For payment processors, the Q2 2023 earnings season has been a far cry from the pandemic peaks, but generally positive. We look at how trends in the payment processing industry are unfolding from the latest results and earnings calls.

For publicly traded payment processors, Q2 2023 has generally been a good, if unremarkable quarter. While investors were sceptical in some cases, the top line numbers have generally been positive and there are indications of an industry establishing a new period of normalcy following significant post-pandemic upheaval.

In the first in a new report series, we delve into the latest and past quarterly and half-yearly earnings to consider the current health of the industry, who is leading on which metrics and what trends are evolving to play a significant role in payment processors’ future development.

We cover a wide range of publicly traded payment processors, some of whom are in direct competition in parts of their business, and some of whom largely occupy niches within the market. These are Adyen, dLocal, FIS, Fiserv, Global Payments, PayPal, Paysafe, Worldline and Square. For some metrics, we use the data for Square’s parent company Block, while for others we use data for FIS’s merchant services division Worldpay, which FIS is currently in the process of spinning back out into its own standalone company.

In this report, we compare available comparable data for each company, alongside keyword analysis from available earnings calls to see how frequently different terms are being discussed by each payment processor.

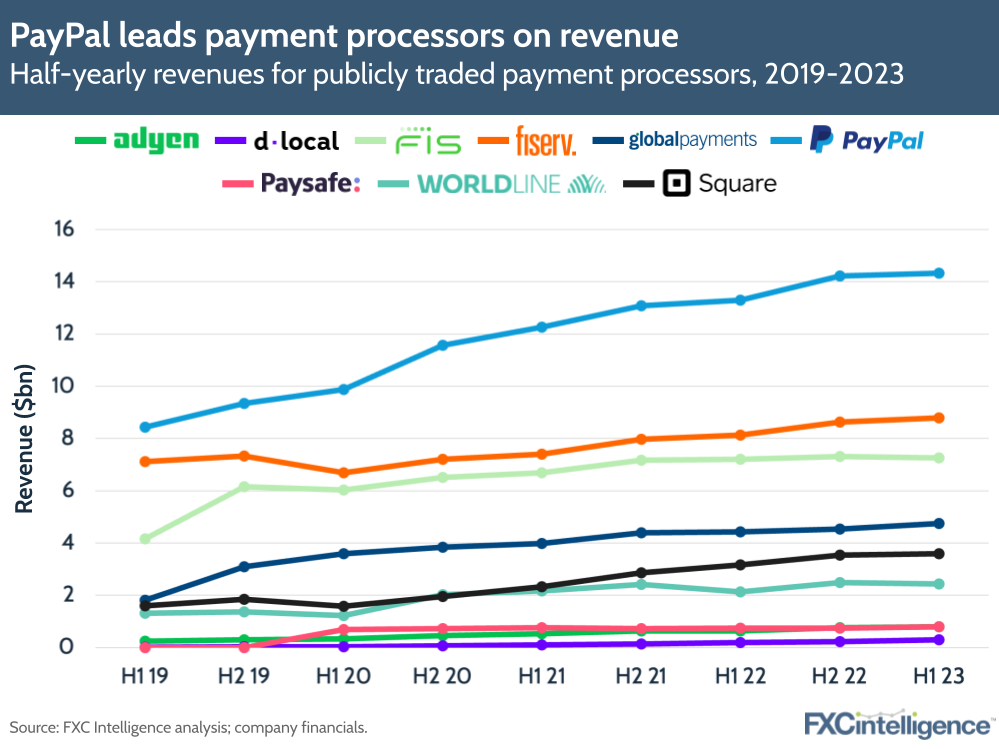

Growth in payment processors’ revenue for Q2 2023

Perhaps unsurprisingly, PayPal has consistently led on revenue over the past few years, and widened the gap with other players during the pandemic. It maintained the gap between it and the next biggest player in terms of revenue, Fiserv, between H2 2022 and H1 2023, which itself has seen consistent if more moderate growth since 2020.

FIS, the next largest player, has seen its revenue flatten over the past year or so, and it is looking to correct this with moves including the spinout of Worldpay.

Other players in the space are more spread out, with Square sitting between Global Payments and Worldline, while Adyen and dLocal sit above LatAm-focused player dLocal.

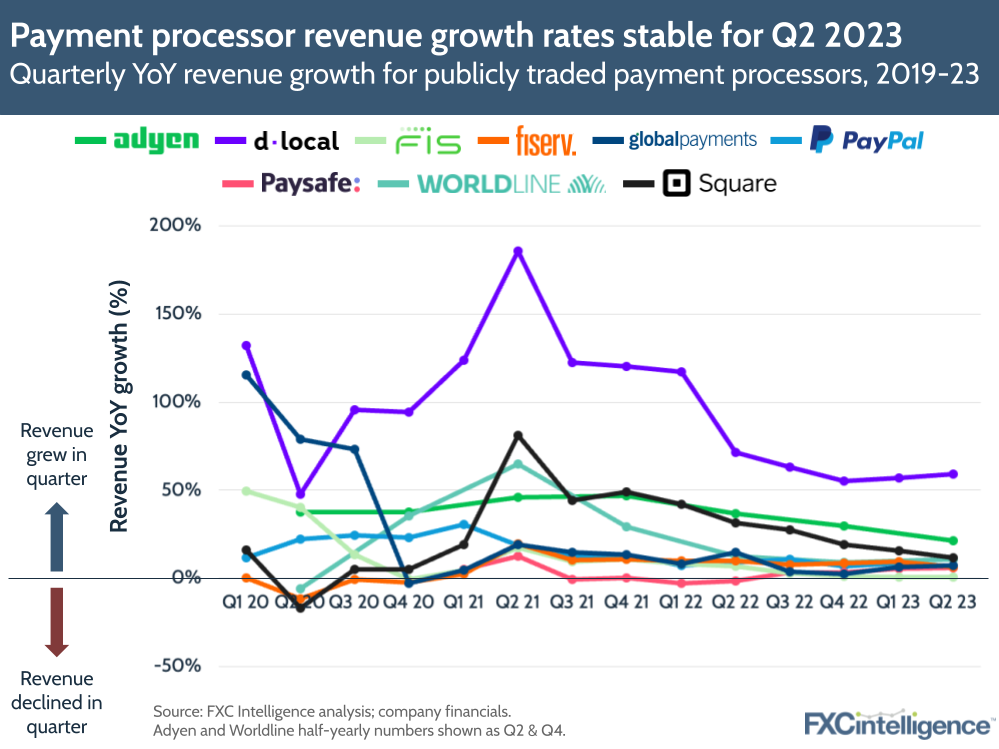

However, on growth rates, there is a general sense of slowing compared to the performance during the pandemic. dLocal, one of the most recently listed companies in the group, saw the highest rate of growth, with a 59% YoY increase in Q2 2023, although this is far below its mid-2021 peak of 186%. Adyen saw the next highest growth rate, at 21% YoY for H1 2023, but a drop in EBITDA resulted in the company’s shares tumbling, while Square saw a 12% YoY increase for Q2 2023 and Worldline saw an 11% increase for H1 2023. All other players saw growth of below 10% for the quarter, with Global Payments at 8%, followed by PayPal (7%), Fiserv (7%), Paysafe (6%) and FIS (1%).

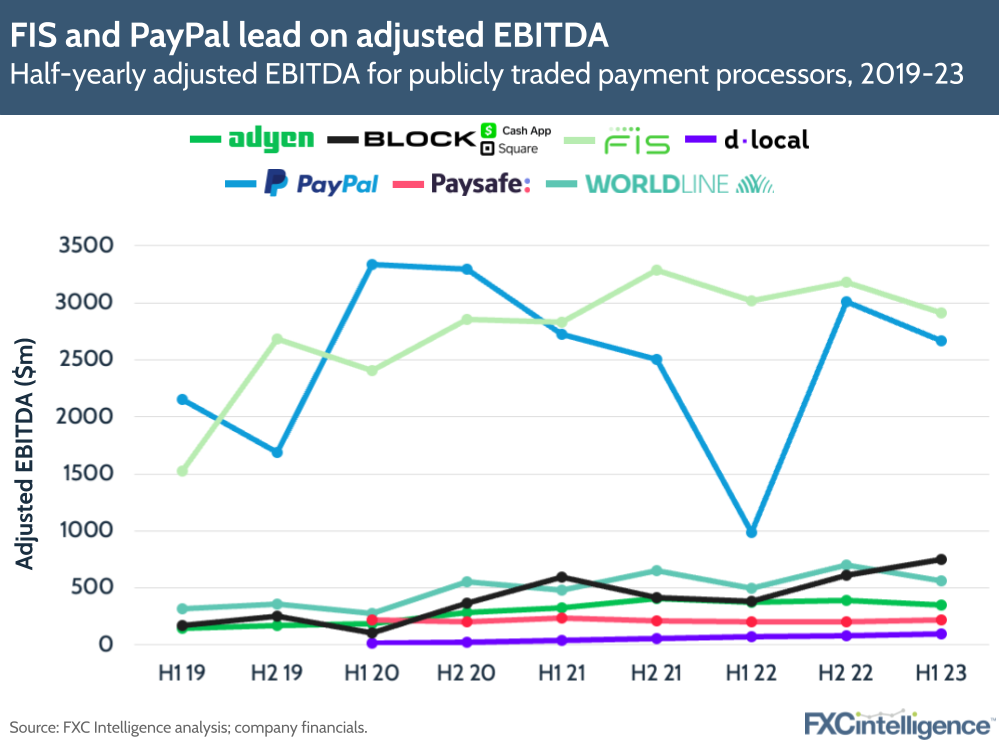

EBITDA and operating profit paint a different picture

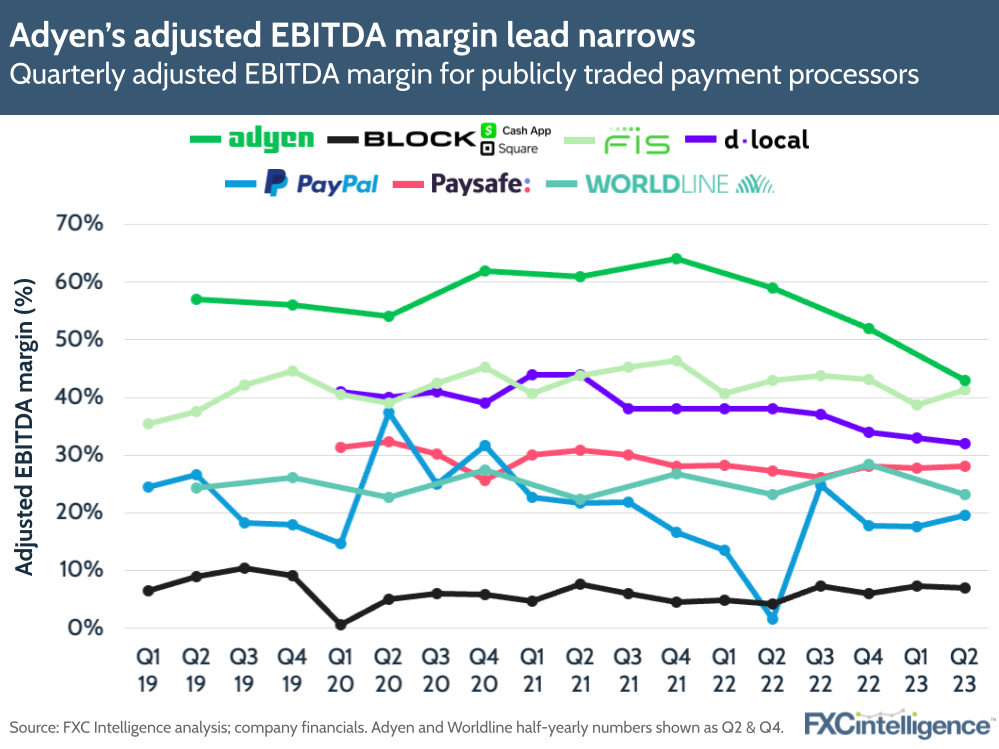

However, looking at payment processors’ adjusted EBITDA paints a different picture in terms of who is leading in the sector. Among those who report this metric, FIS leads, with PayPal in close second, while Worldline, Adyen, Paysafe and dLocal are all significantly below.

Block, while also far below PayPal and FIS on adjusted EBITDA, is the only company to have consistently grown this metric in both H2 2022 and H1 2023.

Meanwhile, looking at adjusted EBITDA margin paints a different picture again. Adyen remains in the lead, but its gap has narrowed significantly over the past few years, to the point where FIS is now only slightly below it on adjusted EBITDA margin. This is the result of a strong, ongoing investment programme, particularly around hiring technical staff, but has been a key contributor to its recent decline in share price.

Significantly, while Block has the lowest adjusted EBITDA margin among the companies that report this metric, PayPal has the second lowest, and has also seen the biggest variation over the course of the pandemic and beyond.

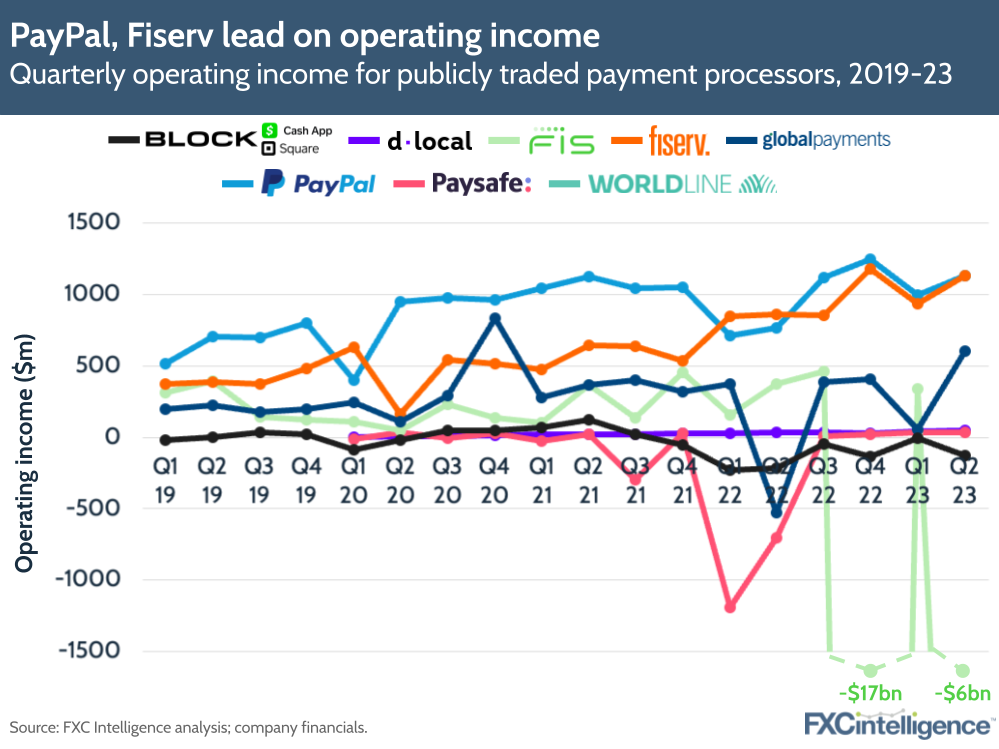

Operating income, however, provides another key view, highlighting the range of levels of profitability that the different companies are experiencing. Block is generally operating at a loss, and has done so in most quarters since mid-2021, while Paysafe is now back in the black after a few quarters of loss. FIS, meanwhile, has mostly been in the black but has had two quarters with significant losses, including Q2 2023, as it looks to reshape its business.

On the other side, PayPal has consistently seen the highest operating income, but Fiserv has been steadily catching up and as of Q2 2023 was just $2m below PayPal on this metric.

How is global card pricing shaping cross-border and domestic transactions?

Payment volume and take rate show potential

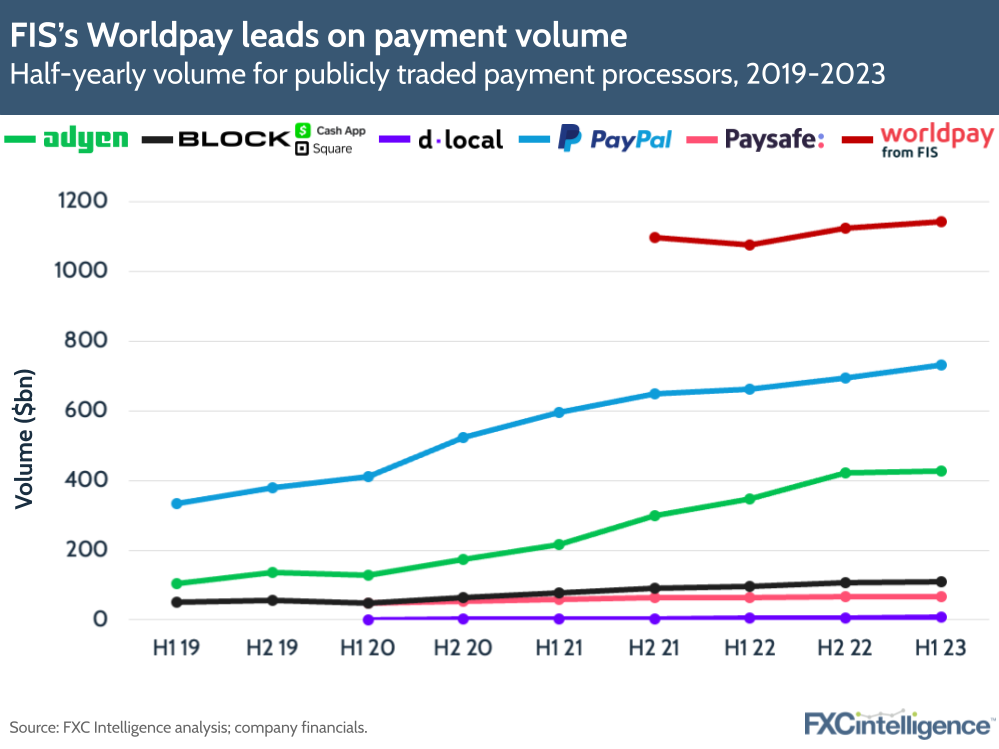

Among companies that report payment volume, there has been a steady increase across all companies, suggesting that the amount of money being spent via payment processors is increasing across all, or at least most, providers.

However, it is notable that the soon-to-be-standalone Worldpay is the leader on this metric – despite its parent FIS being lower on most other metrics – with a volume that now totals more than PayPal and Adyen, the next two biggest, combined. While it speaks to the types of payments being processed, this creates the potential for Worldpay to build on its current position and grow its presence on other metrics once it is a standalone player.

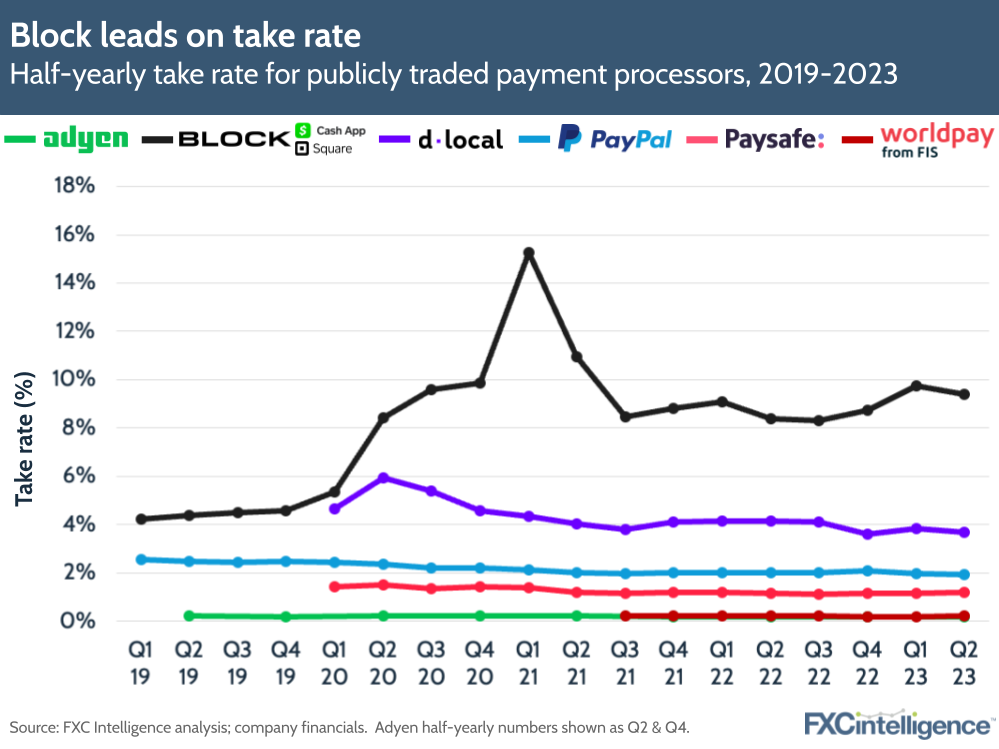

Meanwhile, on take rate, Block is notably in the lead, with dLocal in a distant second. Some companies have also seen this metric decline over the past few years, particularly PayPal and dLocal, while Block has seen an increase.

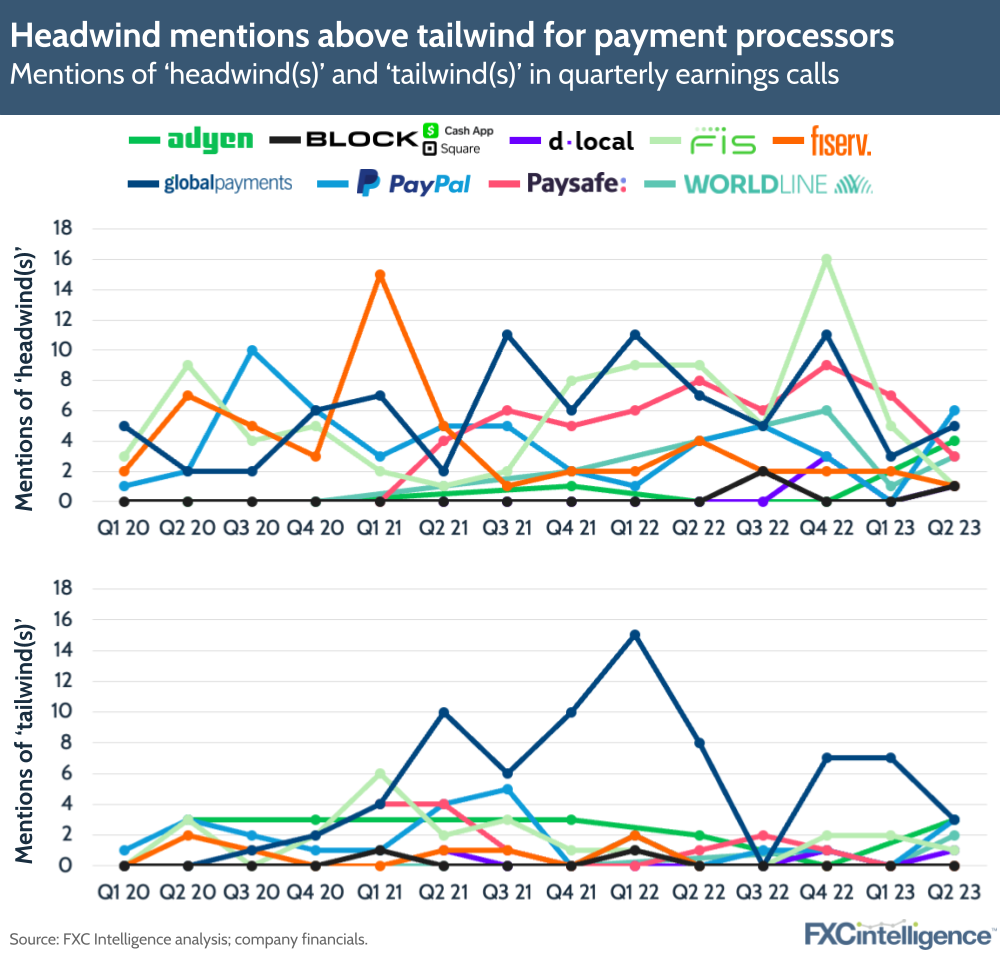

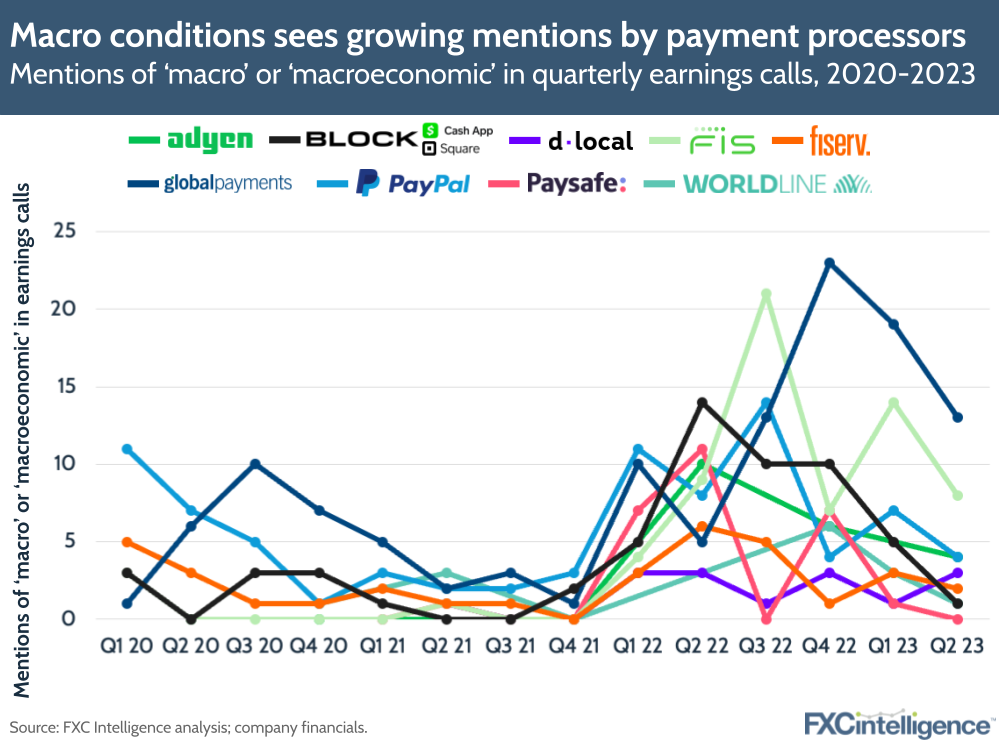

Are headwinds and macroeconomic challenges past their peak?

Looking at the use of keywords during earnings calls, there are a number of trends that reflect the changing market conditions in which companies are operating.

While mentions of ‘headwind’ or ‘headwinds’ has been consistently higher than ‘tailwind’ or ‘tailwinds’, use of the former has reduced for many players in the last two quarters. This was most notable among players such as FIS, Global Payments and Paysafe, which saw particularly elevated uses of the terms in 2021 and 2022.

The use of the terms ‘macro’ and ‘macroeconomic’ also speaks to this. Typically used to discuss macroeconomic challenges that are presenting knock-on impacts to the payments processing industry, the usage of these terms was slightly elevated during the early stages of the pandemic, but broadly reduced thereafter until surging in 2022 amid the Russia-Ukraine war and wide economic downturn.

However, mentions of the term dropped off notably in Q2 2023, suggesting payment processors are not feeling as severe an impact from this as they were a few quarters ago.

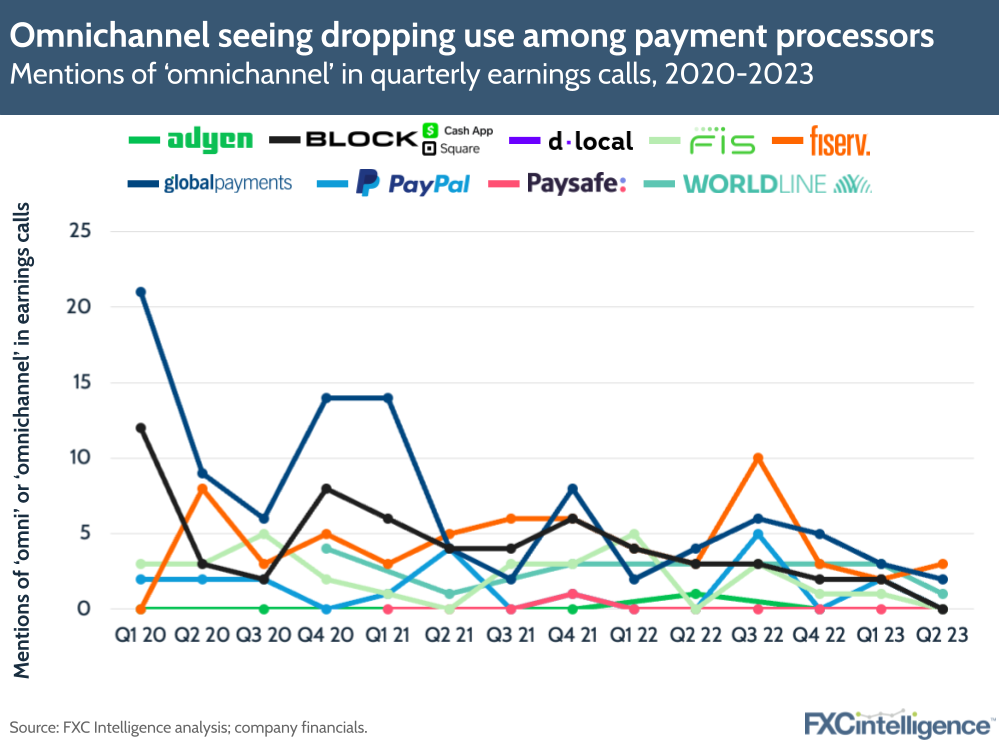

Digital, retail and omnichannel mentions see transition among payment processors

For many payment processors, their business is made up of both in-person point-of-sale solutions and online e-commerce-based payments. However, changing trends in the use of related words does reflect transitions in the market.

For example, uses of the word ‘digital’ peaked during 2021, when the industry was in the midst of a Covid-fuelled ecommerce boom, and although usage has seen an uptick in the most recent quarter, it remains significantly below its peak, particularly for Paysafe, Fiserv and PayPal.

By contrast, mentions of ‘ecommerce’ and related spellings are above Covid-era levels, and are on a generally upward trend for most players except FIS.

However, mentions of ‘retail’ have largely remained around the same levels across the period. Block is the exception here, with the company mentioning retail significantly during the pandemic but having reduced its discussion of the topic since.

Interestingly, use of the term ‘omnichannel’ to indicate a multi-platform strategy across retail and e-commerce has dropped significantly since the 2020 period, suggesting that the positivity around this approach has waned.

How are global ecommerce players approaching cross-border pricing?

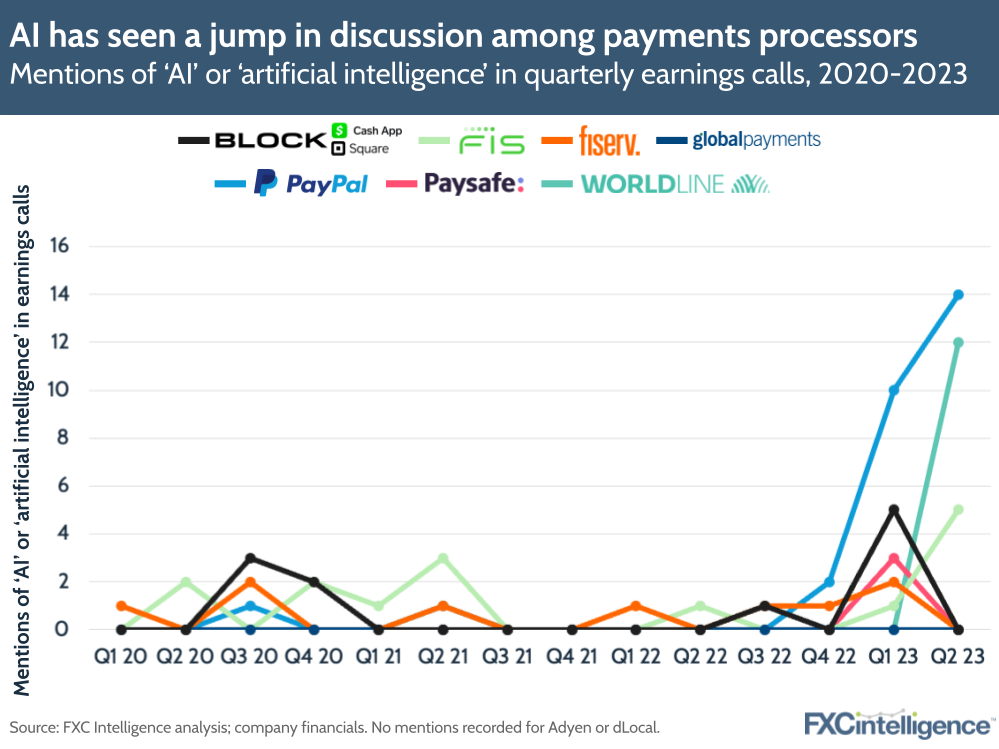

AI shows promise as a developing trend

Finally, there are signs that artificial intelligence (AI) is fast becoming the trend of choice for payments processing, with a significant jump in mentions among multiple companies over the past few quarters.

This reflects a wider enterprise enthusiasm for AI over the past year, particularly with the release of generative AI technologies such as ChatGPT. However, the extent to which AI is set to positively impact the bottom line of payment processors remains to be seen.

It may ultimately see a usage pattern similar to omnichannel, where it moves from the term-of-choice to a less discussed area, or it may see a long-term uptick as the technology reshapes the industry.

Payment processing appears to be in a transitional moment at present, as long-standing leaders begin to flatten their growth while other players shift strategies to claim more of the market. How this evolves remains to be seen, but it is likely that trends detailed here will evolve significantly in the coming quarters.