Visa and Mastercard have released their respective earnings results covering calendar Q1 2026 (Visa’s financial Q2 2026), with cross-border volumes remaining a key growth driver for both companies.

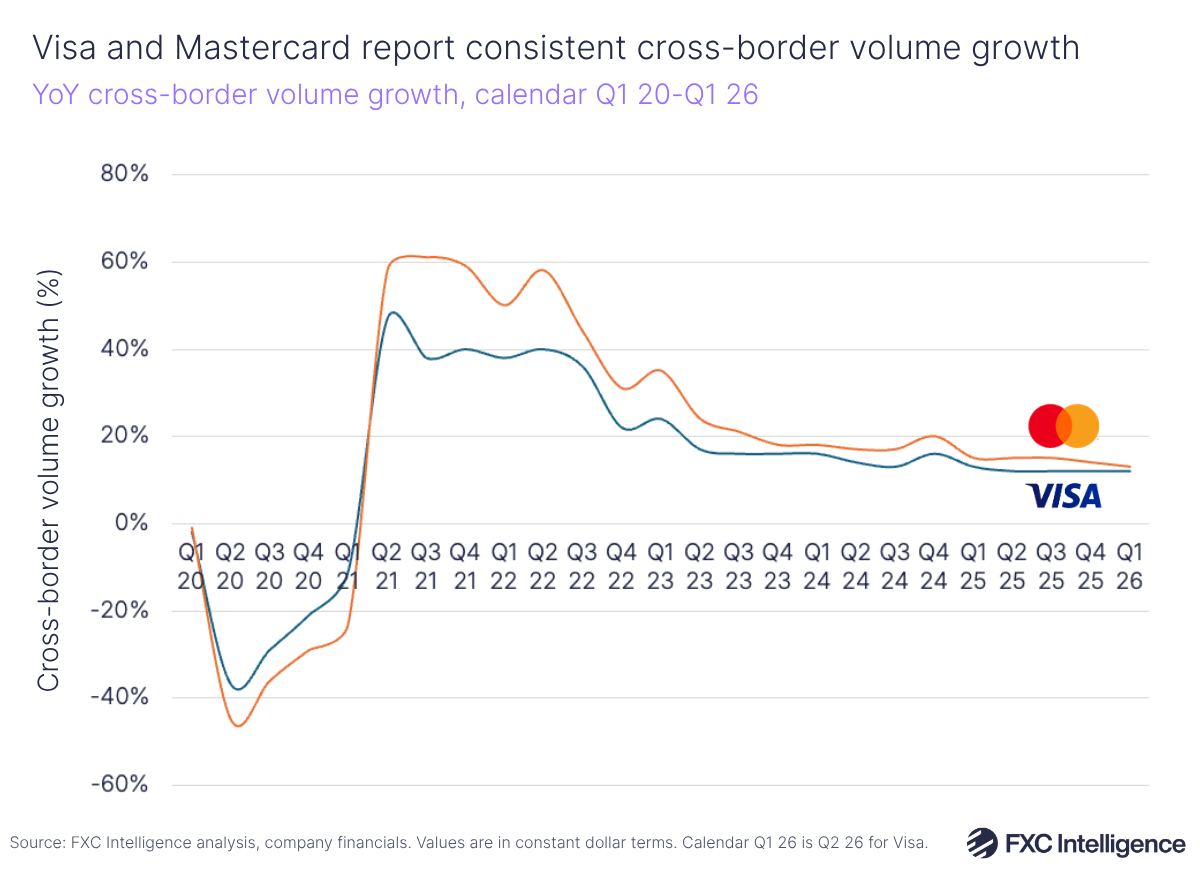

Visa and Mastercard do not share exact cross-border volumes, although both report their cross-border volume growth numbers. In their latest earnings – covering January to March – both saw strong cross-border volume growth, supporting revenue growth for each.

Here, we take a look at some of the key drivers behind recent cross-border growth and explore how both companies have advanced their stablecoin, AI and agentic strategies in the last quarter.

Visa’s Q1 2026 earnings highlights

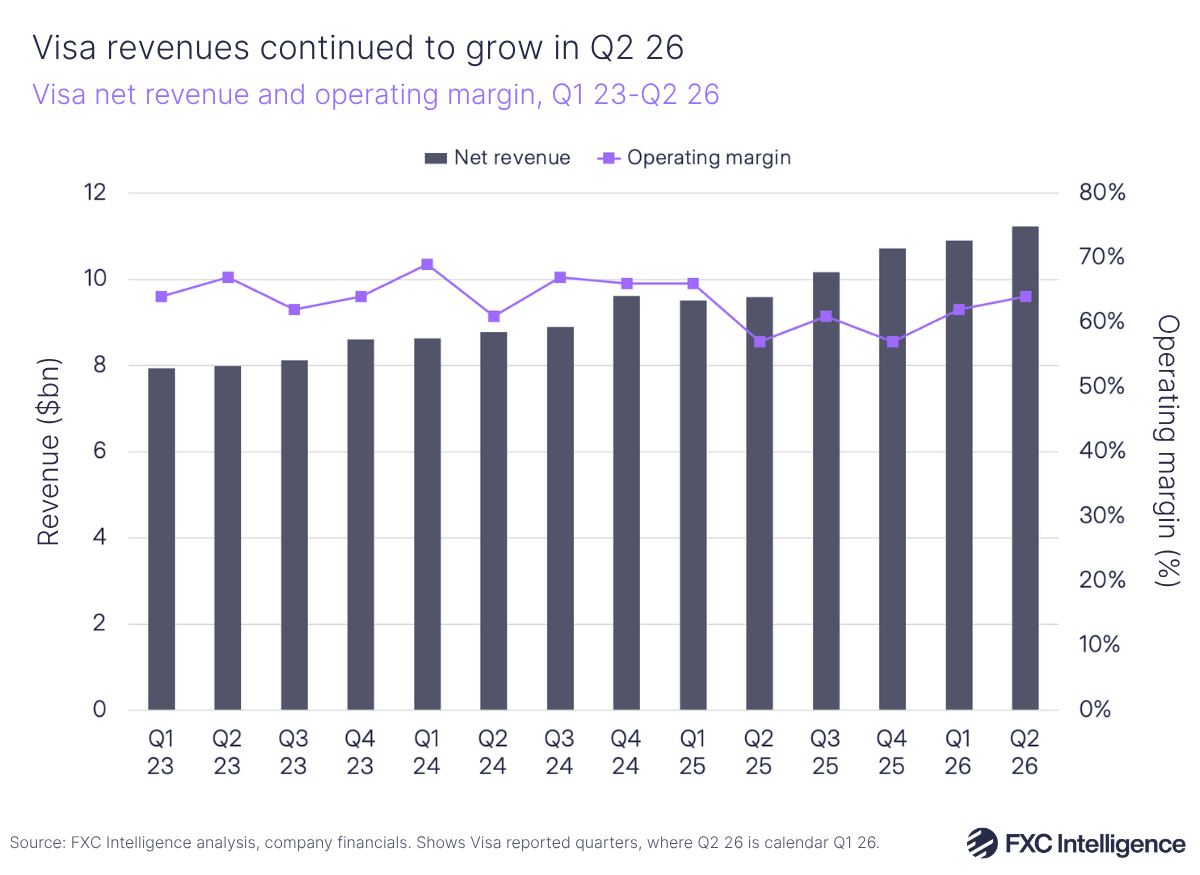

Visa’s strongest net revenue growth since 2022 underpinned its Q2 2026 results (calendar Q1 2026), increasing 17% YoY to $11.2bn or 16% on a constant-dollar basis.

This growth was largely driven by stronger than expected growth in value-added services revenue and lower than expected incentives, which were supported by levels of volatility that exceeded expectations.

Visa reported that cross-border volume grew 11%, outpacing a 9% increase in global payments volume on a constant-dollar basis. Meanwhile, cross-border volume rose by 11% and total processed transactions grew 9%. Growth of international payments volume also remained at a similar rate as seen over recent quarters, up 10% YoY.

Cross-border ecommerce volume also grew 13% YoY, while travel-related cross-border volume was up 10% in Visa’s financial Q2 – which CFO Christopher Suh attributed to improved US inbound volume, which helped offset the impact of ongoing conflict in the Middle East.

Visa Direct saw a 23% increase in transactions to 3.7 billion, driven by consistent strength in domestic and cross-border alike. The money movement platform is also set to enable real-time cross-border remittances and payouts into Mainland China via a connection to UnionPay International’s MoneyExpress platform.

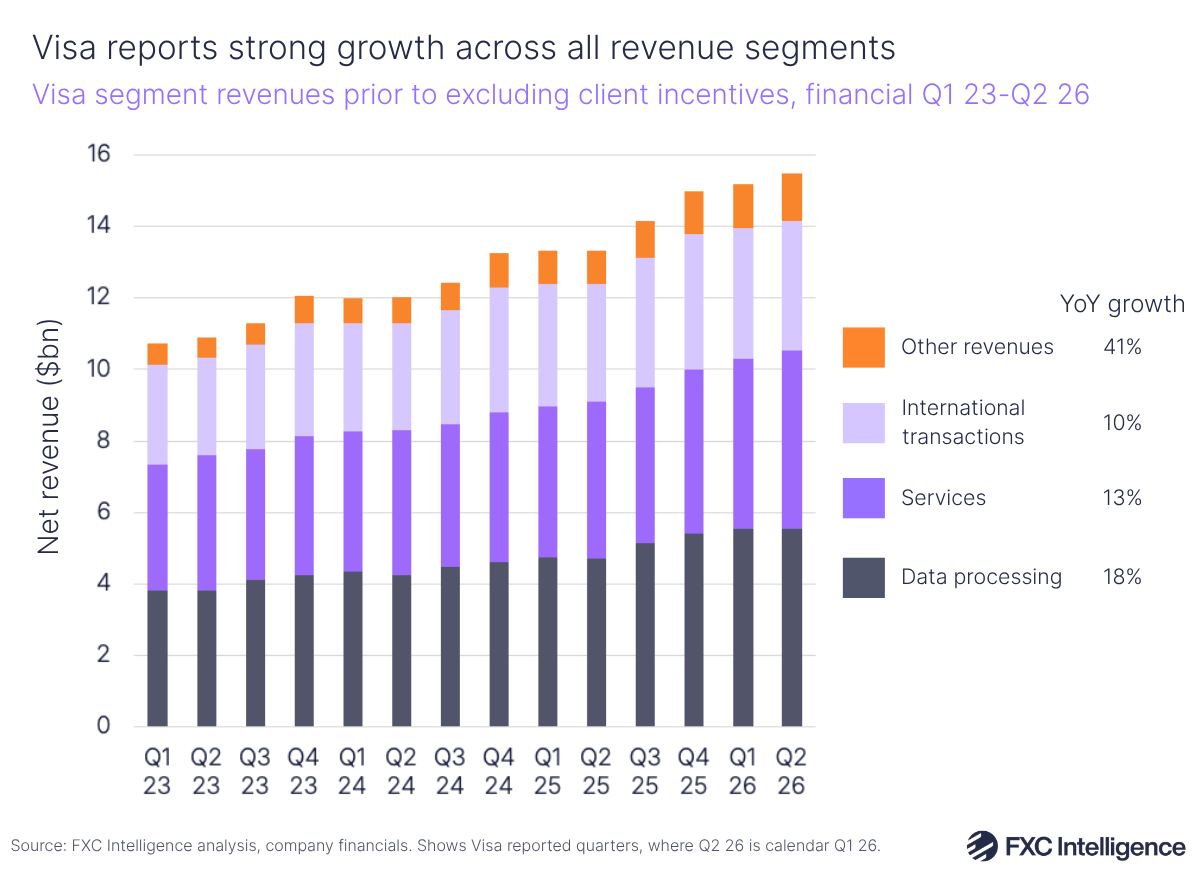

Of Visa’s revenue segments, international transaction revenue continues to grow the slowest, posting a 10% YoY increase to $3.6bn, slightly outpaced by 11% growth in cross-border volume excluding intra-Europe – a key driver of this component. Although Suh described the FX as “favourable”, he explained that this was offset by impacts from volatility lower than last year’s levels, mix and hedging.

Data processing retains the largest share of total revenues at 36%, driven by 18% growth to $5.5bn – supported by strong value-added services performance and higher cross-border transaction mix. Service revenue, consisting largely of fees collected on payment volumes, continued to see strong growth, rising 13% YoY to $5bn and growing its share of total revenues to 32%. Other revenues continued to grow the fastest of all of Visa’s revenue segments since Q2 2023 (calendar Q1 2023), at 41% to $1.3bn, although it still represents the lowest share of total revenues at 9%.

Visa advances stablecoin and AI plans

During the latest earnings call, Visa outlined that consumers across the globe are increasingly engaging with stablecoin-linked cards that provide on and off-ramps that enable them to spend stablecoins online at physical retail locations where Visa cards are already accepted. Businesses are also using these cards to purchase digital advertising and supplies, with Visa saying that stablecoin payment volume increased nearly 200% YoY in Q2.

The company has now added five additional blockchains – Arc, Base, Canton, Polygon and Tempo – to its existing network for settlement. CEO Ryan McInerney also revealed that Visa now has a $7bn annual run rate of stablecoin settlement volume – 52% higher than the $4.6bn run rate seen in Q4. McInerney says this forms part of Visa’s plans to establish itself as a “key interoperability layer” between stablecoin infrastructure and real-world solutions for consumers and businesses.

Visa also outlined that it believes AI and agentic commerce can significantly expand its addressable market by accelerating the digitalisation of commerce and B2B.

“Agents will create significantly more transactions. Agents will intelligently split purchases across multiple transactions, optimising price, timing and value to the buyer,” explains McInerney. “Importantly, in some use cases, we expect agents will pay for their own data and resource consumption transaction by transaction and event-by-event, which creates an entirely new category of commerce with microtransactions.”

Although it remains early days for this type of commerce, Visa says it is already seeing growth in agentic commerce and transactions using Visa agentic tokens. In April, Visa also launched a new solution that enables businesses to connect to and participate in AI-powered commerce, Intelligent Commerce Connect. The solution acts as a network protocol and token vault-agnostic ‘on ramp’ to agentic commerce for agent builders, merchants and enablers.

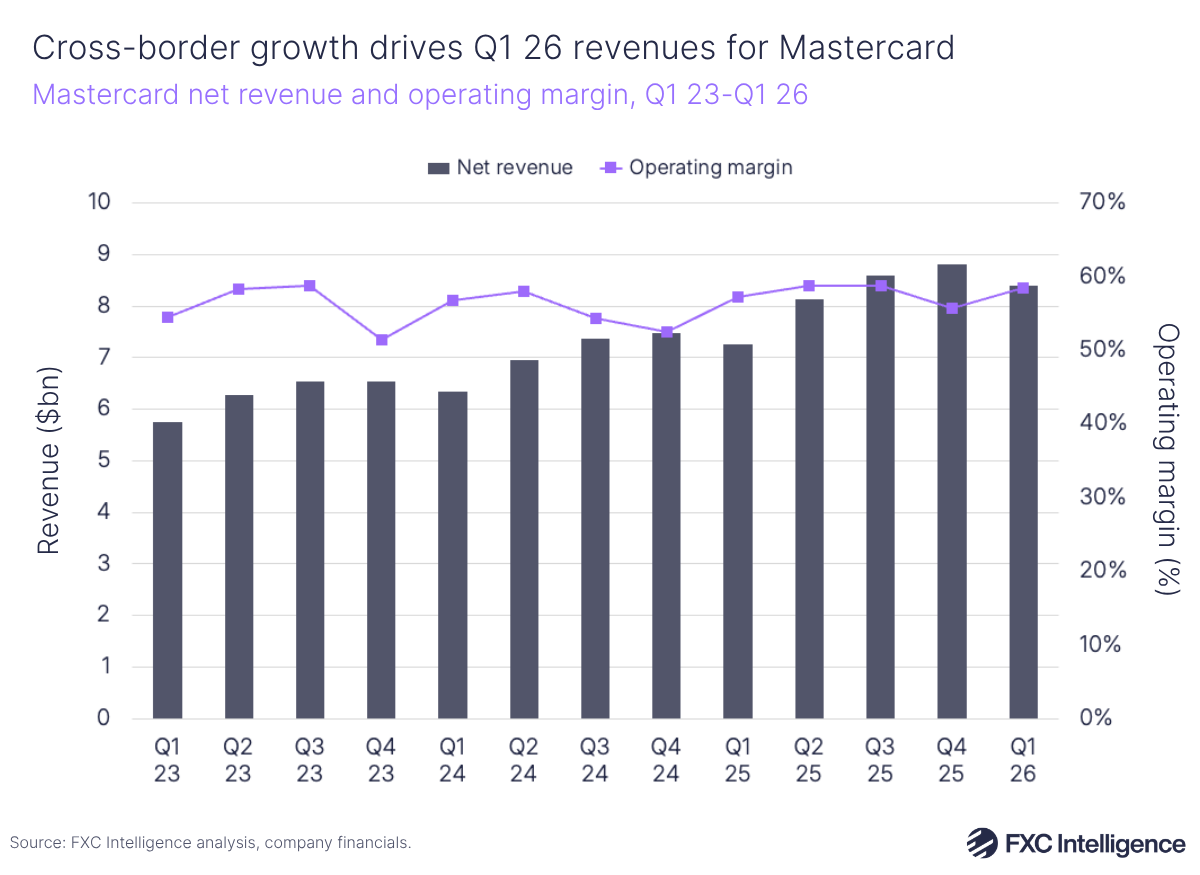

Mastercard’s Q1 2026 earnings highlights

Mastercard saw its net revenue increase 16% YoY (or 12% on a currency-neutral basis) to $8.4bn in Q1 2026. Operating income rose 18% to $4.9bn, giving the company a 58% operating margin – a 1% increase on Q1 2025. Mastercard said these successes were driven by continued growth in its payment network and Value-Added Services and Solutions.

Payment network net revenue increased 12% for the third quarter running, reaching $4.9bn – driven by domestic and cross-border transaction and volume growth. Cross-border assessments – fees charged on cross-border transactions – increased 18%, higher than the 13% growth in cross-border volume. Mastercard attributed this difference to favourable pricing in international markets.

Mastercard’s payment network remains the biggest contributor to its net revenue, generating 59% in Q1. Value-added services and solutions revenue, which makes up the remainder of Mastercard’s revenue, continues to see faster growth and rose 22% YoY to $3.5bn.

CEO Michael Miebach explained that Mastercard Move, the company’s portfolio of money transfer capabilities, “continues to scale”, having extended its connections with the Bank of Shanghai to support SME trade and remittances into and out of China. The company is now targeting insurance disbursement flows in the US in partnership with One Inc, a digital payments network for the insurance industry.

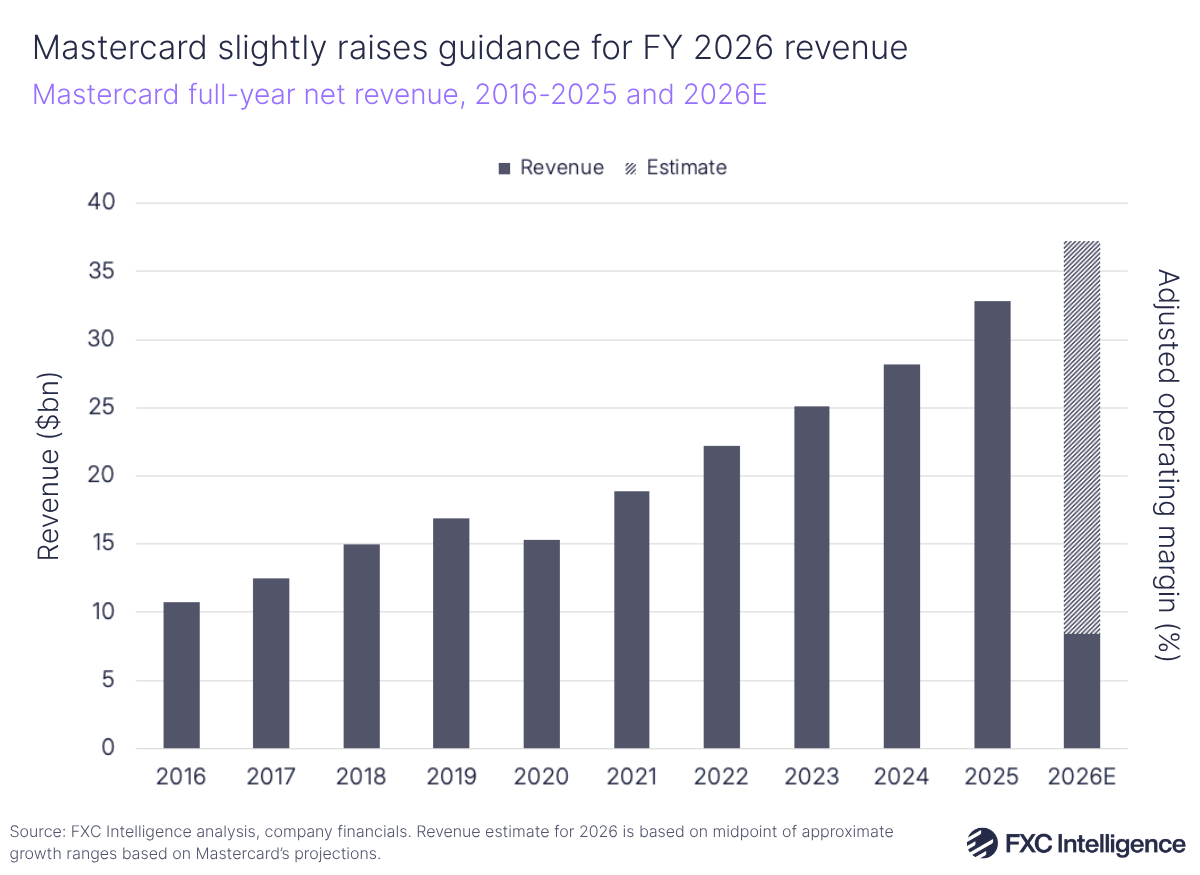

Following its strong start to the year amidst difficult macroeconomic conditions, Mastercard has slightly raised its guidance for FY 2026 to the high end of low double digits to low teens growth compared to 2025. CFO Sachin Mehra explained this includes estimates based on the impact of conflict in the Middle East, which the payments giant expects to have the largest impact during the current quarter.

Mehra also noted that Mastercard’s heavy diversification across geographies, products, consumer segments and services has enabled it to continue to deliver growth, despite significant headwinds.

Mastercard continues development of stablecoin infrastructure and AI standards

Throughout the Q1 earnings call, Mastercard also discussed its planned acquisition of BVNK, explaining that it hopes to pair the stablecoin infrastructure provider’s technology with its global payment network to help connect stablecoin and fiat rails, while solving challenges surrounding interoperability for digital assets. Ultimately, it plans to provide the required interoperability for digital assets, including stablecoins and tokenised bank deposits.

This comes with Mastercard already enabling stablecoin settlement and having integrated stablecoins into Mastercard Move. CEO Michael Miebach also shared that crypto exchange OKX is in the process of expanding its Mastercard crypto card programme into Europe.

“Fundamentally, what we see is that stablecoins and tokenised deposits are here to stay. They’re going to be an important part of the financial ecosystem going forward. We believe that tokenised money will occupy a meaningful part of the money movement in the future,” he added.

The US GENIUS Act, as well as similar regulation in other markets, is providing the regulatory clarity necessary for Mastercard to make significant advances regarding stablecoin technology, with the company explaining that, should the CLARITY Act come into effect, this will add to its momentum.

AI and agentic advancements also formed part of the agenda during Mastercard’s earnings.

Miebach shared that Mastercard is also deepening its partnership with OpenAI and “working to enable agent-to-agent payments and collaborating to embed our services across their solutions while using their tools as an enterprise customer”.

In Q1, it launched Verifiable Intent in collaboration with Google, a record of what a user authorised when an AI agent acts on their behalf. The FIDO Alliance, the industry association developing authentication standards, is now using it as a foundation to set security standards in the space. Mastercard plans to integrate Verifiable Intent into its Agent Pay offering in the coming months, with Miebach saying its significance “cannot be underestimated”.