Tether, the company behind the stablecoin market leader USDT, has announced plans for USAT, a US-based and GENIUS Act-compliant stablecoin. But how does it play into the company’s strategy, and how might it challenge Circle’s USDC?

Last week, Tether, the El Salvador-headquartered issuer of the world’s biggest stablecoin, USDT, announced that it was launching an entirely new stablecoin specifically for the US market: USAT.

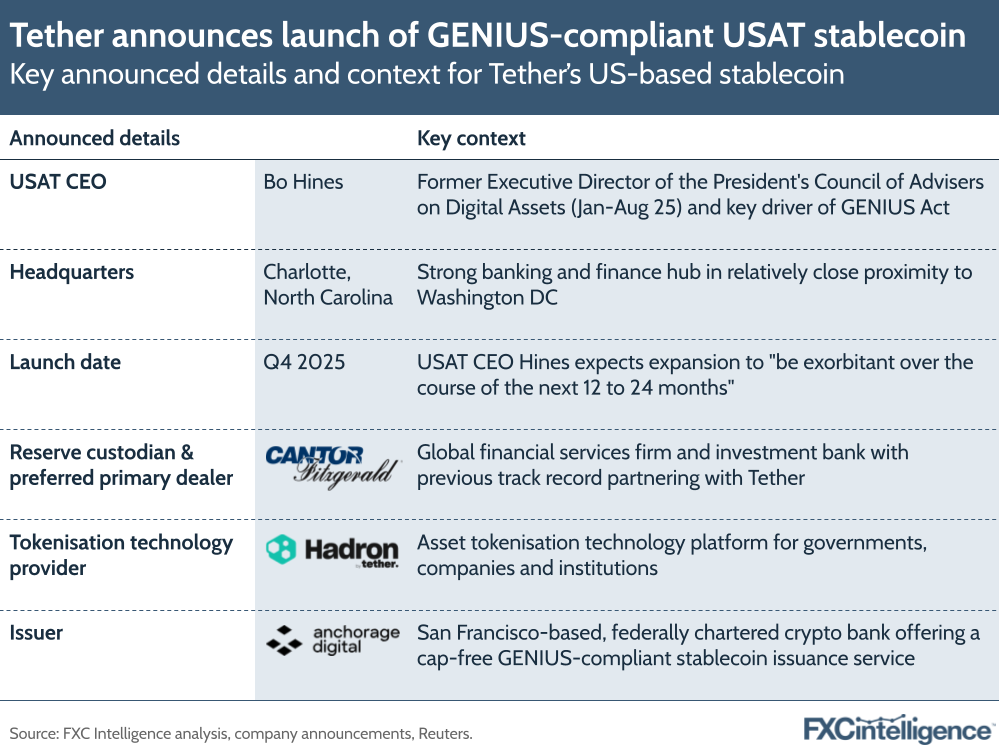

Designed to comply with the recently-passed GENIUS Act, which regulates stablecoin issuance and activity in the US, the stablecoin will be entirely managed and operated from within the country. This includes leadership, with the company announcing the appointment of Bo Hines, former Executive Director of the President’s Council of Advisers on Digital Assets, as USAT CEO.

The move comes as Circle’s USDC has seen growing adoption within the payments industry, while an increased number of other stablecoins are either being launched or seeing growing use, particularly within the US following the passing of the GENIUS Act. For many in the industry, the bill has provided a long-requested regulatory framework for stablecoin development and operation within the US, and has prompted a rush of adoption – particularly among many traditional fintech players.

With this in mind, how have the market conditions driven Tether to launch USAT, and how might it challenge players such as Circle? We explore these questions and more in this report.

USDT’s market position

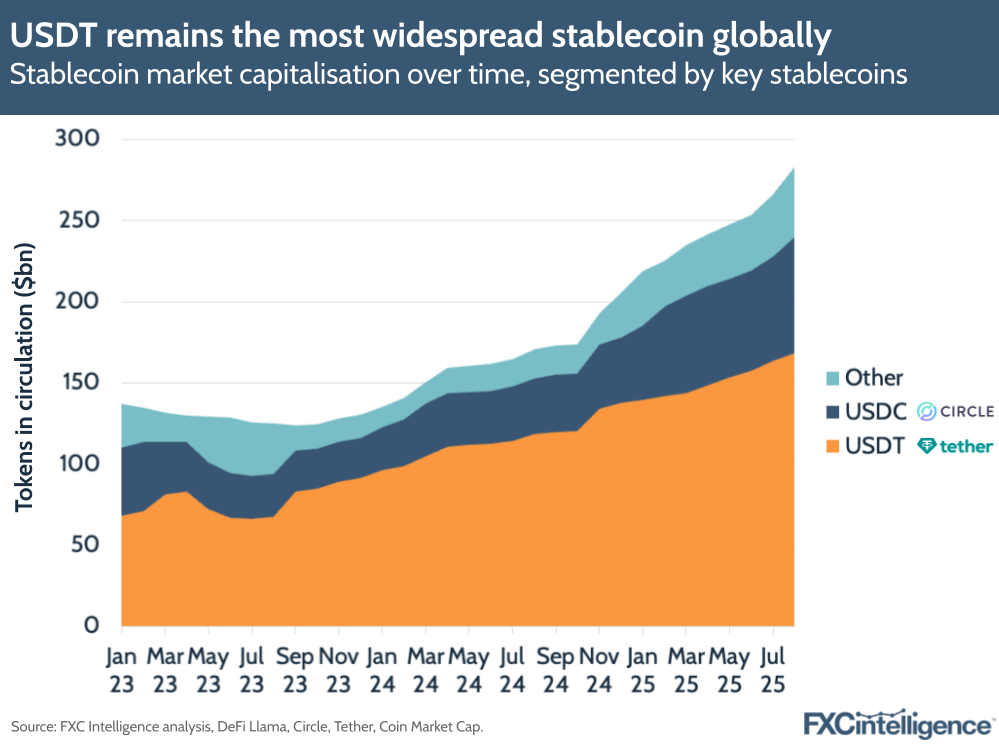

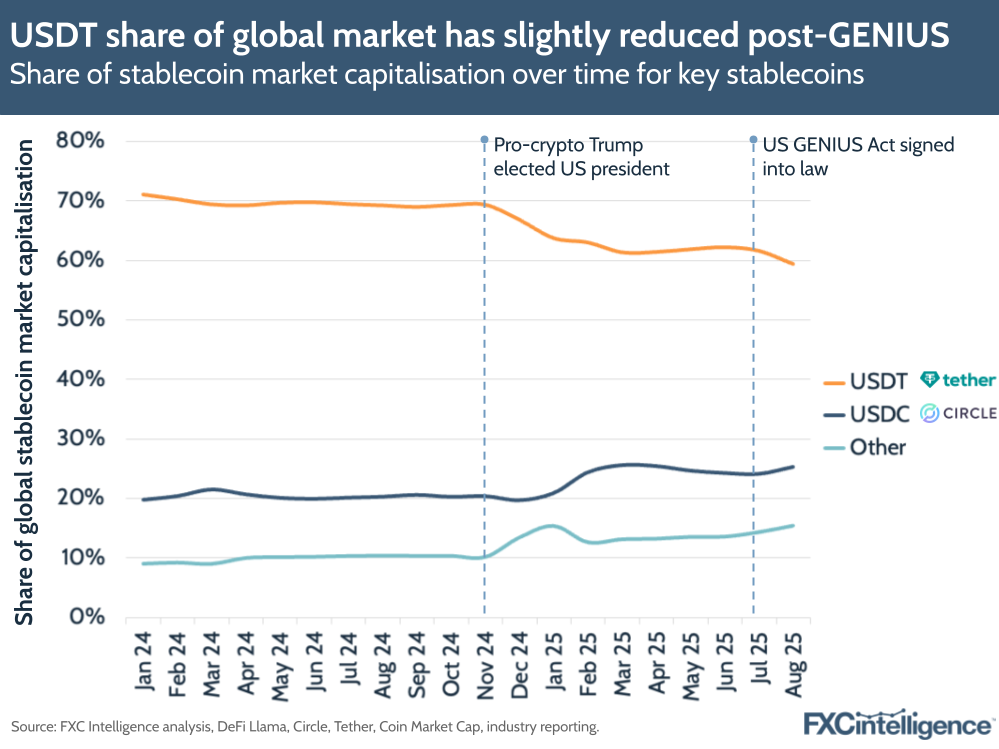

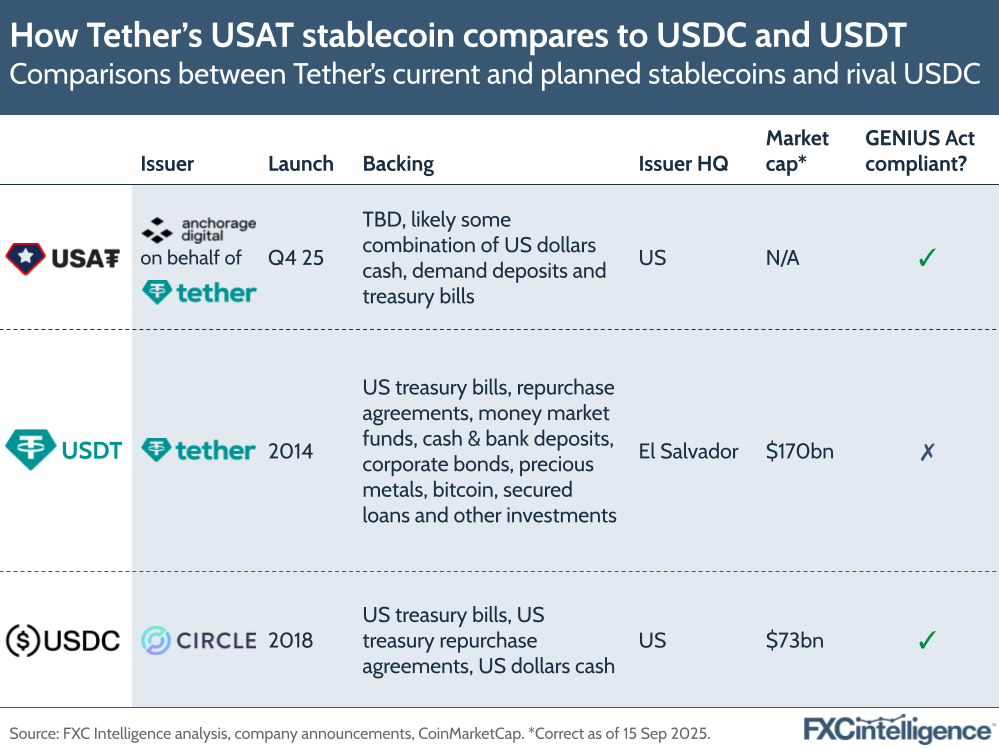

Having gained popularity among crypto investors as well as many in emerging markets looking for a proxy to the US dollar, USDT is unquestionably the global stablecoin market leader. At the end of August 2025, it accounted for around 59% of all stablecoins in circulation globally, with a market capitalisation of $168bn. As of 15 September, that number had passed $170bn.

It has also seen consistent double-digit growth in recent years, typically by around 30-50%. In August, for example, it saw its cap climb by 42% year-on-year.

By contrast, while Circle’s USDC also has a significant share of the global market cap, it remains less than half of Tether’s. At the end of August, this stood at $72bn; a 25% share.The sheer scale of USDT means it offers immense liquidity for those looking to enact high-value payments. Although it is not favoured by many players in the cross-border payments space, some companies who provide high-value cross-border payments to or from emerging markets using stablecoins, such as Orbital, report needing to use USDT to support this on certain corridors.

The impact of the GENIUS Act

USDT had already been treated with greater caution by many Western financial players than its US-based competitor USDC due to differences in transparency, headquarters and reserve backing, however, the passing of the GENIUS Act in July has had a more pronounced impact on the use of USDT.

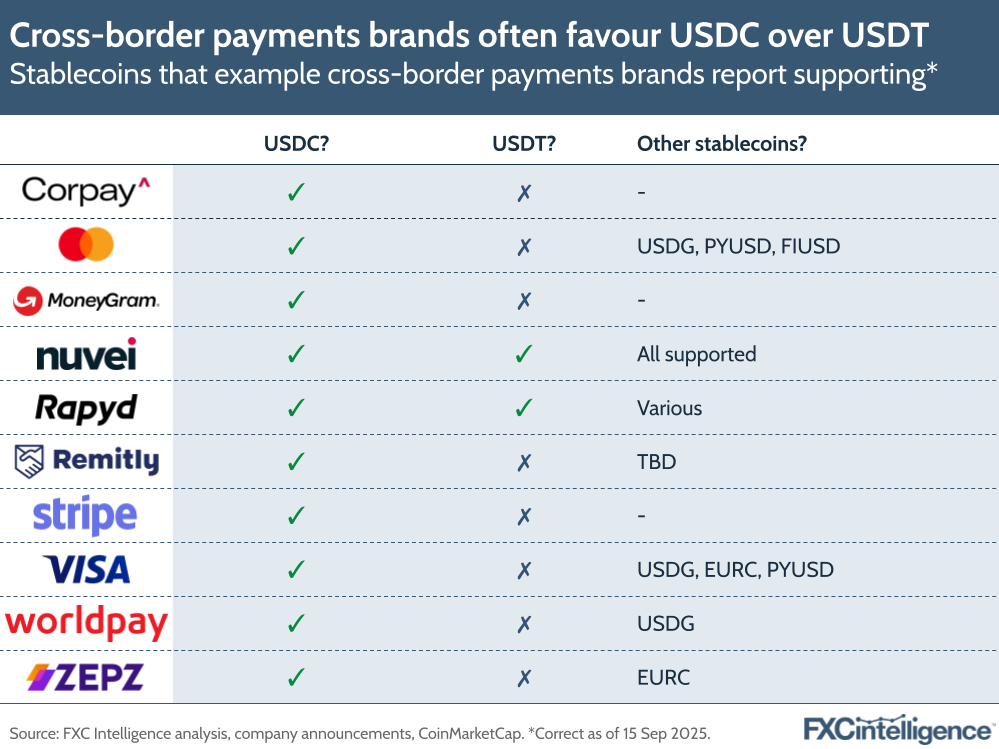

While many players have had some form of stablecoin offering for some time, the number of cross-border payments companies announcing stablecoin-based solutions and products has risen dramatically since the passing of the act and for the majority, USDC has been the primary stablecoin involved.

Remitly, MoneyGram and Stripe are among those who currently only state USDC as a supported stablecoin, while among those that do support USDT, it is typically part of a wider grouping, such as with Nuvei, which supports all stablecoins as part of its settlements solution.

Meanwhile, Mastercard and Visa have both expanded support for stablecoins recently, however in both cases this has excluded USDT in favour of stablecoins that more fully comply with the GENIUS Act.

This is beginning to have a modest but noticeable impact on Tether’s share of the overall stablecoin market. While it has seen USDT’s market capitalisation continue to grow, it has done so at a slower rate than the market overall, resulting in a gradual loss of share. Having consistently maintained around a 70% share of the overall market between November 2023 and November 2024, USDT saw its share begin to lightly reduce from last November when Donald Trump, who was vocally supportive of the crypto industry during his campaign, was elected.

However, since the passing of the GENIUS Act in July, its share has begun to drop at a slightly faster rate: going below 60% in August, the first time it had done so in two years. As of mid September, it has continued to contract, with its share down a further half-percentage point.

Notably, however, not all of this share has shifted to USDC. While Circle’s stablecoin has seen its share grow from 20% in November 2024 to 25% in August 2025, the share held by other stablecoins has also climbed from 10% to 15%.

In terms of total market capitalisation, both are also seeing pronounced growth, with USDC seeing 107% YoY change for August, while other stablecoins saw 146% growth.

USDT compliance challenges

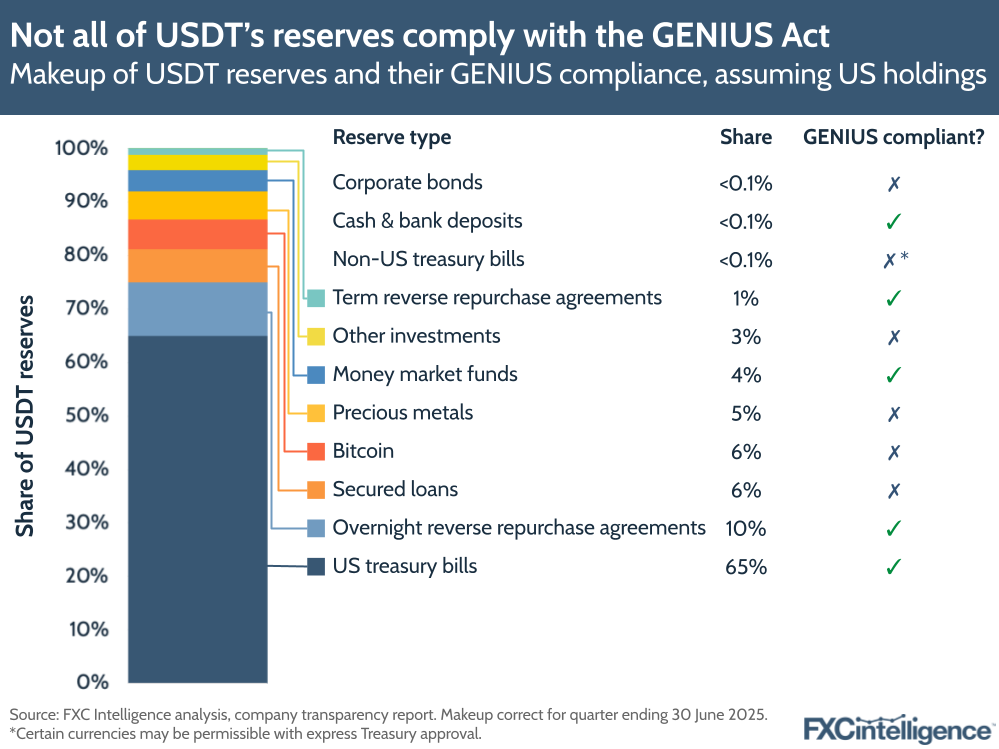

A significant contributor to this is that USDT is at odds with the compliance requirements of the GENIUS Act on a number of points. While the stablecoin is reserve-backed and regularly publishes attestations of its reserves, it falls foul of the regulations on a number of points.

These largely centre around the stablecoin’s reserves. While around 80% of its holdings are in types of assets that are, at least in principal, compliant with the act’s requirements, the rest are either in assets that would only be compliant with specific approval from the Treasury or, in the case of those such as bitcoin and precious metals, completely forbidden as a form of reserve for a GENIUS-compliant stablecoin.

The location of the reserves is also in question. Tether, which until recently was headquartered in the British Virgin Islands before it relocated to El Salvador, does not explicitly disclose where its holdings are located, however they are unlikely to be fully held in the US, which is typically required of GENIUS-compliant stablecoins.

There is also the question of Tether’s auditing of its reserves. The act requires fully, timely audits of all reserves, and while the company does publish quarterly attestations, it has not completed a fully compliant audit by a major firm or equivalent in a manner that is significantly exhaustive to satisfy the Act.

There are also some questions around some of the legal guarantees under US law, particularly those relating to priority rights in the event of insolvency – something that Tether does not look in any way at risk of facing at present, but it would need to prove to be compliant with GENIUS.

While the law favours US-based stablecoin issuers, there is a pathway for foreign issuers to be approved under the law and Tether has publicly committed on several occasions to meet this – something that CEO Paolo Ardoino has said the company has three years to achieve, and which he restated in a press conference announcing the launch of USAT.

However, this is likely to require significant operational overhaul for Tether and in the meantime USAT presents a more immediate solution.

USAT: Tether’s stablecoin for the US market

From its all-American branding to its structural and operational set-up, USAT is a stablecoin expressly designed for the US market. And much of this is in service of GENIUS Act compliance.

Rather than create an issuing entity in the US, Tether has employed Anchorage Digital, a crypto bank that offers a host of Web3-related services, including a stablecoin issuance service. Designed to fully comply with GENIUS at a federal level, meaning it supports the issuance of stablecoins without the state-level cap of $10bn, Anchorage supports the deployment of stablecoins across multiple blockchain platforms, meaning that like USDT and its wider competitors, USAT will be able to be deployed for a variety of use cases.

From a reserve perspective, this means it is likely to be backed by an asset mix much closer to USDC than USDT, and Tether has also brought in a third party to handle the compliant custody of its reserves, in the form of global financial services player Cantor Fitzgerald.

However, Tether will also be harnessing its own stablecoin expertise in the form of its tokenisation technology platform Hadron, which allows organisations, including governments and companies, to tokenise digital and real-world assets. It is likely this is one of the few areas it can immediately handle with GENIUS compliance without needing to gain additional time-consuming regulatory approvals, yet it also serves as something of a marketing tool for Hadron – particularly in the US where it has a strong potential market given the flurry of current activity around stablecoins.

Beyond the infrastructure, Tether’s appointment of Bo Hines, former Executive Director of the President’s Council of Advisers on Digital Assets and a key player in delivering the GENIUS Act’s passing, also speaks to a strong desire to make USAT a part of the US’s stablecoin establishment, rather than USDT, which can be regarded as a foreign outsider.

This is likely to be a critical motive for launching USAT, along with the timeframe. While Tether plans to ultimately make the changes to have USDT accepted as a foreign issuer under GENIUS, this is a multi-year project, and even if Tether achieves complete acceptance of USDT in the US market once it is completed, it will have lost significant momentum to USDC and others in the preceding years.By contrast, USAT’s immediate compliance and all-American styling looks designed to not only encourage acceptance by US brands, but to give Tether a challenger that can compete for this fast-growing market almost immediately. While the company has said that USAT will launch by the end of the year, Hines said in a press conference that he expected the stablecoin’s expansion to “be exorbitant over the course of the next 12 to 24 months”.

Tether’s geopolitical significance

The move comes at a time when Tether otherwise risks seeing its dominance in the stablecoin landscape slowly deplete, as the US becomes a central focus for ongoing development. Likely in recognition of USDC’s strength in this market versus its own, overall Tether CEO Ardoino said that the company had been facing “severe pressure from competitors that want to create a monopolistic environment in the United States”.

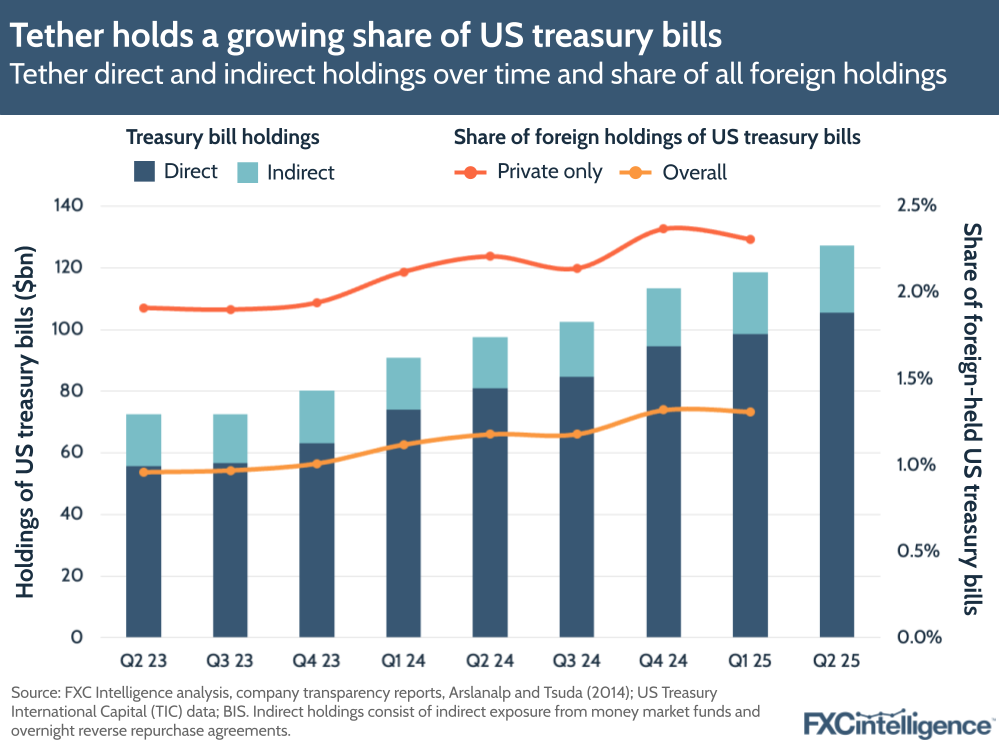

With such a large market cap for USDT, Tether is already an important global player in terms of its holdings of US treasury bills. At the end of Q2 2025, the company reported having $127.3bn in direct and indirect holdings of US treasury bills, $105.5bn of which it held directly, and the numbers are likely to be higher today.

This makes it one of the largest holders of US treasury bills globally – a fact that the company pointed out in its own press release for USAT, with Ardoino quoted as saying this was due to the company believing “deeply in the enduring power of the dollar”.

As of Q1 2025, the most recent period where full Treasury data is available, Tether’s direct and indirect treasury bill holdings accounted for 2.3% of the entire private foreign holdings of US treasury bills globally, and 1.3% of private and government foreign holdings combined.

Such holdings give Tether some notable geopolitical clout, and it is now turning this on the US market through its launch of USAT.

“USAT is our commitment to ensuring that the dollar not only remains dominant in the digital age, but thrives – through products that are more transparent, more resilient, more accessible and more unstoppable than ever before,” said Ardoino in the press release.

Hines’ role in particular is critical to delivering this, with the incoming Tether USAT CEO saying the stablecoin was “designed to strengthen America’s role in the global economy”, a sentiment he built on in the press conference.

“We want people to know that Tether is here to participate in the US economy in a huge way.”