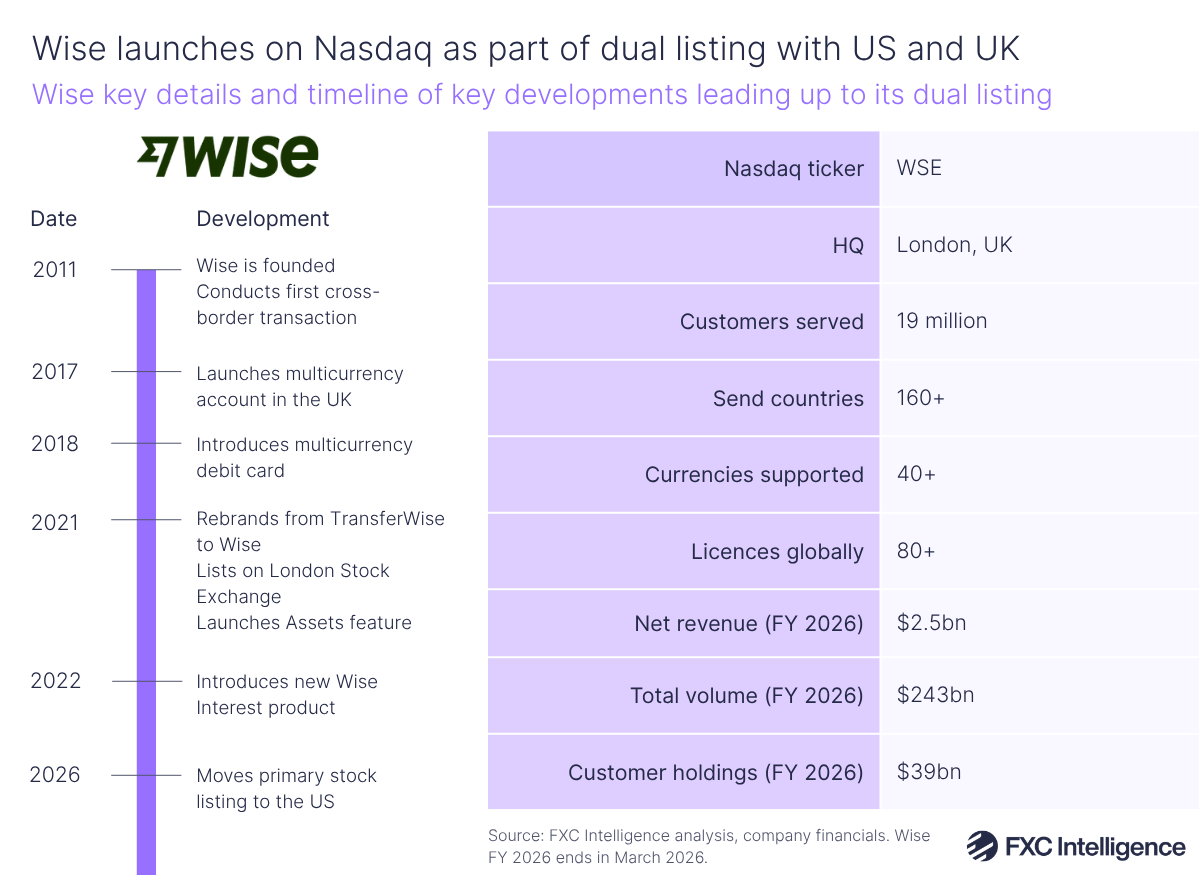

This week, Wise began trading on the Nasdaq, meaning that it is now primarily listed on the US’s second-largest stock market while retaining its listing on the London Stock Exchange. We’ve summarised some of the key points from the company’s latest figures and investor presentation below.

Wise has been in the US for over 10 years and already holds 49 money transmitter licences in the country. However, the new listing both gives it access to the world’s most liquid capital market and grows its reach across thousands of US banks, consumers and businesses. It also aligns with Wise’s ongoing application for a US national trust bank charter, through which it aims to deepen its connection to the US payment networks.

Wise used its presentation to introduce its core strengths to US investors, arguing that its money transfer network enables competitive pricing and speed (with 75% of cross-border transactions settling in under 20 seconds). It is also difficult to replicate, with Wise having enabled direct settlement accounts with central banks in eight countries (each of which requires a multi-year regulatory approval process) to bypass correspondent banks and reduce pricing.

The company frequently mentioned its take rate, which fell from 64 bps in Q1 2025 to 51 bps in Q4 2026, helping spur cross-border volume growth. Wise CFO Emmanuel Thomassin said that the company continually tracks pricing to ensure it still delivers a margin for the company while sharing excess benefits with customers.

Aside from growing its core money transfer offering and expanding its Wise Account product, Wise is looking to grow Wise Platform – its white-label network solution allowing Tier 1 banks, neobanks and tech companies to use Wise infrastructure to enable global transfers. The company said that the platform is being priced at parity with its direct retail business, making the platform more compelling for partners and allowing it to simultaneously compete with and support banks.

Wise CTO Harsh Sinha also gave an update on how Wise sees stablecoins, specifically around their use cases in cross-border money movement and managing currency volatility. The company argued that significant on/off-ramp friction in stablecoin rails means that Wise’s network is still faster and more cost-effective for transfers, thanks to its investment in fast local domestic payment systems and broad infrastructure reach.

On currency volatility, Sinha said that Wise’s multicurrency account already offers a solution allowing customers to hold and exchange currencies easily. However, he added that Wise’s infrastructure is “extendable” and it would be able to add stablecoins for money movement if it does solve problems for its customers in the future.

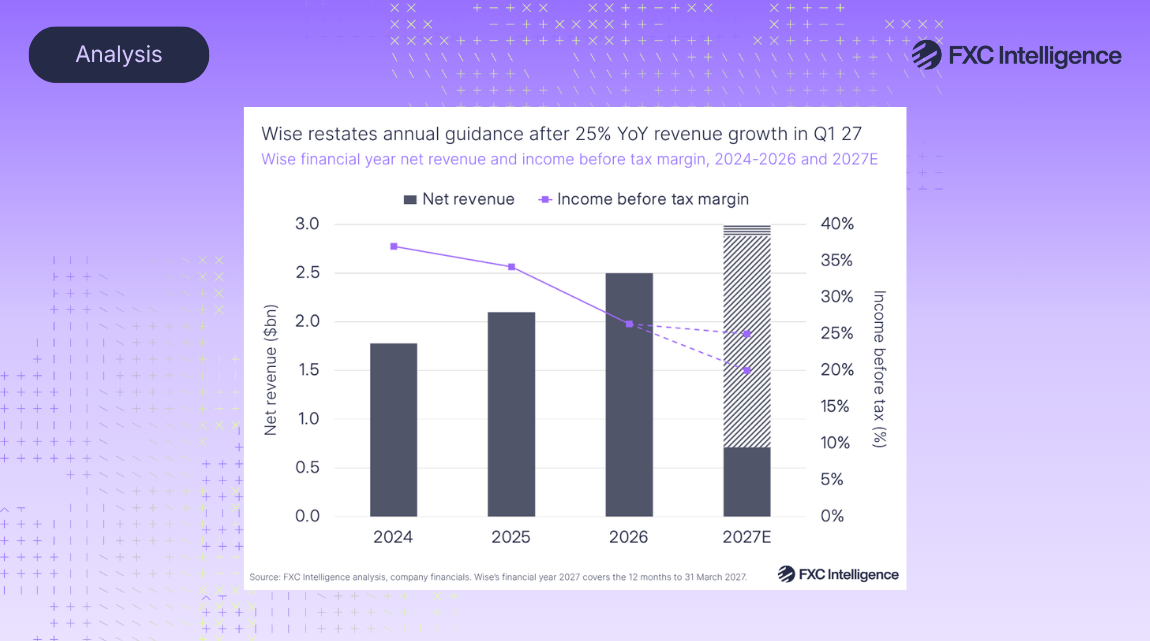

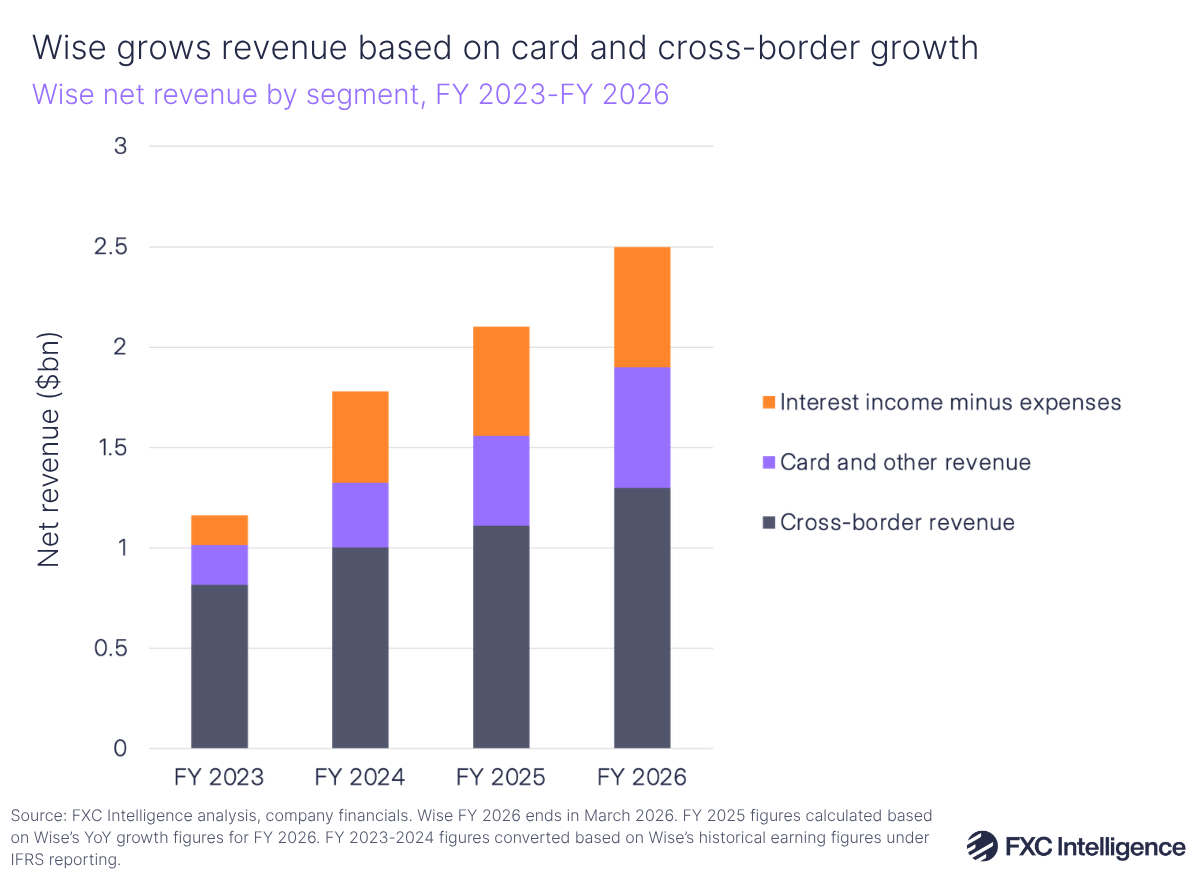

Wise also shared preliminary US GAAP figures for FY 2026 (ending in March 2026), with metrics provided in USD for the first time. Previously, the company shared underlying income, which only included the first 1% yield of interest on customer balances that Wise intends to keep. In its new presentation, Wise presented its core topline figure as net revenue, which includes all the interest income accrued minus any interest paid out to customers. This rose by 19% in FY 2026 and contains two core streams: transaction revenue – which contains the company’s cross-border revenue segment as well as card and other revenue, including fees across cards, Wise assets and other products – and interest income, which comprises interest accrued on customer balances.

Transaction revenues rose 22% YoY to $1.9bn, driven by a 17% rise in cross-border revenue to $1.3bn and a 34% rise in Card and other revenue to $0.6bn. As of this dual listing presentation, cross-border currently accounts for just over 50% of Wise’s revenue. Cross-border volumes rose by 31% YoY to $243bn, while the company noted 37% growth in card spending, up to $44bn. Overall, customers grew to 19 million, up 21%.

The company’s income is also split globally, with 28% of revenue coming from Europe, 26% from the UK, 18% from APAC, 15% from the US and 12% from Rest of World. The company also noted that for H1 2026, its income before tax (IBT) formed around 25% of its net revenue.

A huge emphasis for Wise has been its shift to customers holding balances with the company, which in turn is driving more money transfers, card spending and interest income. Customer holdings rose 40% to $39bn, including $9bn in holdings for Wise Assets, which allows users to invest held currencies in stocks or funds.

Under Wise’s targeted framework, the first 1% yield of interest income generated will cover its costs for operating Wise Account, with 20% of the above 1% yield kept as profit and 80% being passed back to customers. In practice, Wise generated $800m in total interest income and returned $200m to customers in FY 2026, with this being partly because UK regulation has prevented Wise from paying customers interest.

Going forward, Wise aims to generate 15-20% net revenue CAGR and a 15-20% IBT margin in the medium term, though it expects to report a 20-25% IBT margin until it is able to substantially pay out its target of 80% interest income above a 1% yield.