Banks, neobanks, financial institutions and payments companies have been increasingly exploring stablecoin-powered services for consumers and businesses alike, with new offerings enabling them to hold, send, make payments and earn rewards using stablecoins becoming more commonplace.

Stablecoins, which are currently usually pegged to the US dollar, can offer a range of different benefits that may make them more advantageous than using fiat currencies for individual users and businesses.

For users in countries where the local currency is volatile and can quickly lose value, stablecoins offer an accessible way to hold a more stable currency, such as the US dollar, by proxy, without requiring a possibly complex foreign currency bank account.

For businesses, stablecoins offer the potential to provide a programmable form of money using smart contracts, enabling them to set rules that determine when funds are paid or released based on specific conditions – such as paying suppliers once a shipping company confirms goods have been delivered.

For sending funds cross-border, stablecoins do not require any correspondent banks or other intermediaries before they reach a recipient, reducing the cost of these transfers in some cases. As an added bonus, because these types of transfers are sent via blockchain networks and do not require the involvement of traditional banks, they are not slowed down by operating hours and can be sent ‘instantly’ at any time of the day or week.

In this report, we explore the differences between various stablecoin offerings from cross-border payment companies to hold and send stablecoins alongside fiat, the different end-users they target, potential pain points related to these offerings and planned future developments in the space.

How do stablecoin holding and sending capabilities vary?

While there are currently many offerings enabling users to hold stablecoins in a wallet or account and then send them to others or use them to make payments, these offerings come in a number of forms – with the capabilities and reach of each varying.

Brazil-based Nubank and London-headquartered Revolut are both neobanks that enable users to buy, sell, store and transfer USDC alongside a range of other crypto assets within their apps – with dedicated crypto sections of each app and these assets kept separate from fiat currency accounts. Consumers or small business customers of these neobanks can purchase USDC using selected fiat currencies to keep the value of their savings stable relative to the US dollar without needing access to a traditional US bank account. They may also leverage the stablecoin for international trade, with it potentially offering faster and cheaper settlement than some fiat transfers.

Africa-focused payments technology company Flutterwave also enables merchant customers to hold USDC and USDT within its dashboard – enabling them to accept stablecoin payments from customers. By doing so, it aims to give businesses easier access to always-on cross-border payments. Flutterwave is also among the companies utilising stablecoins to make cross-border transfers cheaper and faster for consumers while giving them the opportunity to hold stablecoins and choose when to convert back to fiat.

“Stablecoins make Flutterwave accounts more reliable, useful and globally connected than a traditional bank account alone,” explains Mercy Emmanuel, Stablecoin and Blockchain Commercial Lead at Flutterwave. “This strategy bridges the gap between traditional fiat and the global digital economy, offering a programmable, stable-value asset that enhances the overall utility of the Flutterwave account.”

Remitly provides a multicurrency wallet compatible with both fiat currencies and stablecoins to members of its Remitly One programme, giving them a way to hold USD and USDC in one place. This specifically aims to give consumers living in areas where the local economy and currency are volatile a way to protect the value of their holdings. This offering is currently only available by invite, with plans to expand access in the future.

Similarly, Zepz’s Sendwave wallet enables users based in the US to send funds to 30+ countries worldwide, which recipients receive in USDC. They are then able to store the stablecoins in the wallet and choose when they want to withdraw the money, converting it to a local currency. Withdrawals are not possible for Sendwave wallet users in the US, highlighting that the main use case is for sending remittances. Through this offering, Zepz aims to ensure that users can easily use this money for everyday spending and that it holds its value over time.

“This is particularly relevant for customers across the Global South, where currency volatility and limited access to the global financial system make it harder to hold value, access stronger currencies and plan for the future,” explains George Goodyer, CTO at Zepz. “We’re starting to see early changes in how customers use the product. Beyond sending money, they are beginning to hold balances and use the wallet more actively within their networks. It’s still early, but it points to a broader shift from one-off remittances to something more flexible that better reflects how people actually manage money across borders.”

MoneyGram also enables users in Colombia and El Salvador to hold USDC within its app, enabling consumers to store their value until they decide to use it and convert back to local currencies. Via a partnership with blockchain network Stellar, the money transfer giant offers cash-to-USDC on and off-ramps at participating MoneyGram locations. This aims to give participants of the informal economy without access to bank accounts a way to retain easy access to cash while protecting themselves from market volatility.

Which currencies and rewards do commercial stablecoin offerings support?

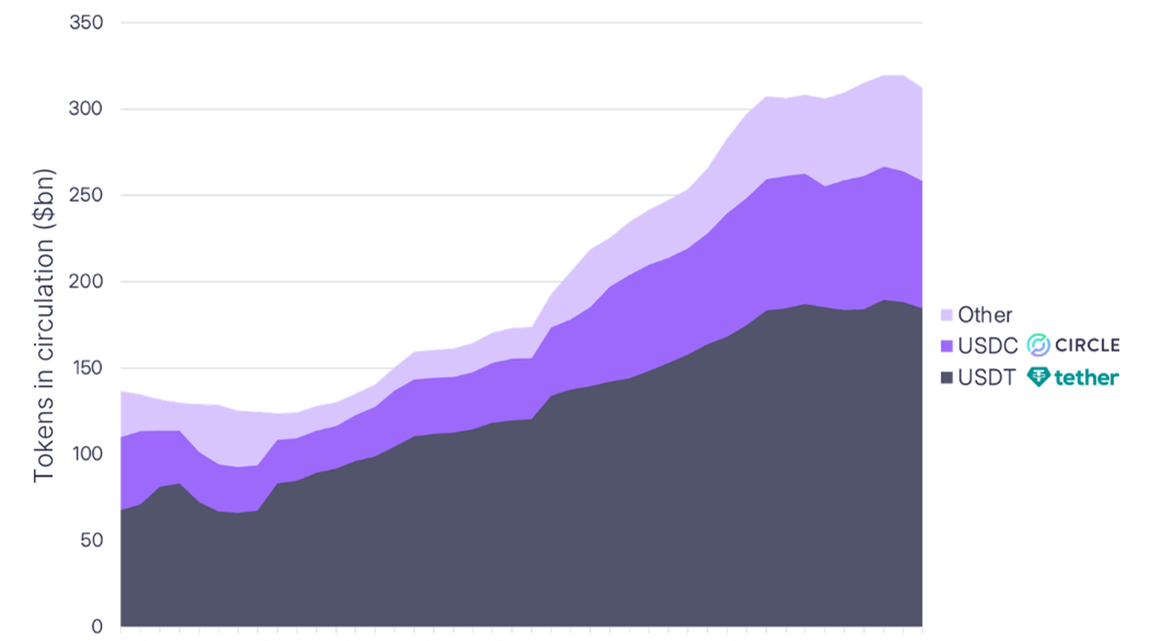

Currently, the majority of these offerings only leverage stablecoins pegged to the US dollar, with USDC the most supported of the companies we selected, with USDT second.

Of the stablecoin-compatible wallets and accounts we looked at, MoneyGram, Nubank, Remitly and Zepz only leverage USDC, while Flutterwave, Revolut and Bitso Business support both USDC and USDT. Revolut also enables users to buy Ripple’s RLUSD.

“Holding USDC and USDT provides users with significant financial flexibility, allowing them to manage fiat and stablecoin liquidity within a single, unified environment,” says Emmanuel. “This integration facilitates near-instant settlement – shifting transaction times from days to seconds – which improves cash flow and capital access. Furthermore, users benefit from reduced intermediary fees and the ability to embed automated, programmable treasury strategies directly into their payment flows.”

The majority of stablecoins in circulation continue to be made up of USDT and USDC, although USDC’s regularly audited USD reserves in cash and cash equivalents mean it is aligned with the GENIUS Act, which outlines requirements for stablecoins in the US. USDT, which has bitcoin reserves alongside other less typical forms of backing, is not compliant – resulting in more US-based companies choosing to leverage USDC.

“Before introducing any stablecoin to our customers, we carried out extensive due diligence, particularly around reserve management and potential risks,” adds Zepz’s Goodyer. “Our priority was simple: if we were going to offer this, it had to be redeemable 1:1 for US dollars and meet a very high bar for safety, transparency and reliability.”

Other companies have also chosen to launch their own stablecoins pegged to the US dollar. PayPal launched PYUSD in 2023 and now enables businesses to pay suppliers and service providers across borders using the stablecoin 24/7. It also gives businesses the option to pay freelancers directly in PYUSD, avoiding currency conversions and exchanges, while giving individuals a way to send PYUSD to eligible wallets and accounts globally and ensuring recipients can avoid local currency depreciation.

Mercado Pago, the financial services platform developed by online marketplace Mercado Libre, also issues its own stablecoin – the Meli Dollar (MUSD). This asset is currently available in Brazil, Mexico and Chile and can be bought using the local currency of each country. Users can use their MUSD balances to fund or partially fund purchases made on the Mercado Libre marketplaces or at a range of selected partners.

Some of these companies also offer selected benefits to consumers and businesses on stablecoin balances and spending. Bitso Business, Coinbase, Nubank, PayPal and Remitly are among the companies that offer some form of reward return on stablecoin holdings, generally ranging between 3% and 4% per year.

Meanwhile, Mercado Libre’s subscription loyalty programme Meli+ gives members cashback on all purchases – whether they use MUSD or fiat currency to pay. All cashback is paid in MUSD and stored on its platform.

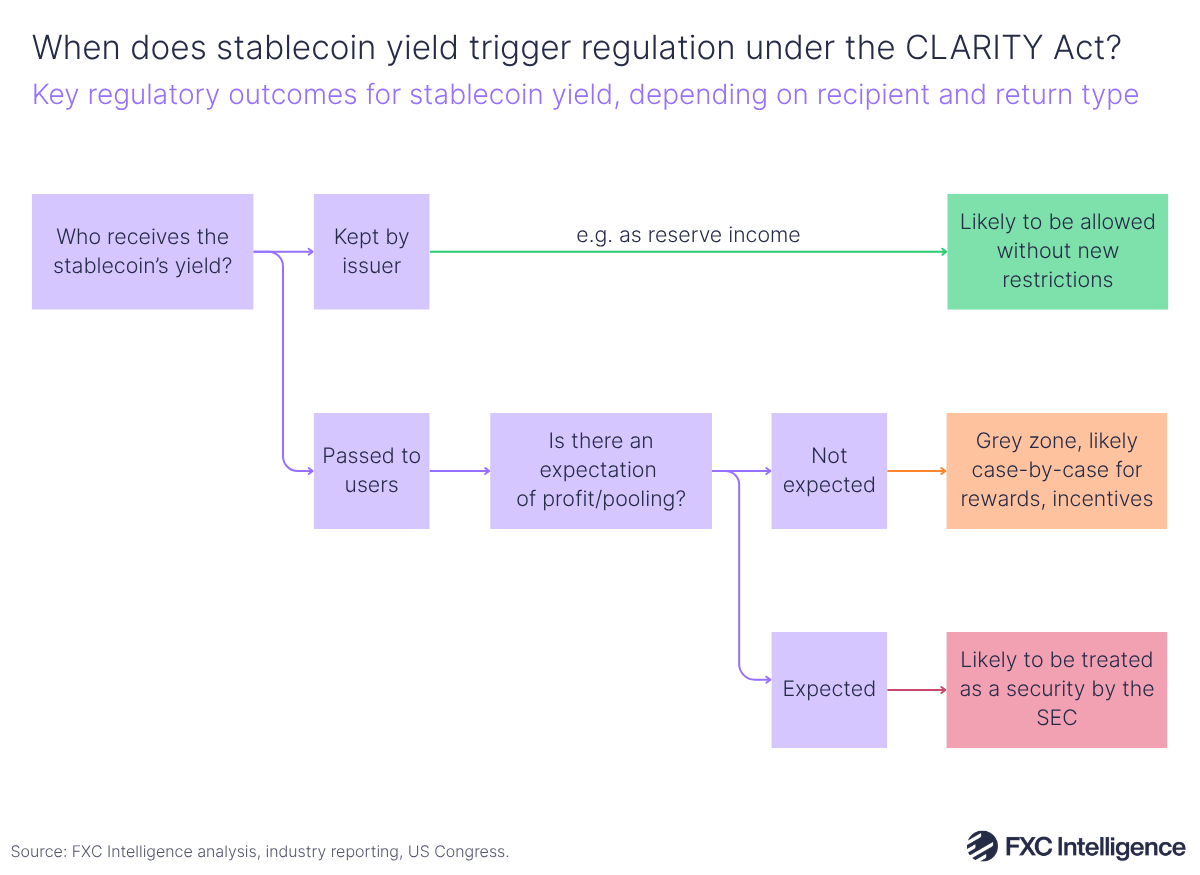

The Digital Asset Market Clarity Act (CLARITY Act) in the US continues to move through US Congress and one area of focus has been how it could impact rules around stablecoin yield. Current proposals suggest that any yield or rewards paid out for holding stablecoin balances could be restricted. If passed, this could result in rewards pivoting to be tied to activity-based actions, such as making payments with or trading stablecoins.

As it stands, stablecoin issuers are not allowed to pay yield to holders, as per the GENIUS Act, but the CLARITY Act could take this further and stop other distributors or rewards programmes from sharing earnings related to stablecoins – something many banks are pushing for.

What’s next for commercial stablecoin accounts and wallets?

Aside from regulatory uncertainty and the potential for new rules to come into play that place restrictions on how stablecoins are used for these companies, there are also technical barriers for companies aiming to implement stablecoin-powered offerings to their portfolios.

According to Zepz’s Goodyer, working with a new layer of technology presented one of the biggest challenges when moving into stablecoins and blockchain, given the need to ensure it had the right expertise and technology in place.

“At the same time, we had to make sure that none of that complexity showed up for our customers,” he explains. “We don’t build for people who want to navigate crypto systems; we build for people who want something simple, reliable and easy to use. So a big part of the work was making sure the experience feels familiar, even if what sits behind it is quite different.”

According to Flutterwave’s Emmanuel, integrating stablecoin capabilities into its offerings also created challenges. “The integration involved significant technical and operational hurdles, particularly in building secure fiat-to-crypto bridges and ensuring real-time visibility for CX teams into fund movements,” she adds. “Teams faced early challenges with transaction reliability, including inconsistent fee displays, ambiguous transaction minimums and the requirement for reliable transaction hash tracking. Furthermore, the company navigated a complex regulatory landscape balancing the necessity of VASP licensing and strict KYC/AML compliance with the requirement for a seamless, user-friendly experience.”

Now, an increasing number of companies appear to be getting closer to launching fully fledged stablecoin-powered offerings that enable users to operate as if they were fiat. Although many of these companies have established ways for consumers and businesses to hold balances in stablecoins and earn rewards from these holdings, the ability to use them for real-world payments is currently less widespread.

However, there are already signs that more of these capabilities are not far away. Zepz has outlined plans to gradually roll out stablecoin-linked Visa cards across various markets, starting in Brazil, enabling users to use their stablecoin balances for everyday purchases anywhere Visa is accepted. Similarly, Nubank is reportedly exploring how it could link stablecoins to credit cards to enable their usage for payments.

Other companies are planning to bolster the capabilities of their existing stablecoin offerings in other ways. PayPal, which already enables users to send PYUSD to compatible wallets and accounts globally, has plans to further expand its influence beyond the 70 markets where users are currently able to buy, hold, send and receive the stablecoin – gradually adding more over time.

Flutterwave currently only enables clients to fund their stablecoin balances using supported fiat currencies and external wallet addresses. However, it does appear to have plans to eventually enable them to receive settlements in stablecoins and has labelled this feature as ‘coming soon’.

As stablecoin-powered account and wallet offerings become more accessible, it seems likely that more companies will begin to explore how they can enable customers to make payments using stablecoin balances. Companies will also continue to build out the range of related capabilities they offer, which could bring different options into closer alignment with one another – although imminent CLARITY Act developments could impact how these evolve.