Wero – the European Payments Initiative’s instant payments solution – is seeing growing adoption. What role will it play in Europe’s perceived payments sovereignty challenge, and how might it impact cross-border payments?

The payments landscape in Europe has shifted in recent years, with a significant focus on digital and real-time payments.

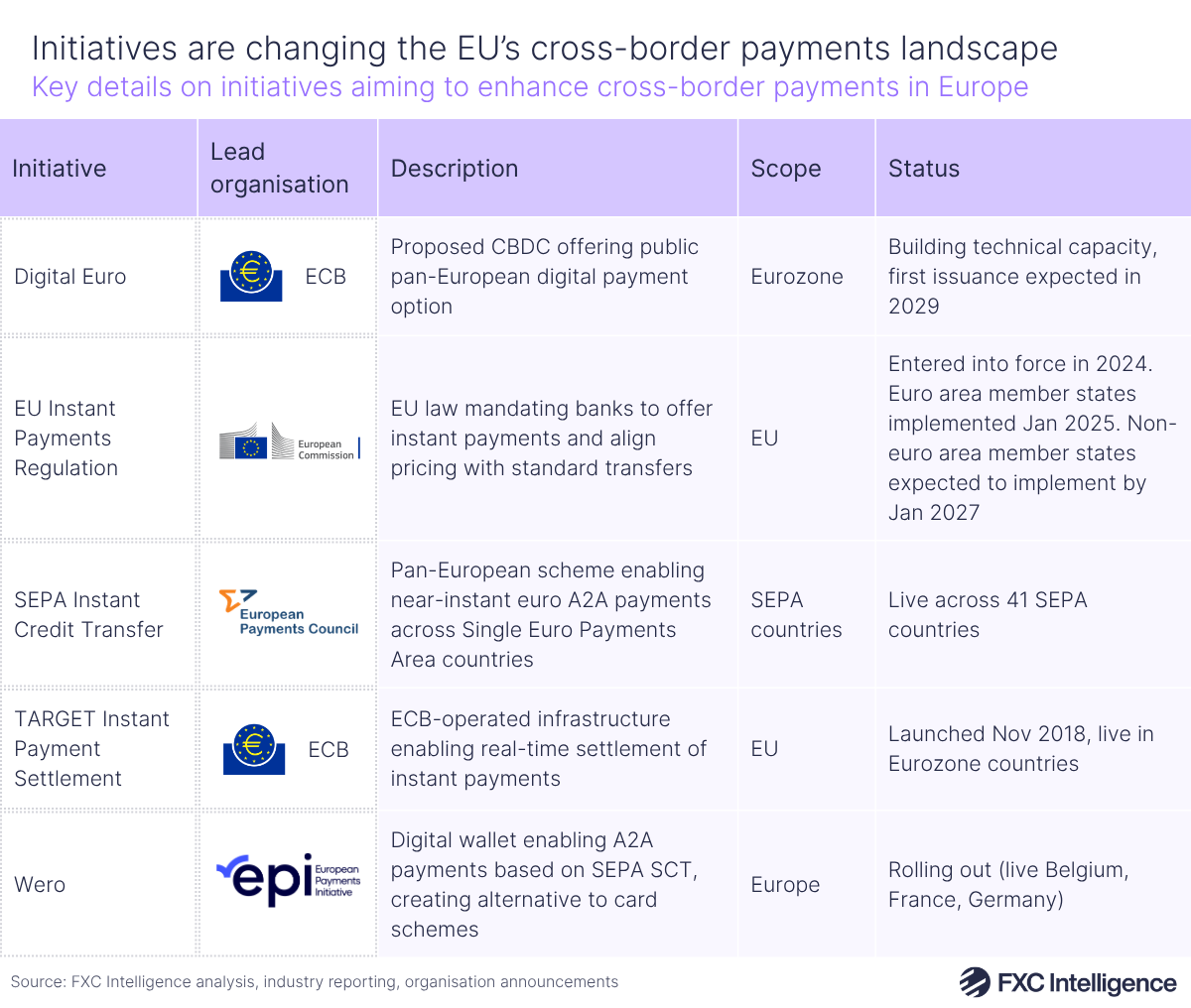

Europe’s central bank and other policymakers have backed new infrastructure schemes to expand the payments ecosystem, such as the SEPA Instant Credit Transfer (SCT Inst) scheme, which now enables near-instant transfers across 41 countries, as well as the TARGET Instant Payment Settlement scheme to settle these payments in central bank money. On the private sector side, players across the payments space have introduced solutions to enable easier, faster and less costly payments for consumers and businesses.

While steps are being taken to unify payments in Europe, the space remains deeply fragmented. Individual countries have different consumer payments habits and have often introduced their own national solutions for payments that aren’t otherwise interoperable. However, European policymakers have also become increasingly concerned about the prominence of non-European card networks within the continent and the extent to which they are able to maintain control over the systems that enable consumers to make payments.

Europe’s sovereignty over payment systems has been a subject of debate and discussion amongst those in the industry and has been a key motivator for European policymakers’ backing of Wero: a pan-European instant account-to-account (A2A) payment system enabling users to send and receive money between bank accounts in under 10 seconds.

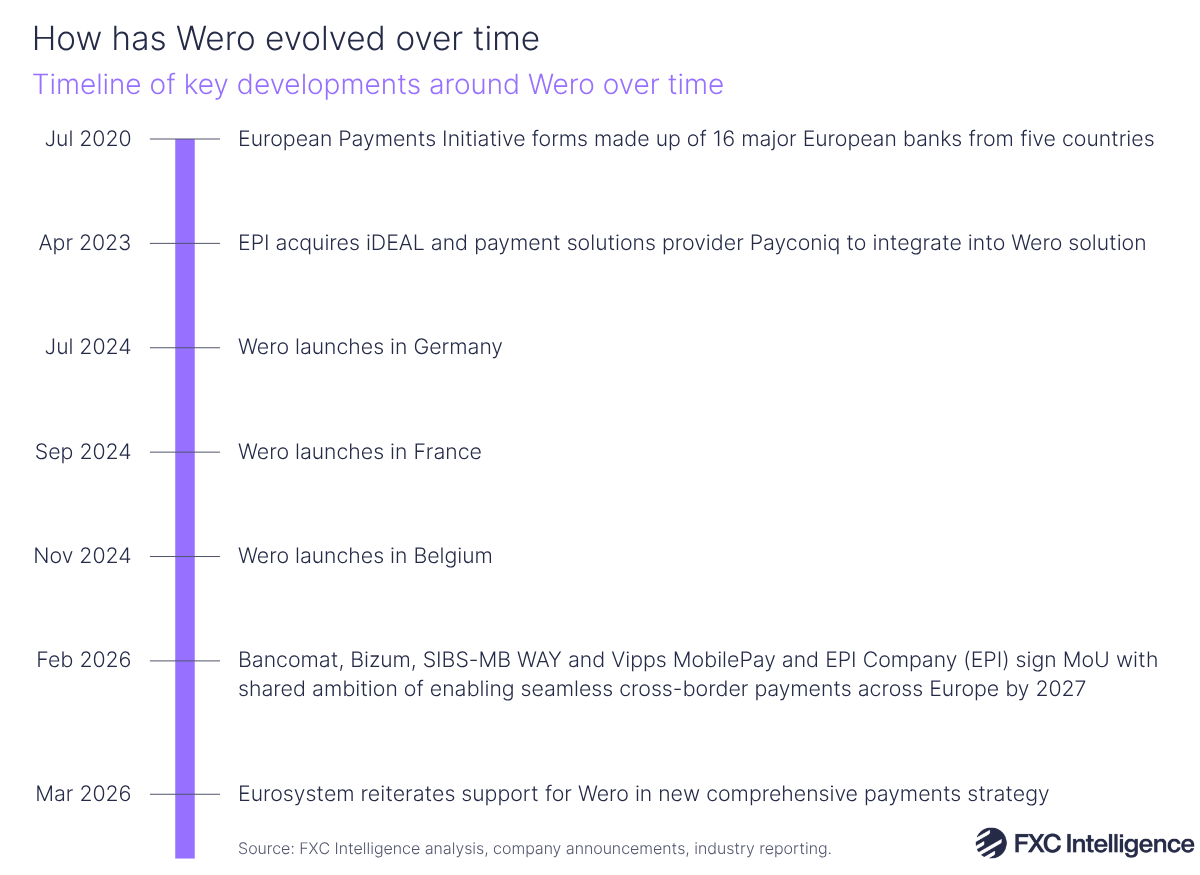

Wero is being developed by the European Payments Initiative (EPI), a consortium of 16 European banks and payment service providers, and has received support from the Eurosystem, comprising the European Central Bank (ECB) and central banks across euro-using countries. Initially launched in 2024, Wero has received scepticism from some commentators, but remains a continued discussion point in the industry as Europe continues to push to unify payments.

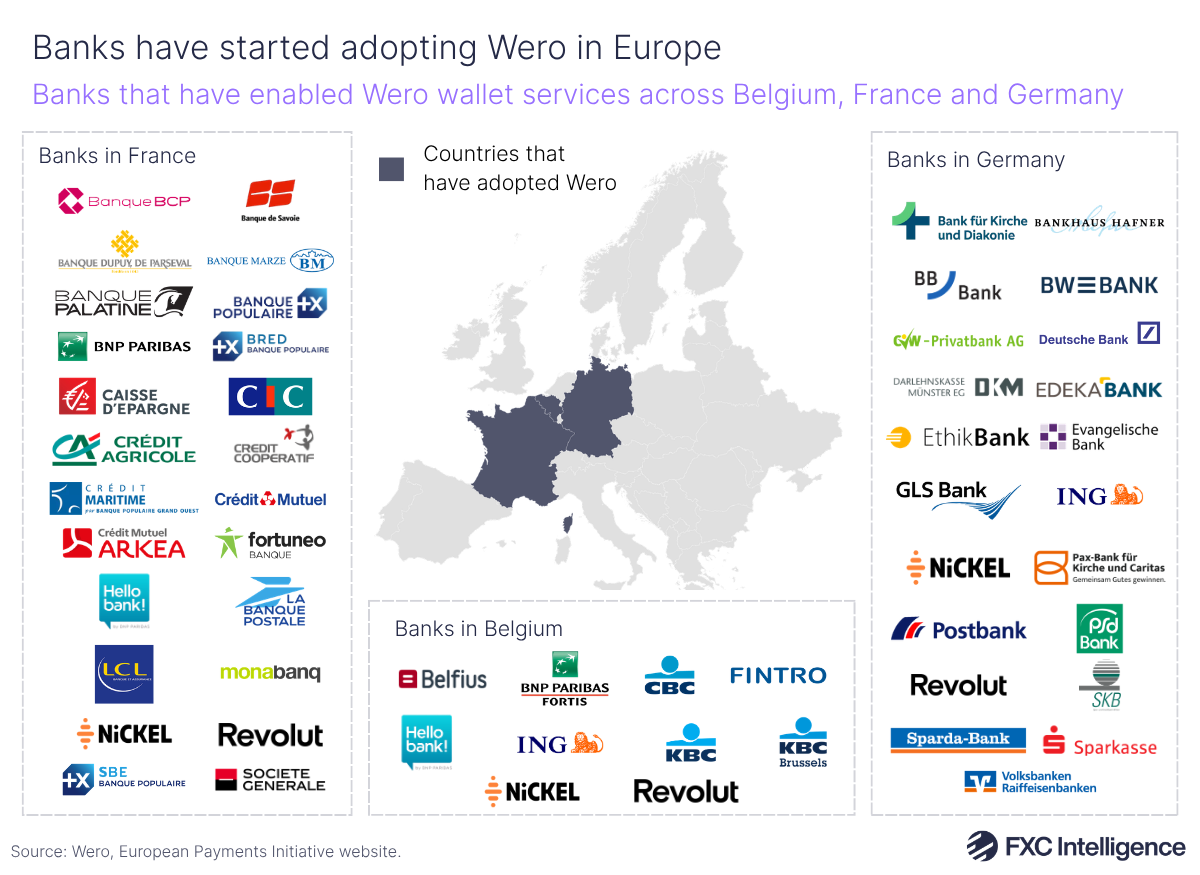

In February, EPI signed an agreement to connect Wero with the European Payments Alliance (EuroPA) – represented by four other European national systems – with the ultimate goal of enabling seamless cross-border payments across Europe by 2027. Currently, Wero is available for P2P payments in Germany, France and Belgium, and can be used by customers at over 50 banks across those countries. Wero is accepted for online payments in Germany and Belgium, and this is expected to extend to France this year, while features are also expected to expand to Luxembourg and the Netherlands in 2026.

In this report, we explore the extent of Europe’s payments sovereignty challenge and Wero’s potential role within it, as well as its current adoption and how this could all impact cross-border payments. To find out more, we spoke to Ludovic Francesconi, Chief Member and Strategy Officer at EPI.

What is Europe’s payments sovereignty challenge?

European policymakers have become increasingly concerned about the region’s dependence on payment systems that are built, run and operated outside of Europe, and particularly the level of control they can therefore exert over the payments consumers need to be able to make every day.

These concerns spiked when Russia was disconnected from international card networks following its invasion of Ukraine, and have continued this year over reported fears from payments leaders that US President Donald Trump could potentially block Europe from accessing US payments infrastructure. Another aspect has been the fees and transaction data that non-European card networks are able to accrue from payments in the region.

Policymakers and European banks have increasingly spoken about the importance of payments sovereignty – the concept of European banks and governments establishing their own independent, secure and home-grown digital payment infrastructures. The goal of many EU-focused initiatives has been to reduce reliance on international card schemes for key use cases, including cross-border and ecommerce payments.

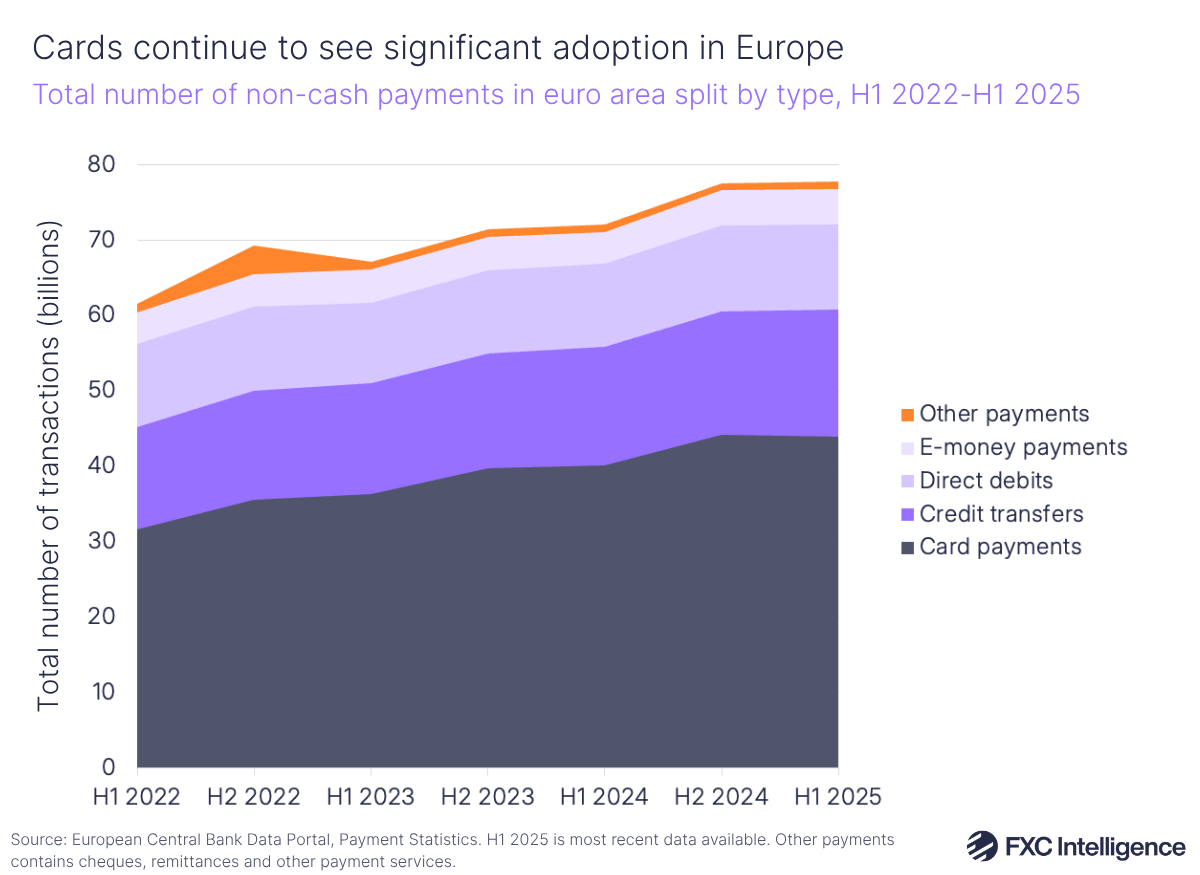

Cards are deeply rooted within Europe’s consumer payment landscape, and are only becoming more so as digital transactions continue to grow. The euro area’s total non-cash payments rose 7.7% YoY to 77.7 billion in H1 2025, according to data published by the ECB in January 2026, with the total transaction value rising by 2.9% to €116tn.

Of these transactions, card payments accounted for 57% of all transactions, versus 22% for credit transfers, 14% for direct debits and 6% for e-money payments. The number of payment cards in circulation at the end of H1 2025 rose by 12% to 879.3 million, averaging 2.5 payment cards per euro area inhabitant.

Where Europe’s policymakers are concerned is the share of card payments taken up by non-European card schemes. Piero Cipollone, Member of the Executive Board of the ECB, stated in a February 2026 speech that international card schemes account for two-thirds of card transactions in the Euro area, with 13 out of 21 euro area countries not having access to a domestic card scheme.

“Currently, card-based payments providers have high control over the transactions as they have been able to implement a cross-border monopoly over the past decades,” Francesconi explains. “That enabled them to set their own tariffs with high margins.”

In addition to concerns about other countries, in particular the US, being able to shut off or otherwise control key parts of payments in Europe, Europe’s central bank claims that banks in the region are losing fees to international card schemes, making it harder for them to compete effectively in the market and resulting in foreign players having increasing control over European transaction data. It has also raised concerns around the potential of US dollar-backed stablecoins replacing the euro in digital transactions, in turn limiting the ECB’s monetary policy control over those payments.

“We can no longer afford to rely mainly on foreign solutions for a matter as critical as daily payment,” said Cipollone in his speech. “If Europeans can no longer pay, they are no longer in control of their money. And the economy is exposed to grinding to a halt suddenly. Even without reaching this point, such a dependency could be used as leverage against Europe’s interests.”

Sovereignty and avoiding a potential shutdown have been key motivators for Wero, which EPI says “answers the need” for a sovereign European cross-border payment system. “After the Covid pandemic and the first lockdowns, we became convinced that sovereignty would become increasingly important in the European landscape and in the hearts of the citizens of Europe,” says Francesconi. “Wero embodies this alternative vision, positioning itself as a truly pan-European solution, helping avoid the risk of a shutdown.”

Has Europe’s payments sovereignty challenge been overstated?

European policymakers and banks have pitched foreign dependency as being a key motivator behind many of the ongoing schemes trying to unify payments in the region. However, the question of whether Europe has a payments sovereignty issue, and to what extent, is politically driven and some commentators have criticised the way it has been framed in the media, while others have said issues of dependency are being overstated.

Some commentators say that the idea of sovereignty is largely focusing on the card scheme and rail layer of payments, at which non-European companies dominate. However, payments actually consists of multiple layers, including processing and acquiring, digital wallets and A2A services, which are sometimes conflated in discussions around sovereignty.

For example, a policy briefing from Belgian think tank CEPS argues that a significant portion of processing is handled by European companies, such as Worldline, Nexi, Nets and Stripe. Digital wallets such as Apple Pay are sometimes mentioned in sovereignty discussions but are largely interface layers sitting on top of existing payments infrastructure. While they may compete with other digital wallets on the front end of transactions, they don’t ultimately determine how transactions are processed or settled. The same is true for A2A overlays, which aside from Wero include Bizum in Spain, iDEAL in the Netherlands, Swish in Sweden, Blik in Poland, MB WAY in Portugal, Vipps MobilePay in Nordic countries and Bancomat Pay in Italy.

Meanwhile, a piece from the Information Technology & Innovation Foundation (ITIF), a US-based research institution, argues that there are regulations in place already to ensure pricing competition in the European market. Under the Interchange Fee Regulation (IFR), interchange fees in the EU are capped at 0.2% for consumer debit transactions and 0.3% for consumer credit transactions. Separately, the EU’s Payment Services Directive (PSD2) requires banks to allow third-party payment providers to access customer accounts, which gives the customers the ability to transfer directly between bank accounts without using card networks.

There has also been scepticism levelled at the idea that US card networks would actually block or otherwise restrict access to payments in Europe, for example in response to a geopolitical event, given that Europe remains critical to US card companies’ earnings. For example, Visa saw just under $3tn, or 21% of its total payment volume, coming from Europe in its FY 2025 (spanning the year-long period ending in calendar Q3 2025), while Mastercard saw $3tn of purchase volume (specifically related to Mastercard-branded cards), or around 34% of its volumes.

Some commentators have argued that the significance that Europe has had for these businesses, as well as the resulting impact it would likely have on US financial institutions and the US economy, makes it unlikely that they would block payments in the region.

On EPI’s side, it maintains that applying regulations will not solve challenges that exist around European payments sovereignty, and that limiting foreign providers in Europe is required to open up space in the market for applying regulations. “Local champions also need to appear to contest existing actors,” says Francesconi. “Which is why solutions like Wero are necessary.”

How has Wero evolved over time?

In effect, Wero is an A2A solution running on Europe’s existing SEPA scheme to enable fast P2P and ecommerce payments. Customers with accounts at banks that have adopted Wero are able to download Wero as an app and use it as a payment or money transfers solution linked with their account to send money to other Wero users instantly and securely.

Merchants are able to accept payments through Wero via an acquirer, similar to other payment methods, with pricing set at a small percentage fee with built-in caps. The system is designed to avoid interchange fees being charged by card networks, therefore allowing for more competitive pricing. In this sense, it supports the drive towards payments sovereignty by bringing consumers into a system where pricing and payments infrastructure is controlled by European banks and acquirers.

“Wero is reducing costs for merchants by providing them a locally made infrastructure that works along local PSPs, therefore mechanically reducing costs,” explains Francesconi.

While Wero’s initial focus was on P2P payments, it is gradually evolving to enable ecommerce and PoS purchases. This is set to be followed by other value-added services, such as BNPL options offered by banks, digital ID verification and merchant loyalty programs. Ultimately, the goal is to focus on intra-European cross-border payments, with a goal of reducing the need for multiple local payment methods across markets.

“For merchants, online payments are deploying now with the first strategic agreements signed and in-store rollout imminent, supported by our fully cloud-native, API-based infrastructure for easy integration and future additions of subscriptions and loyalty programmes,” explains Francesconi.

Wero launched in July 2024 in Germany, followed by France in September and Belgium in November of that year. This came the year after EPI acquired iDEAL, the Netherlands-based scheme that has become the leading online payments method in the country, as well as Luxembourg’s Payconiq to help it develop its new pan-European platform.

The system has grown its adoption over time, and is currently supported by over 50 banks across the three countries it serves, including major banks such as BNP Paribas and ING and neobanks such as Revolut. It is expected to expand into the Netherlands and Luxembourg in 2026. As well as being backed by 16 major European banks, Wero also has the support of over 1,100 active members, spanning banks, acquirers and payment service providers.

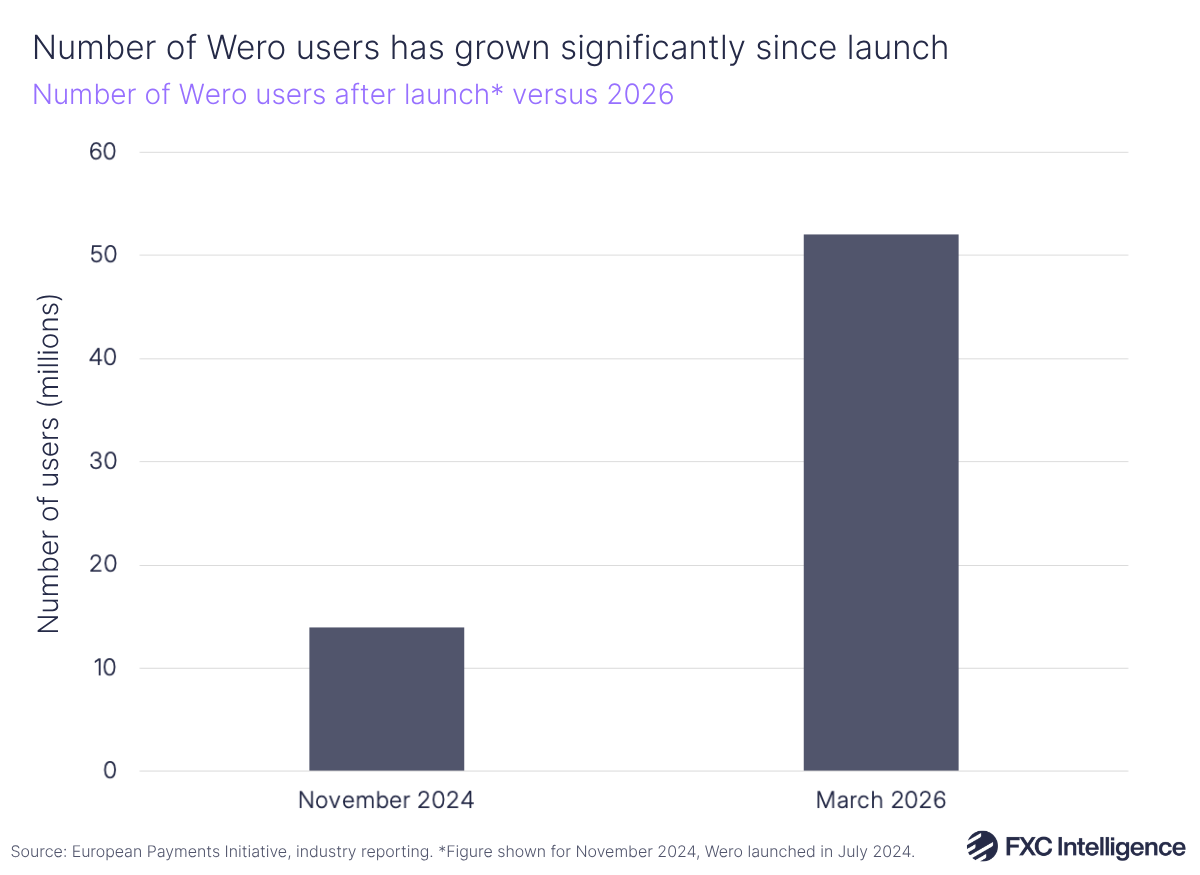

Wero has also seen significant uptick in adoption, having reached 53 million registered users as of March 2026. BNP Paribas reported that in its first year, Wero saw over 100 million transactions, with a total amount transferred of €5bn. These figures highlight strong growth, though Wero is still accounting for only a small fraction of the billions of transactions, worth trillions of Euros, happening across the continent.

The ultimate goal over the next two to three years, EPI says, will be to become a scalable network, with Austria and potentially other markets coming next thanks to a growing coalition of banks and payment providers. “In addition to this, our partnership with members of the EuroPA alliance will enable us to connect directly or indirectly with most of the banked consumers by 2027,” says Francesconi.

How has the payments industry responded to Wero?

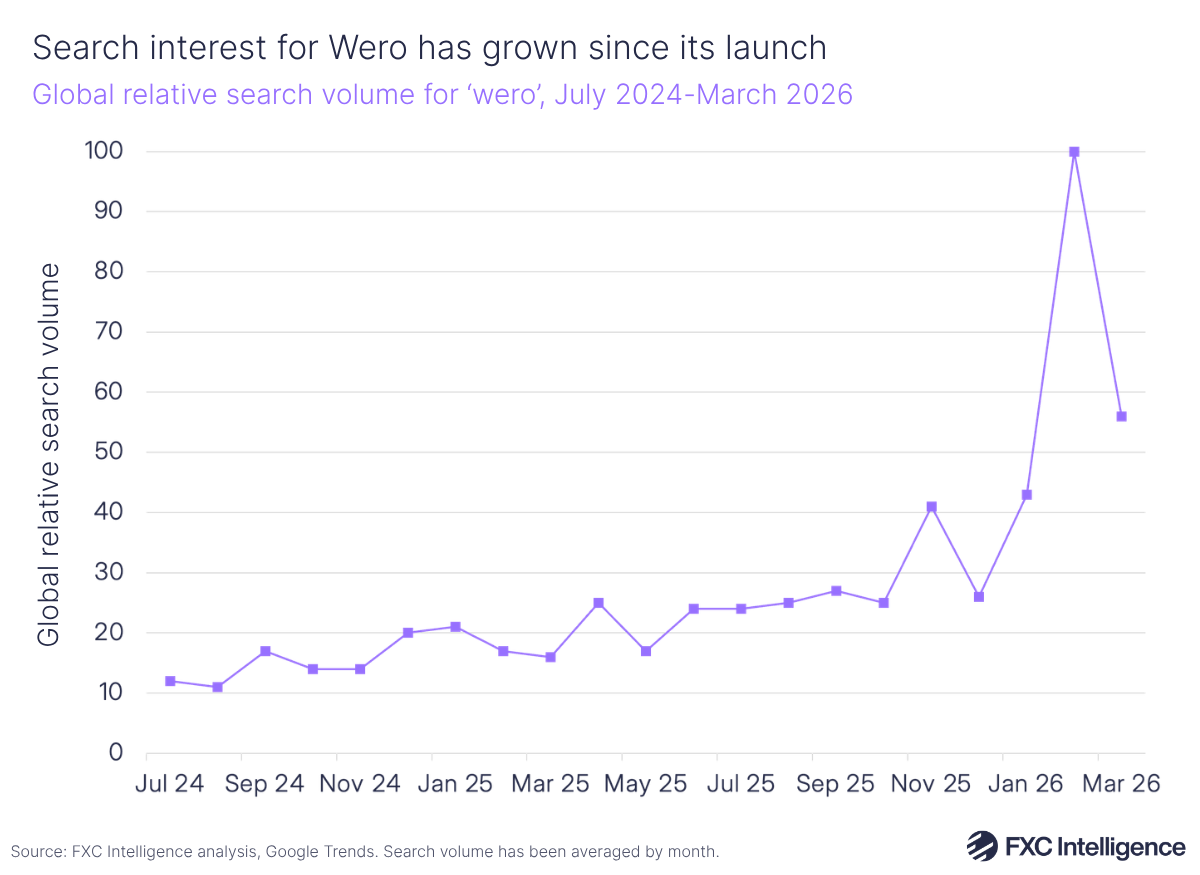

Nevertheless, the industry has increasingly been discussing and engaging with Wero, highlighted by growing search interest online. Google Trends data measures how popular a search term is compared to its own peak popularity over a given time. Spanning the period from Wero’s launch in July 2024 to March 2026, search volume for the term ‘Wero’ was relatively low in the months after its launch but rose in 2025 and peaked in February 2026.

This spike in global search interest aligns with growing media discussion of Wero in alignment with several key developments, in particular EPI signing a memorandum of understanding with members of the EuroPA Alliance to enable interoperability between payments systems in Europe. Having said this, a significant amount of the interest here is forward-looking – Wero is still an early-stage solution, but its role in the conversation around Europe’s payments sovereignty, as well as other initiatives being introduced in Europe such as the digital euro, are driving growing interest in the industry.

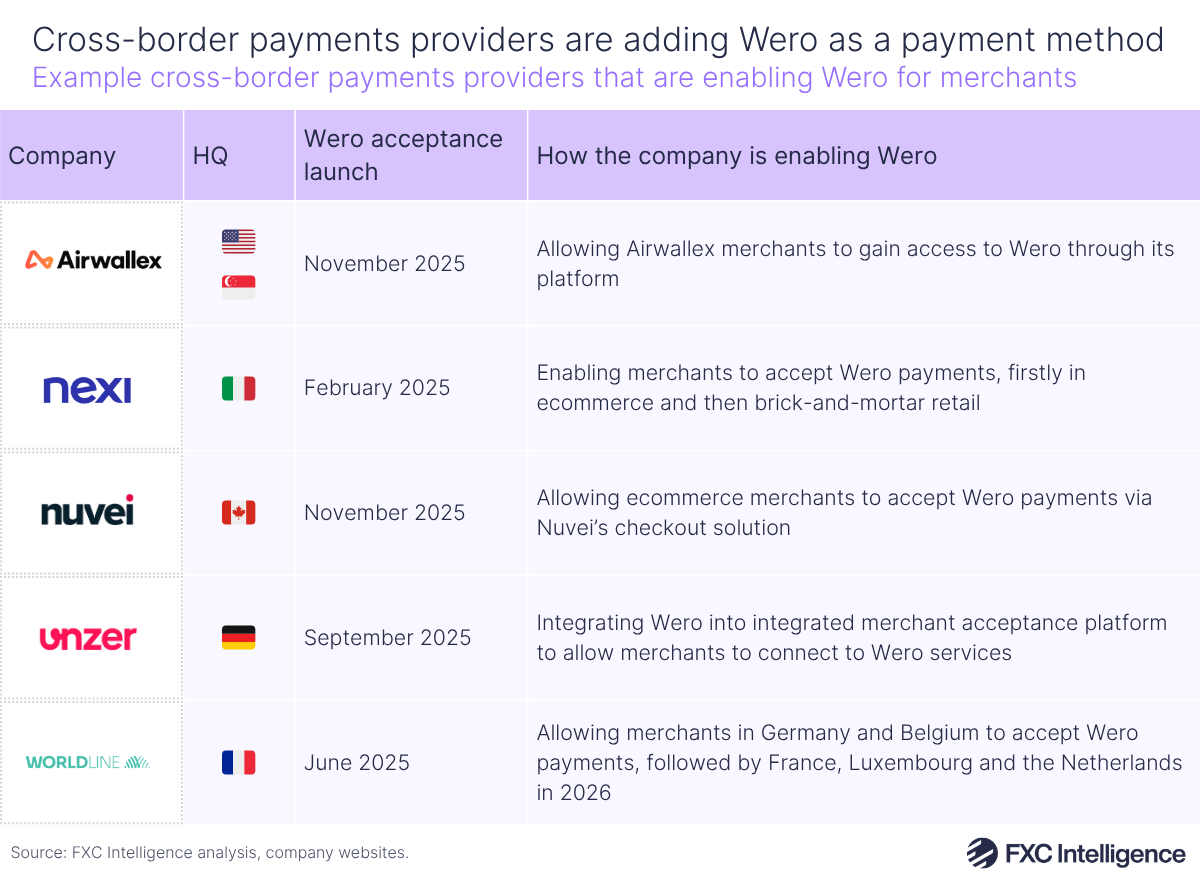

A number of payments companies have already committed to supporting Wero, in particular ensuring that they can connect merchants to the payment method and that it can be used seamlessly across different countries and platforms.

For example Nexi, Nuvei, Unzer, Worldline and Airwallex have all formed partnerships with EPI to enable merchant acceptance of Wero, signalling an interest from payments providers to support the payments method as it comes online.

“Wero represents a major milestone for European commerce – and by offering it directly through our platform, we’re continuing to empower our global customer base and merchants with cutting-edge local payment methods, global multicurrency accounts and embedded financial tools,” said Kai Wu, CRO at Airwallex, in a press release following Airwallex becoming a Principal Member of EPI in November.

Wero in the context of the EU’s broader payments strategy

Wero is a commercial product backed by private European banks, though it has openly received support from the ECB’s Eurosystem and fits into several ongoing initiatives in Europe. In the first case, its growth is intrinsically linked to the continued expansion of SEPA Instant, which has now been mandated by the EU’s Instant Payments Regulation.

Under the regulation, all payment service providers (PSPs) located in euro-using EU member states needed to provide users with the ability to both receive and send instant cross-border credit transfers in euros as of October 2025. For PSPs in member states not using the euro, the deadline for receiving instant euro payments is 9 January 2027, while the deadline for enabling sending instant euro payments is 9 July 2027.

The mandating of instant transfers across the EU aligns with Wero’s growth and adoption, as banks are now required to enable the key instant payments infrastructure on top of which Wero sits as an A2A layer. This could potentially boost the market for Wero to tap into and spur its growth over time.

Another key aspect of Europe’s strategy often linked with payments sovereignty is the digital euro – the proposed central bank digital currency being issued by the ECB, and which has received support from member states across the region.

The ECB aims to introduce a digital euro to essentially ensure that digital payments continue to be rooted in central bank currency as more consumers increasingly switch from cash to digital payments. However, it is also deeply linked to sovereignty, with the EU trying to protect against money being moved across borders via other means, such as through stablecoins introduced by non-European providers or non-European CBDCs.

Following a preparation phase starting in November 2023, the Eurosystem announced in October 2025 that it had moved into a technical preparation phase for the digital euro. However, it is still essentially waiting on legislation to adopt a digital euro. If this happens in 2026, a pilot and initial transactions could take place in mid-2027, with the potential first issuance of the digital euro happening in 2029.

The Eurosystem’s recently published comprehensive payments strategy document highlighted the potential of the digital euro to be co-badged onto physical cards, which would reduce the need to use non-European card schemes for acceptance outside the home country within the euro area. In addition, it says that the digital euro could be hosted next to private sector solutions in multi-bank wallets.

Wero’s link to the digital euro is therefore dependent on its progress, but the key parties involved have historically suggested they could support each other. In an interview with the European Payments Council in December 2024, CEO Martina Weimert said that EPI would be willing to integrate the digital euro to allow consumers to use it as a payment method through the Wero digital wallet.

However, EPI says that the digital euro aims to be both a currency and payment solution, and therefore does “overlap” with the role of a pan-European payment scheme such as Wero with regards to rules, acceptance, user experience, and integration among merchants and PSPs. There is, therefore, a risk of effort being duplicated and “head-on competition” on the payment layer. “According to us, Europe does not need to duplicate; it needs to accelerate and join forces,” says Francesconi.

Why is EPI’s recent alliance with EuroPA significant?

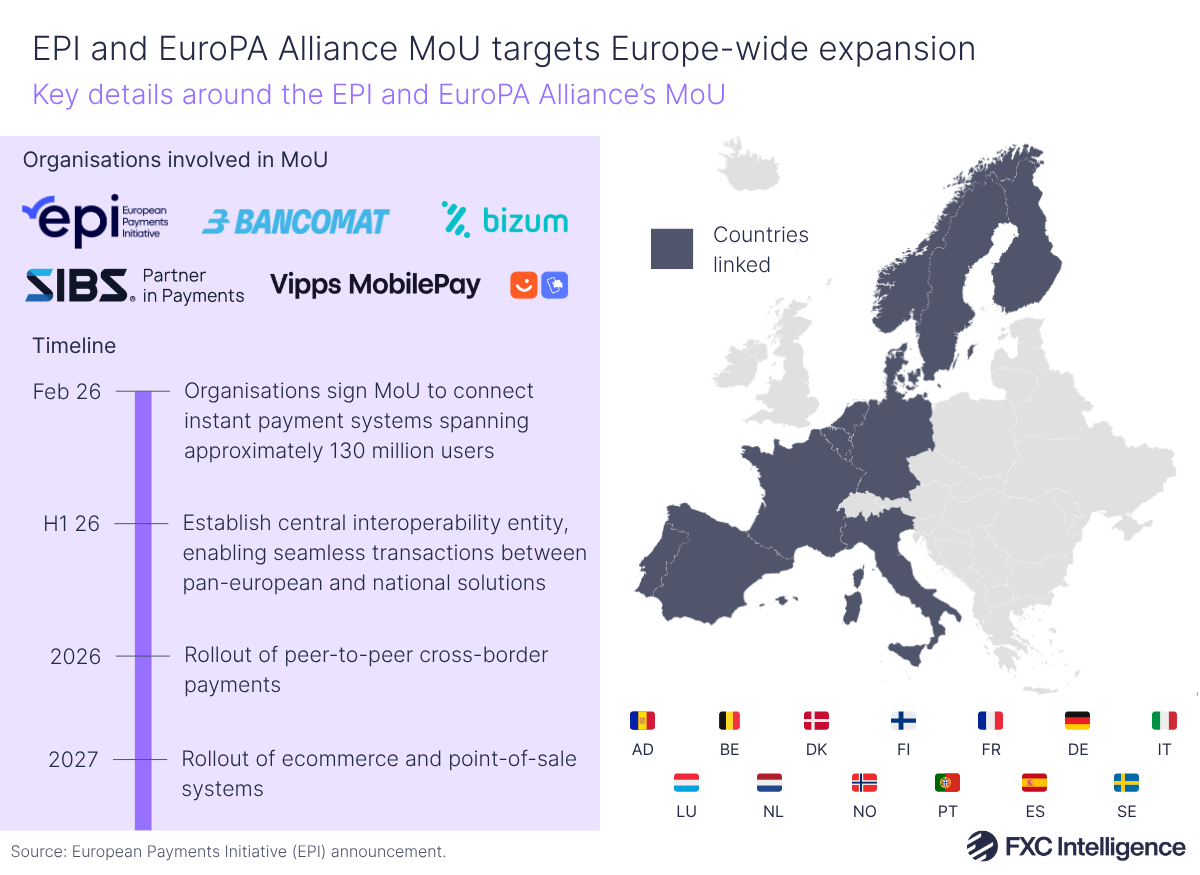

The aforementioned agreement between EPI and several other significant payment systems in Europe essentially shows the next step in a plan to create a “pan-European” solution to cross-border payments in Europe. The key goal of the MoU is to create a central interoperability hub for the different payment systems – initially including Bancomat, Bizum, SIBS-MB Way, Wero and Vipps MobilePay – with this hub acting as a technical layer that enables transactions to flow seamlessly between these different solutions.

As part of the announcement, EPI said that Europe remains highly dependent on non-European players, and that the initiative aims to demonstrate that European banks and PSPs “have both the infrastructure and the scale to deliver a concrete alternative rapidly”.

The initiative currently includes solutions that serve approximately 130 million users spanning 13 European countries, covering around 72% of the EU and Norway’s populations. However, the coalition is open to other European countries, including non-euro markets. Countries that have a domestic payments solutions already can join the coalition, and countries without will be able to implement one of the solutions already available.

“The huge user base of 130 million users immediately creates a very attractive offer for all merchants and consumers operating cross-border,” explains Francesconi. “The launch in 13 countries also means that we are confident enough about cross-border payment schemes.”

The move is significant for Wero in the sense that it quickly connects it to other systems within one layer, and as such could boost its adoption in countries where it is made available. However, it also suggests that EPI is not pitching to take control of the whole European payments landscape in isolation. Instead, it is building interoperability with other already strong payments infrastructures in Europe in order to quickly build up to a more connected system.

While Wero has pursued acquisitions in some markets, it is using collaborations with other systems to quickly build scale as part of a wider interoperability initiative. Building this scale is important to allow the system to compete with other providers already enabling cross-border payments in Europe – but it also suggests that Wero is just one part of Europe’s perceived payments sovereignty challenge, rather than being the key component on its own.

“Over half of European member states have no alternatives to non-European payment providers,” says Francesconi. “Those that have an alternative used to be isolated from one another. Hence the path for Wero was laid out from the beginning: cooperation where it is possible and offering a sovereign European alternative to international solutions.

“The coalition is open to all European countries and solutions, and other markets outside the Eurozone: markets that have already developed a national solution can join directly, while those wishing to join that do not have a national solution can implement one of the solutions already available within the initiative.”

Challenges to Wero’s success

Europe has previously tried to introduce pan-European solutions to compete against international card competitors. For example, the Monnet Project was a scheme launched by a group of European banks in 2008 to create a unified pan-European card scheme for payments. Despite receiving support from the European Central Bank, the project fell apart after a key failure to align on card interchange fees across banks operating in different regions.

While this scheme tried to create a viable card alternative, Wero is approaching the problem from an account-to-account standpoint, thereby trying to encourage consumers to route payments through European payments infrastructure and therefore remove card intermediaries altogether. However, the key issue here is how Wero can effectively encourage users to adopt a new payment method that is more convenient and cost-effective than cards.

In Europe, consumers and merchants already use and accept card payments every day, and so a new payment method will need to offer significant incentive or reason to encourage better adoption across the network. From the consumer’s perspective, Wero needs to be as easy to use to make payments and send money across borders as current payment methods.

EPI says that the key challenges for Wero are user adoption, merchant acceptance and seamless cross-border interoperability, but it says these are not “structural risks”.

“On adoption, the key is delivering a product that’s simple, reliable and clearly differentiated from existing options,” says Francesconi. “That’s why we’re rolling out progressively with strong banking partners to ensure immediate reach and trust.

“On merchant acceptance, we’re working closely with partners to make integration as frictionless as possible, while ensuring a compelling value proposition compared to existing schemes. Finally, interoperability across European markets is complex by nature, given regulatory and technical diversity. We’re addressing this through a unified infrastructure and close coordination with participating institutions.”

Looking at the cross-border side, as an A2A layer based on SEPA infrastructure, Wero is specifically focused on European countries, with payments specifically operating in this region for the foreseeable future. However, European businesses sell to consumers from around the world and Europeans’ own need to make payments to other countries. This means that, even if Wero broadens its customer base, international cards that are accepted globally will continue to be incredibly important to consumers in Europe, as Wero payments for the meantime won’t be accepted in other countries.

That being said, EPI says that it may collaborate with markets outside the eurozone in the future if the desire exists. “Wero is first intended to offer a credible, sovereign and competitive European alternative, adapted to local and cross-border needs,” explains Francesconi. “However, if any other market outside the eurozone without a local solution is willing to cooperate with Wero, just like the EuroPA coalition, then we are open to expansion beyond Europe. All the more, we are looking in the long term at supporting our consumers beyond the frontiers of Europe in their travelling around the world.”

From the merchant’s perspective, consumer’s adopting the method en-masse is critical, but Wero also needs to be cost-effective and at least as convenient to add as a payment solution to other methods. Related to this, commentators in the space have also argued that there currently exists a lack of clarity about chargebacks and dispute resolution for customers making payments through Wero, which could result in additional costs for merchants.

Currently, Wero allows for payments to be reclaimed after transactions have been completed, which strengthens protection for consumers, but some have argued it also introduces uncertainty for merchants and payment service providers enabling the payment method. For example, it could lead to additional administration/customer service costs for merchants around the process of enabling chargebacks; uncertainty over cash flow, as chargebacks could occur weeks after payments are made; and PSPs being more strict about the merchants for which they are willing to enable Wero payments.

Ultimately, Wero has seen initial momentum and its backing from European payments leaders, banks and PSPs in the regions reflects a will from the industry to continue pushing it forward. However, its ultimate success is based on a number of factors that will drive a network effect amongst consumers, merchants and banks.