dLocal saw record volumes and solid cross-border growth across its regions and verticals in Q1 26, though rising expenses hit the company’s profits. This report explores the company’s Q1 drivers and future strategy, including its approach to stablecoins.

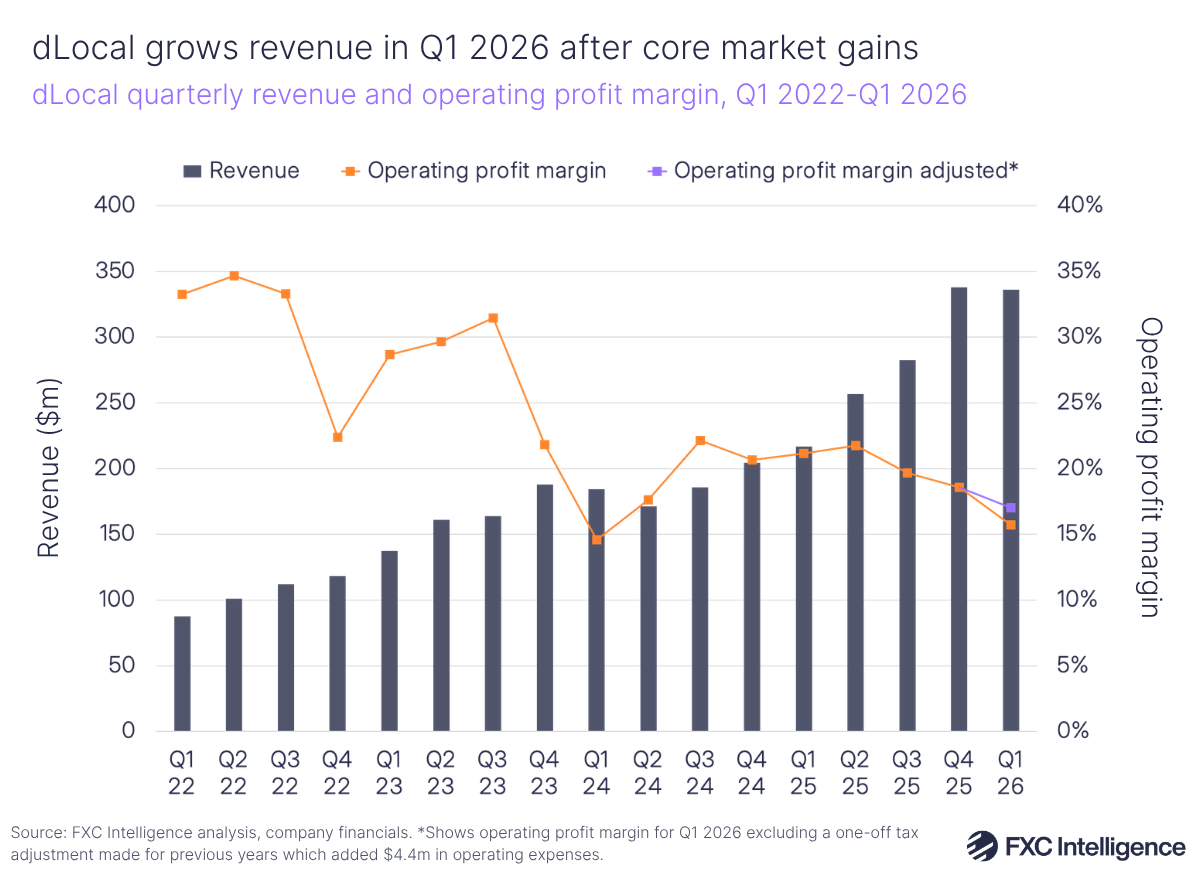

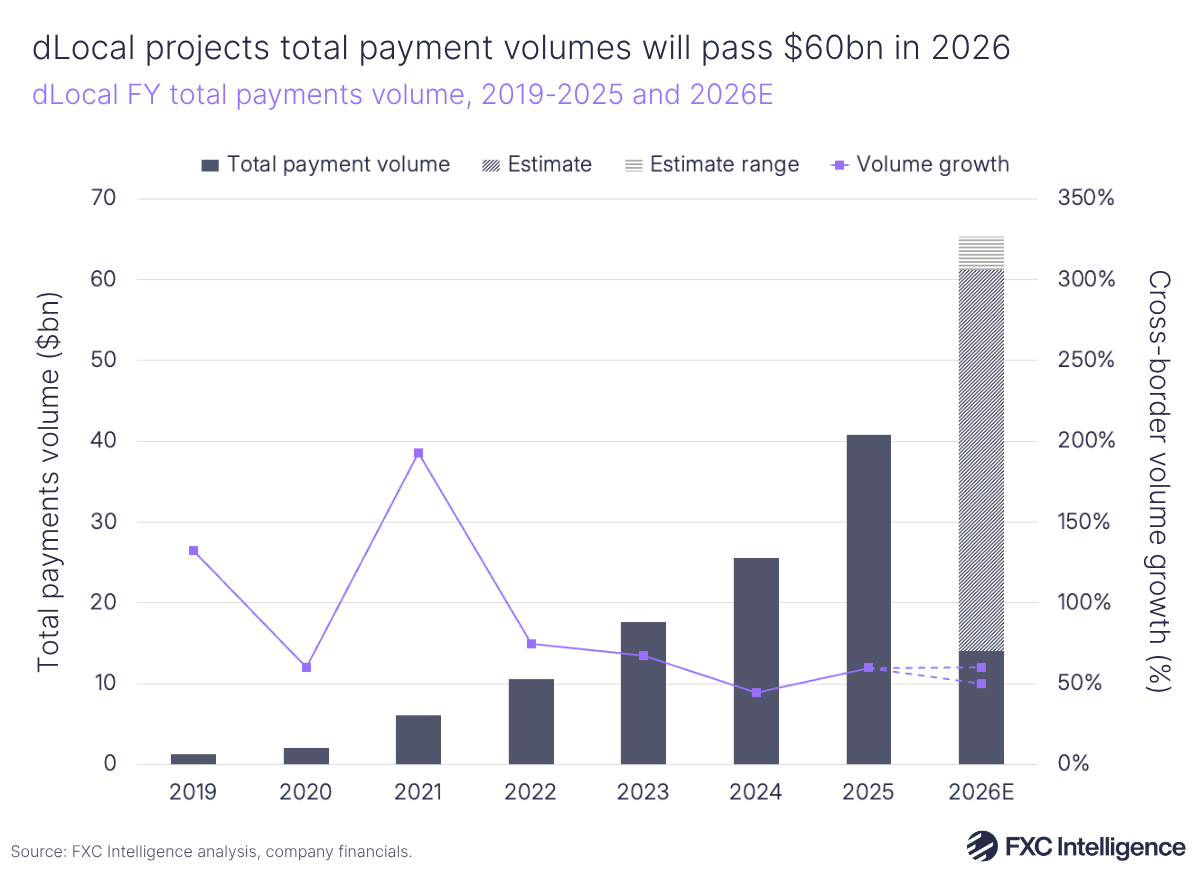

Uruguay-based processor dLocal reported strong results in Q1 2026, with revenues growing 55% YoY to $336m on the back of volumes rising 73% to $14.1bn – a record for the company.

dLocal also broke its record for gross profit, with this rising by 40% YoY to $119m, giving a margin of 35%. However, a tax adjustment for previous years and growing operating costs affected the company’s operating profit and net income, with the former growing at a slower rate compared to Q1 2025 while the latter declined by 10% YoY. This led to dLocal’s share price declining after the company announced its results.

Marking its tenth year in business, dLocal has remained strongly focused on emerging markets but continues to diversify, building a broader base across Latin America while expanding into Africa and Asia. It now operates in 60+ markets, supporting over 1,000 payment methods and serving more than 760 enterprise merchants.

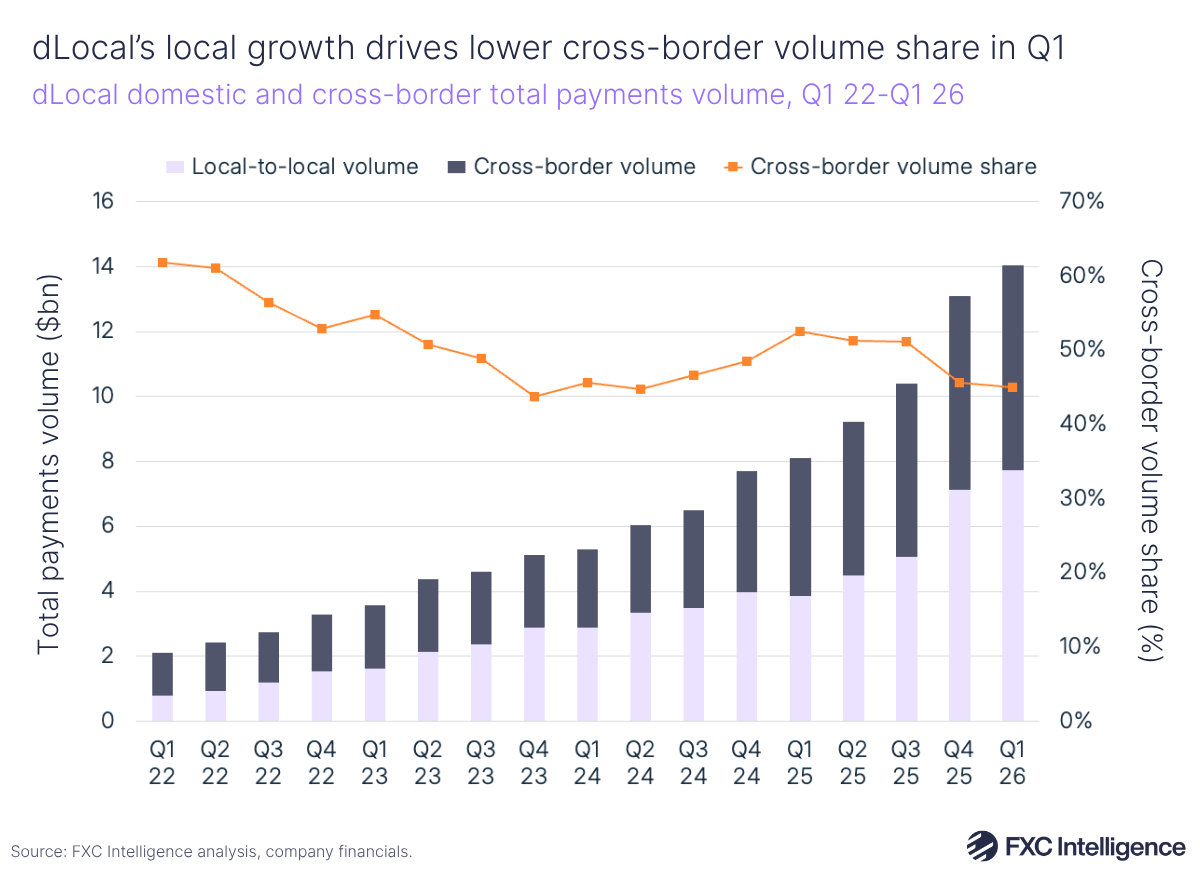

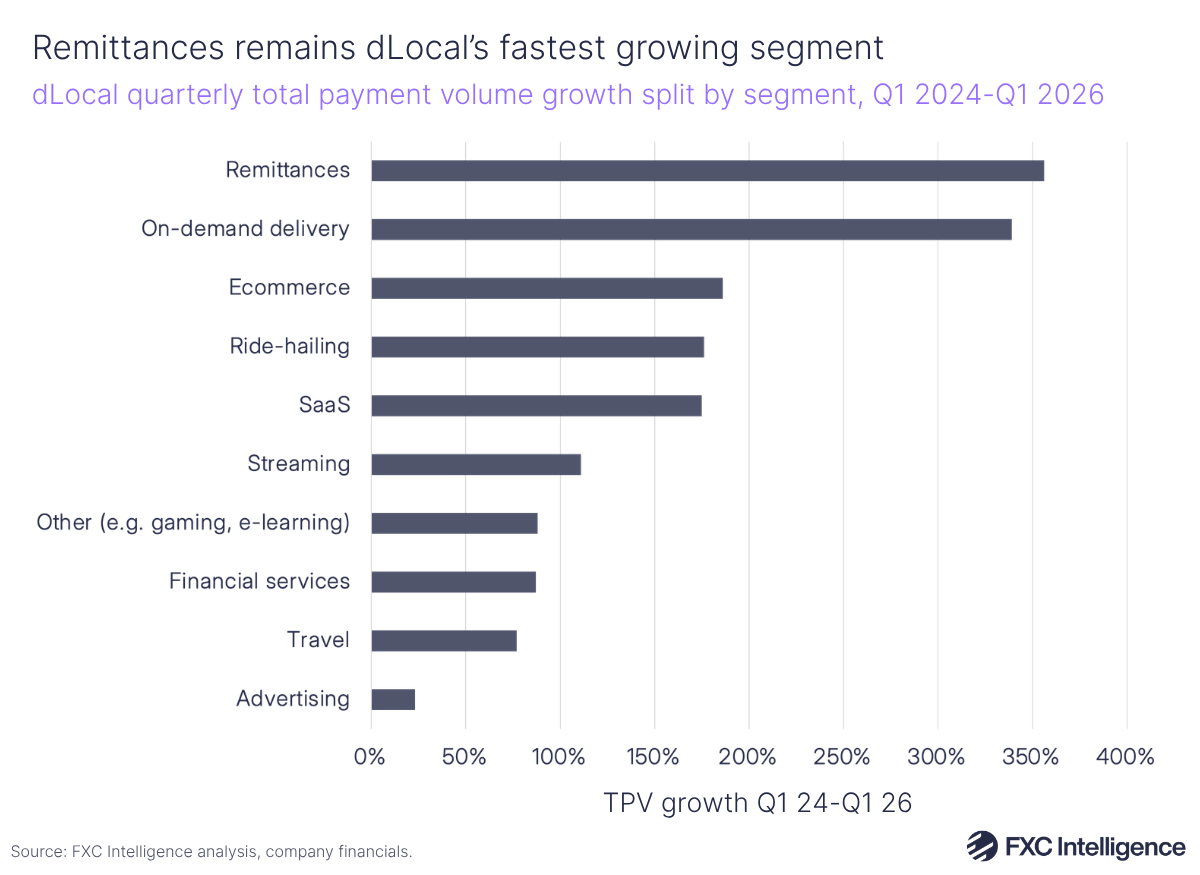

This diversification strategy applies to its different verticals too, with the company noting significant gains over the last few years across its core segments in ecommerce and financial services, though remittances has been its strongest growth vertical, having seen volume growth of 339% in Q1 2026 versus Q1 2024 (based on the company’s two-year comparison outlined in its earnings). Cross-border volumes grew significantly for dLocal in Q1, though strong growth in pay-ins and local-to-local volumes has seen cross-border take a lower share in dLocal’s overall TPV.

During its earnings call, dLocal explained how core trends were driving and impacting growth across its core regions, as well as how new technologies such as stablecoins and agentic AI fit into its wider strategy to target local payments enablement as its customers increasingly make infrastructure a key aspect of their go-to-market strategy.

dLocal’s key revenue drivers and profit metric refocus in Q1

dLocal revenue grew 55% YoY to $336m in Q1 26, driven by a 73% YoY rise in total payment volume (TPV) through its platform to a record $14bn. This was the fastest quarterly volume growth the company has seen since Q2 2023, and also marks its sixth consecutive quarter of 50%+ growth.

The company also noted record gross profit, with this rising 40% YoY to $119m. As of this quarter, dLocal has moved away from reporting adjusted EBITDA as its key profit metric and is now focused on operating profit, as it sees this as a more comparable measure to the operations of other companies in the industry.

Operating profit grew 15% to $52.7m during the quarter, including a one-off tax adjustment made for the fiscal years of 2023-2025. Calculated against the company’s revenue for Q1, dLocal’s operating margin was 15.7%. Excluding the tax adjustment, operating profit grew by 17% to $57m, which would give a margin of 17%.

Overall, operating profit rose at a slower rate compared to Q1 2025 and declined vs Q4 2025, which the company linked to operating expenses being carried over from H2 2025 into Q1 2026, driving a 58% rise in opex overall.

Based on the company’s previous methodology for calculating adjusted EBITDA, this metric would have been approximately $72m including the adjustment, a rise of 25% YoY versus Q1 2025.

Rising payment volumes are driving the business to keep its full-year guidance unchanged. dLocal expects total payment volumes at the upper end of its guidance for 2026, which was 50-60% YoY growth (equating to $61bn-65bn), with gross profit rising by 22.5-27.5% ($493m-514m). Operating profit is expected to grow to around the midpoint of a 27.5-32.5% range ($280m-291m).

dLocal’s local volumes outpace cross-border volumes in Q1 2026

In Q1, dLocal saw significantly faster growth in local-to-local volumes – tracking payments where dLocal collects and settles in the same currency within the same country – versus cross-border volumes, where dLocal collects in one currency and settles in a different currency in a different country.

Cross-border volumes grew 49% to $6.3bn, driven primarily by dLocal’s financial services, SaaS and travel segments while local volumes grew by 101%, with these mainly driven by on-demand delivery, ride-hailing, streaming and advertising segments.

Rapid local volumes means the company’s split is changing, with cross-border volumes accounting for 45% of TPV in Q1 2026, versus 53% in Q1 2025. CEO Pedro Arnt noted that dLocal serves the on-demand delivery business for several significant players in its ecommerce and ride-hailing verticals, with these verticals having a higher local-to-local component with stronger adoption of local payment methods.

The shift towards local-to-local volumes reflects a broader trend that dLocal continues to track, which is that local payment methods are ultimately the primary way consumers are transacting online. During the earnings call, the company noted examples such as Peru, South Africa, Saudi Arabia, Nigeria and Egypt, where supporting local payment methods and card schemes is important for capturing share. Arnt noted that compared to international acquiring, where merchants use international card rails to complete transactions, the company is able to deliver up to 20 percentage points conversion uplift in certain markets.

Remittances remains dLocal’s fastest growing segment

While it did not break out specific volumes in this quarter, dLocal highlighted TPV growth it has seen across its verticals from Q1 2024-Q1 2026. Over this period, the company’s remittances segment has grown by 356%, making it the fastest growing segment, followed by on-demand delivery (339%), ecommerce (186%), ride-hailing (176%) and SaaS (175%).

Remittances growth is linked to the company continuing to support geographic expansion by major players, driven by a “sustained strategic focus and ongoing merchant onboarding”. Meanwhile, ecommerce remains the company’s largest vertical and continued to ramp up as multiple global players added additional markets.

On-demand delivery’s strong growth reflected growth from regional players, with this segment and ride-hailing seeing expanding global partnerships with leading players. Volumes for both segments are largely local-to-local. During the earnings call, Arnt also noted significant opportunities in travel and gaming, which the company says are historically underpenetrated verticals for which it is building out payment flows.

Finally, financial services has historically been another large segment for dLocal, and notably includes its crypto and stablecoins services. It rose by 87% over the period due to expanding global partnerships with leading players.

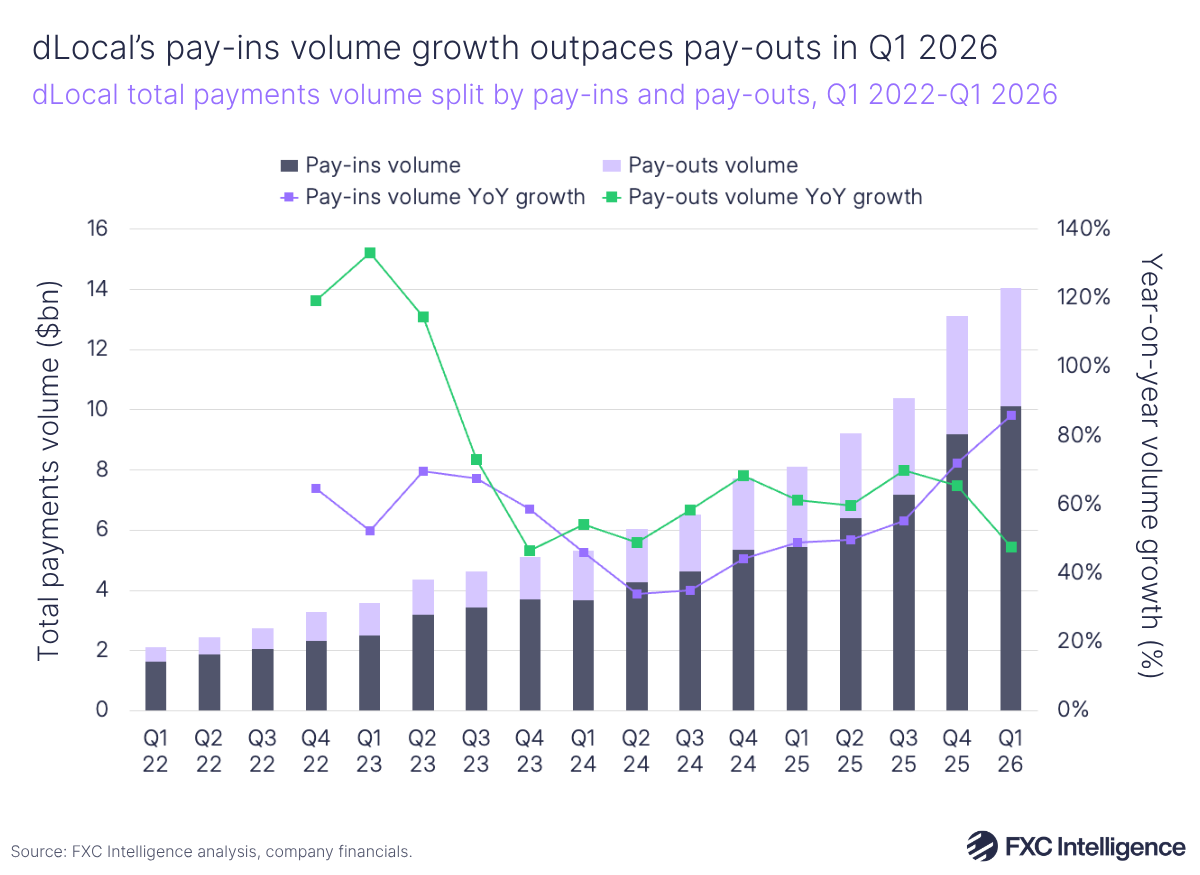

Pay-ins volume growth outpacing pay-outs

Reflecting dLocal’s changing cross-border mix, dLocal is also seeing faster growth in pay-ins volume – spanning transactions where dLocal’s merchant customers receive payments from customers – against pay-outs volume – transactions where dLocal disburses money in local currency to business partners or customers of its merchant clients.

Pay-ins volume grew by 86% to $10.1bn, reflecting dLocal’s growth in on-demand delivery, ride-hailing, SaaS and streaming. Meanwhile, pay-outs grew 48% YoY to $3.9bn, likely driven by strength in remittances and other segments requiring pay-outs.

Pay-ins took a 72% volume share of dLocal’s TPV in Q1 2026, and its faster growth versus pay-outs highlights dLocal’s strengths in localised payment acceptance across many of its core verticals.

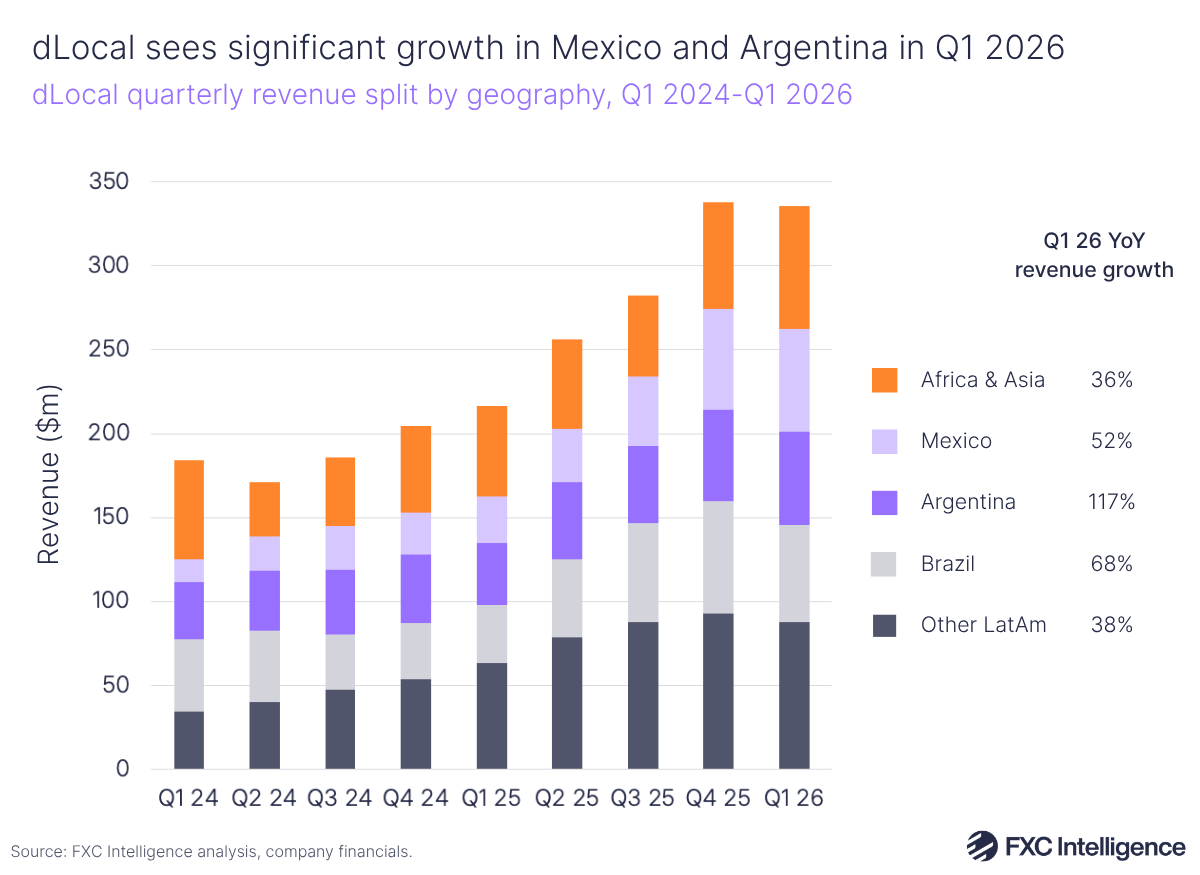

dLocal’s core markets drive bulk of growth in Q1 2026

dLocal reported solid YoY revenue growth across its geographies in Q1 2026, with LatAm markets rising by 61% YoY to $263m, while Africa & Asia (now containing Egypt, previously broken out separately) rose by 36% YoY to $73m. LatAm, however, did see a 4% QoQ decline, driven by a less favourable payment method and merchant mix in Brazil and smaller LatAm markets, as well as narrower FX spreads.

Across its largest markets, dLocal saw a strong recovery in Argentina, which saw revenue rise 117% on the back of strong volume growth, while Mexico revenue grew by 52% and Brazil grew by 22%.

dLocal focused on the different markets’ profitability in Q1 2026 earnings, with Argentina seeing strong volume growth and normalised funding costs driving 87% QoQ growth to $16m in gross profit after volatility related to the country’s elections in H2 2025, and 46% growth YoY. Meanwhile, in Brazil, gross profit rose 112% YoY to $28m – though this was down 20% versus the previous quarter, which the company linked to difficult comparisons vs a strong Q4.

dLocal also called out that notable volume gains in Nigeria, Mozambique and Vietnam helped drive Africa & Asia’s gross profit up 34% YoY to $34m. Africa and Asia now represent 29% of the company’s gross profit, while its QoQ growth (16%) is faster than QoQ growth for the company overall (3%), which dLocal said highlights how it is helping the company diversify its earnings.

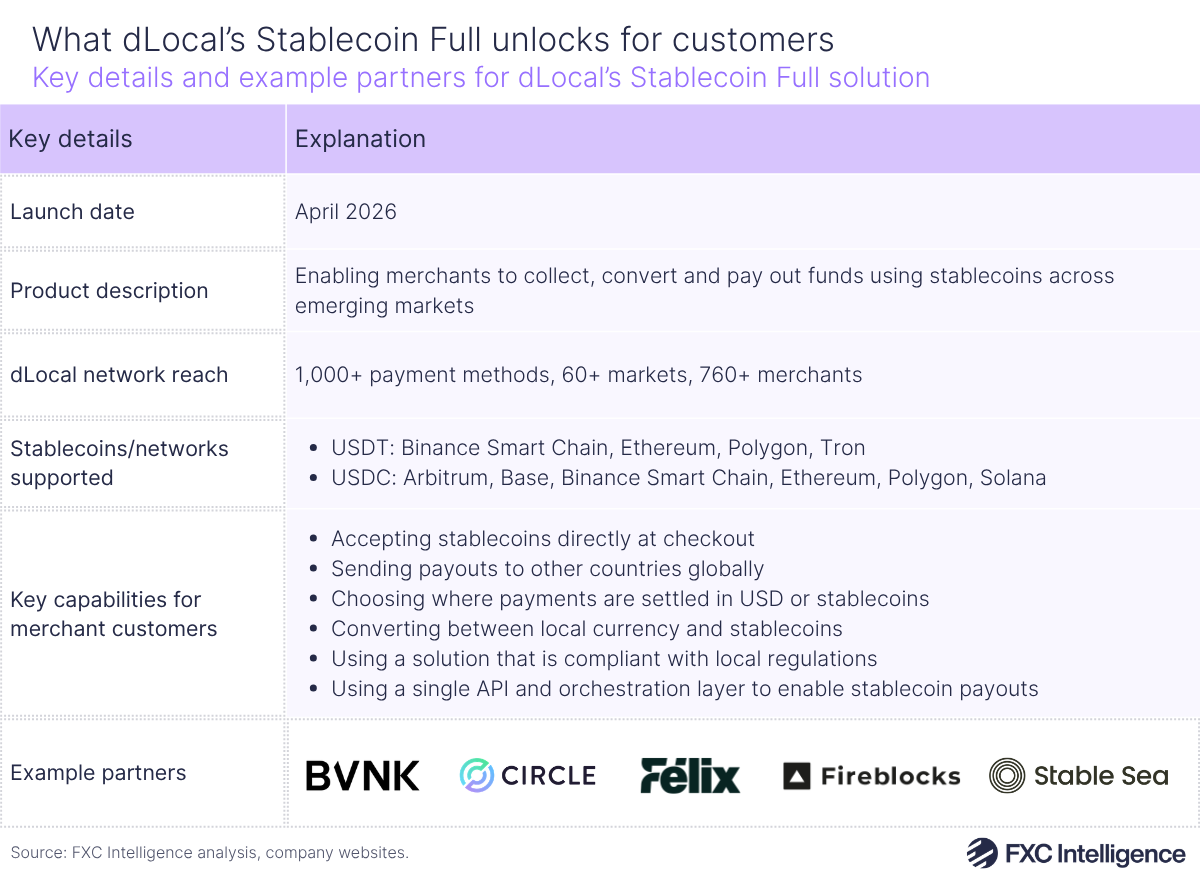

Where stablecoins and agentic fit in dLocal’s strategy

Responding to a question in the earnings call, Arnt also explained how dLocal is thinking about two major payment trends: agentic AI, on which the company has collaborated with Google on creating its Agent Payments Protocol standard, and stablecoins, for which dLocal has recently launched Stablecoin Full – its solution allowing merchants to collect, convert and pay out funds using stablecoins across high-growth economies.

Arnt said that following the launch of Stablecoin Full, the company has seen a rapid increase in settling to and from merchants in stablecoins. On agentic, he said that the focus should be on ensuring that global alternative payment methods that are served are included in emerging agentic protocols.

However, he added that while dLocal is working on both of these areas, the company doesn’t see these as being big generators of volumes and business in the short term. Instead, the major interest is on supporting alternative payment methods and solving complexity for rapidly expanding real-time networks in emerging markets. For the moment, dLocal remains focused on core digital wallets, real-time networks, local card schemes and localising credit cards, which he said make up the “bread and butter” of dLocal’s volume.

Arnt also added that businesses in the space now see payments infrastructure as a core part of their go-to-market strategy, with merchants coming to dLocal to ask about real-time networks such as Pix in Brazil and Bre-B in Colombia, The company is seeing more interest in credit solutions, buy now pay later, local wallets and card schemes. Separately, dLocal also mentioned an upcoming card-present solution it is developing to power payment operations for a large client across a few Latin American countries.

The overall picture is that cross-border continues to grow significantly within dLocal’s wider revenue, but its key focus remains on enabling merchants and businesses to support local payment methods in emerging markets.