis, as well as that from other players in the space, continues to speak to a significantly broader TAM within B2B payments, which in recent years has prompted companies on the Top 100 to increasingly target it as a category.

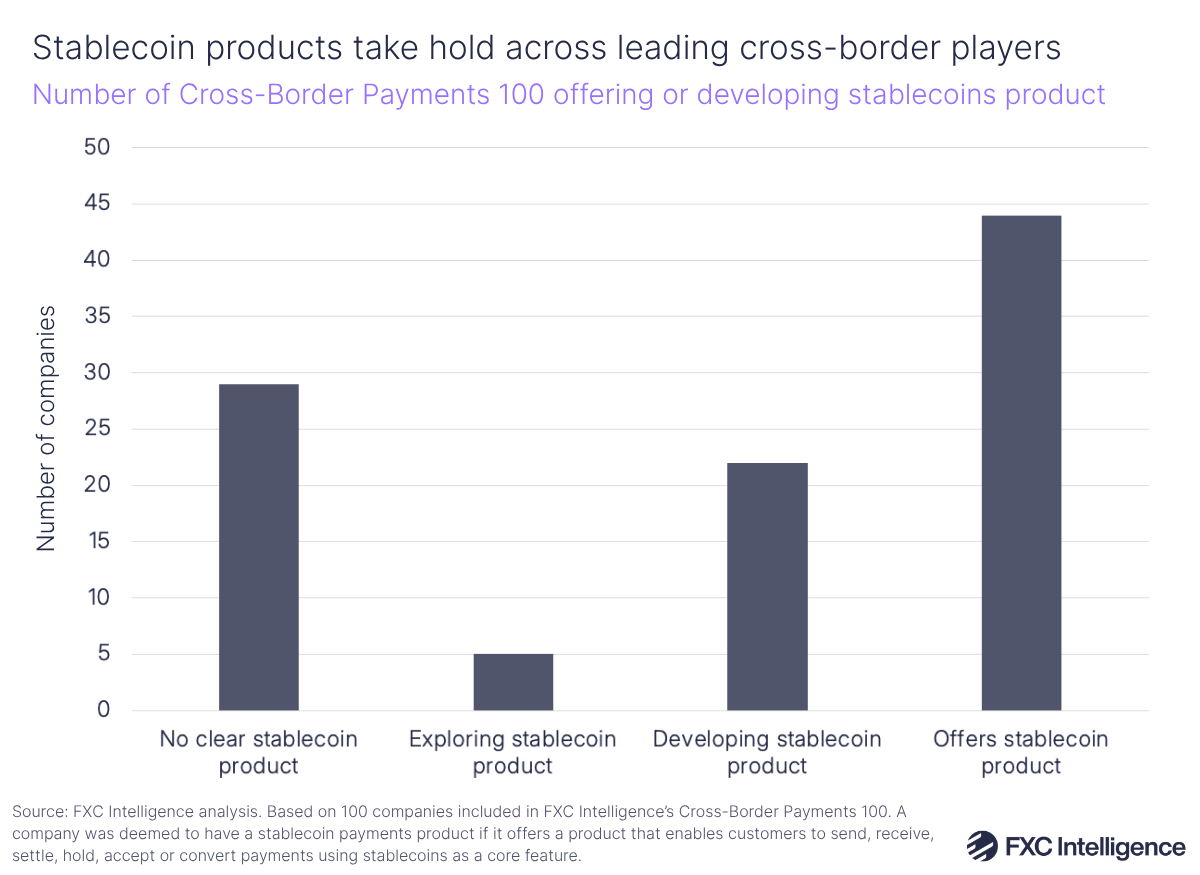

Stablecoins take hold across leading cross-border players

Though there are a smaller number of players with a core blockchain focus (e.g. Stellar and Circle), a significant number of companies in the cross-border payments space have driven investment in stablecoins solutions, either through partnerships with other providers or in issuing their own stablecoins.

Across the list, we identified a total of 44 companies that currently have a live stablecoin product, with 22 developing stablecoin products while five were at the exploratory stage. 29 meanwhile did not clearly identify that they had a stablecoin offering. A company was deemed to have a stablecoin payments product if it offers a product that enables customers to send, receive, settle, hold, accept or convert payments using stablecoins as a core feature.

Companies in each category – spanning banks, remittance companies, fintechs, crypto exchanges and payment processors – are either launching stablecoin products or forming partnerships to support them.

For example, Mastercard recently announced it was acquiring stablecoin infrastructure provider BVNK for $1.8bn, while Visa is piloting Visa Direct payouts to stablecoin wallets. In money transfers, Zepz has introduced stablecoin-linked payment cards while Western Union has launched its own stablecoin on the Solana blockchain. Banks in the space are also piloting tokenised deposits or developing their own stablecoins.

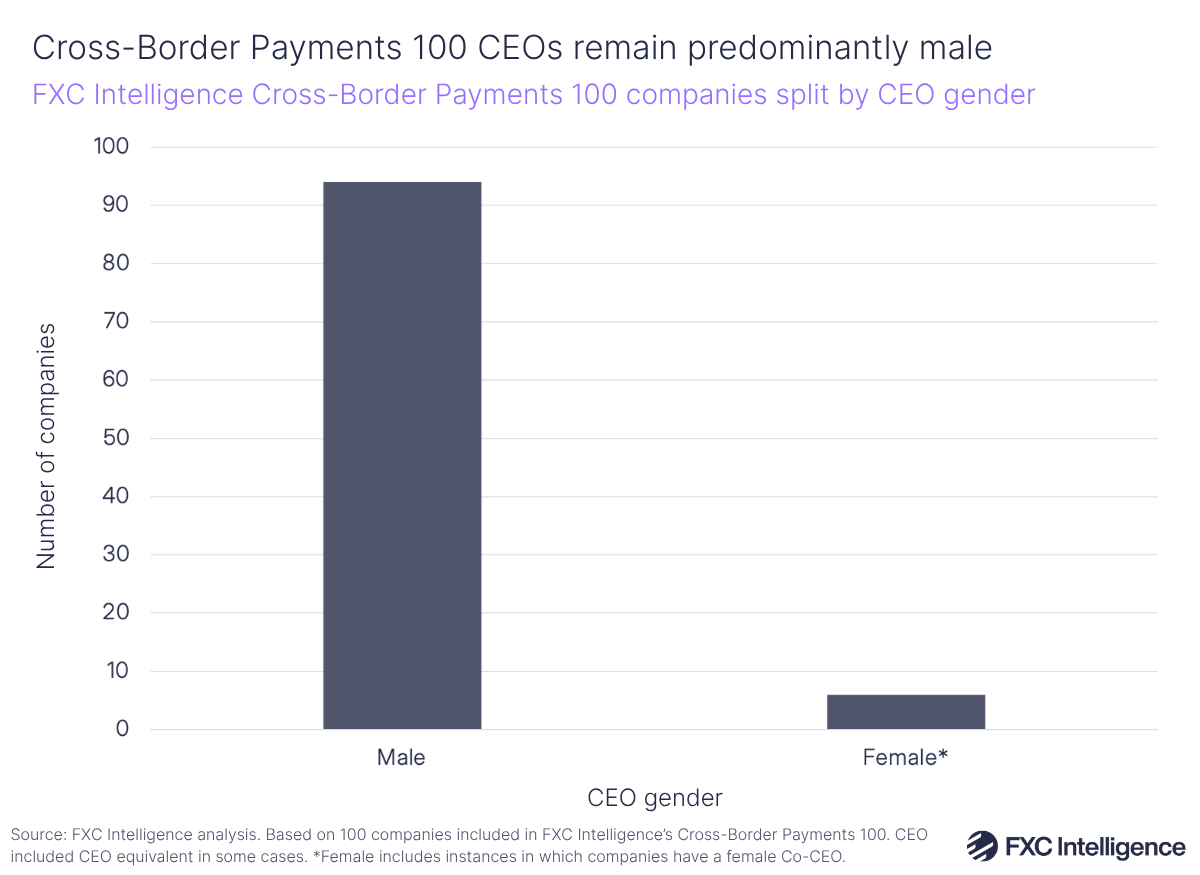

Gender diversity in cross-border leadership remains low

A continued challenge in the cross-border payments space is a lack of gender diversity at the highest level of leadership. In total, there were six female CEOs (or CEO equivalent) in this year’s Top 100, one more than the previous year.

The payments industry continues to drive forward initiatives to help increase gender diversity. For example, Women in Payments runs a formal mentorship programme aimed at developing future female payments leaders, while Innovate Finance recently released the 10th edition of its annual Women in Fintech Powerlist for 2025.

Companies on our Top 100 list are also taking action in this area. Several, for example, have signed the UK’s HM Treasury Women in Finance Charter, under which organisations pledge to set internal targets for gender diversity in senior management and annually publish progress. Wise is one such example, having achieved 40% representation of women at C-suite level, with functional teams made up of more than 40% of women globally.

Other trends across FXC Intelligence’s Cross-Border Payments 100

As part of our review process of leading companies in the space, we identified several other trends based on companies’ most recent developments.

Agentic AI is playing a varied impact across players

Agentic AI remains a nascent area in payments, but a significant number of companies, particularly ecommerce and payment processors, are preparing for a future in which AI may make purchases on behalf of consumers.

For example, OpenAI, Google, Mastercard, Visa and Adyen have worked to develop standards for agentic commerce. Meanwhile, Checkout.com is focusing on building an interoperability layer for this platform. Companies have also spoken about AI creating greater efficiency across areas such as fraud detection, customer service and supporting new product development.

Providers are developing into financial platforms

As businesses in the cross-border payments space have grown, a key theme has been the move from just offering money transfers to full-fledged financial services spanning areas such as cards, payroll and banking services. In particular, many players in the space, such as Revolut and Wise, are pursuing banking licences to extend their business into new areas and give them better access to local payment systems.

Consolidation is shaping the major business players

Several players on the list have either made major acquisitions recently or are beginning to see the benefits from them. Global Payments has acquired Worldpay to create a processor handling $3.7tn in payment volume, while Stripe acquired Bridge for $1.1bn last year, allowing it to launch its new payments-focused Tempo blockchain in March 2026. Recently, Corpay’s Group President Mark Frey explained to us how the company’s 2025 acquisition of Alpha was not just boosting its corporate customers but also its capabilities around virtual accounts.

Acquisitions are enabling companies to expand their reach into new geographies, pursue new products and tap into major growth areas, particularly with regards to building technology stacks and adding new licences.

Emerging markets are a key driver

Several of the new entrants to this year’s Top 100, including bKash in Bangladesh, GCash in the Philippines, PhonePe in India and PagSeguro in Brazil, have helped transform payments in their local markets while also serving a need for inbound remittances. Other players have seen significant growth from their focus on emerging markets, particularly dLocal, which continues to see record volumes on the back of its services to LatAm corridors.

FXC’s Cross-Border 100 points to a changing industry

Assessed rigorously each year, our Cross-Border Payments 100 continues to point to an industry with significant reach and demand globally. As the market continues to grow, companies consolidate and both maturing and inbound players tap into opportunities in the space, we could continue to see more new players appear on next year’s list.