FXC Intelligence has launched the industry’s most comprehensive guide to the stablecoin payments infrastructure buying process: FXC Buyer’s Guide: Stablecoin Payments Infrastructure. This definitive resource draws on a decade of cross-border expertise, alongside in-depth interviews with buyers, deep research and vendor-supplied data to provide strategic guidance for payment companies, governments, corporates, investors, banks and NGOs. Below is the full executive summary, and you can learn more about subscribing to unlock the full Buyer’s Guide on our product page.

Executive summary

FXC Intelligence is the leading data and intelligence company for cross-border payments, having spent the last 10 years developing datasets in the fiat and digital asset market and working with many of the leading players. This unique combination of expertise across cross-border payments and digital assets has led us to launch this guide to serve as the definitive source for organisations for whom cross-border payments are important and that are now exploring the potential that stablecoins can offer.

Over the past 18 months, the cross-border payment industry has undergone a significant shift with regards to stablecoins. Organisations across the industry have engaged with the technology, and many have begun to transition from experimental pilots to utility-driven deployment. However, adopting stablecoin payments, whether for internal treasury, external recipients or as part of the delivery of services for end users, requires companies to engage with an entirely new infrastructure stack. With this not only comes a different technological landscape, but also different vendors, standards and norms to negotiate.

Organisations are faced with the challenge of building their expertise in the area from the ground up and making decisions that meet their needs at a time when the industry is maturing rapidly, and where they do not have a complete picture of the complexities and pitfalls of the sector.

This guide provides detailed, strategic information for financial institutions, payments companies, governments, corporates, investors and NGOs who are exploring or engaging with the buying process. It can also help support investors looking to analyse the sector and conduct due diligence on the market; to enable governments, regulators and NGOs to better understand the sector as they develop policy; and to help train and upskill payment teams on stablecoins, providing the context and depth not available in public sources, including AI.

Built on highly granular in-depth research, interviews with buyers and both independently collected and vendor-supplied non-public data, it brings together the full range of need-to-know information on the buying process, including how the technology stack works, effective ways to engage with vendors and exhaustive benchmarking and profiles of leading infrastructure providers, as well as current applications of stablecoins in cross-border payments and regional dives. This has seen us work closely with many of the leading providers to benchmark their capabilities – including by validating data they shared with us that is not available publicly – and also speaking to many buyers around the world, from a wide variety of institutions, to understand how to help organisations navigate the buying process.

The executive summary is available both as a PDF and in digital form on this page. You can access both after the login below (or by scrolling down if you are already logged in), but if you are from a bank whose internal policies impact your ability to sign up, please email us to request a copy.

The main sections in this guide are as follows:

Stablecoin infrastructure explained

A breakdown of the stablecoin infrastructure stack, exploring how different parts of the technology fit together, from wallet infrastructure to liquidity and the on and off-ramping processes.

The regulatory and compliance landscape

A review of the rapidly evolving regulatory environment globally, including key differences between the US’s GENIUS Act and the EU’s MiCA regulation.

The buying process

A detailed, strategic framework for organisations looking to adopt the technology, including a breakdown of each step in the process and detailed due diligence questions to ask potential vendors.

Positioning matrices

A review of our analysis and benchmarking of leading vendors, including how they compare across different areas and capabilities and how their suitability varies by use case, as well as how they compare for regional coverage.

Provider profiles

Exhaustive, in-depth profiles of each of the 11 vendors focused on in this Buyer’s Guide, including in-depth information about their coverage, product range, strengths and weaknesses.

Emerging solutions for payments

A review of nascent stablecoin payments-related solutions that are gaining interest but are not yet mature enough for exhaustive benchmarking.

In this executive summary, we review the current state of stablecoins’ use in cross-border payments in 2026, including exclusive and newly updated data on the total addressable market for stablecoins, before highlighting some of the top-level takeaways from the wider guide.

Unlock full access to the industry’s most comprehensive guide to stablecoin payments infrastructure

The state of stablecoin payments adoption in 2026

The last year has seen adoption of stablecoins by the payments industry grow dramatically. While in 2024 the technology was largely a fringe element adopted by a small number of specialists, by the end of 2025 FXC Intelligence analysis shows that almost every major company within the sector had either begun to make use of the technology or announced plans to do so.

Though much of the early discussion was focused on ‘stablecoin sandwich’-type applications, where a payment begins and ends in fiat currencies but stablecoin technology is used for the middle part of the transaction, initial adoption has leaned more towards internal treasury applications, with many companies using the technology to reduce the need for large numbers of liquidity pools in different markets and speed up reconciliation and settlement processes.

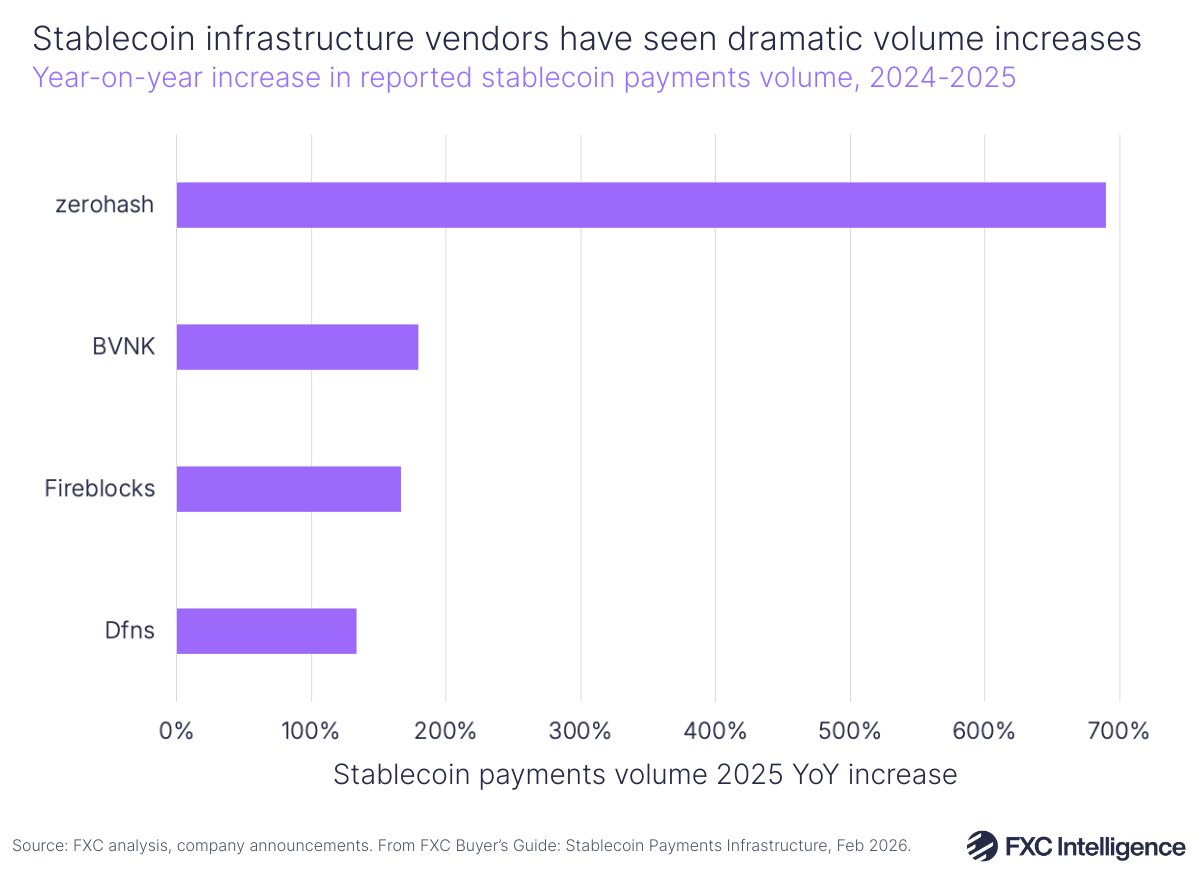

This increased adoption has had a noticeable impact on the wider stablecoin industry. The market capitalisation of stablecoins has surged, with USDC, the second-largest stablecoin by volume globally and the largest that is GENIUS Act-compliant, seeing its total volumes climb by around $20bn between the start of 2025 and the start of 2026, while the number of transactions has also soared. BVNK, a leading provider of stablecoin payments infrastructure solutions, saw its payments volume climb by around 180% YoY to $30bn in 2025, having seen its growth rates accelerate over the preceding few years.

This trend is by no means exclusive to BVNK, however: vendors across the space have seen three-figure growth.

Fireblocks, a provider of self-managed solutions that is widely used across the industry, including by both cross-border payments companies moving into the space and managed providers harnessing the company’s orchestration or wallet capabilities, saw its payments volume climb by more than 160% YoY in 2025, with wallet infrastructure provider Dfns seeing growth topping 130%.

Meanwhile, some previously smaller players saw their volumes surge even further. zerohash, a US-based provider of managed payments solutions, reports seeing active stablecoin usage on its platform climb by 146% YoY and transaction volume grow by 690%.

This is reflected by the fact that many different cross-border payments providers have launched stablecoin solutions. MoneyGram, for example, launched a number of stablecoin-focused products in 2025, including the release of a stablecoin-based app in Colombia and a crypto-to-cash on and off-ramping solution named MoneyGram Ramps.

Cross-border payments network provider Thunes, meanwhile, has announced a variety of stablecoin-based solutions over the last 18 months, including stablecoin payouts and its stablecoin-based Liquidity Management Solution. Others include Worldpay (stablecoin payouts), Remitly (fiat-stablecoin multicurrency wallet) and Zepz (stablecoin-linked cards).

Notably, all of these companies’ stablecoin initiatives have seen them partner with at least two stablecoin infrastructure providers of one form or another, a practice that is widespread across the space. At present, making use of multiple partnerships is highly commonplace within the sector, as companies combine multiple providers to either cover the entire infrastructure stack or ensure sufficient geographic coverage for their needs.

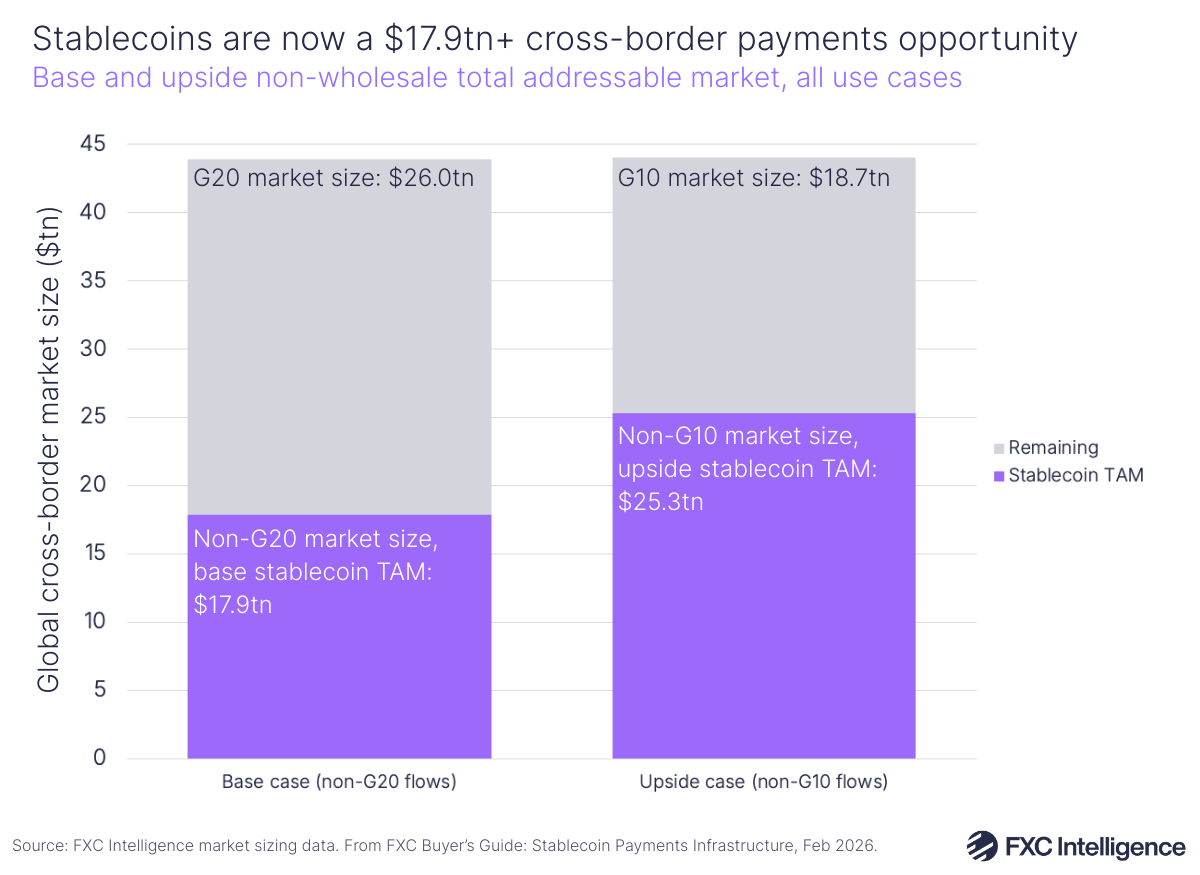

How big is cross-border payments’ total addressable market for stablecoins?

In 2025, we assessed the base total addressable market (TAM) for non-wholesale money movement to be $16.5tn globally, however that has been revised upwards. Today, using new FXC Intelligence market sizing data for 2025, we assess the base stablecoin cross-border payments TAM to be $17.9tn, with the upside TAM now reaching $25.3tn.

This represents a significant share of global non-wholesale cross-border payments volume, which FXC Intelligence market sizing data shows reached $43.9tn in 2025. This covers all non-wholesale applications, sometimes referred to as retail payments, across business-to-business (B2B), consumer-to-business (C2B), business-to-consumer (B2C) and consumer-to-consumer (C2C) payments.

The stablecoin TAM is based on the non-G20 share of total cross-border flows globally for the base case, and the non-G10 share for the upside case, in recognition of stablecoins’ outsized potential for emerging markets payments – something that remains as true today as it was a year ago, and which is likely to continue to be so for the foreseeable future.

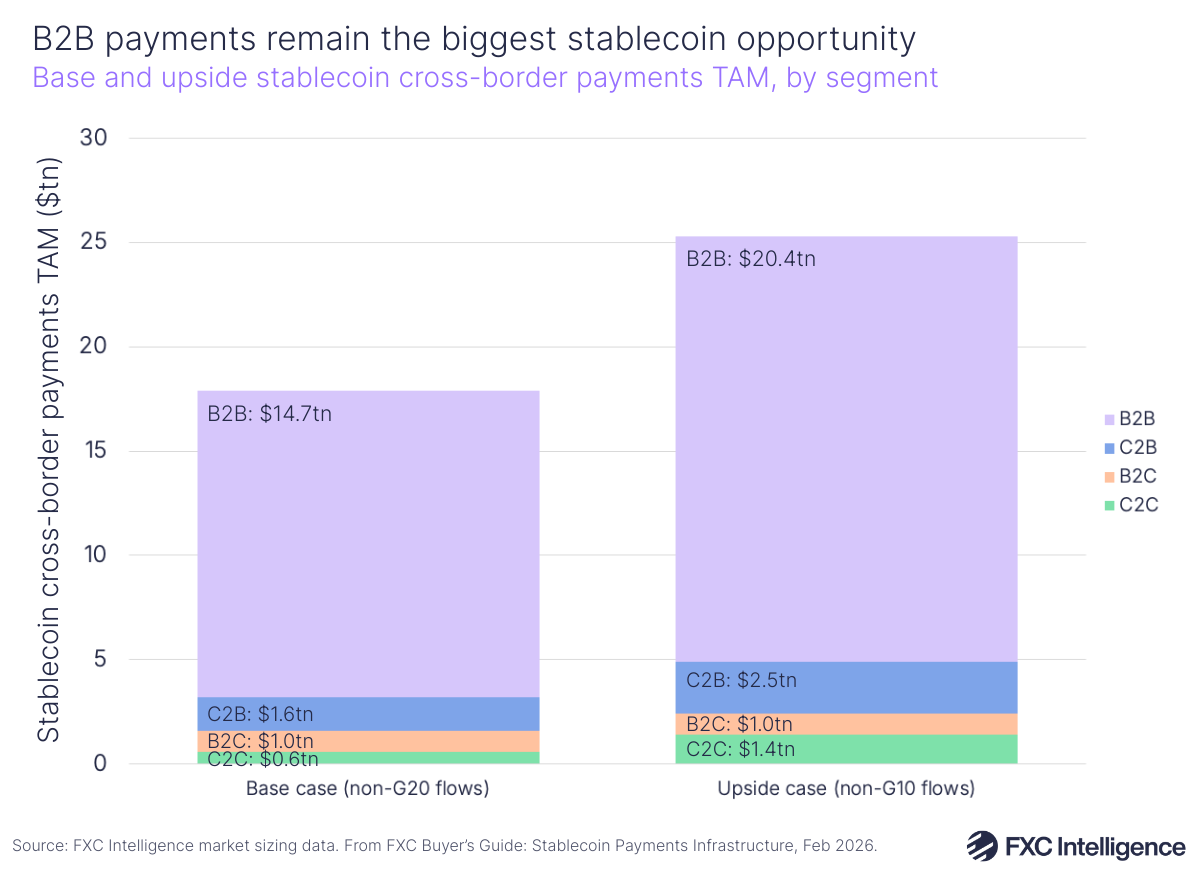

Within this, B2B payments remain the largest opportunity in terms of flows, with the base B2B TAM being $14.7tn and the upside being $20.4tn. C2B payments comes in second, at $1.6tn to $2.5tn.

B2C payments, meanwhile, have a stablecoin TAM of $1tn, while C2C payments now represent an opportunity of between $0.6tn and $1.4tn.

However, much of that opportunity is still to be realised, suggesting that the industry may see several years of very high growth yet. At present, we assess the share of cross-border payments being delivered using stablecoins to be significantly less than 1% of total non-wholesale flows, despite having grown significantly in 2025.

Unlock full access to the industry’s most comprehensive guide to stablecoin payments infrastructure

The stablecoin infrastructure framework

Despite sometimes being discussed in monolith terms, stablecoin infrastructure is not a single alternative rail, but a stack of interoperating systems. These include not only the stablecoins themselves and the processes that enable them to be issued, redeemed or exchanged, but also a host of other intersecting elements.

These include the blockchain networks on which they move, of which there are a number of high-liquidity default options, as well as less widely used options that provide different choices in terms of settlement and transaction fees. In some cases, networks will provide incentives to encourage their use, while some companies are increasingly making use of ‘Layer-2’ networks that sit on top of widely used ‘Layer-1’ networks to reduce costs and increase speeds.

Wallets are another fundamental element, acting not as a kind of virtual pocket to store value, but as addresses from which transactions and other critical steps in the payments orchestration process can be initiated and managed. They are a foundational part of stablecoin infrastructure, serving as essential nodes in the on-chain movement of funds as well as being used to store value both for providers’ clients and their end users, and how they are securely managed can be configured in a wide variety of ways depending on their application, the client’s risk appetite and their regulatory requirements.

Other elements include the on and off-ramping of funds from fiat to stablecoin and vice-versa, the provision of compliance solutions including KYC/KYB and liquidity solutions at both ends of the payment process.

However, how companies engage with this stack varies significantly depending on the types of providers they opt to use. While the capabilities of each provider vary, they can be broadly grouped into two types:

Managed payment providers

Combine multiple parts of the infrastructure stack into a combined solution, typically handling many technical and compliance elements and reducing the technical and regulatory burden on their clients. Typically, they offer faster time-to-market for companies with limited stablecoin expertise.

Self-managed payment providers

Provide modular solutions that can be implemented as part of a broader technical stack, offering greater direct control and flexibility over areas including pricing and execution, although carry a higher technical and regulatory burden. Often favoured by companies with higher volume requirements and technical capabilities.

The regulatory and compliance landscape

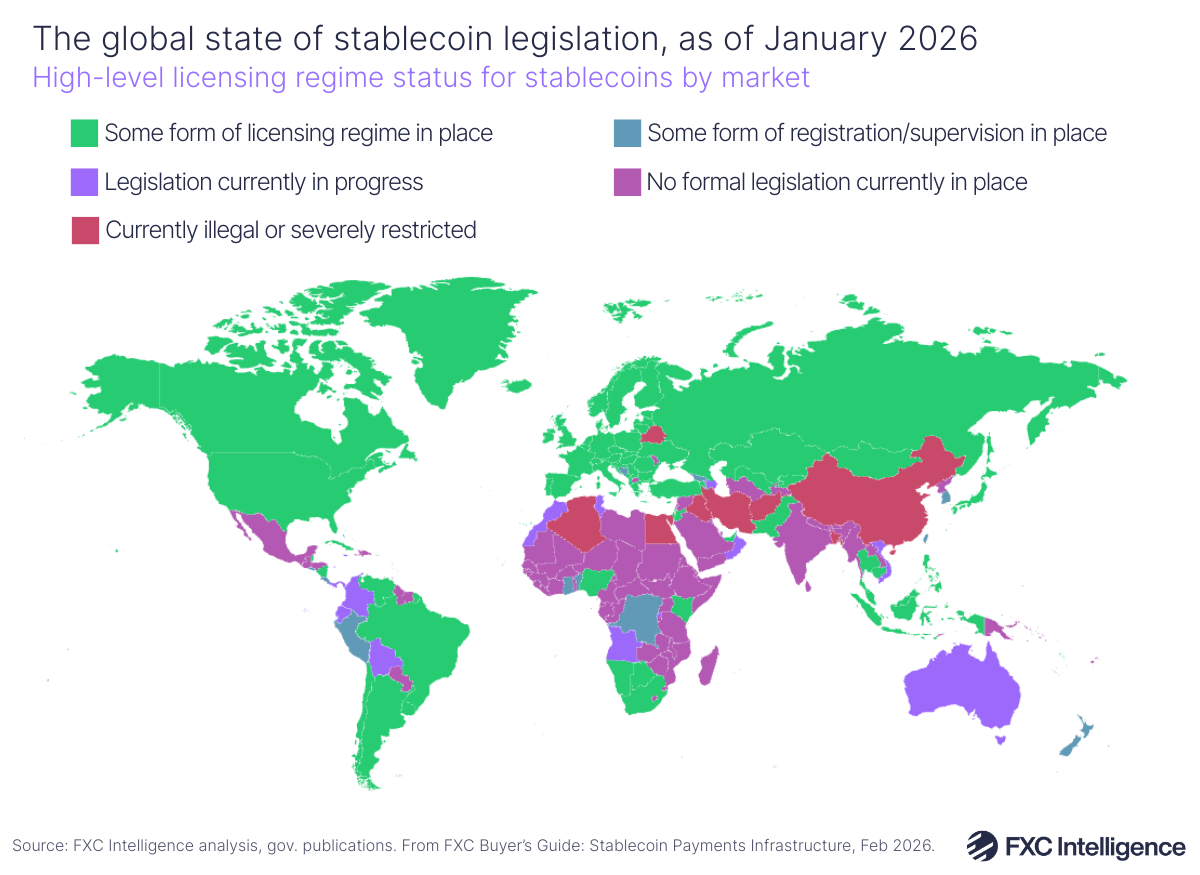

The global regulatory landscape around stablecoins is far from settled, and varies significantly from market to market. While there are growing numbers of regions with some form of regulatory regime, there are also many where this is not yet the case or where regulations are still in the process of being developed.

While initial legislation often focuses more broadly on cryptocurrencies, more recent additions have been made to reflect the use of stablecoins and related assets for cross-border payments. These typically focus around areas including consumer protection, financial stability, market integrity, operational resilience and anti-money laundering.

Two of the most notable recent regulations focused on stablecoins are the US’s GENIUS Act and the EU’s MiCA. However, while the former has arguably been the biggest catalyst for cross-border payments stablecoin adoption, it largely focuses on the issuance and management of stablecoins. MiCA is more comprehensive, focusing additionally on aspects including the providers of services relating to stablecoins and other crypto assets.

Known as crypto asset service providers (CASPs) under the EU law, these are also more broadly known as virtual asset service providers (VASPs). These definitions typically cover companies that operate in areas including the custody, exchange, payment or receipt of stablecoins and in many markets, such companies must be registered or licensed, under recommendations by the Financial Authority Task Force (FATF).

Around 40% of markets globally have some form of VASP regime in place, which can impact what services a provider can offer in a local market if they do not have the necessary licence or registration. However, not all markets with such legislation have begun issuing licences.

The other critical aspect of stablecoin legislation is the Travel Rule, another FATF recommendation, which requires certain information about a stablecoin payment’s sender and recipient to accompany the transaction, ensuring traceability to support anti-money laundering, fraud protection and sanction compliance efforts. Although not in place in all markets, the Travel Rule is widespread enough that it has become standard for most companies within the space, with many providers integrating with third-party solutions to ensure end-to-end compliance.

Unlock full access to the industry’s most comprehensive guide to stablecoin payments infrastructure

Stablecoin legislation status of the world’s top 10 markets by GDP, as of January 2026

| Market | Region | Status | Companies already licensed or registered in this market? |

| United States | North America | Some form of licensing regime in place | ✔ |

| China | East Asia | Currently illegal or severely restricted | – |

| Germany | Europe | Some form of licensing regime in place | ✔ |

| Japan | East Asia | Some form of licensing regime in place | ✔ |

| India | South Asia | No formal legislation currently in place | – |

| United Kingdom | Europe | Some form of licensing regime in place | ✔ |

| France | Europe | Some form of licensing regime in place | ✔ |

| Italy | Europe | Some form of licensing regime in place | ✔ |

| Russia | Europe | Some form of licensing regime in place | – |

| Canada | North America | Some form of licensing regime in place | ✔ |

Insights from the buying process

Companies engaging in the stablecoin infrastructure buying process often face challenges negotiating with the broad number of providers, different solutions available and being able to effectively assess the right approach for them. To aid this, we spoke to payment companies, investors, Tier 1 banks and fintechs who are already buyers to build up the insights in this section.

An important first step to streamlining the process is to determine what a company’s strategic objectives are for adopting stablecoins, be they internal treasury, customer-facing solutions such as pay-ins and payouts or to increase the reach and capabilities of their own cross-border payments offerings.

Beyond this, deciding between a managed and self-managed strategy is an important step, although many companies do opt to use a mix of both and typically evolve their approach over time as their needs change and their confidence with the technology grows.

Either way, it is likely that their solution will eventually involve more than one vendor, as no single provider can solve every problem in the stablecoin space globally. Many organisations use multiple vendors not only for coverage, but also redundancy, with different providers excelling in different functions or regions.

Buyers interviewed about their own experiences consistently highlight several areas of note to consider in the process. These include:

- Underestimated timelines: Many buyers say onboarding took longer than they had initially expected, and onboarding for large institutions can be highly complex. The process can take multiple months, depending on the provider and the buyer’s requirements.

- Compliance maturity: Not every provider is equally mature regarding regulatory standards and buyers do need to ensure they conduct due diligence to confirm a provider meets their compliance needs.

- Liquidity depth: Different providers will be better suited to moving different send amounts, with high-volume treasury requiring providers that can match large ticket sizes reliably and without significant slippage.

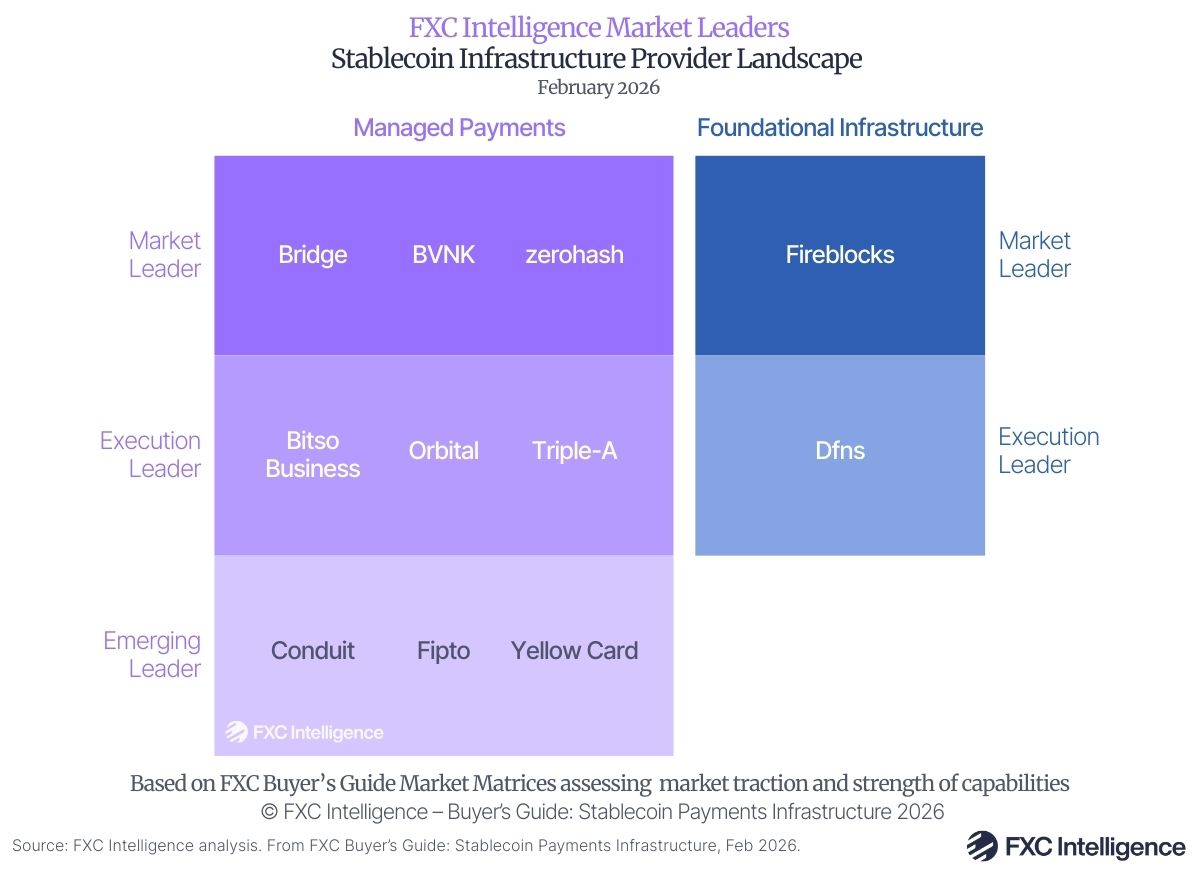

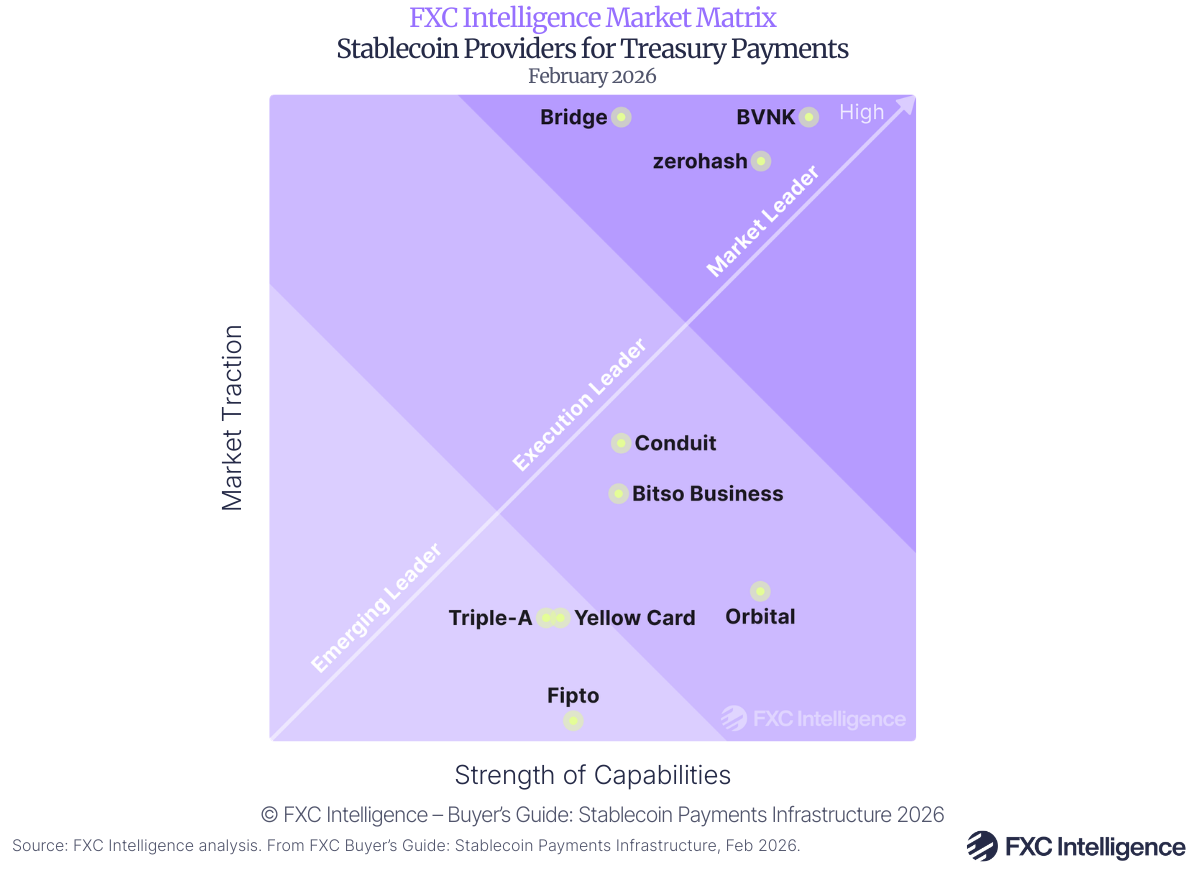

FXC Market Matrix and vendor positioning

The guide sees FXC review the capabilities of 11 different stablecoin infrastructure providers across a wide range of areas, including their licensing and infosecurity capabilities, pay-in and payout rails and fiat currency support and their range of support for stablecoin/blockchain pairs. Every provider reviewed had strengths across these capabilities, with different providers being better suited to different use cases. The 11 companies with in-depth profiles included in the guide are:

- Bitso Business

- Bridge

- BVNK

- Conduit

- Dfns

- Fipto

- Fireblocks

- Orbital

- Triple-A

- Yellow Card

- zerohash

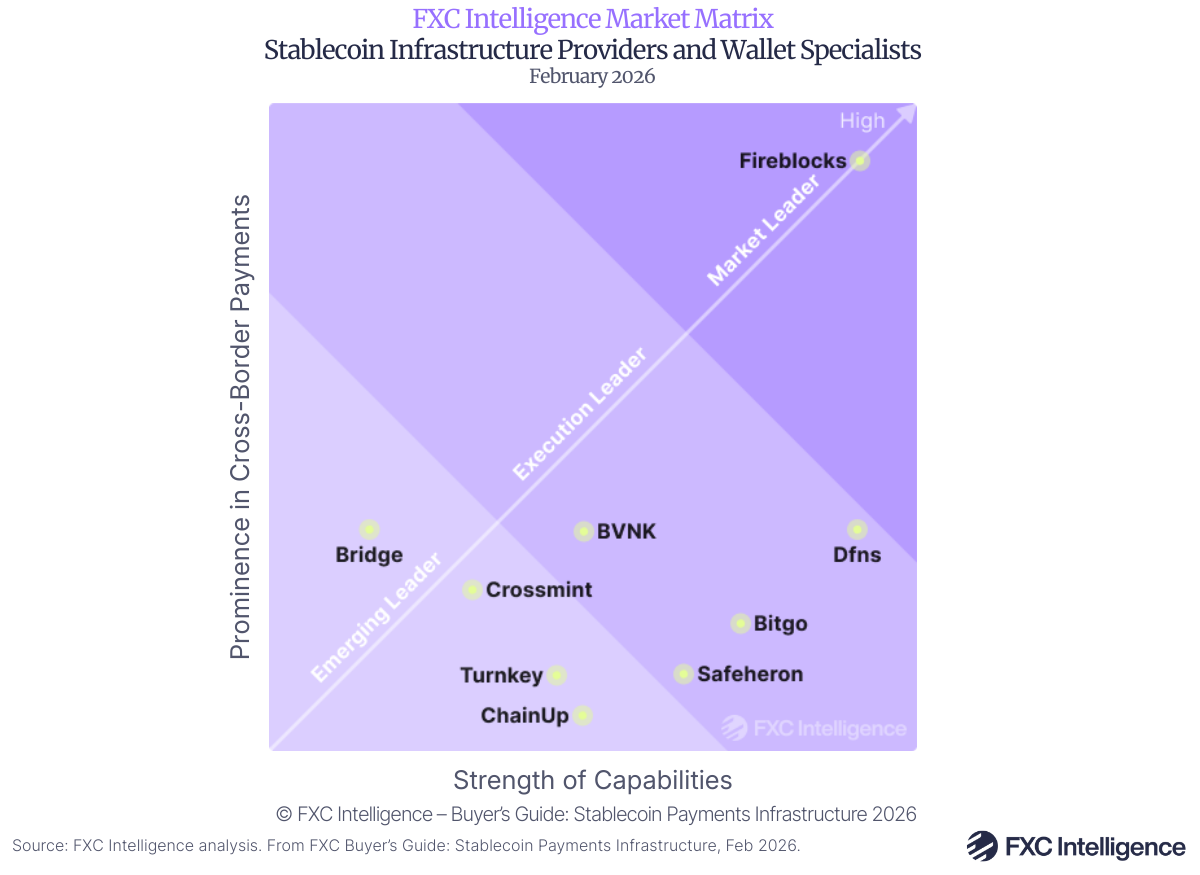

We also reviewed the capabilities and reach of a further 13 providers in the space to provide broader benchmarking and context. These are:

Managed payment providers:

- Alfred

- Mural

- Nilos

- Noah

- OpenFX

- OpenPayd

- Rail

- Ripple

Wallet infrastructure providers:

- BitGo

- ChainUp

- Crossmint

- Safeheron

- Turnkey

This guide sees FXC produce a number of Market Matrix graphics, in which we evaluate providers based on their market traction and the strength of their capabilities. For each use case, this sees us combine them into one of three categories:

Market Leaders

Companies that have demonstrated strong market traction and have strong capabilities in the areas required for that particular use case. For example, in treasury payments, these companies typically have a focus on regulatory compliance, licensing and infosecurity while also prioritising key global currencies.

Execution Leaders

Companies that may not have the same market traction as Market Leaders, but who have strong specialisations either regionally or by customer segment, reflected in their capabilities around areas such as local rails support.

Emerging Leaders

Smaller scale or up-and-coming providers who are still growing their presence but have specific specialisations that make them a strong option for companies with certain requirements, such as expertise and compliance in a particular market.

Many providers also have strong regional specialisations, with those looking for providers for Asia-Pacific markets, for example, being likely to find a given player to be better suited to their needs than a company focusing on the Americas.

For those requiring self-managed solutions, there are similarly different solutions for different needs, although Fireblocks is notable for its scale and relatively unique position as a provider of multifaceted stablecoin infrastructure capabilities, via a platform through which other providers can easily be integrated.

Get access to the proprietary benchmarking data underpinning the Buyer’s Guide

Looking ahead: Emerging solutions

Much of the stablecoin industry is still relatively nascent, and there have been a wide variety of solutions launched that may ultimately prove to be valuable elements of stablecoin infrastructure in a cross-border payments setting, but which are not yet sufficiently developed to fully benchmark in this guide.

Stablecoin payment networks, most notably Circle Payments Network, Fireblocks Network for Payments and Paxos’ Global Dollar Network, are a notable example, having all launched within the last 18 months. Although they vary, these typically enable companies to easily connect to onboarded vendors’ services, acting as an intermediary to make it easier to connect to different solutions in the stablecoin infrastructure stack. While these have grown since launch, they typically remain small relative to other parts of the market at present and generally have only a fairly small number of live vendors, many of which are connected on multiple networks.

Stablecoin issuance, meanwhile, is an option for many companies, although something that is not always the most advisable approach to tackling stablecoin payments in all cases. When effective, it can provide an additional source of revenue from reserve yields, as well as providing strong branding opportunities, and there are a growing number of providers who offer issuance solutions as part of their range of products. However, companies can face challenges getting stablecoins to sufficient scale.

Finally, a number of new blockchains that have been designed specifically for the cross-border payments industry are currently being tested that could ultimately prove to be valuable additions for the sector. The most notable of these are being developed by Stripe and Circle, with both including features that are designed to combat issues such as high and volatile fees as well as the need to hold cryptocurrencies to pay on-chain fees, while reducing the settlement time to less than a second.

While all of these solutions are still emerging, we will continue to monitor them, and may go into more detail in future iterations if they reach a sufficient level of maturity and adoption.

Unlock full access to the industry’s most comprehensive guide to stablecoin payments infrastructure