Corpay beat its expectations in Q4 and FY 2025 with strong cross-border sales and is already seeing gains from its recent Alpha acquisition. We spoke to Corpay Cross-Border Solutions Group President Mark Frey to discuss key drivers of the company’s outsized growth, the impact of tariffs and its plan for 2026.

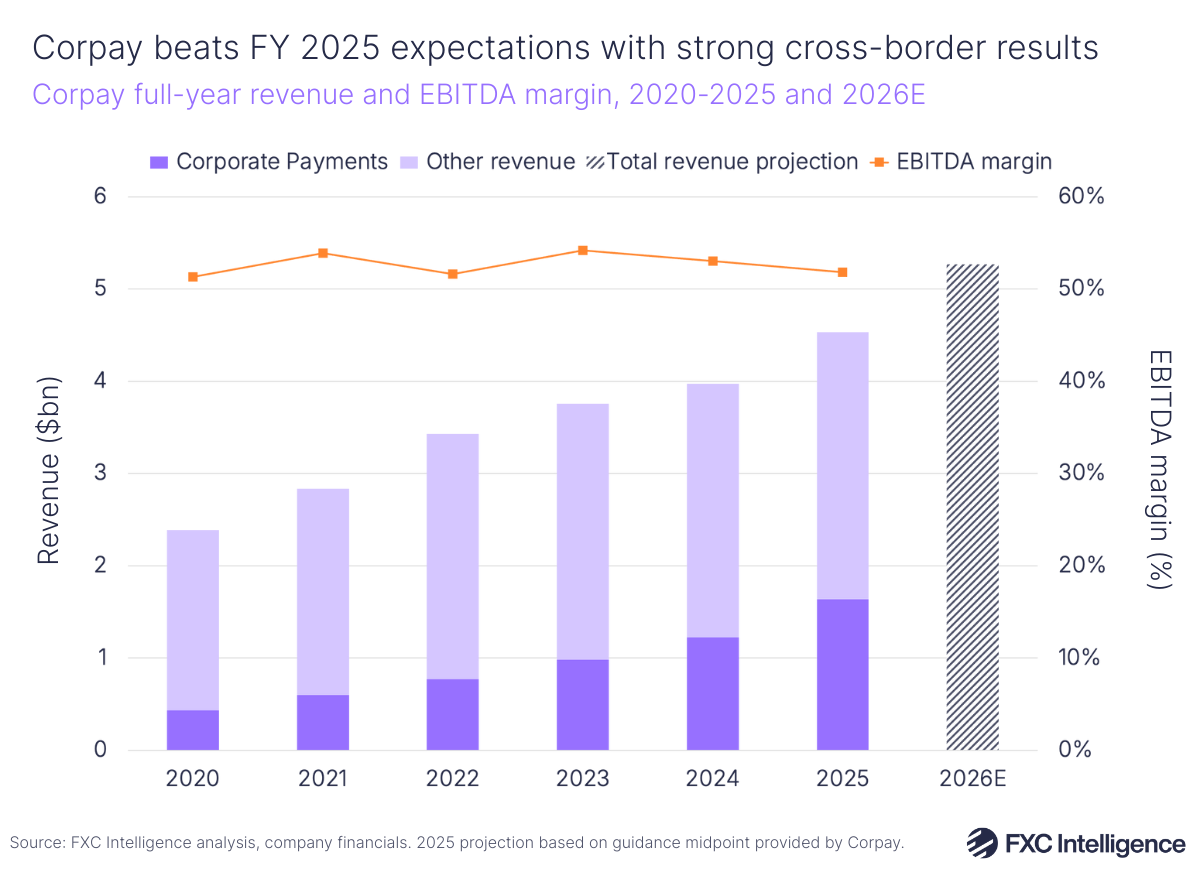

Corpay delivered strong results in Q4 and FY 2025, with revenue rising 21% for the quarter to $1.2bn and up 14% for the full year to $4.5bn. After a year marked by significant trade uncertainty caused by US tariffs, investors responded well to Corpay’s resilience (its share price rose by 12% the day after its results) while its recent acquisition of Europe-focused B2B payments provider Alpha is set to drive further growth in 2026.

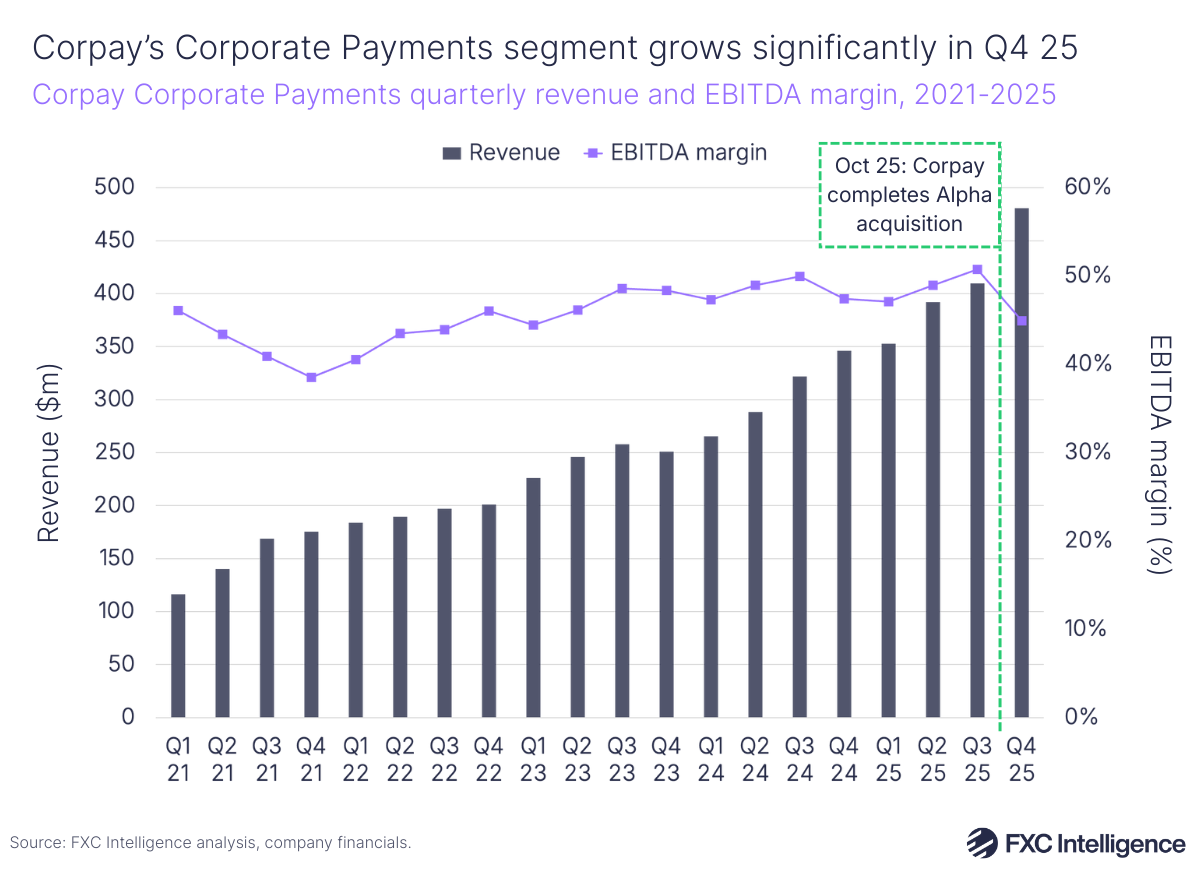

Corporate Payments revenue rose 39% to $481m in Q4 2025, with a key driver of this being cross-border sales. Bolstering this, Corpay completed its $2.4bn acquisition of Alpha in November, extending its cross-border solution set while giving Alpha access to Corpay’s global footprint. The company projects Alpha could now drive $300m of revenue for the company in 2026. In terms of revenue, the company projects it will accrue $5.2bn-5.3bn this year, up 15-17% compared to 2025.

Corpay is continuing to take steps to centre Corporate Payments, its key cross-border business. Aside from closing the Alpha acquisition, in Q4 the company also completed its deal with Mastercard, which acquired a $300m minority stake in Corpay’s cross-border services and is now introducing the company to its wide set of financial institution clients. Combined with the Alpha acquisition, this deal now puts the total enterprise value of Corpay’s Corporate Payments’ business at $13bn, according to the company. Corpay has closed two deals with financial institutions through its Mastercard partnership with significantly more in the pipeline, highlighting how it is continuing to open up access to banking cross-border flows globally.

Corpay is also shifting focus through changes to its portfolio. Last week, it announced the sale of PayByPhone, a mobile parking payments business it acquired in 2023, to Lightyear Capital, with the deal expected to close in Q2 2026. Two further additional divestments are currently in the pipeline.

To find out more about how Corpay is driving its outsized growth and targeting new opportunities in 2026, we spoke to Mark Frey, Group President of Corpay Cross-Border Solutions.

Corpay’s key growth drivers in Q4 and FY 2025

Daniel Webber:

Corpay has seen very strong Q4 and FY revenue growth. What’s driving this?

Mark Frey:

From the top of the organisation, we’ve increasingly focused on the corporate payments business and we are beginning to migrate to more of a Corporate Payments focus across the enterprise.

That is obvious with the inorganic investments that we’ve done, both on the domestic payable side with the AvidExchange deal and then obviously the Alpha transaction within cross-border.

Broadly across the enterprise, in our international vehicle payments business, in our Brazilian business and in our North American vehicle payments business, we continue to focus on enhancing our corporate payment solutions within that marketplace.

The business overall is re-pivoting towards corporate payments that we think will deliver sustaining growth. The total value of the market that we can hunt in ultimately, in terms of new customer acquisition, just gives us a better trajectory and runway for growth as a corporate payments franchise going forward.

That’s really what we’ve been focused on organically and organically. We will continue to reorganise the business in that direction, and we will continue to try and cross-sell services across our various customers to make use of the corporate payment assets that we’ve assembled.

We do think that there’s still more runway for deals. The total addressable market is super attractive for us, as is our ability now to cross-sell at scale into our existing customers in the lodging business, in the vehicle payments business and in various geographies.

We’re now beginning to execute in a material form on that, and I think it’s going to begin to support the growth in those other segments of the business as well.

Corpay Q4 2025 and FY 2025 highlights

Corpay beat its growth expectations in its final quarter of 2025, with revenue growing 21% YoY to $1.25bn. Organic revenue growth (which removes the impact of macroeconomic events and acquisitions) rose 11%, largely driven by 16% organic growth in Corporate Payments. Full-year revenue, meanwhile, rose 14% to $4.5bn.

The company’s overall adjusted EBITDA in Q4 25 rose 18% to $712.4m, driving a 13% rise for the full year to $2.6bn. For the full year, the company’s non-adjusted EBITDA margin was 52%, down slightly from 53% in 2024 but showing the company’s continued profitability this year.

Going forward, the company provided guidance for its full-year revenue to be between $5.2bn and $5.3bn, with Q1 2026 organic growth expected to be 9% YoY at the midpoint. As part of this, the company is expecting Alpha in its first full year to contribute around $300m to 2026 revenue.

Inside Corpay’s payments strategy

Daniel Webber:

How are you thinking about the different aspects of payments, and what role do these play within your strategy?

Mark Frey:

We’re focused on three key segments for our business. There’s the FX risk management and hedging; there’s the cross-border payments, some of which are cross-border but in the same currency, so there isn’t FX. Most of our revenue, of course, comes from the FX transactions, and that’s the part that’s growing in terms of volume most aggressively.

Then there’s the virtual account business, which is relatively newer but we think highly complementary to those first two segments and allows us to acquire customers with greater scale. We are super encouraged by the growth that we continue to see in the payments business, and here it’s servicing crypto and stablecoin and more traditional avenues.

We have a big financial institutions and payment aggregation business where we service other financial intermediaries, and that’s a partner-driven business that allows us to scale significantly and scale transaction and volume growth.

To the earlier point, we’ve always believed that the cross-border FX payments business is really about scale, and we continue to see the benefits of this and those benefits are accelerating the larger that we get.

We still have lots of runway in front of us in terms of scale economics that we’ll achieve as the business continues to grow, and we want to lean into that advantage as much as we possibly can in the marketplace.

Corporate Payments receives boost from Alpha acquisition

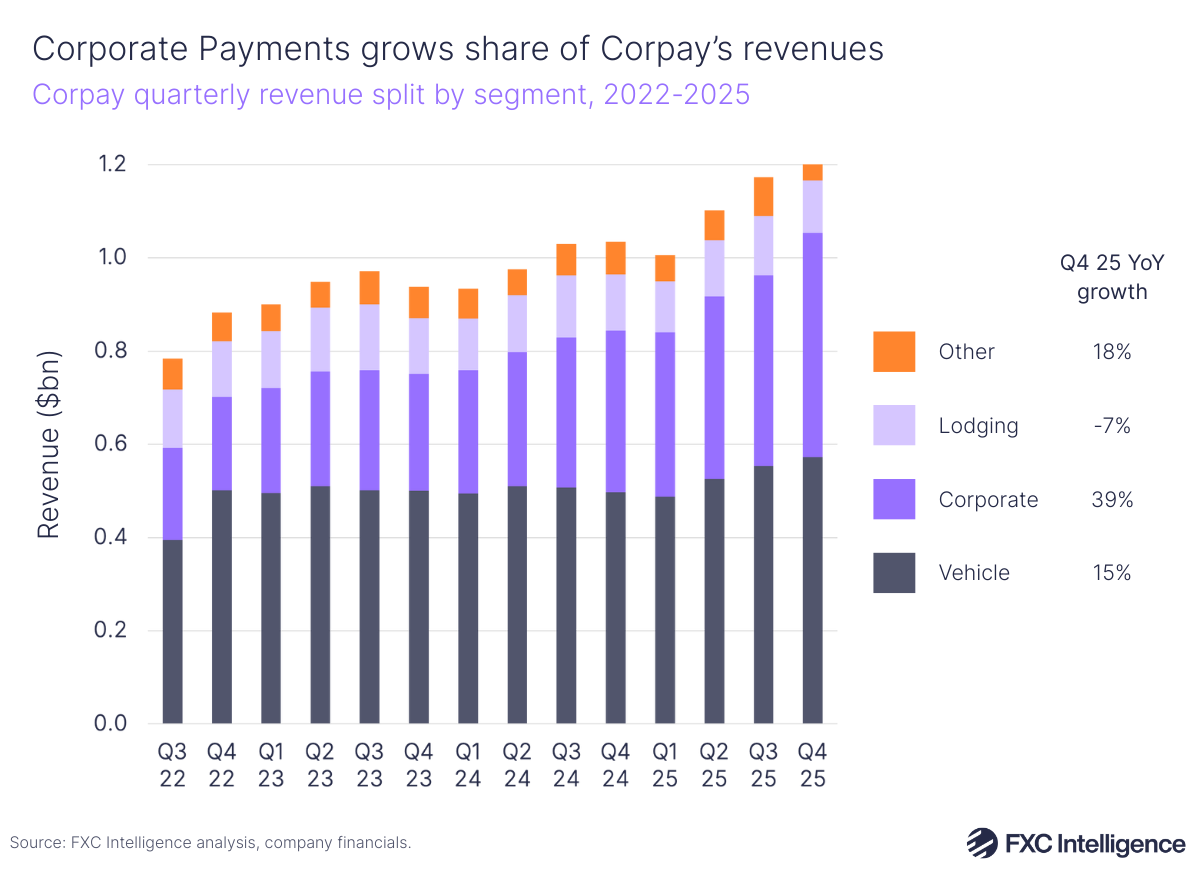

Corporate Payments remained a major driver of Corpay’s revenues in 2025, with the recently closed Alpha acquisition providing a significant boost in Q4. The segment’s revenue grew 16% organically, while in total revenue rose 39% to $481m in Q4 2025 – the fastest growth rate Corporate Payments has seen since Q1 2022.

The key factor here was spend volumes rising by 67% to over $81bn, while Corpay Chairman and CEO Ron Clarke also noted that cross-border had continued to deliver strong sales in Q4, with demand staying resilient even after “trade-related uncertainties” during the year. However, the company’s revenues net per spend declined slightly from 0.71% in Q4 2024 to 0.59% in Q4 2025.

For FY 2026, Corporate Payments is expected to drive organic YoY growth in the mid-teens, including a drag on float revenue from lower interest rates. This growth is expected to once again be faster than high-single-digit growth for Vehicle Payments and low-single digit growth for Lodging.

How Corpay is navigating tariff impacts

Daniel Webber:

Talk us through how you’ve been navigating some of the macro elements and headwinds such as tariffs.

Mark Frey:

The area where we saw the biggest impact from the tariffs was really our North American business, so the US, Canada and the corporates that we onboarded in Mexico as well.

Where we felt the most impact was actually the US business in particular. There were certain sectors, export and import, where we saw significant strains as Liberation Day tariffs began to play out. With the level of uncertainty in the marketplace, the constantly changing macro dynamics with which tariffs were moving and which were not, it just became very difficult for decision makers to make decisions in terms of how they wanted to run their business.

Now, markets are a little quieter. We’ve seen a little less volatility in terms of announcements from the US administration and other jurisdictions. That improving certainty is allowing businesses to adjust to the new level of tariffs where they exist and is allowing them to begin to plan with a little bit more confidence, which allows them to come back into the market.

We see increased hedging activity as a result. We see that trade flows are beginning to rebuild. We see that some trade flows are actually being redirected in certain cases, so for certain customers that were doing dollar Canada exposure before, we now see them doing dollar-yen or dollar-Korea.

We see a lot of Canadian firms that have shifted to exporting products to Europe and Mexico and away from the US, so there’s a rebalancing of trade flows that has occurred. It’s taken some time for businesses to adjust and to begin to lean into those new trade routes and those customers and/or vendors and begin to a) hedge once again, now that they’ve reestablished these trade routes and b) begin to grow and invest with a little bit more confidence.

We’re starting to see some capex spending come back. I think firms are beginning to be a little less cautious about their balance sheet and their P&L, and are beginning to focus on growth once again, which for our market is definitely a positive.

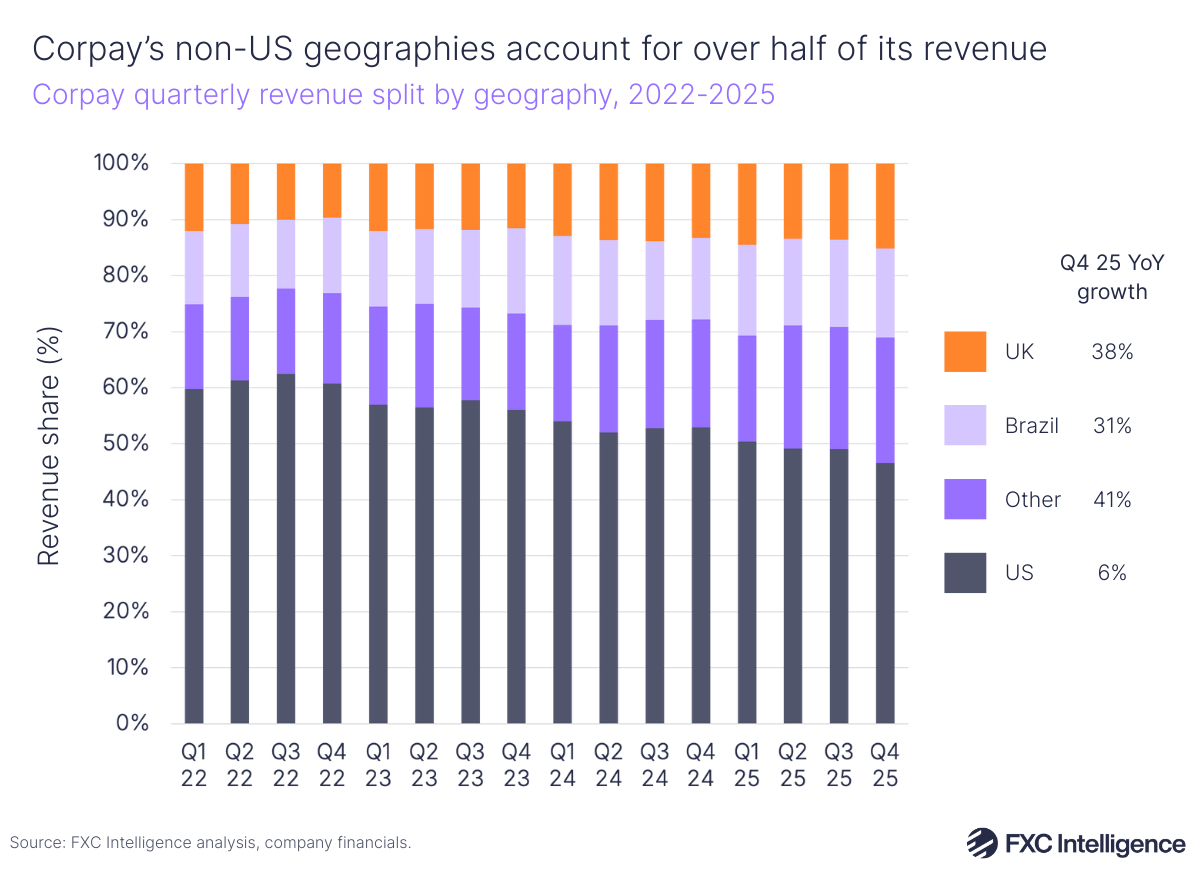

Non-US geographies take higher share of Corpay

Corpay continues to see its share of revenues from non-US geographies increase over time. UK revenues rose 38% YoY in Q4 2025 and took a 15% share of Corpay’s overall revenue; Brazil rose 31% and took a 16% share; and Other (including other markets outside the US) rose 41% and accounted for 22% of revenue.

Meanwhile, US revenues rose 6% in Q4 2025 and accounted for a 47% share of revenues. The company highlighted that one of its priorities for 2025 was working to improve US sales, particularly in its Vehicle Payments and Lodging sections, though these are not the company’s core cross-border segment.

During the earnings call, Clarke mentioned that anything that would roll back or even “fix” tariffs would be a plus to the cross-border business.

How Alpha is driving growth for Corpay

Daniel Webber:

Let’s talk about Alpha. Corpay mentioned in the earnings call that it is already outperforming, and it is only just getting started. What’s come together so quickly there?

Mark Frey:

Certainly our prior experiences have been very helpful in terms of where to target our efforts and where we can get early returns from.

The investment thesis that we had overall is that we could bring size, scale and capability to the Alpha organisation, and that we would be able to accelerate Alpha’s growth given some of the products and services and capabilities that Corpay has.

We’ve been able to help in terms of access to liquidity, payment rails, the jurisdictions that we service and the licences that we have around the world, which have been able to unlock some previous latent capability that existed within Alpha. Also, the private markets capability that Alpha had has allowed our somewhat nascent private markets capability to really accelerate.

With the expertise that we can now leverage on a global basis, we can take that business and expand to the US, Canada, Singapore and Australia with some authority, given our more robust overall human capital footprint. We have really been able to accelerate the growth of what was historically a very European-centric private markets business in Alpha, and now take it to other geographies and leverage their expertise in these other markets.

The early returns have been slightly more positive than what we expected. We had an ambitious plan and things have gone a little bit ahead of schedule in terms of our ability to build and capture some of those opportunities. The key ideas that we laid out have very much all hit, ultimately, and we’re firing on all cylinders in terms of where we expected to be at this point in the acquisition.

We were able to close a month earlier than what we had anticipated, so that’s allowed us to just go a little bit faster. We had a little bit more time in Q4 last year to do the planning and get organised from a people perspective, which has allowed us to get into 2026 and really be in execution mode rather than still planning.

We’ve been very encouraged by the quality of the people within the Alpha business and by the capabilities that we can resell across Corpay. The core thesis – that Alpha was effectively a subscale provider in the marketplace, and that the resources and capabilities that Corpay could bring to the equation would really help accelerate Alpha’s own growth – has definitely proven to be the case, and we’re going to lean into that very heavily over the coming quarters.

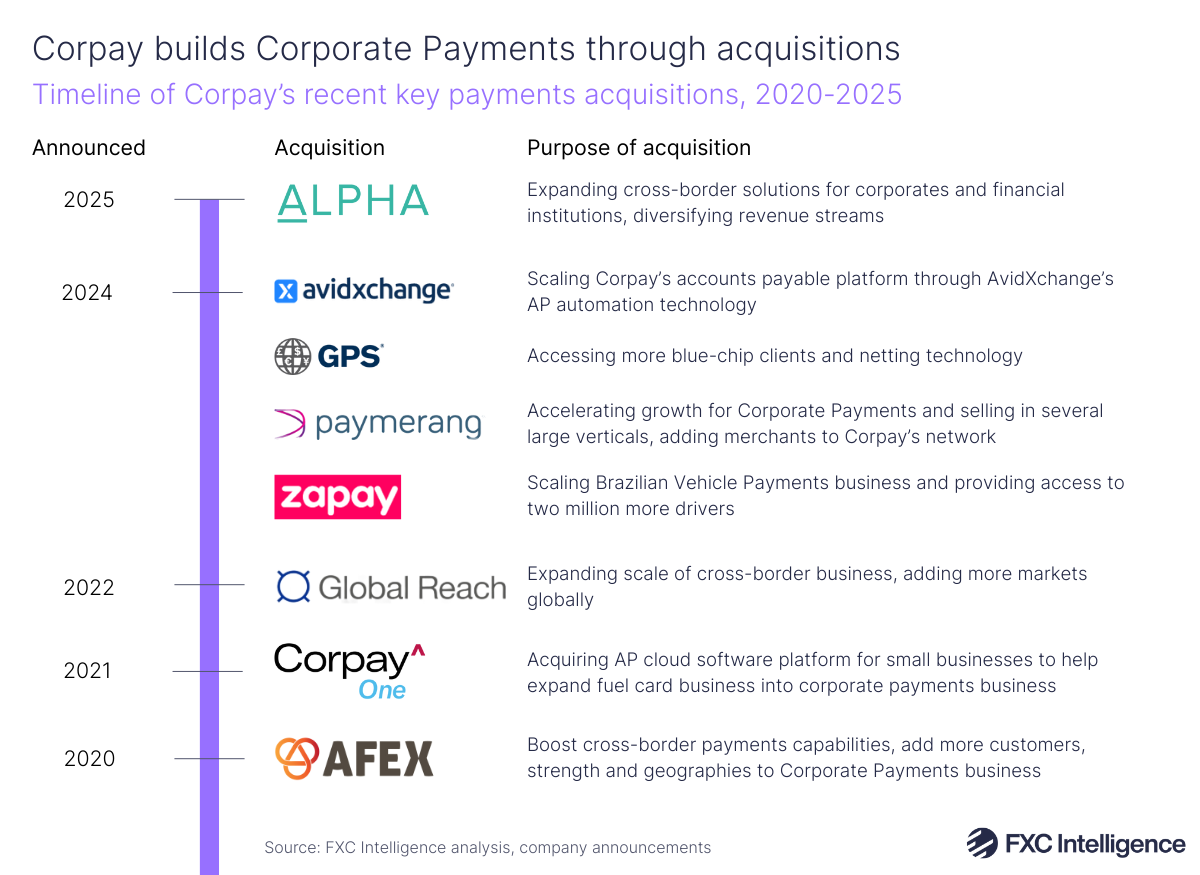

Corpay builds Corporate Payments through acquisitions

With Alpha, Corpay has continued a trend of expanding its Corporate Payment business through acquisitions. The Alpha acquisition is expected to significantly grow its opportunities in the US, Europe and Asia.

Earlier in Q4, Corpay also closed its acquisition of AP automation software provider AvidXchange, which in tandem with Alpha is expected to add approximately $1 of cash earnings per share to its 2026 outlook.

Based on results shared in Corpay’s earnings, core growth accounted for $115m of the $214m YoY rise in revenue in Q4 2025. Meanwhile, acquisitions – based on 2024 proforma revenue of Alpha of $45m, B2B payments provider GPS of $17m and mobile payments provider Gringo of $8m – accounted for $70m of the rise. Positive impacts from exchange rates delivered $36m of the revenue increase, with divestitures subtracting $7m.

How Mastercard is accelerating Corpay’s sales process

Daniel Webber:

Can you provide some more colour on your relationship with Mastercard?

Mark Frey:

Mastercard has gone very, very well. We have enough experience in selling to financial institutions, both Tier 1 global money centre banks and Tier 4 or 5 regional specialists, to know that there’s typically a much longer, multifaceted sales cycle where you’re selling to the treasury and the transactional banking component of a financial institution, but you still have all of the information security, IT issues and overall compliance due diligence that you need to get through as part of the sales process.

Mastercard has helped us accelerate that overall sales process. What we’re seeing is that opportunities are progressing through the pipeline much quicker than they normally do with the support and the relationships that Mastercard can introduce us to.

We’ve also been able to work very closely with the team at Mastercard that’s focused on providing these introductions to us, and to really focus on finding the right fit from the thousands of financial institutions that exist within Mastercard’s networks, [identifying] where we want to focus and where we can add value quickly, and also having an open dialogue where we know those banks are ready to buy.

It’s quite surprising that just a few months in, we’ve got a couple of material closes already and customers now are getting to scale. The pipeline has evolved and developed quite a bit faster than we had originally anticipated. We thought it would be a bit more of a slow burn to get those introductions off the ground and go through the process of discovery with each of these financial institutions. We’re finding that appetite is a little bit more robust for our services than perhaps we forecast.

Mastercard has been a very effective partner at providing introductions and co-selling with us, and we’re running quite a bit ahead of schedule. We’re starting to take what was a very cautiously optimistic view of the relationship and be a little bit more bullish. We think there’s a lot of upside to this business in a sector that we know we play well in, but now [we have] a partner that can just connect us with the right individual within the financial institution.

Corporate payments grows share of Corpay’s revenues

Corpay continues its shift to centre Corporate Payments as it grabs a higher share of the company’s overall revenues. In Q4 2025, the segment once again exceeded growth across the company’s Vehicle Payments and Other segments, while Lodging saw a 7% decline. With a 39% share of Q4 2025 revenue, up from 33% in Q4 2024, Corporate Payments is getting closer to surpassing the company’s largest segment, Vehicle Payments, which accounted for 46% of revenue in Q4 2025.

Corpay pushes to target international banks

Daniel Webber:

How is your international bank account strategy evolving now?

Mark Frey:

Looking at the US and continental Europe, once you get into Tier 3 and 4 regional players, there are many banks that quite frankly just do not have international treasury capabilities.

They have reduced capacity to access in-country rails, move money for customers and provide FX liquidity at scale, and we see that this is just a really good natural extension of the franchise that we built over time. Our initial success that we have had servicing Tier 1 financial institutions in emerging markets has set us up very well to accelerate that growth amongst a much larger target set in the Tiers 2-5 segment of the marketplace. This is a very target-rich market.

The Tier 1 money centre banks have begun to pull back from correspondent banking, in some cases due to risk appetite, but more so because of operational scale and the inability to deliver services to a much smaller financial institution and the ability to deploy technology solutions.

So, a big part of what we do is provide a white-label solution that becomes the transaction banking platform for customers that want to do international business in these smaller financial institutions. That technology footprint allows us to go faster because it cuts the time to market and the time required to deploy a solution for the financial institution.

We’re finding that that mix of capability, international reach, the jurisdictions that we can service and the technology platform that we have is [attractive] for financial institutions that are really looking to better commercialise their existing corporate customers, and the international business that they’re conducting. It also helps these financial institutions defend their clients against the larger Tier 1 financial institutions.

Really, a big part of the value proposition is that if you have a $500m-turnover corporate that is banking with a Tier 3 financial institution, and is doing significant quantums of international business, there’s risk at some point that that business walks out the door and goes to a J.P. Morgan, BofA, Wells Fargo, a Citibank or a Barclays. What we’re finding is we can help them better defend those customers and better commercialise them versus their traditional value proposition.

Daniel Webber:

And the go-to-market there is to provide the platform for the banks. The bank retains the customer and uses you to effectively give all the capabilities behind that.

Mark Frey:

Yeah, it’s two parts. It’s being a traditional correspondent, if you will, that’s moving the money, but it’s providing the customer-facing platform that allows them to do the FX and the cross-border payments at scale.

Corpay’s stablecoins strategy

Daniel Webber:

Where are you using stablecoins, and what are customers asking you about it?

Mark Frey:

Customers don’t come to us and say, ”hey, can I make a stablecoin payment?” They come to us with problems, and then we use our various assets to solve those problems. The problem case that we’re typically using digital payments for, whether it be stablecoins or blockchain, is the always-on, 24/7 payment.

For example, someone needs to move pounds out of the UK to acquire liquidity in the US after the pound sterling cut off. They can’t move it via Swift and they want to do it late on a Friday evening East Coast time, or they want to do it on a Saturday. We’re able to provide that on-chain FX liquidity and be able to move money for them through digital channels. That’s the most compelling use case that we’ve seen.

The promise of stablecoin and digital transactions is that they’re cheap or free. They’re not really that free. They’re definitely not that cheap compared to very effective fiat rails. [Another promise is] that they’re instantaneous. We have lots of means by which we can move payments on a real-time basis. We can credit liquidity around the world in 30 seconds less than a number of markets using our real-time routes.

The thing that we are really able to solve with stable and or digital payments in blockchain is the always-on 24/7, to be able to move money after hours on the weekends. That is the problem that this set of solutions really begins to open up opportunities within, and that’s where we’re leaning into.

Daniel Webber:

What proportion of payments are you now pushing through stablecoins in the back end on the treasury side?

Mark Frey:

Well, it’s still small. I’d say it’s less than 2% of our payments overall. Some of the ticket sizes are particularly compelling. These are not small transactions. These are very large transactions in terms of value, but the payment count is still relatively modest.

Even if we lean into this very heavily, it will never be close to 100%. This will always be a rail category in my view. If I fast forward 10 years, I’m still going to be using Swift for a portion of our business. We’ll be using in-country payments, SEPA or IACH payments in different jurisdictions around the world. We’ll still be leveraging real-time payment rails in a fiat currency.

We’ll be leveraging blockchain, stablecoin and other mechanisms and closed-loop networks to move liquidity as well. Those other capabilities still have natural advantages in terms of cost, scale, liquidity and the ability to reach everywhere in the world ubiquitously. That will be very difficult for digital payment means, whether it be blockchain-enabled or stablecoin-enabled, to compete with for a long period of time.

Adoption is going to take a long time to build, ultimately. And there’s no question in my mind, it will never be anywhere close to 100%.

Daniel Webber:

Mark, thank you.

Mark Frey:

Thank you.