Mastercard’s $1.8bn acquisition of BVNK represents one of the largest moves in the stablecoin space to-date, and comes with significant potential implications for the industry. We take a deep dive into the reality, strategy and potential impact of the deal, with insights from Chris Harmse, co-founder and Chief Business Officer at BVNK.

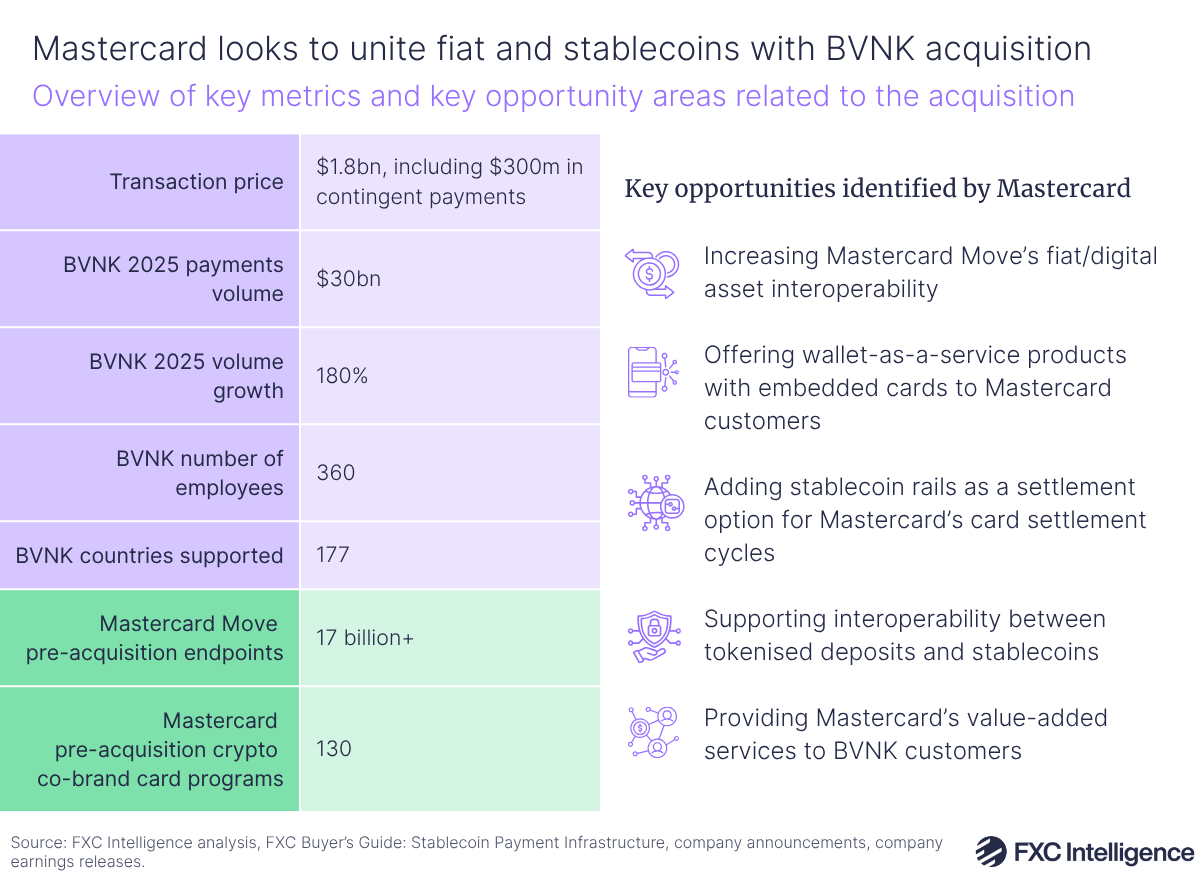

Last week, Mastercard announced that it will be acquiring stablecoin infrastructure provider BVNK for up to $1.8bn, in a deal that includes $300m contingent payments that will be made on delivery of “certain commitments” according to Jorn Lambert, Chief Product Officer at Mastercard, speaking on a call to investors.

He characterised the deal, which is set to be completed by the end of the year as “advancing [Mastercard’s] digital currency strategy whilst opening up incremental opportunities”, including broadening the reach and capabilities of the company’s payment network infrastructure solution Mastercard Move.

For BVNK, meanwhile, the acquisition enables the company to take its offering to an entirely new level.

“The team will be architecting stablecoin infrastructure at Mastercard scale and setting the industry standard for how the world accesses the stablecoin market,” explains Chris Harmse, co-founder and Chief Business Officer at BVNK.

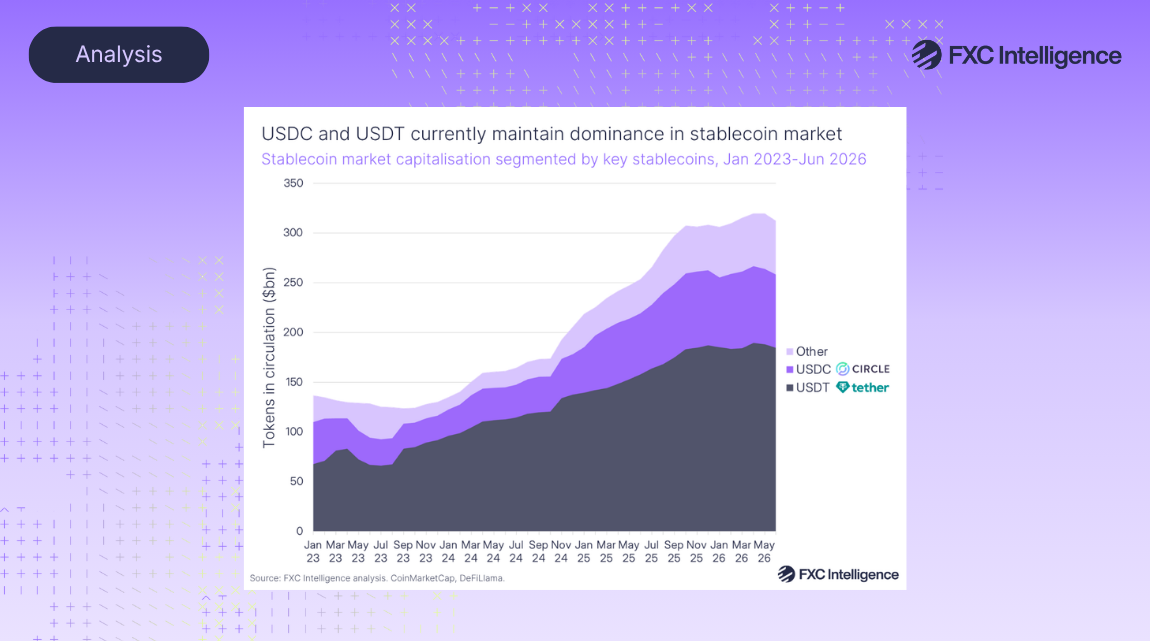

While stablecoins remain less than 1% of the world’s cross-border payments flows, the opportunity is significant, with FXC market sizing data estimating the base total addressable market to be around $17.9tn. 2025 also saw significant growth in stablecoin payments: industry interest has surged since the US passing of the GENIUS Act in the US in July, with the majority of high-profile companies in the sector either announcing or initiating projects using the technology.

This has seen BVNK announce partnerships with a wide range of companies across the sector, while Mastercard has simultaneously been making its own moves in the stablecoin space. However, this acquisition has the potential to significantly step up its efforts, and impact how many in the industry engage with and utilise the technology.

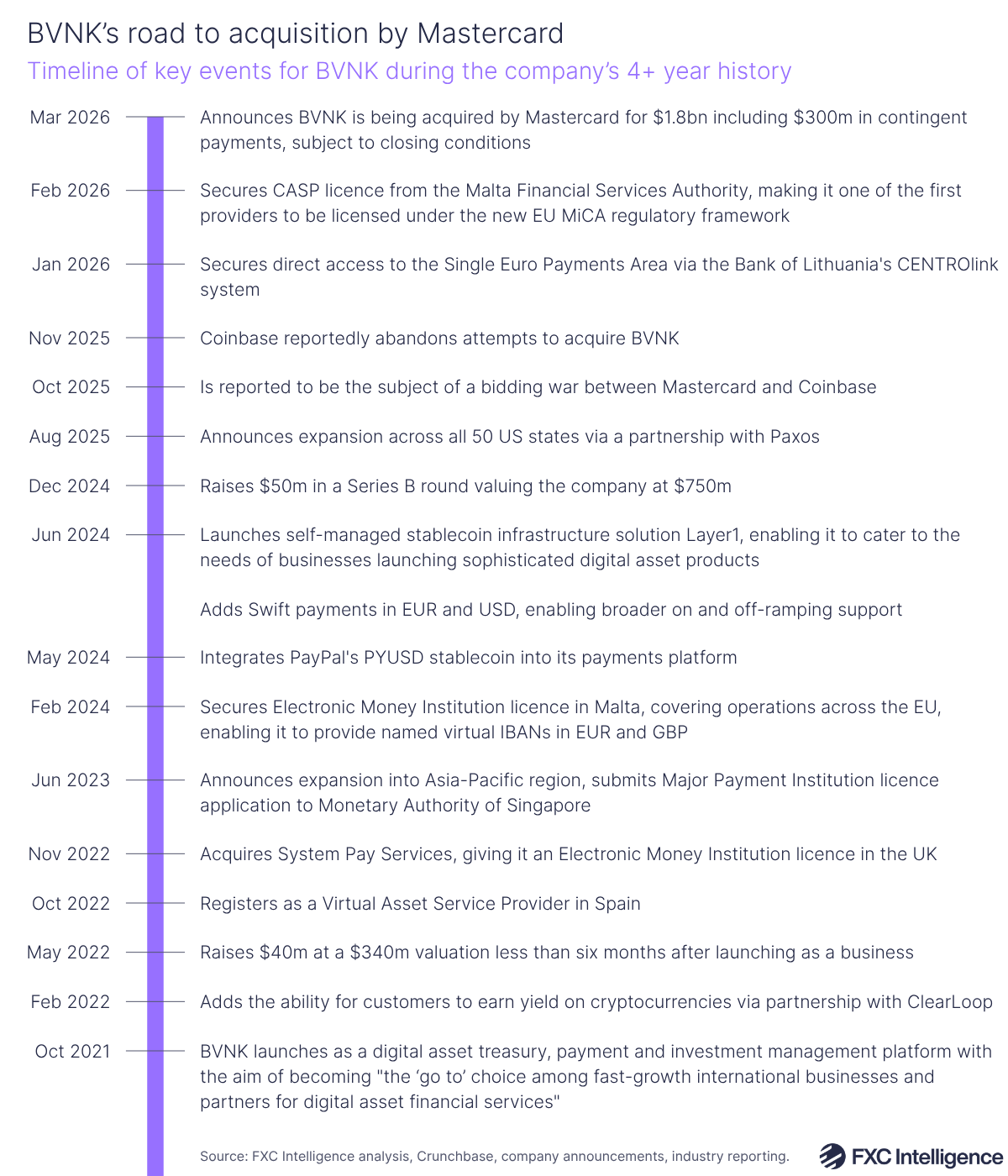

BVNK’s road to a $1.8bn sale

The acquisition announcement comes just four and a half years after UK-based BVNK was founded in London by South African entrepreneurs Jesse Hemson-Struthers, Donald Jackson and Chris Harmse. All three had prior digital asset experience via emerging markets-focused P2P crypto provider Coindirect, which Hemson-Struthers and Jackson co-founded in 2017 and Harmse joined in 2020 as Head of Trading.

At launch in late 2021, the company pitched itself as meeting a gap in the crypto financial services market between providers serving small-scale retail customers and institutional clients handling multi-million dollar flows.

“BVNK aims to plug that gap in the mid-market and become the ‘go to’ choice among fast-growth international businesses and partners for digital asset financial services,” said BVNK co-founder and CEO Jesse Hemson-Struthers, in a release announcing the company’s launch.

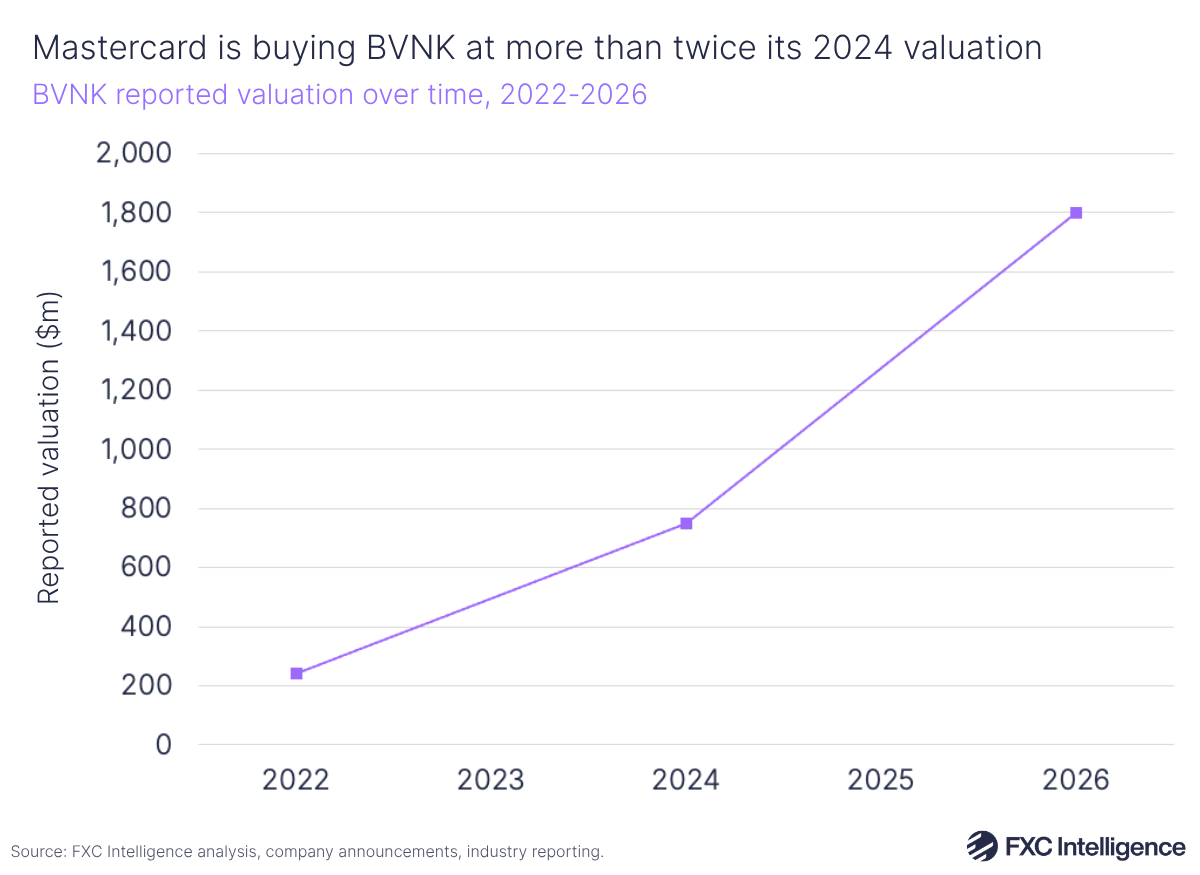

To start with, the company provided payments, treasury and investment management solutions to businesses. This saw it provide business accounts that included a KYB solution to store and pay funds in GBP, EUR and USD as well as digital asset wallets, with additional capabilities to earn interest on capital and a Markets solution for large-volume trades. Less than a year later the company had closed a $40m funding round that valued BVNK at $340m and by the end of 2022 had acquired System Pay Services, giving it access to the company’s UK Electronic Money Institution licence and e-money solutions for businesses.

Over the following years it has steadily built its solutions out further to support companies developing digital asset solutions for their own end-users via managed solutions, as well as in 2024 adding a self-managed solution, Layer1, that is designed to rival providers such as Fireblocks.

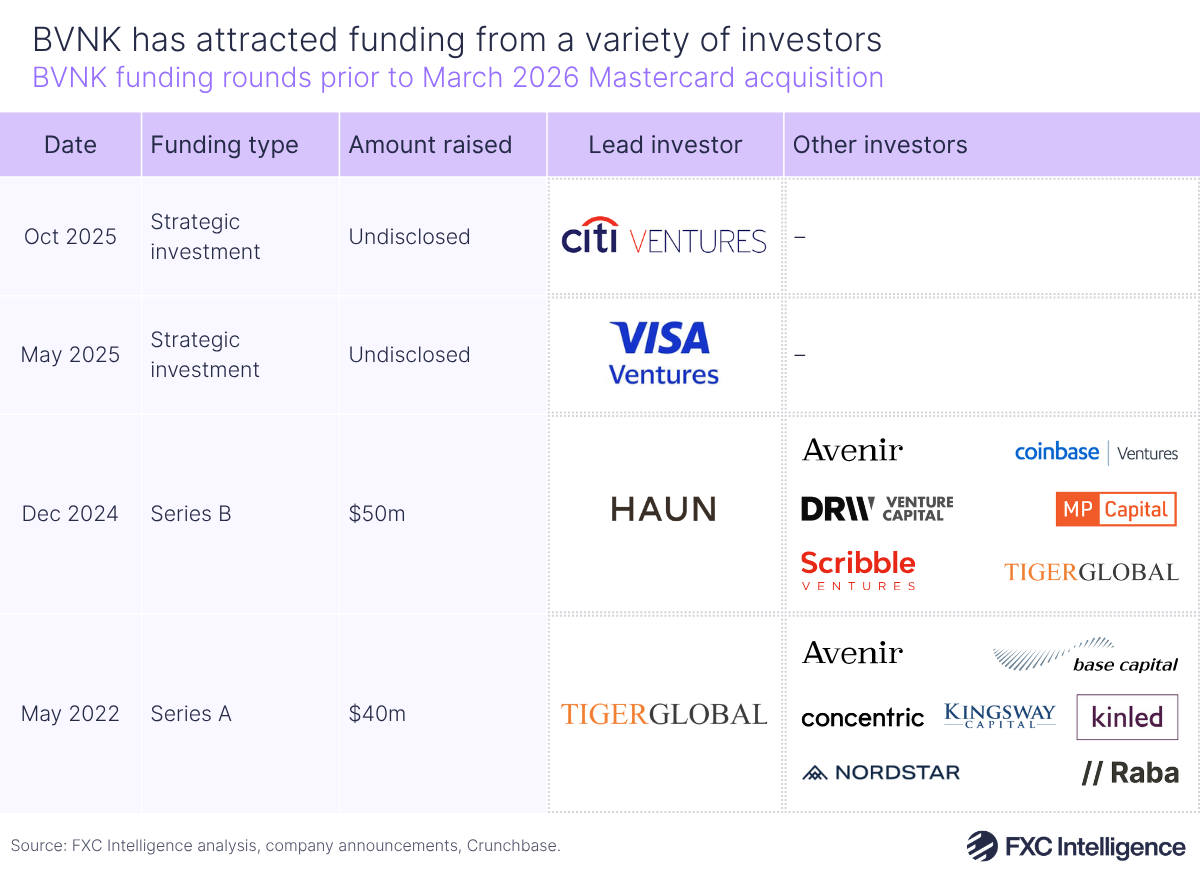

BVNK’s funding history

As the payments industry began to engage with stablecoins in particular, the company also shifted its narrative and attention to this part of the digital assets ecosystem. By the time the company announced it had closed its Series B funding round in December 2024 it was describing itself as “powering stablecoin payments for businesses worldwide”.

The funding round, which saw BVNK raise $50m, also saw the company’s valuation climb to $750m – significantly above its 2022 valuation, although less than half of what it would be acquired by Mastercard for less than 18 months later.

In both its major funding rounds the company has seen investment from high-profile investors, including Tiger Global Management, Coinbase Ventures and Menlo Park Capital. However, the company has also more recently seen strategic investment from both Visa Ventures in May 2025 and Citi Ventures in October 2025 as the company’s profile jumped on the back of the GENIUS Act-fuelled rise in payments industry interest in stablecoins.

Responding to growing industry adoption

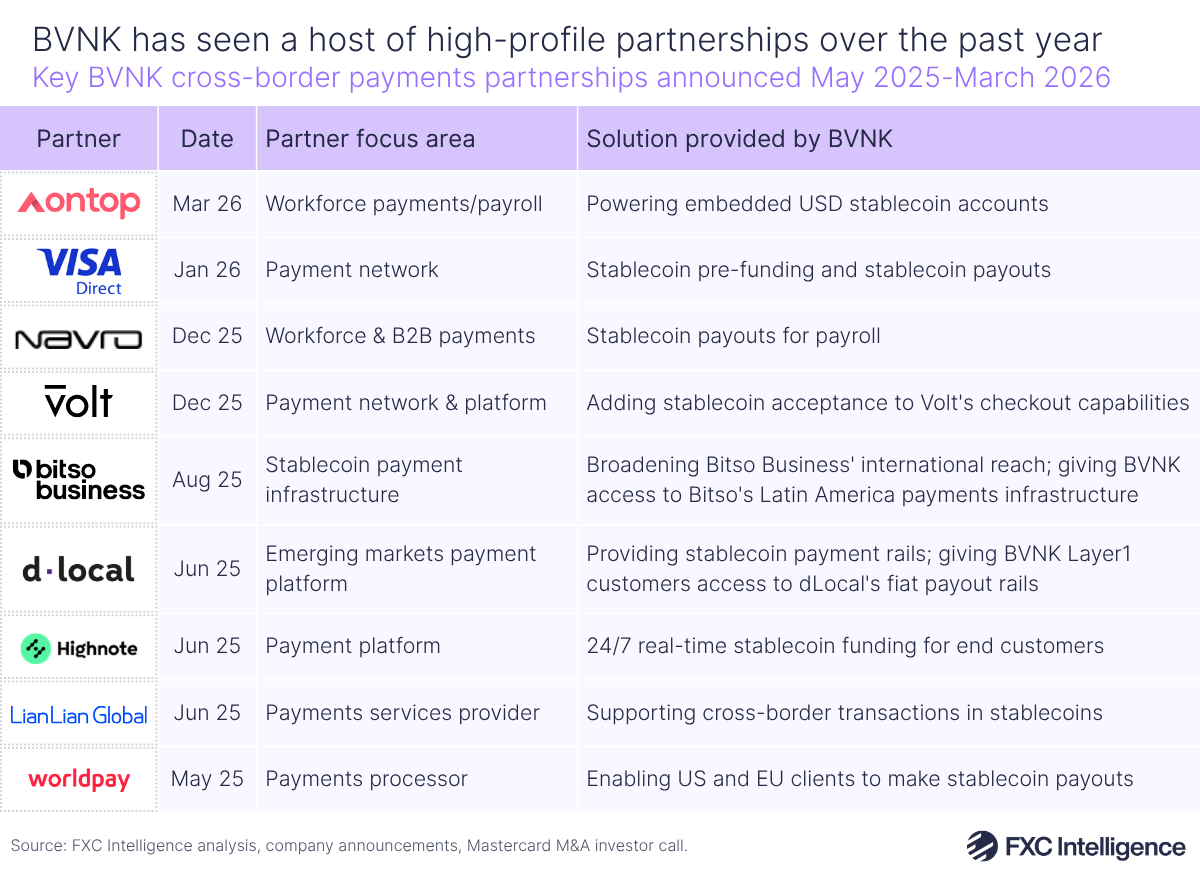

The cross-border payments industry has seen a dramatic increase in interest in stablecoins over the past year or so, and this has seen BVNK announce a number of high-profile partnerships with different organisations.

Visa’s investment was also followed by a high-profile partnership between BVNK and Visa Direct, which was announced in January 2026. Initially designed as a pilot with a view to broader rollout over time, this sees BVNK enable Visa Direct customers to both fund payouts and receive payments in stablecoins. However, it is unclear if this partnership will remain in light of the Mastercard acquisition, with Mastercard’s Lambert telling investors that “we don’t know to what extent that will be continuing” and characterising the partnership as “a very small part of [BVNK’s] overall picture”.

In addition to the Visa Direct announcement, the company has also inked deals with payment processor Worldpay; a variety of payments platforms, including dLocal and Highnote; and other stablecoin payments providers, including Bitso Business.

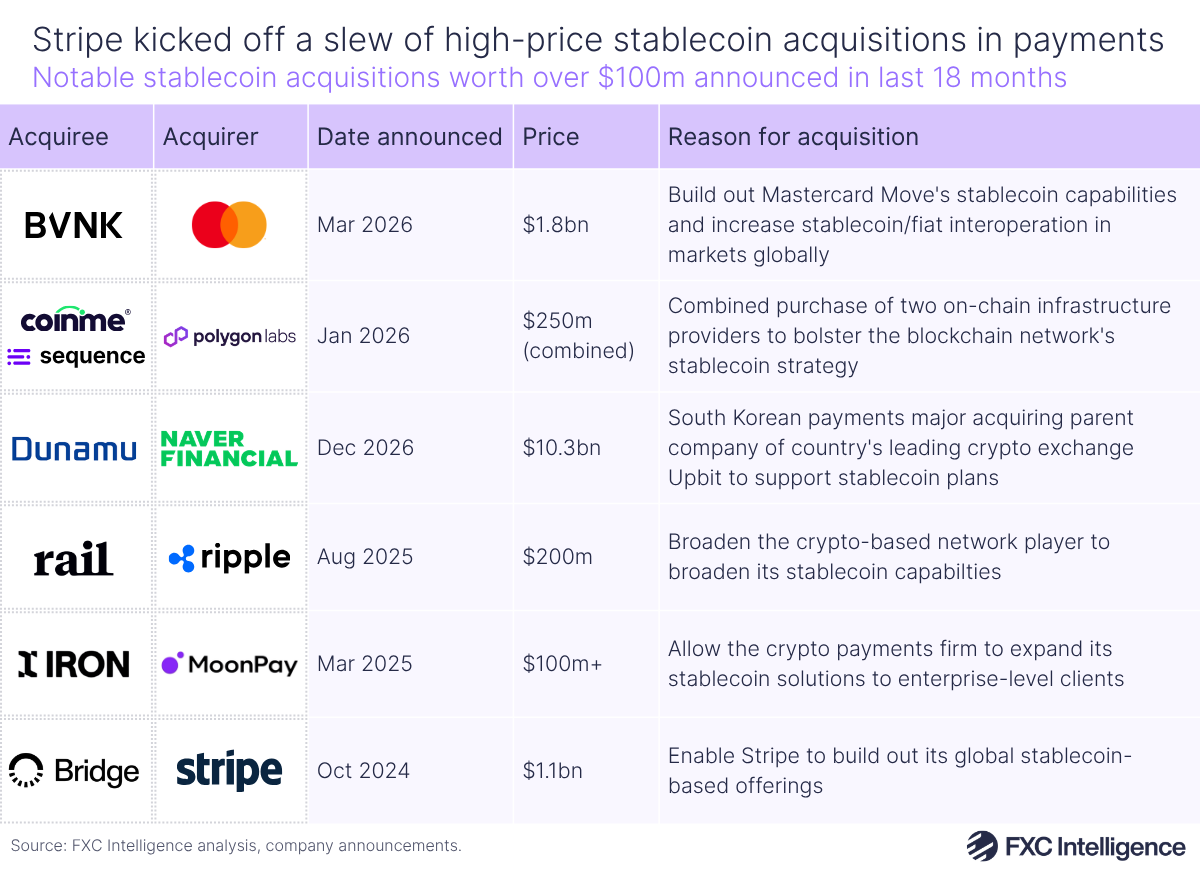

Broader industry acquisitions

BVNK is the latest in a number of stablecoin-focused companies to be acquired in big-ticket deals. Stripe’s late-2024 acquisition of BVNK rival Bridge for $1.1bn was arguably a key driver in the surge in interest in stablecoins among payments companies. Since then, while many companies have opted to partner rather than buy, there have been a number of acquisitions at all scales, with Ripple and MoonPay among those to make nine-figure acquisitions to bolster their stablecoin offerings.

Meanwhile, there have also been a flurry of reports of other potential acquisitions that have not come to pass. In October 2025, Fortune reported that BVNK was in advanced talks with both Coinbase and Mastercard, while later that same month Mastercard was reportedly close to acquiring BVNK competitor zerohash for between $1.5bn and $2bn, although the deal was ultimately abandoned in January of this year.

What Mastercard is getting in BVNK

Mastercard’s acquisition of BVNK sees it acquiring a company that is one of the leading providers of managed stablecoin payments infrastructure solutions globally – and which FXC Intelligence identified as a market leader for treasury payments in FXC Buyer’s Guide: Stablecoin Payments Infrastructure earlier this year.

Highlighting the provider’s mix of send, receive, convert and hold capabilities for digital currencies, Mastercard’s Lambert told investors that BVNK’s applications spanned B2B, P2P and “me-to-me” (digital currency wallet funding).

“BVNK abstracts the complexity of blockchain payments: it initiates, routes and settles payments. Its modern API-driven platform integrates easily in existing platforms across the ecosystem, enabling customers to access liquidity providers, stablecoin issuers and multiple chains through a single connection without having to build or maintain this infrastructure themselves,” he added.

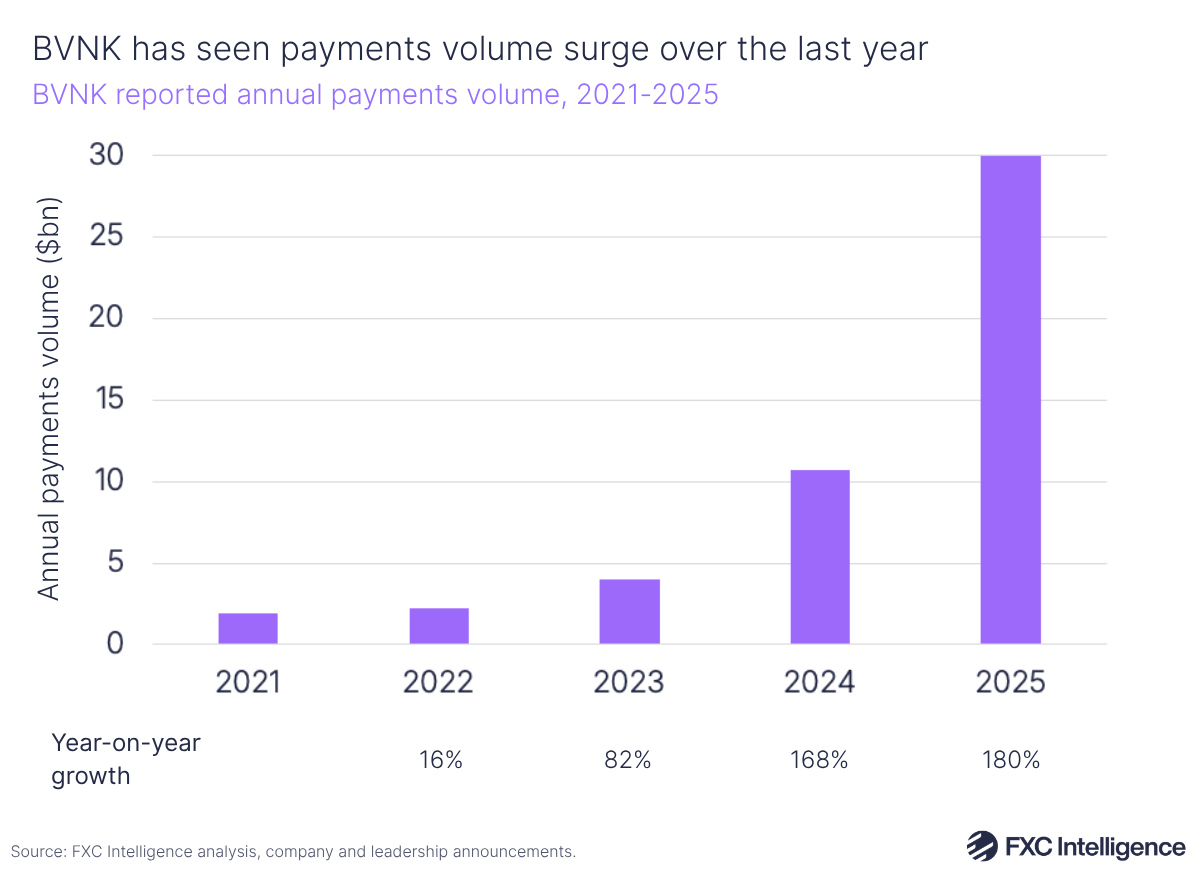

These capabilities have seen adoption of the company’s solutions climb significantly over the past year, with BVNK seeing payments volume reach $30bn in 2025, a 180% increase on 2024.

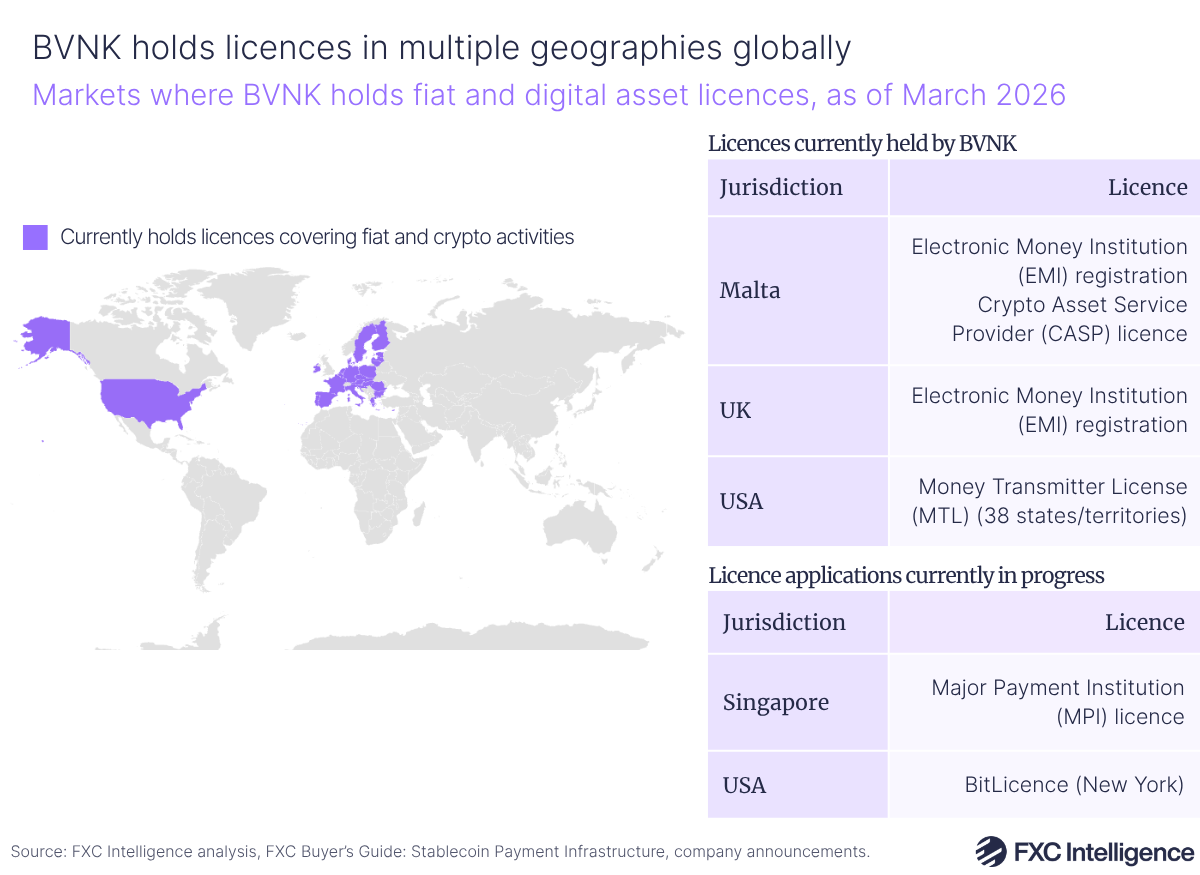

Lambert also noted the company’s comparatively strong range of licences, noting that BVNK “embeds licensing, compliance and regulatory tooling directly into its offering”.

BVNK currently holds licences covering digital asset and fiat activities in the EU, UK and US, and is notable for being one of the first stablecoin infrastructure providers to receive a crypto asset service provider (CASP) licence in the EU under the newly implemented Markets in Crypto-Assets Regulation (MiCA). The company is also in the process of securing a further licence in the US, as well as a Major Payment Institution licence in Singapore that is key to broadening its APAC offering.

While the company combines broad capabilities, market reach and licensing, BVNK’s Harmse argues that the appeal for the card network player was “all about the team plus the technology”.

“BVNK has assembled one of the best teams in digital payments and stablecoin infrastructure anywhere in the world – people who are actively shaping the future of the global money movement,” he says.

“With this deal we’re combining BVNK’s technology and talent with Mastercard’s global ecosystem to create an entirely new frontier.”

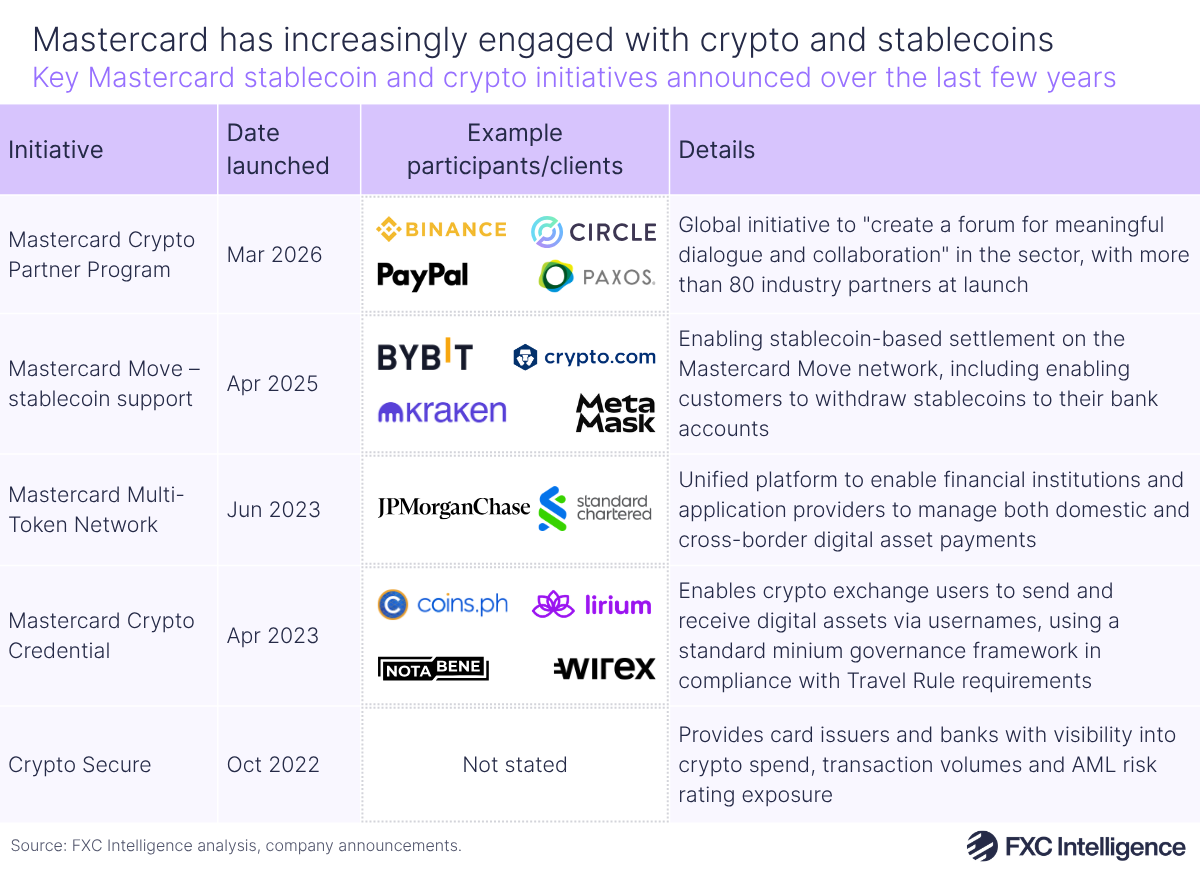

Mastercard’s existing stablecoin initiatives

The acquisition comes as Mastercard has made a growing number of moves to bolster stablecoin and broader digital asset capabilities across its network, some of which have been running for several years. While many of its initial solutions focused on crypto transactions and related activity, the company has also increasingly broadened into stablecoin-based capabilities.

First launched in 2023, its Multi-Token Network connects banks with blockchain technologies, enabling them to manage domestic and cross-border payments using digital assets, while in 2025 the company added stablecoin support to its payment network solution Mastercard Move. While this initially targeted crypto-first providers such as exchanges, the company has since also added the ability to pay stablecoins out to digital asset wallets on the Mastercard Move network via a partnership with Thunes.

Shortly before it announced its acquisition of BVNK, the company also announced the launch of the Mastercard Crypto Partner Program. Designed as a “shared framework for collaboration”, this sees Mastercard enable would-be developers of digital asset-based products to partner with Mastercard teams and organisations across the full spectrum of crypto-fiat capabilities, including issuers, infrastructure providers, on and off-ramp providers, crypto card enablers and blockchains. In doing so, it is positioning itself as a key growth enabler in the space, aided by what Lambert describes as the company’s “vibrant network of partners”.

“We will continue to focus on empowering our customers and our partners to innovate and scale on an open network,” he added.

Combining Mastercard and BVNK: Commercial opportunities and strategic evolution

In the investor call, Lambert told Mastercard investors that the acquisition would “advance [Mastercard’s] digital currency strategy while opening up incremental opportunities”.

“The addition of BVNK to the Mastercard network will bring more optionality and end-to-end capabilities to meet the needs of our customers and partners for the years ahead, all aligned with our current strategy and focus on driving long-term growth,” he added.

Noting the recent climb in stablecoin adoption as “a globally accessible, borderless real-time settlement system” while stressing that “there is no consumer problem to be solved here”, he highlighted how BVNK’s solutions would be used to increase the strength and breadth of Mastercard’s digital asset capabilities.

This includes broadening the support for digital assets on Mastercard Move, including greater interoperability between fiat currencies and digital assets, as well as adding new stablecoin-based solutions, including the provision of wallet-as-a-service products that include embedded Mastercard cards and adding stablecoin rails as a settlement option its card settlement cycles. The company also sees the potential to provide its value-added services, including its safety and security solutions, to BVNK clients.

“BVNK will power stablecoin capabilities across Mastercard’s payment endpoints, enable 24/7 stablecoin settlement for processors and acquirers and more, while Mastercard provides BVNK with global fiat infrastructure (push-to-card, account, wallet),” explains Harmse, adding that “these synergies can unlock incredible value for customers on both sides”.

“What makes this combination powerful is the balance between independence and scale. On the BVNK side we will continue operating with our own roadmap, culture and speed of innovation, while gaining access to Mastercard’s global infrastructure, fiat rails and card capabilities. At the same time, Mastercard can integrate stablecoin functionality into their network.”

Enabling stablecoin/fiat interoperability

While there are shorter term commercial benefits, the ability to expand interoperability between digital assets and fiat currencies is a particular focus for Mastercard.

“We plan to make it seamless to move from fiat to digital currencies and vice versa by connecting and vertically integrating the Mastercard and BVNK stack,” Lambert told investors, highlighting that the company ultimately saw this broadening to include not only stablecoins but also tokenised deposits.

Pointing to existing use cases across remittances, payouts, P2P payments and B2B payments, as well as growing potential for capital markets and treasury management, Harmse says that the key to achieving this kind of seamless movement lies in security and compliance.

“The key to support these use cases is to connect these rails seamlessly to existing fiat rails, applying the security, reliability and compliance standards that are the bedrock of payments,” he says.

“As different digital currencies and tokenised deposits are issued and their use cases scale, so too does the need for highly secure and compliant payment orchestration between fiat and digital currencies across multiple chains. Bringing the capabilities of BVNK and Mastercard together will deliver trusted interoperability at scale that can seamlessly connect across systems.”

Industry implications and future potential

In looking to combine the capabilities of BVNK and Mastercard, the payment network is making this interoperability narrative central to how it is thinking about the acquisition, and in doing so is pushing against prior assumptions that digital asset-based networks are a challenger to fiat-based payment networks such as Mastercard Move.

“The question is not whether stablecoin rails are better than fiat rails, but how both can be combined in a single offering and distributed scale,” said Lambert.

If it succeeds in this approach, it could see the current perception division between fiat and digital assets narrow, and so help change perceptions around the role stablecoins can play in payments.

“We’re creating a completely new model for delivering stablecoin infrastructure at scale. Mastercard brings a trusted network that moves trillions across more than 200 countries, along with deep relationships with financial institutions worldwide,” explains Harmse.

“BVNK provides some of the most advanced stablecoin infrastructure in the market, processing tens of billions of dollars annually for global payments leaders. Together, we’re creating infrastructure that makes an entirely new business model possible.”

Ultimately, however, this acquisition is a bullish statement from Mastercard on the future role of stablecoins in cross-border payments and beyond.

“We expect that in time, almost every financial institution and fintech will provide digital currency services to their customers, be it with stablecoins of tokenised deposits,” said Lambert.

If stablecoins do ultimately gain the levels of adoption their proponents project, Mastercard is putting itself in a strong position to capitalise on the shift.

“As stablecoins grow and promise to represent a meaningful share of global cross-border payments by 2030, this partnership positions us to unlock entirely new revenue opportunities neither company could capture alone,” concludes Harmse.