Corpay’s Q1 2026 earnings saw the company report another strong performance overall and in its Corporate Payments Business, as well as announcing some key tokenisation and blockchain partnerships. We spoke to Corpay Cross-Border Solutions Group President Mark Frey to learn more about how the company is thinking about strategy across this year and beyond.

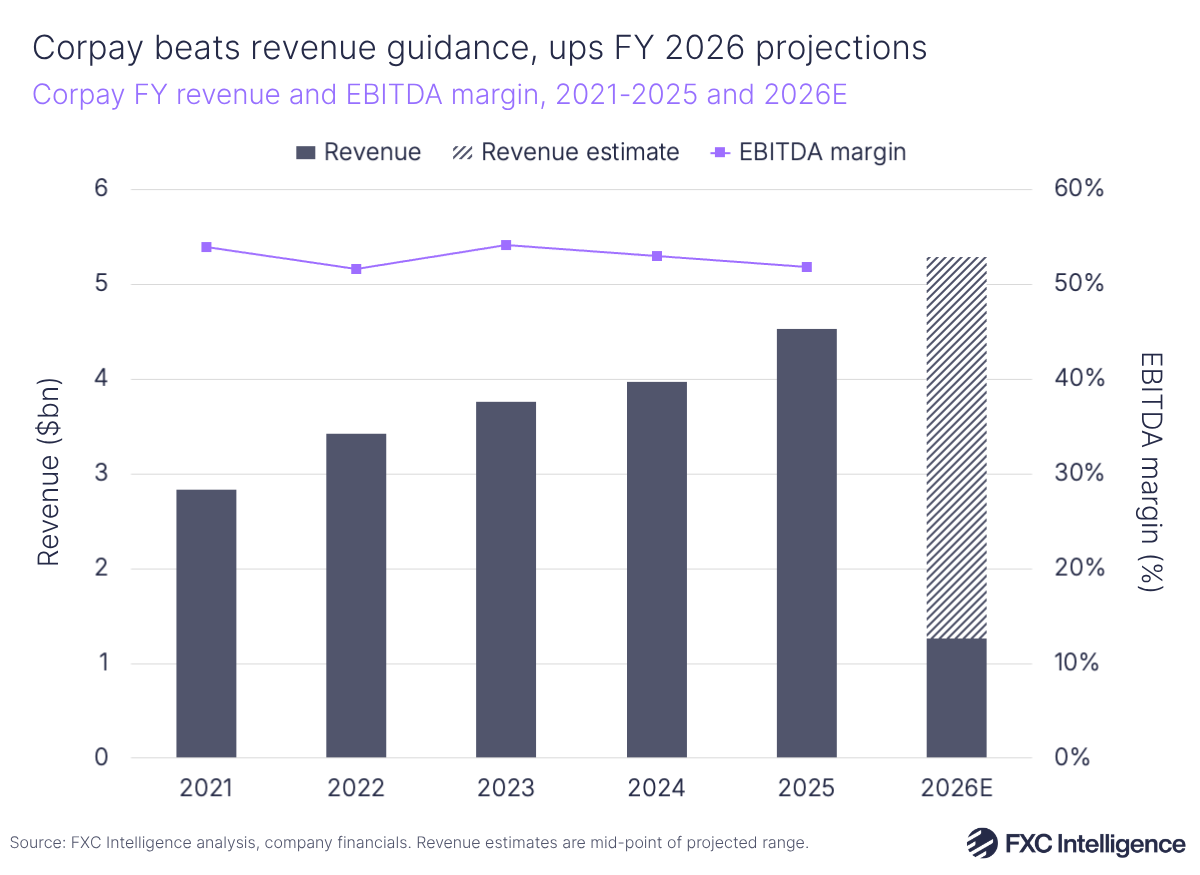

Q1 2026 saw Corpay report another very strong set of results, beating top-line projections to reach $1.3bn in revenue, an increase of 25% YoY, or 11% on an organic basis, excluding gains from the recent acquisition of Alpha.

Investors responded positively, not just to the outsized growth but also to news of two key partnerships with J.P. Morgan and BVNK, which focus on the use of tokenisation and blockchain technology to enhance Corpay’s overall money movement.

This follows a partnership with Mastercard that saw the card giant take a stake in Corpay while referring financial institutions to the corporate payments player, which is beginning to show significant results, while the company is also seeing its 2025 acquisition of Alpha begin to show impact.

With Corpay increasingly centring its strategy around its fast-growing Corporate Payments division, we caught up with Mark Frey, Group President of Corpay Cross-Border Solutions, to find out how the company is evolving its growth strategy and incorporating tokenisation into the mix.

Corpay’s blockchain partnerships with J.P. Morgan and BVNK

Daniel Webber:

Before we jump into the numbers, let’s talk about some of the bigger picture. You put out a big announcement on the rails side about a relationship with two interesting, quite different companies for blockchain-based settlement: J.P. Morgan and BVNK. Talk us through how you see the partnership with both companies expanding what you’re building.

Mark Frey:

It has been an area of focus for us for some time to continue to build out our overall payment network and our interoperability, and the biggest area that we’ve been digging into with intensity is really the digital arena, in both public blockchain and private blockchain. We see this as really the fourth generation of payments: from Swift, to in-country, to real-time and now digital.

On the BVNK side, our announcement this week was focused on making digital wallets available across our network. These are companion wallets to pair with each of our multicurrency accounts that exist on our network today.

Our customers can hold fiat in multiple currencies and can also hold [digital] currencies and stablecoins in digital wallets and then send and receive payments from those digital wallets, with a primary focus on stablecoin. We’re already at a pilot stage of testing internally and have been using it from a treasury perspective for some time, and we’re set to go live with a customer solution in Q2.

The second side was the announcement with J.P. Morgan Kinexys, expanding our relationship with them. We really are significantly ramping up our payment processing that is going across the Kinexys network. It’s basically a private blockchain network solution ultimately to instruct payments as opposed to sending them across Swift.

We think of private blockchain as a primary means of us processing all fiat currency payments in the very near future, given the scale that we’re already achieving. We’ve had a long-standing relationship with Ripple where we’ve employed this capability in that arena. We’ve expanded now to J.P. Morgan Kinexys and have one other tier-one bank that we’re working with on this front as well. But with J.P. Morgan Kinexys, we’ve been able to significantly ramp payments over a short period of time to deliver some scale.

What I love about the solution is that, through our various private blockchain capabilities and now especially with Kinexys, we’ve been able to reduce the cost of processing a payment. We’re able to see those payments land on average within 22 minutes, even when we’re sending overseas, after hours, and that they are 24/7 always on.

What we have are traceable, near real-time, very cost-effective Swift wire alternatives to move money all over the world. And it has been something that we’ve seen as significantly cannibalising our Swift volume and moving it onto these private blockchain networks, which we think will continue to occur over a significant period.

The other beauty of what it achieves from a customer experience standpoint is no correspondent fees. These are effectively the equivalent of guaranteed charges on our Swift payments but effected in real-time and after hours.

It’s a very compelling solution for the downstream customer and with some cost efficiency for us as well. We’re certainly excited about it. We think that this is the future of cross-border payments, quite frankly, and it is something that we will continue to build into our network.

The impact of tokenisation on Corpay

Daniel Webber:

Where else does tokenisation help in the business? Does it help on your back end or allow you to automate things more?

Mark Frey:

It certainly helps in terms of all the operational friction of processing payments. It significantly negates the correspondent delays, lifting charges, investigations and exception handling in all forms, quite frankly.

Also because the payments arrive so quickly, we don’t get the standard queries of ‘money not received’ because it’s there in 22 minutes. And when the funds credit, it eliminates probably 95% of the queries that we get from customers of the money being stuck in a correspondent or stuck in a compliance queue or something else. Whereas we’ve seen significant streamlining of the processing of these payments and are certainly excited about the results thus far.

Corpay beats expectations in Q1 2026

In addition to its strong revenue growth, Corpay also continues to see strong earnings, reporting adjusted EBITDA of $689m, for a 55% adjusted EBITDA margin, and non-adjusted EBITDA of $636.9m, for a 51% EBITDA margin.

The results have seen the company increase its projections for FY 2026, with revenues now expected to be between $5.25bn and $5.33bn, equivalent to 17% YoY growth. Corpay also expects to see Q2 2026 deliver revenue of around $1.3bn, an 18% YoY increase.

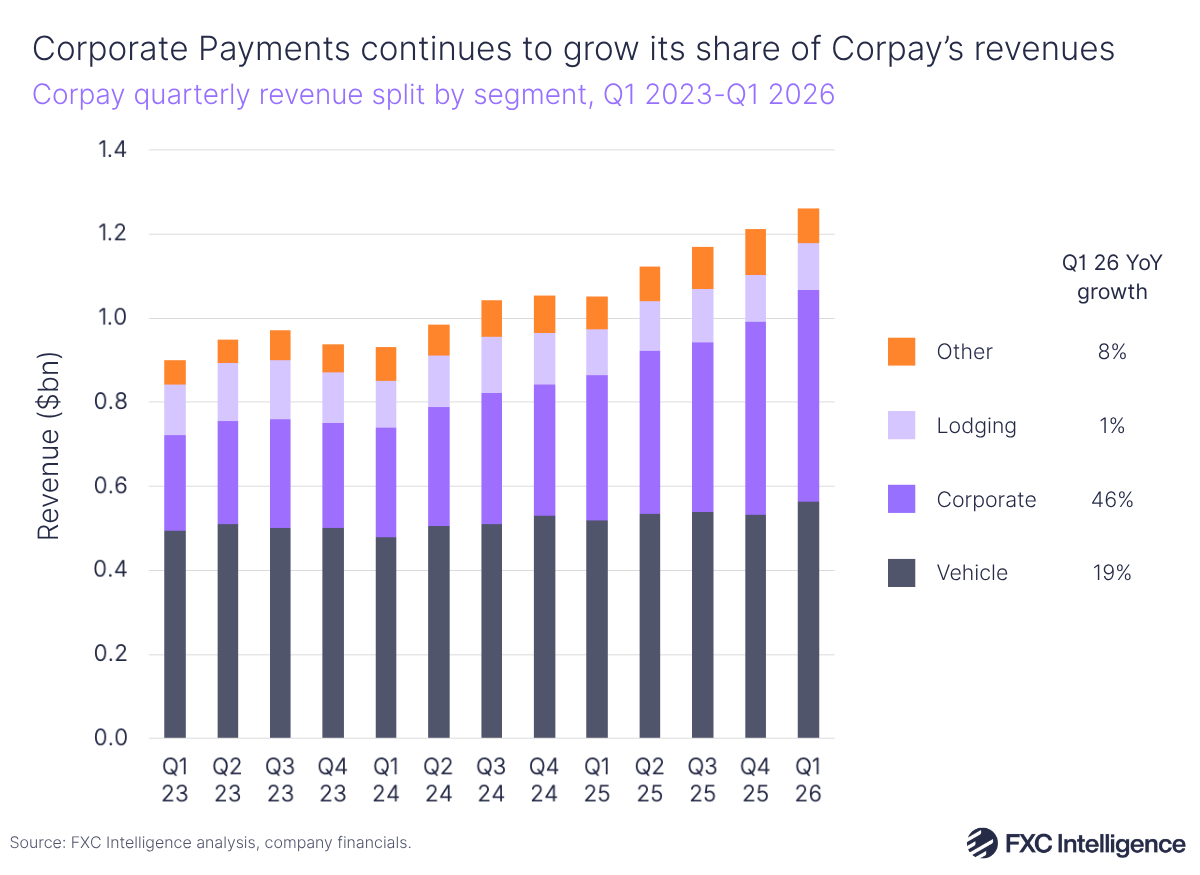

This was aided by the fact that the company has seen all of its segments returning to growth this quarter. While Corporate Payments continues to lead growth, climbing 46% YoY or 16% on an organic basis, the company’s largest segment Vehicle Payments has seen a 19% YoY increase, or 10% on an organic basis. Lodging, which has seen negative growth for the past few quarters, saw growth that was essentially flat in this latest quarter.

Corporate Payments has become increasingly central to the business and now accounts for 40% of revenue, only slightly behind Vehicle Payments’ 45% and up from 34% a year ago. Corpay is also actively centering the unit further and is in the middle of a deliberate transformation from a diversified B2B payments conglomerate into a focused, higher-growth Corporate Payments business, which CEO Ron Clarke told investors will see the company continue to divest more non-core areas of the business with constrained TAMs and use the funds to acquire further assets to bolster its Corporate Payments business.

FX hedging’s evolution

Daniel Webber:

There’s a lot of efficiencies happening in payments, but managing the risk between two currencies is still an important need. How are you seeing the FX hedging piece evolve and complement the fast-changing payment side?

Mark Frey:

In simple terms, what people need to understand is that irrespective of the rail that’s employed, whether it’s a stablecoin, whether it’s a private blockchain, whether it’s Swift or in-country or real-time rail, that’s only one part of the value chain. It’s probably the smallest part of the value chain.

That is something that is highly commoditised. There’s no price, ultimately, that is in the movement of money just purely across rails in terms of economics that we extract. 95% of our economics actually come from the FX conversion of making and facilitating cross-border payments.

That will continue unless the world accepts the US dollar everywhere, which increasingly is less the case today than it has historically been – dollarisation is reducing across the world. We see even fewer large US corporates sending US dollar payments internationally and they’re trying to go local and trying to find cost savings everywhere that they possibly can.

What even large American corporates have now finally understood is that when they send US dollars internationally, their vendors are just building in an FX buffer because those funds need to be converted at destination and then applied in local currency. So everyone is trying to find efficiencies and the world is becoming less dollarised.

So we’re seeing a greater intensity of FX in our cross-border payments, and that’s where all the economics come from. It’s not just the FX liquidity provision, of course; it’s all of the value-added services around that. It’s the risk management planning, it’s the valuation of risk and measuring of risk, it’s the trade execution, it’s also actually extracting data.

Our customers aren’t simply executing an FX trade by voice. They’re executing FX trades and instructing thousands of payments via ERP integrations, API integrations. So it’s all of the technology that supports the workflow and the approval modeling for clients that are making payments at scale that generates all the economics.

Corporate Payments sees strong growth, shifting take rate

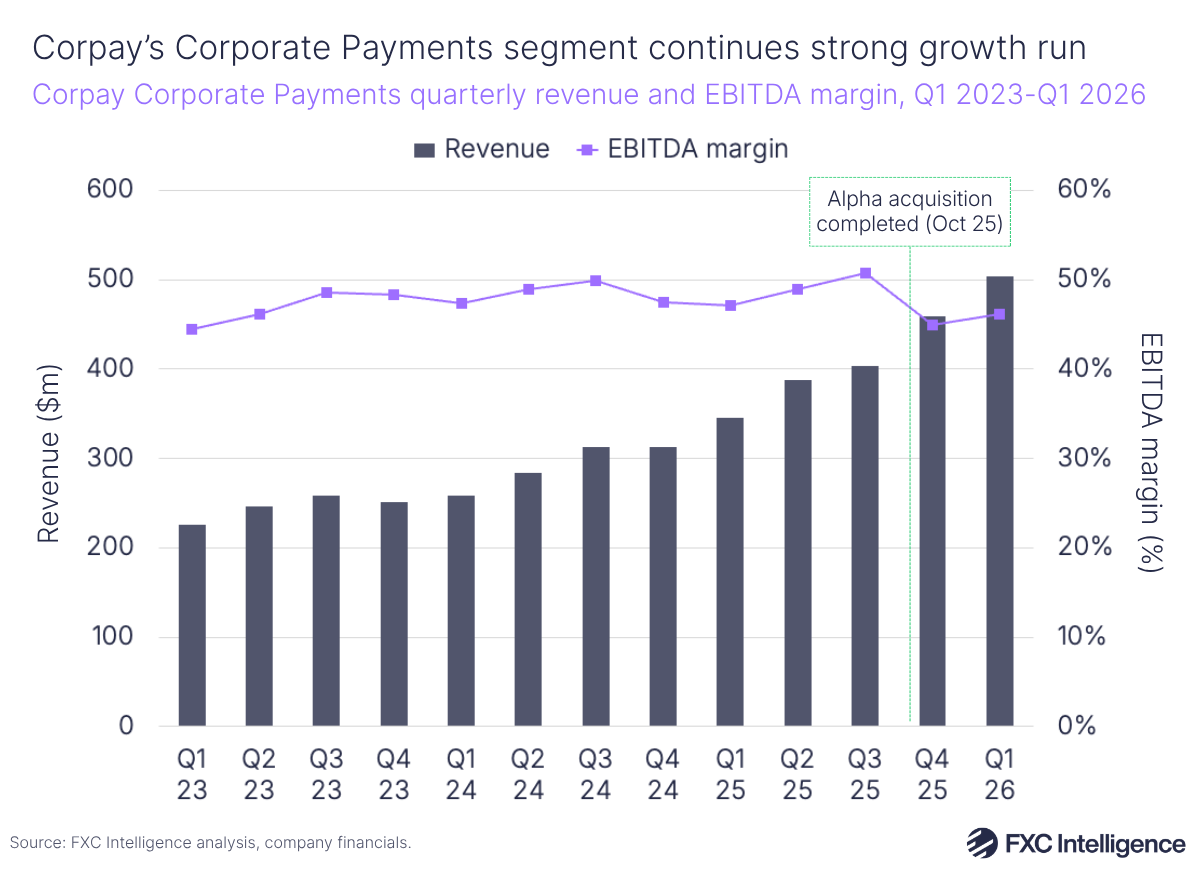

Corpay’s Corporate Payments segment saw revenue increase 46% YoY to $504m, including gains from its recent acquisition of B2B payments company Alpha, which itself saw 17% YoY organic revenue growth, excluding float compression.

Cross-border sales have also helped drive above-expectations performance, increasing 40% YoY in Q1 2026, while cross-border revenue growth is reported to be in the “high teens” on an organic basis.

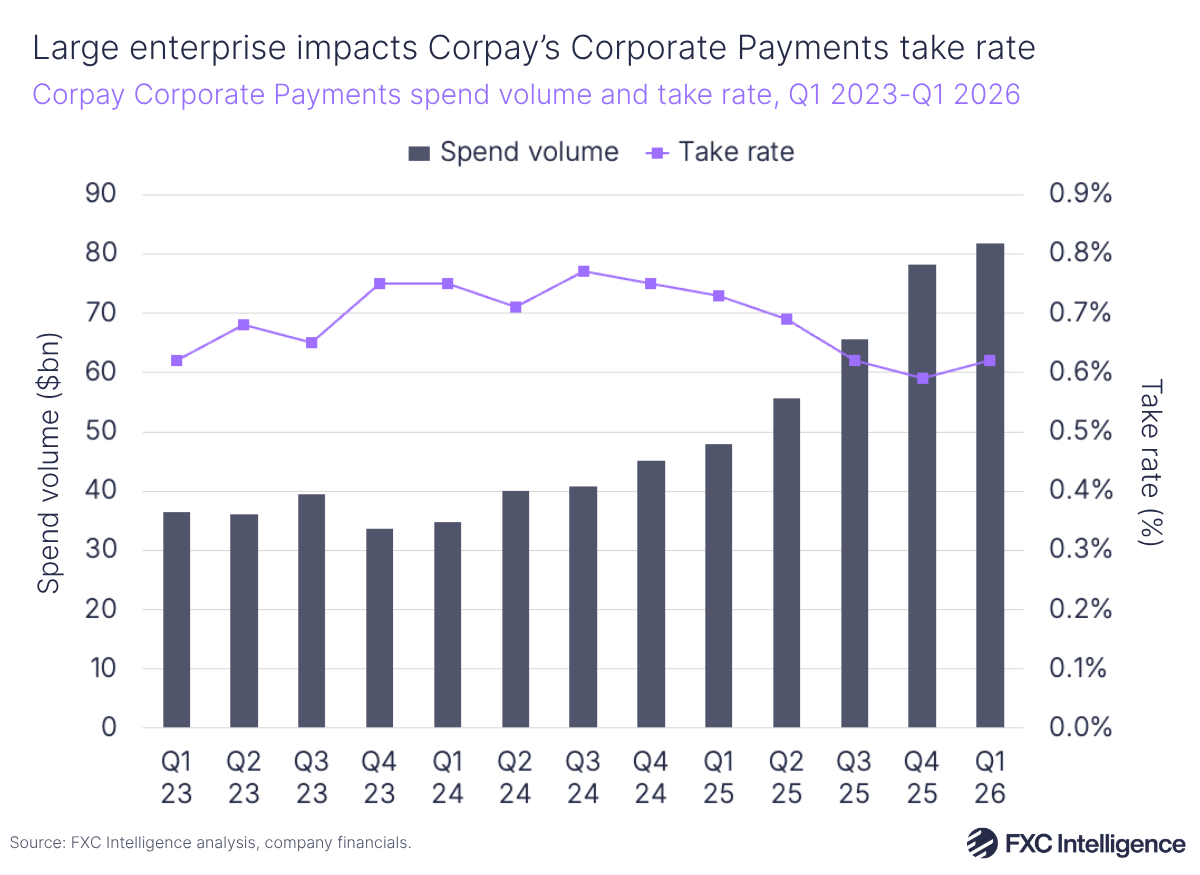

Notably, the unit has seen a decline in take rate, which was 0.62% in Q1 2026, down from 0.72% a year previously. This has been attributed to growth in large enterprise clients transacting at below ten basis point-levels, while excluding these accounts yield is reportedly holding steady.

The company’s payables and AP automation business is also performing well on volume growth and sales, and is now operating in Europe, where it has reached a run rate of around $15m despite having been a completely US business up until around six months ago.

Corpay’s Q1 2026 growth

Daniel Webber:

Let’s run through some of your Q1 numbers, which were again exceptionally strong and above the growth of the market. Can you add some colour on what’s continuing to drive them?

Mark Frey:

It was a very strong quarter for us across the Corpay franchise, really strength in all of our key market segments, not just in the Corporate Payments segment. We saw really strong performance and above expectations in our Vehicle Payments business, in our Lodging business, which had a nice bounceback quarter as well and returned to growth.

We saw very strong organic growth with a nice beat in Q1, roughly $25 million ahead of expectations, with a raise for the remainder of the year for, we think, continued strong performance despite the overall macro environment in the remaining three quarters.

So we’re bullish on the top line and we’ve had a very strong drop to the bottom in terms of our overall EBITDA result as well. Very happy at a macro level at the top of the house, a strong beat and raise from Q1 and a nice outlook for the remainder of the year.

Increasing focus on higher-value corporate payments

Daniel Webber:

Corpay is now deliberately trying to move towards higher focus corporate payments and away from being more diversified, which it was in the past. Can you talk through what the key ambitions are there.

Mark Frey:

The vision of the business is to become predominantly a corporate payments organisation, ultimately. This is the part of our business that has been growing most robustly for a number of years now. In moving up-market in the Vehicle Payments business to the mid-market corporates, what we’ve found is that there is the ability to cross-sell other Corporate Payment services into those mid-market customers because they have international payments, they have domestic payments at scale that we can convert to virtual card.

For our traditional fuel customers, in moving up-market, we are now just cross-selling our Corporate Payment services into those customers both in the US, the UK, in Europe as well. We think that this is going to significantly improve the growth prospects of that segment, ultimately. Really what it is is that the entire business is becoming more Corporate Payments-oriented as opposed to these distinct point solutions that we’ve sold historically.

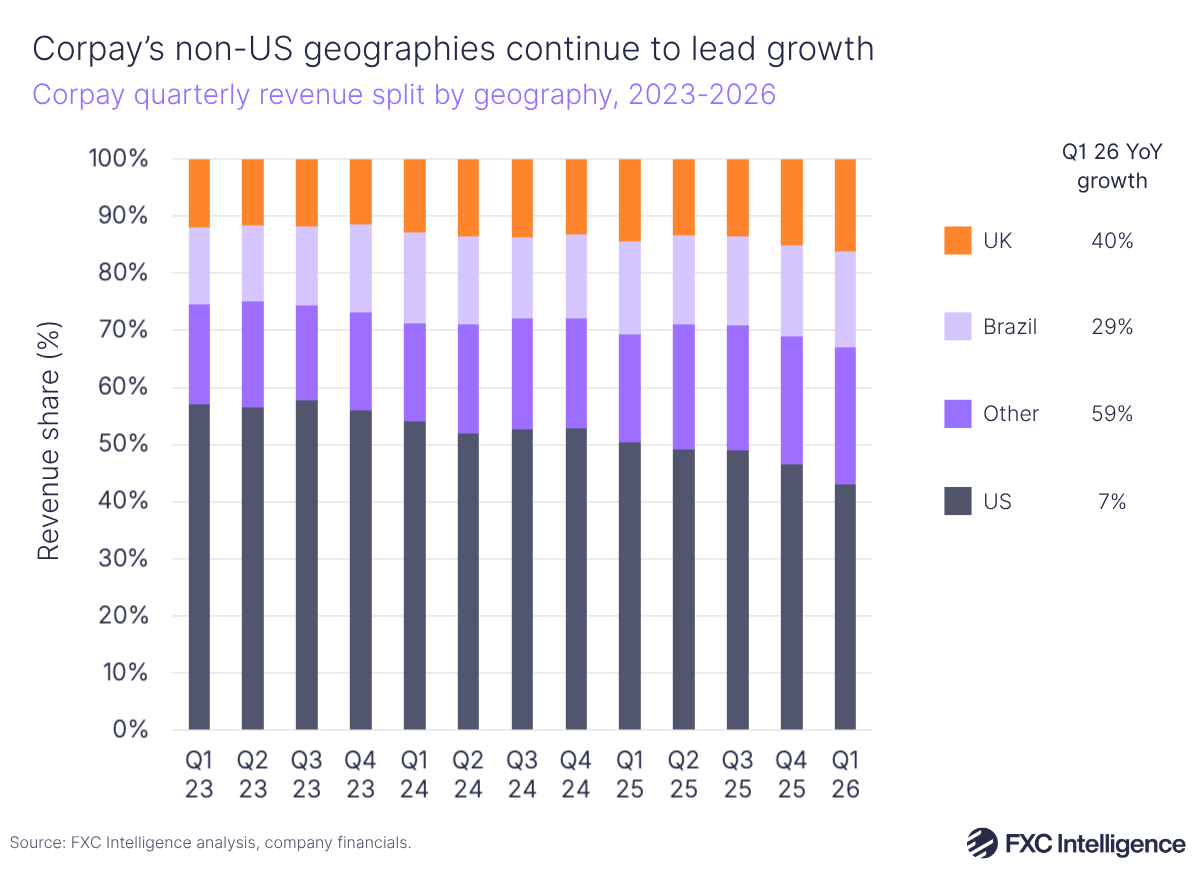

Corpay grows global reach

Corpay has seen non-US geographies being a particularly key driver of growth overall, with non-US revenue accounting for 57% of overall revenue in the quarter, up from 50% a year ago and 46% two years ago. The two largest non-US markets, Brazil and the UK, continue to grow at a faster rate than the US’s 7% YoY increase, at 29% and 40% respectively, while other markets are now seeing the strongest growth, at 59% YoY.

While initiatives such as its Mastercard partnership are helping in this area, expansion of a number of products internationally is also helping drive international growth. In particular, the multicurrency accounts product has been extended to a number of new geographies this quarter, and is also a popular product with financial institution clients gained via the Mastercard partnership.

The company also noted that FX volatility in Q1 created a favourable sales environment, reporting around $62m of positive FX revenue versus the previous year.

Traction from Corpay’s Mastercard partnership

Daniel Webber:

You’re beginning to see good traction from your partnership with Mastercard now it’s settled in. Talk us through your thoughts there.

Mark Frey:

We’ve been very pleased with the outcome that we’ve received through that partnership with Mastercard. A very active pipeline, just under 50 financial institutions in process in terms of our various sales stages today. We’ve closed a number of deals; some of them are very attractive, large-sized deals, perhaps a little bit larger than what we were expecting to come through this channel quite frankly.

What we’ve found is that these financial institutions are hungry for payment solutions. They’re hungry for rail interoperability. They’re hungry for access to digital services; they’re hungry for FX capability to be delivered via those payment services, and so it’s been a really good fit for us and a very strong partnership.

What we’ve been impressed with is Mastercard’s ability to really accelerate the sales process; obviously a very well-known brand with great relationships with these financial institution partners. They’ve been able to effectively walk us in to meet with the right folks at each institution and have significantly accelerated what is traditionally a very long sales cycle.

Benefits from the Alpha acquisition

Daniel Webber:

We’re almost at time. Is there anything else that you want to discuss that we didn’t get to talk through?

Mark Frey:

It’s definitely worth touching on the Alpha acquisition and how that integration is coming along. We’ve already begun to convert corporate customers in a handful of geographies to the Corpay platform.

Materially speaking, we will have most of the business converted in Q2 and it will be stood up on the Corpay platform, which provides us a great deal of flexibility. More product and capability that we can sell into each of those customers, more operational efficiency that we can offer on the back end.

We’re only a few months away from fully integrating Alpha’s core banking platform into our overall tech stack going forward. So that will be a significant enhancement to our capability in the private markets and the corporate space to provide virtual accounts to our downstream customers.

We think this is a business that we can scale really, really nicely. Alpha’s been a really good grower for us already, with 17% organic growth, excluding the float compression and interest rate compression that we saw in Q1. A really good outcome given all the change especially that’s going on in that business. We’re very pleased with that outcome and are running a little bit ahead of schedule of where we expected to be in terms of synergy realisation, top and bottom line, and sales are coming in a little bit stronger than what we had forecast.

Daniel Webber:

Excellent. Mark, a pleasure. Thank you.

Mark Frey:

Thank you.