The proposed Digital Asset Market Clarity Act of 2025, largely referred to as the CLARITY Act, has been drawing considerable attention as it moves through US Congress, particularly around its potential impact for stablecoins. However, some of the reaction from retail investors, particularly related to issuer Circle’s share price dive, suggests a lack of understanding of the nuances of the bill. We take a look at how the proposed legislation could genuinely impact the stablecoin payments industry.

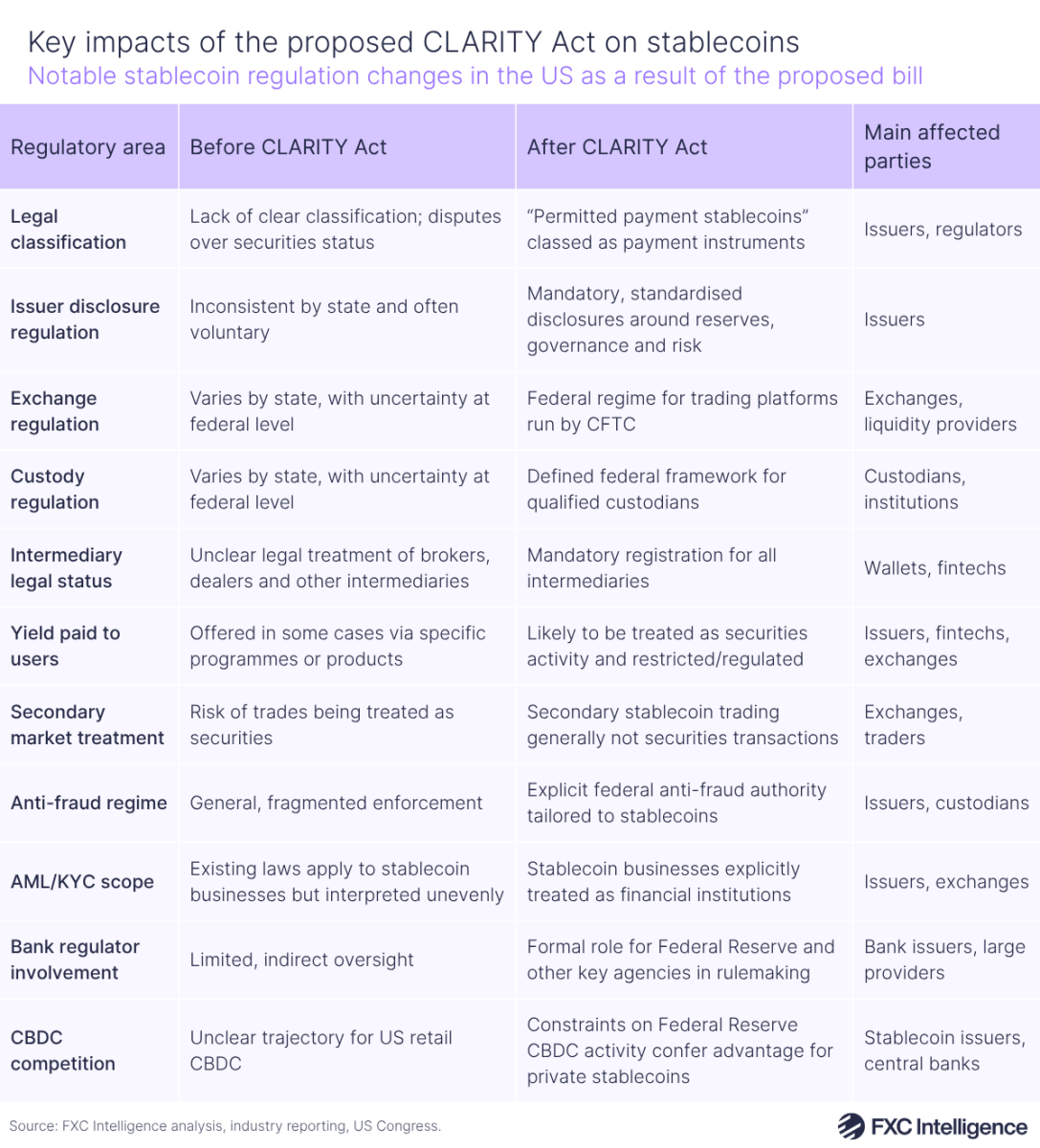

The CLARITY Act is an in-progress bill within the US that concerns digital assets; so far it has passed in the House and is now undergoing review in the Senate. While parts of it complement the stablecoin-focused GENIUS Act, which was passed into law in July last year, the CLARITY Act has a far broader scope. Focusing on all forms of digital currency, particularly those relating to trading and investment, it places a particular emphasis on increasing regulatory oversight of the space as a whole. As a result, not all aspects of the bill are relevant to the stablecoin industry, although there are several areas where the bill would, if passed, create notable changes for the industry.

Firstly, the bill legally separates fiat-backed stablecoins from other forms of digital assets, putting an end to questions over whether they are a security and clarifying specific oversight for “permitted payment stablecoins” that differs from other types of blockchain-based tokens. This will also see increased requirements around reserve disclosures and governance, including making these at a consistent federal level – presently, disclosure rules can vary depending on the state a company operates in.

There is similarly increased regulatory oversight surrounding both custody and payments intermediaries, with the latter needing to be registered rather than existing in the current grey area. There is also clarity around secondary market trading to prevent the act of purchasing stablecoins on exchanges or from liquidity providers being treated as securities trading, while bank regulators also now have a formal role in rulemaking and enforcement.

Other elements move anti-fraud, AML and KYC activities from being subject to a patchwork of regulatory entities to being treated more directly and explicitly, including with an explicit anti-fraud authority to target activities such as the misrepresentation of either reserves or means of redeeming a stablecoin.

Notably, the bill would also bolster stablecoins over central bank digital currencies (CBDCs) by prohibiting the issuance of retail CBDCs by Federal Reserve banks.

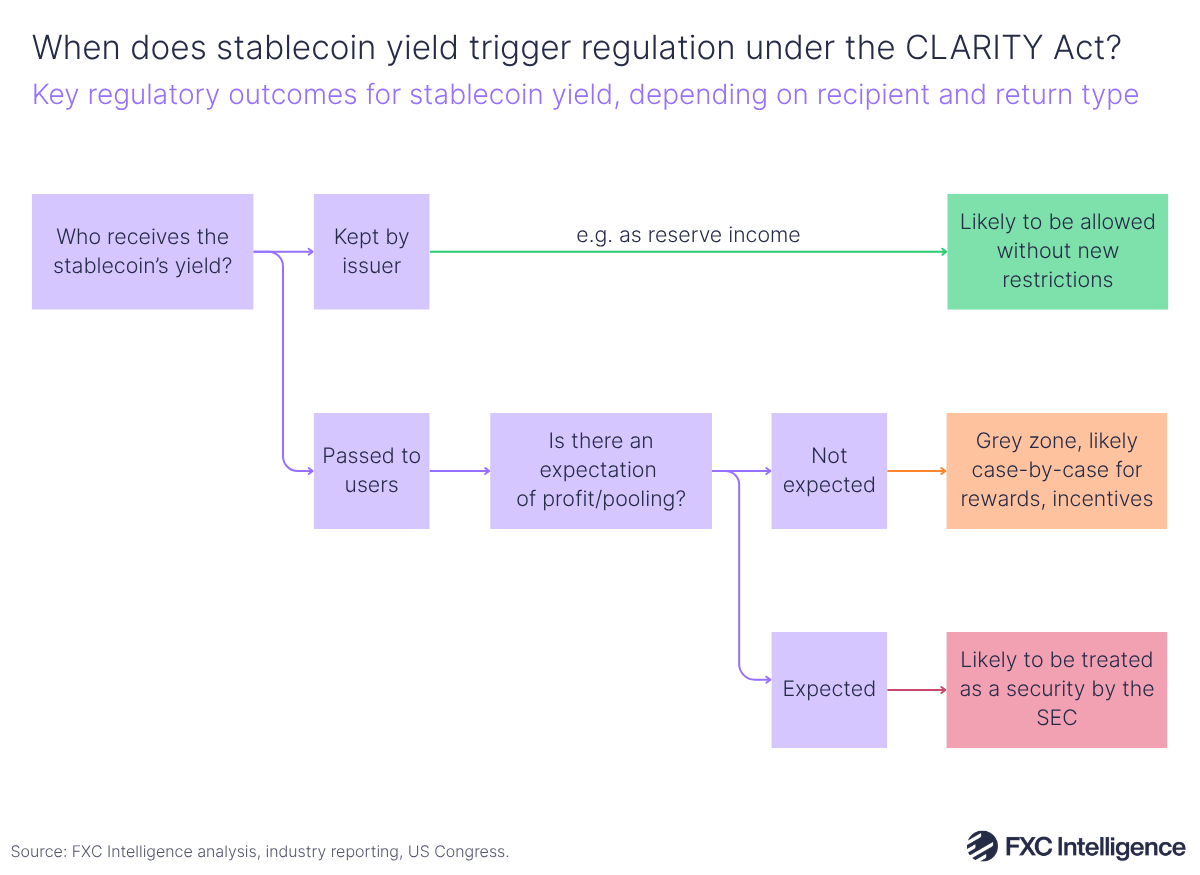

One area that has drawn particular attention, however, is the impact on stablecoin yields, which are treated differently from other areas in the stablecoin-focused legislation due to their ability to shift the status of stablecoins from payment instrument to security.

While the bill focuses on payments applications for stablecoins, there is no specific authorisation or defining of a regime for paying interest or yield on stablecoins. Instead, while the bill does not lay this out in a single clause, it is thought that in some cases it would trigger the treatment of a stablecoin as a security, making it subject to different, more stringent regulatory oversight.

The lack of explicit focus on this area had led some to believe that this would impact the practice of earning income on a stablecoin’s reserves – the primary form of revenue for USDC issuer Circle. However, this is unlikely to be the case. Instead, it currently appears that it is only stablecoin products that pass on yields to their users, and in this case it is thought that framing these as rewards or incentives may limit the additional impact – something that many cross-border payments players already do.

While the bill is still in development it may change, and there are likely to be clarifications provided if it does come into law. However, at present this bill’s primary impact for the stablecoin payments industry is likely to provide greater regulatory clarity.