An extensive review of MoneyGram’s financials and strategy as it agrees to an acquisition by Madison Dearborn Partners.

The announcement on Feb 15, 2022 that MoneyGram International, one of the biggest remittances players globally, has entered an agreement to be acquired by leading private equity firm Madison Dearborn Partners is a major development for the payments industry.

MoneyGram has had a difficult few years until recently, following a failed acquisition by Ant Financial and a $125m fine from the US FTC in 2018. But since the beginning of the pandemic, it has been able to refocus its business on digital, with a stated goal of being 50% digital by 2024. It has also been one of the most innovative remittances companies in the crypto and blockchain space.

The acquisition, which will see it return to being a private company, represents a big potential next step as it continues to build on its digital strategy. It may free MoneyGram from the ties of public market ownership and focus on EBITDA margins and allow it to invest in new products, infrastructure and growth and emerge anew several years down the line. Easier said than done given the competition in the remittances industry, but private ownership backed by a deep-pocketed private equity player would give it a good chance to achieve this.

There are some big questions to answer. How does MoneyGram compare to other players in the space and what opportunities lie ahead for a new owner? And whilst MoneyGram has entered into an agreement to be bought by Madison Dearborn, a 30-day ‘go-shop’ period means MoneyGram can solicit other offers and a different owner could emerge. In our detailed report below, we look at all these questions and more.

Background to Madison Dearborn’s potential acquisition of MoneyGram

Terms of the current deal with Madison Dearborn Partners

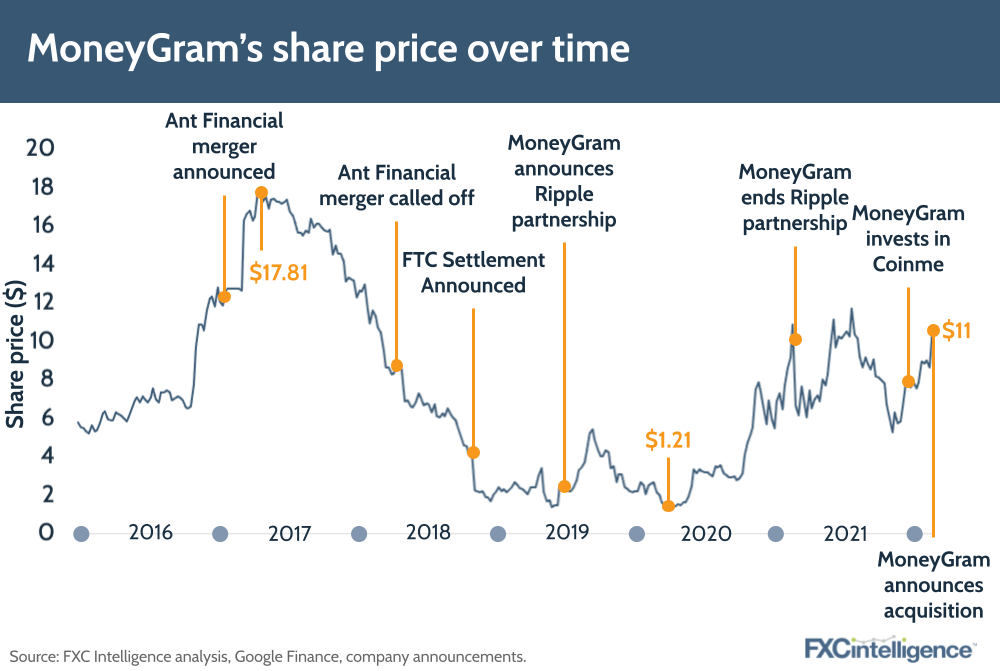

The agreement with Madison Dearborn Partners (MDP) announced on February 15, 2022 sees all outstanding shares of MoneyGram acquired for $11 per share in an-all cash transaction. Its total value is around $1.8bn, although this includes outstanding debt of $799m, putting the valuation of MoneyGram at about $1.1bn. This was at a premium of about 50% to the price in mid-December before media speculation began about a transaction and a 19% premium to the price on February 14, the day before the announcement.

MDP intends to refinance MoneyGram’s outstanding debt, with debt financing agreements already in place with Goldman Sachs, Deutsche Bank and Barclays. The company anticipates the deal closing in Q4 2022, at which point MoneyGram will become a private company, with no shares available on any stock market globally.

Following the close of the transaction, it is expected that MoneyGram will continue to operate under the MoneyGram brand and be led by Alex Holmes and the company’s existing leadership team. MoneyGram will maintain its headquarters in Dallas, Texas.

MDP is a US private equity firm has a strong track record of investments and acquisitions, having previously completed the leveraged buyout of a number of high-profile companies, including Nuveen investments, LA Fitness and Yankee Candle. Payments companies in its investment portfolio include Evo Payments and PayPal.

However, while MDP has put in a strong offer for MoneyGram, the agreement does include a 30-day ‘go-shop’ period. This means that until March 16, 2022 MoneyGram is allowed to actively seek alternative offers from rival companies, and if it receives a better offer from elsewhere it may ultimately reject MDP’s offer in favor of this new challenger.

Figure 1

History of MoneyGram

MoneyGram began life as two companies, the 1940-founded Travelers Express, a Minneapolis-based provider of money orders that later became known as Viad Corp, and the 1988-founded MoneyGram Systems, a subsidiary of First Data-owned Integrated Payment Systems. After IPS was sold off in 1992, it was renamed MoneyGram Payment Systems and by the end of the decade was serving customers in over 100 countries.

The company went public in 1996 but formed MoneyGram International in 1997, with MoneyGram Payment Systems owning 51% and Thomas Cook Group owning the remaining 49%.

In 1998 the modern iteration of MoneyGram was formed when Viad Corp acquired MoneyGram Payment Systems and folded it into the Viad-owned Travelers Express. In 2003, this was spun off as an independent company following its acquisition of Thomas Cook’s share. In 2004 it was renamed MoneyGram International and became a publicly traded entity.

For the next few years MGI grew its business and value, with agent locations climbing to almost 100,000 by the end of 2006. However, it was hit badly by the 2008 financial crisis, losing over $1.6bn in investments and ultimately having to sell a majority stake in order to generate cash.

After returning to profit in 2009, MoneyGram once again began to grow its business, reportedly considering a sale in 2013, however it was hit badly by the loss of a partnership with Walmart in 2014, forcing a number of layoffs, and saw shares fall consistently until late 2015.

The company had another turnaround over the next few years, and in 2017 it saw a bidding war to acquire the company between Ant Financial and Euronet. Chinese-owned Ant Financial won, with an offer of $18 a share, however 2017 became a year in limbo as MoneyGram waited and lobbied for regulatory approval for the acquisition. The company even had to refile after its initial application expired without a decision, but at the start of 2018 the Committee of Foreign Investment in the United States announced it was blocking the merger due to national security concerns.

The company’s share price began to slide on the news, but took a sharper tumble in November of that year when the company announced it had agreed to pay a $125m fine to the US Federal Trade Commission. According to the FTC, this was “to settle allegations that the company failed to take steps required under a 2009 Federal Trade Commission order to crack down on fraudulent money transfers that cost US consumers millions of dollars”.

Led by CEO Alex Holmes, who was appointed in 2016, MoneyGram has since embarked on a multi-year period of rebuilding, which has seen it remove bad business – taking a year-on-year hit in the process – and develop a long-term strategy to improve its future development. This included taking a $30m investment from Ripple at $4 a share and adding Visa as a deposit partner. In 2019 it also launched a new money transfer app as part of an increased focus on digital.

Having seen some impact from the pandemic in 2020, in Q2 2021 MoneyGram announced that it had exited its Deferred Prosecution Agreement and undertaken extensive debt restructuring, providing increased liquidity for H2 2021 and ultimately placing it in a strong position for its acquisition by Madison Dearborn. The February 2022 offer sees shares priced at $11 each, around a 50% increase on the company’s stock price in mid-December 2021.

Figure 2

Summary of MoneyGram’s Coverage

Today, MoneyGram provides remittance services to over 200 countries and territories, and has over 400,000 locations globally. Customers have the ability to send and receive money transfers at these retail locations, or at kiosks, online or via MoneyGram’s app. The company places a strong focus on providing a broad range of pay-in and pay-out methods, enabling customers to use the solution best suited to their needs – an omnichannel approach. Since a large portion of the remittance sector (and MoneyGram’s business) is still cash focused, this makes sense.

While MoneyGram has increasingly looked to digital, CEO Alex Holmes regards cash to still be “a super important part of the remittance mix”.

“Cash is still relatively king in most markets,” he told FXC Intelligence CEO Daniel Webber following the company’s Q1 2021 earnings results. “It’s the most liquid tradable form of payment that you can have, particularly in countries where you don’t necessarily trust the governments.”

For consumers, MoneyGram also offers additional services in some markets, including bill payments, money orders and cheque processing. The company also provides services to businesses, including its global network of agents, which include baking and biller solutions.

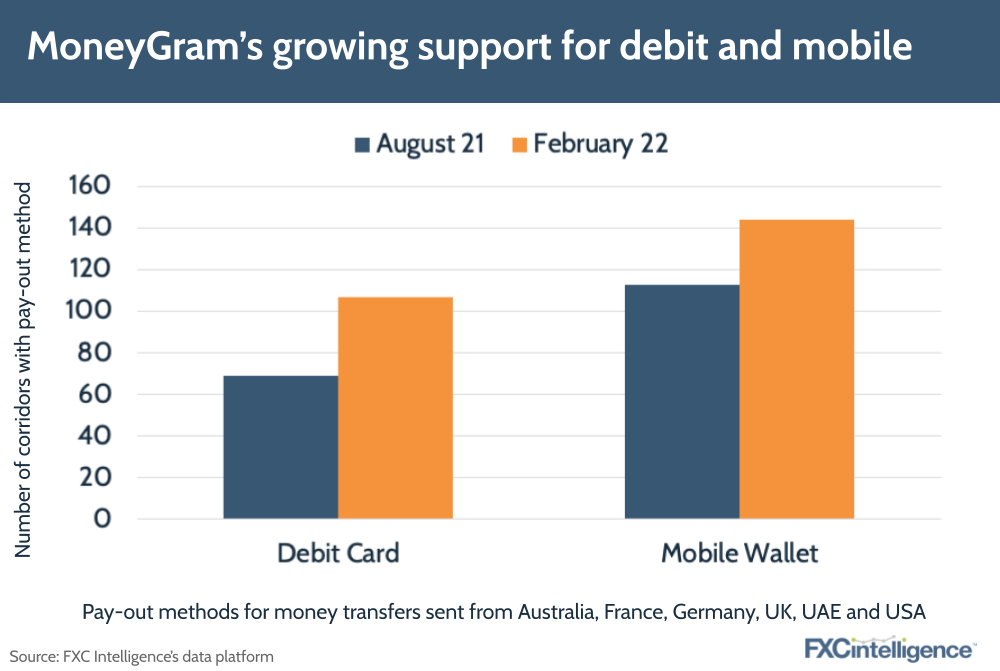

Over the past few years, MoneyGram has increasingly been pushing payouts to debit card and mobile wallets as well as bank accounts to strengthen its digital offering. As an example out of Germany, over the last six months the focus has been on debit cards and mobile wallet capabilities. MoneyGram is not alone in this strategy, many of the players in the sector are following the same path.

Figure 3

Shift to Digital

While MoneyGram retains its global network of cash pay-in and pay-out locations, the company has increasingly been focused on growing its digital offering – both in terms of its capabilities and the adoption by users. This has ultimately impacted how it characterizes itself as a company, with it describing itself as “a global leader in the evolution of digital P2P payments” in the press release announcing its acquisition by MDP.

This has seen it increase focus on payments via its app and website, as well as to accounts – a result of its partnership Visa Direct that Holmes in Q1 described as an “interesting inflection point in the mindset of a lot of consumers”.

“People have gotten a lot of solace with their mobile devices and the access to see that money sitting there,” he said, adding that it is also “a good medium to send to yourself”.

Notably, while the company is attracting retail customers to its digital offering, 85% of its digital customers in Q2 2021 were brand new to the company. This digital increase is in part attributable to the pandemic, with online customers skewing younger, although Holmes does highlight that the 15% who have gone from retail to digital remain a significant amount.

“The number is increasing just because of the sheer size of the walk-in business. On the flip side, even though that 15% is a small percentage number, it’s on such a large base that it’s actually beginning to fill the monthly active user pot quite substantially,” he told Webber following the publication of the company’s Q2 2021 numbers.

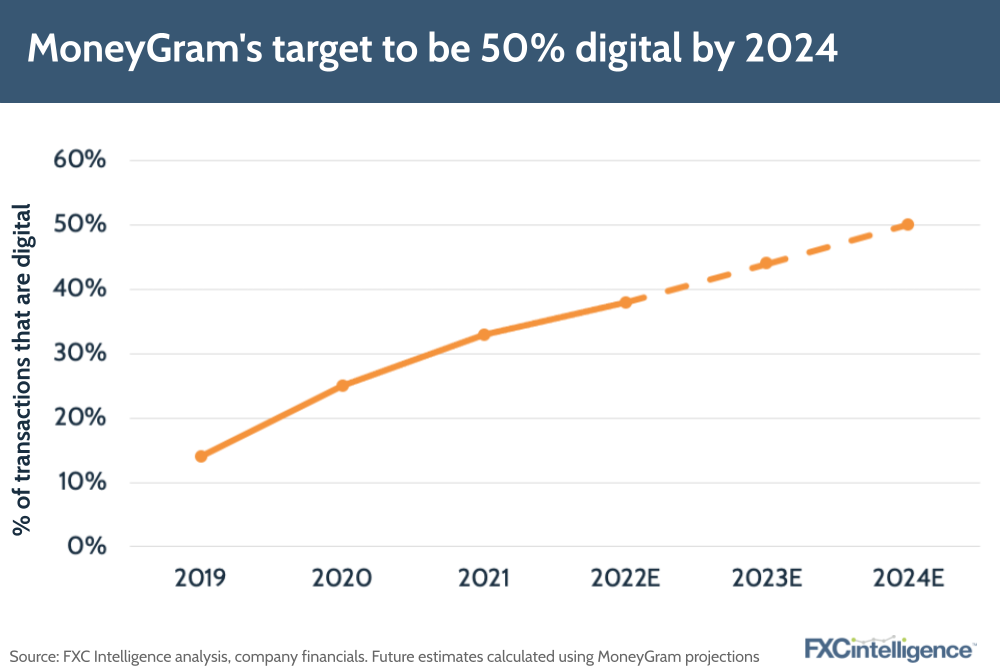

Nevertheless, MoneyGram is pursuing a target of 50% of transactions being digital by 2024, which following Q2 Holmes described as necessitating the company to “push and grow the digital business as quickly as possible”.

This, he said, includes further enhancements on the company’s app, optimizing pricing, increased marketing investment and “figuring out where the marginal returns are on investment”.

“We’ve been trying to optimize and get more targeted on the online, because you can spend millions and get nothing back for it,” he said. “So we’ve been really trying to tighten that up and get targeting. That’s really lowered our cost of acquiring individual customers.”

He has also highlighted the potential for further partnerships to increase access in certain markets.

Figure 4

The move to cryptocurrency

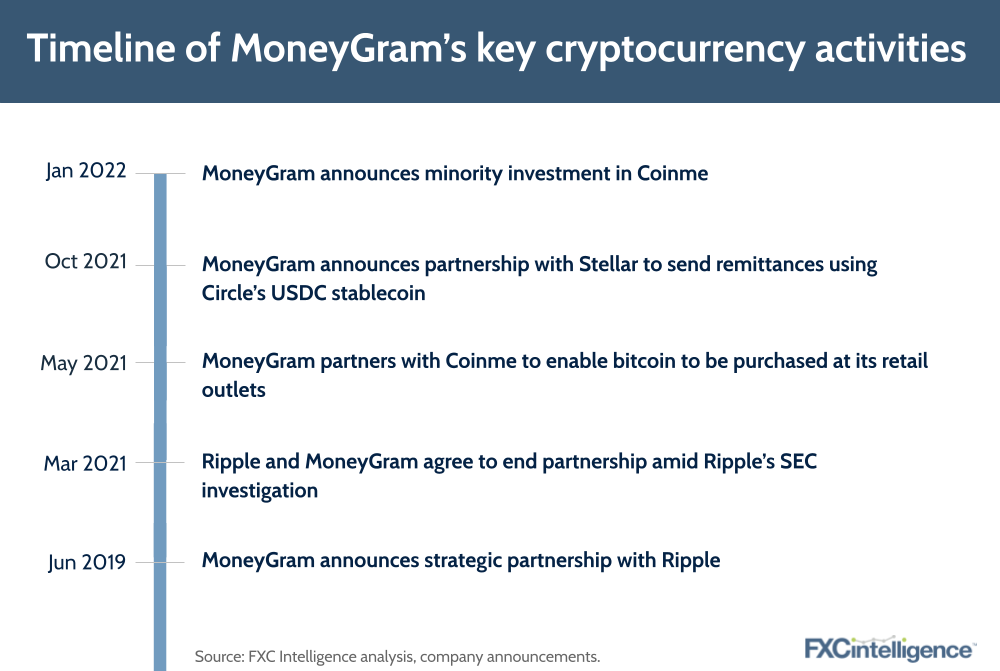

While MoneyGram has increasingly focused on digital, it has also begun to explore its potential role in the rapidly emerging cryptocurrency industry, and has already engaged in the space far more than other remittances players.

While in 2019 it previously partnered with Ripple to use stablecoins for cross-border payments and foreign exchange settlement, an SEC investigation into the blockchain startup saw that partnership end in 2021.

However, in October 2021 the company launched a new initiative using the technology in partnership with Stellar, which this time would see the company send money using Circle’s stablecoin USDC. In January 2022 it also added support to buy blockchain from its retail outlets through a partnership with Coinme, taking a 4% stake in the company as part of the deal.

Speaking to FXC Intelligence shortly after the Coinme announcement, Holmes said that while the company is “not betting the farm” on the technology, it does see a potential role for MoneyGram in the space, by enabling interoperability between fiat and crypto and adding payment rails to such digital currencies.

“MoneyGram operates all around the world, and effectively we’re a money transfer remitter, but we’re also in many respects kind of a foreign exchange outlet,” said Holmes.

“If you start to think about interoperability between crypto and fiat, you think about the Stellar platform and you think about what Coinme’s doing, MoneyGram can play a really interesting role in many, many markets around the world.”

To understand the full range of data coverage we have on crypto, please contact us

Figure 5

MoneyGram International: Key Financials

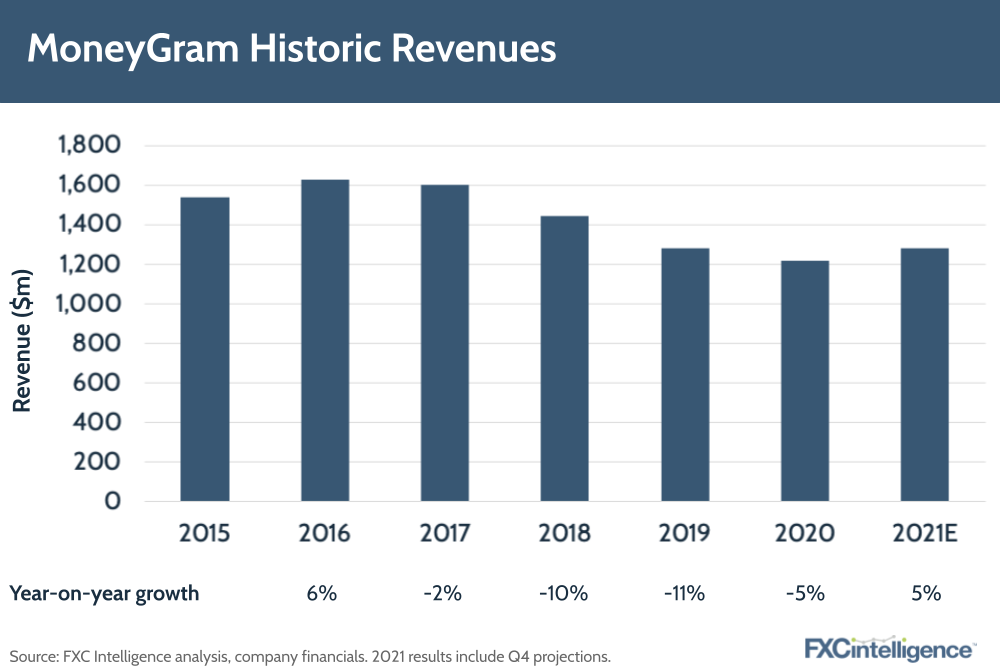

MoneyGram is recovering from its 2018 hit

While MoneyGram suffered a hit to growth in 2018 when it was fined by the FTC, it has since begun to recover, despite the impact of the pandemic. Nevertheless, the company’s revenues remain below pre-2018 levels and improving these will be key for the new owner.

Figure 6

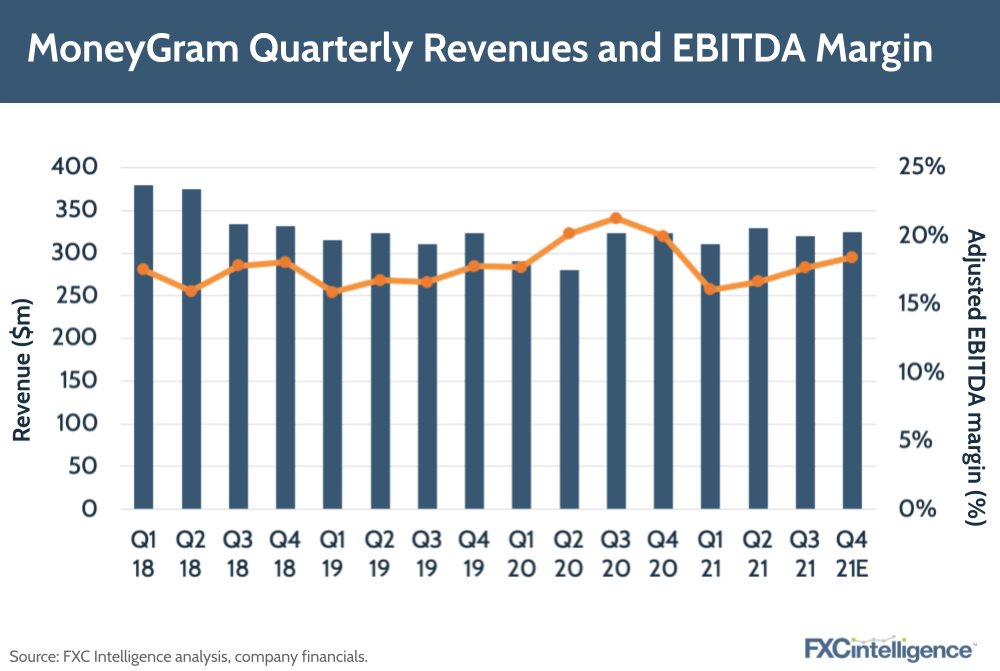

MoneyGram has bounced back from the pandemic

Although MoneyGram’s revenue did suffer from the pandemic alongside its rivals, it has shown a good recovery, particularly through 2021.

Figure 7

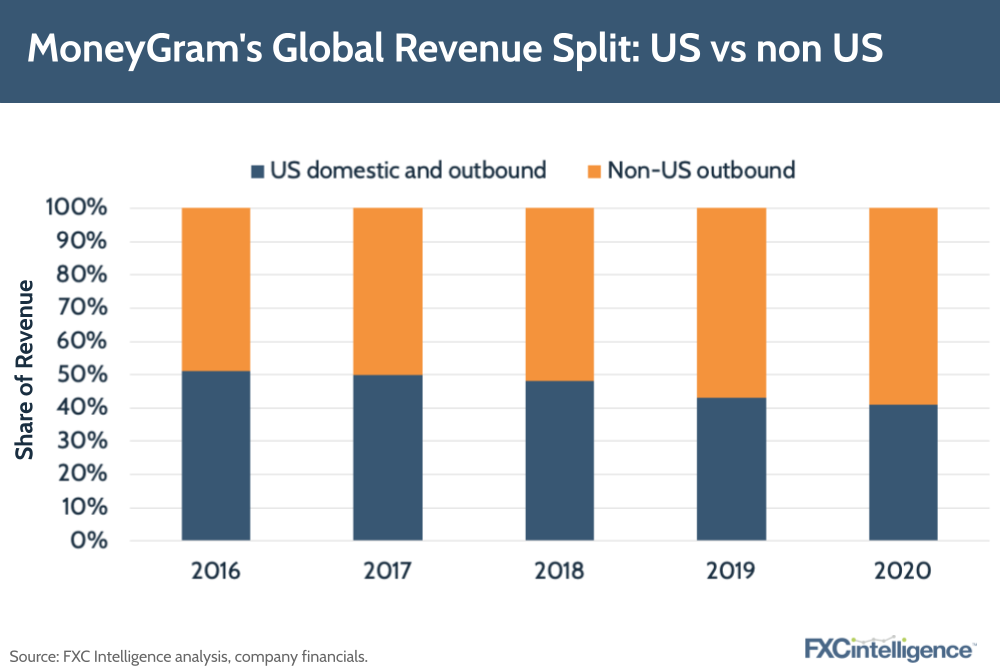

International market share is growing

While MoneyGram’s revenue remains dominated by US domestic and US outbound remittances, its international business has grown significantly over the past few years, having overtaken the US in 2018. The size of its international business is still far behind Western Union, presenting a big growth opportunity.

Figure 8

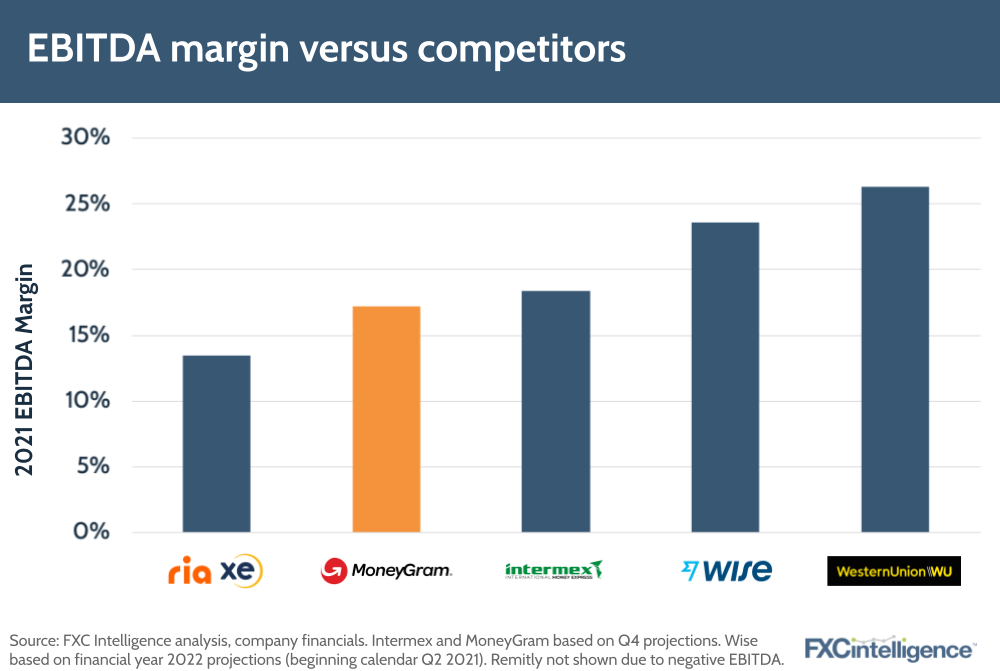

EBITDA margin falls short of competitors

While MoneyGram has a higher EBITDA margin than Euronet’s money transfer business, which includes Ria and XE, as well as Remitly, it has a lower margin than other rivals, including Western Union and Wise. If a new owner can add more scale to MoneyGram and potentially bring in new systems and even higher margin products, these could all plot a path to higher EBITDA. If MoneyGram ends up as a private company again, it is likely EBITDA will fall away as a core goal whilst it starts a new growth path and will come back only when its new owner looks to sell the business again.

Figure 9

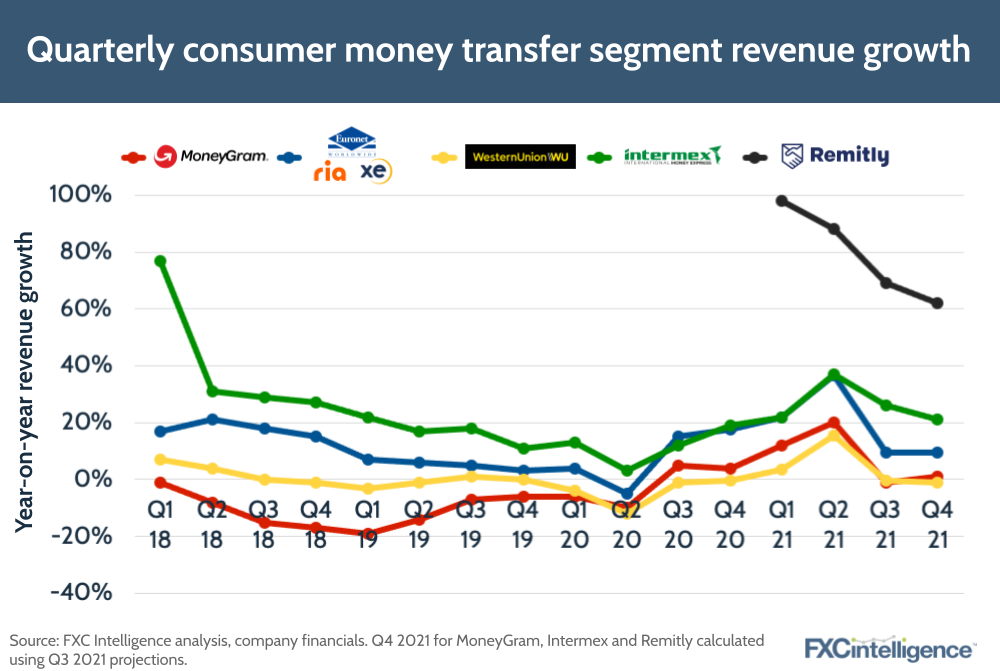

Solid pandemic recovery fueled by digital

The company’s quarterly growth had historically been weaker than some of its competitors – in part due to other constraints such as the restructuring of the business from its Deferred Prosecution Agreement. More recently, growth has improved significantly, particularly in terms of post-pandemic recovery driven by its digital business.

Figure 10

MoneyGram’s Digital Business

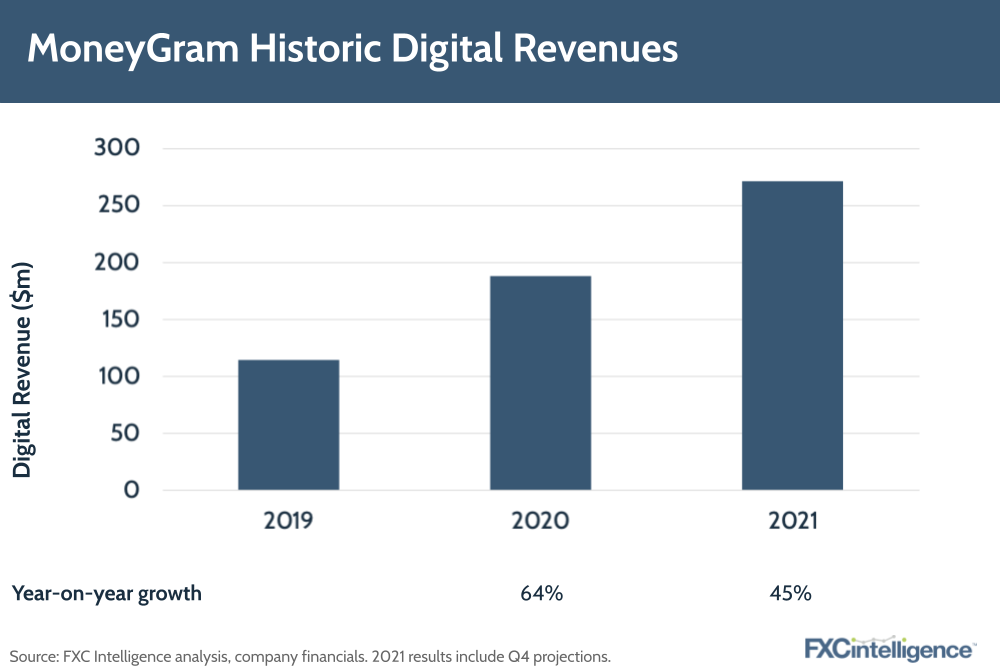

Showing strong digital growth

MoneyGram’s digital revenue has grown far more strongly than its overall revenue, and did not see the same dip during the pandemic. It is now more than twice its 2019 levels. Overall though, MoneyGram’s total revenue has declined in recent years and any new owner will be faced with turning this around as it re-focuses on growth.

Figure 11

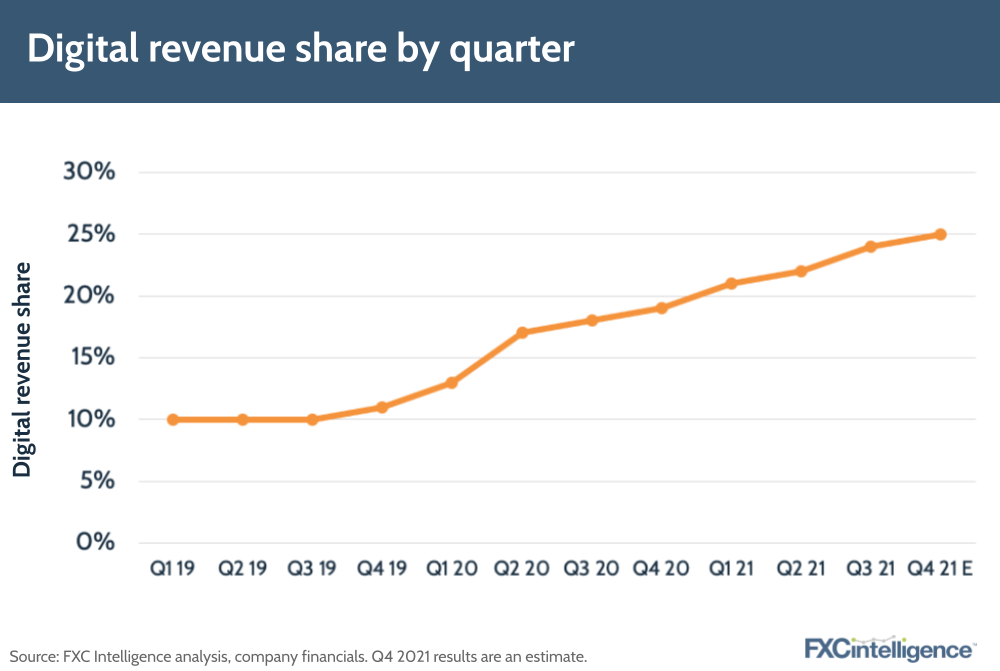

Digital revenue is taking an increasing share

Digital revenue is becoming an increasingly important contributor to the company’s top line, and is now approaching a quarter of all revenue.

Figure 12

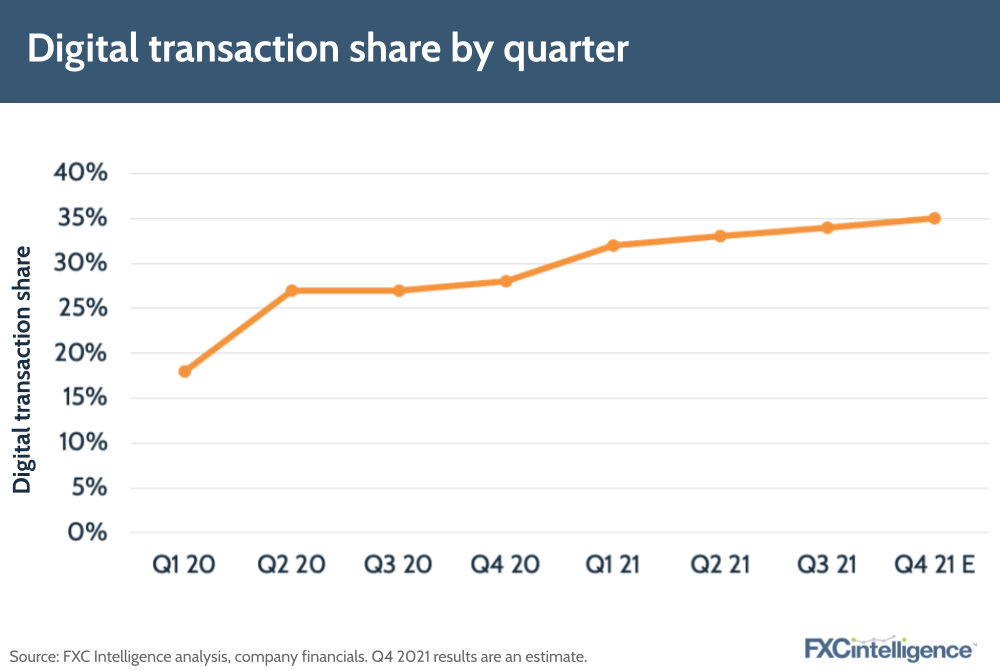

Digital transactions are becoming key

Digital transactions are similarly growing their share, and now account for almost a third of all of MoneyGram’s transactions. Digital transaction share sits above digital revenue share reflecting both the typically larger send amounts on digital and lower take rates.

Figure 13

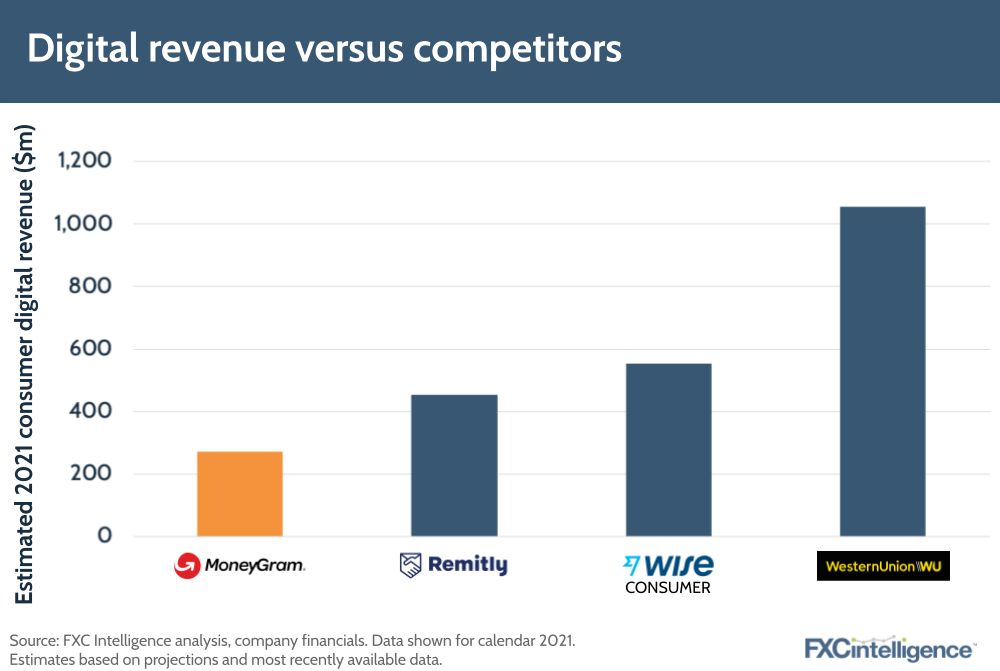

Digital revenue outstripped by rivals

While MoneyGram’s digital revenue is strong, it is by no means the largest of its competitors, with Western Union, Remitly and Wise all showing strong digital revenues too. However, with MoneyGram’s rate of growth its digital share may help it catch up. Notably others who have lower levels of digital revenue, such as Intermex, do not publish a digital revenue number.

Figure 14

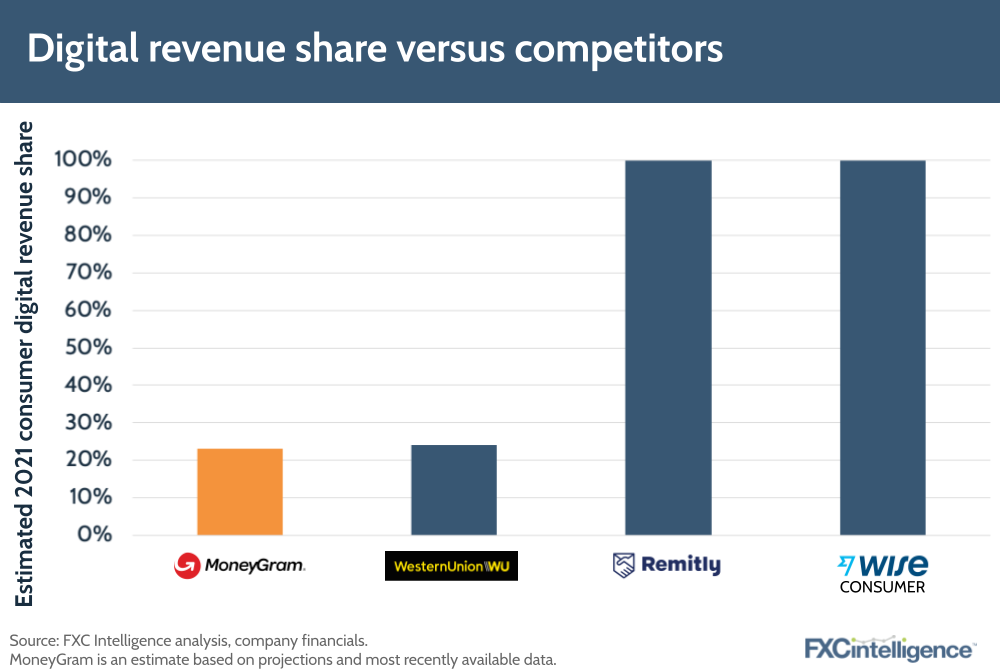

MoneyGram and Western Union are similar on digital share

MoneyGram’s share of digital revenue is similar to its biggest traditional rival, Western Union. Both saw their digital businesses transformed in the early part of the pandemic and have since broadly returned to normal growth rates.

Figure 15

Take Rate and Volume

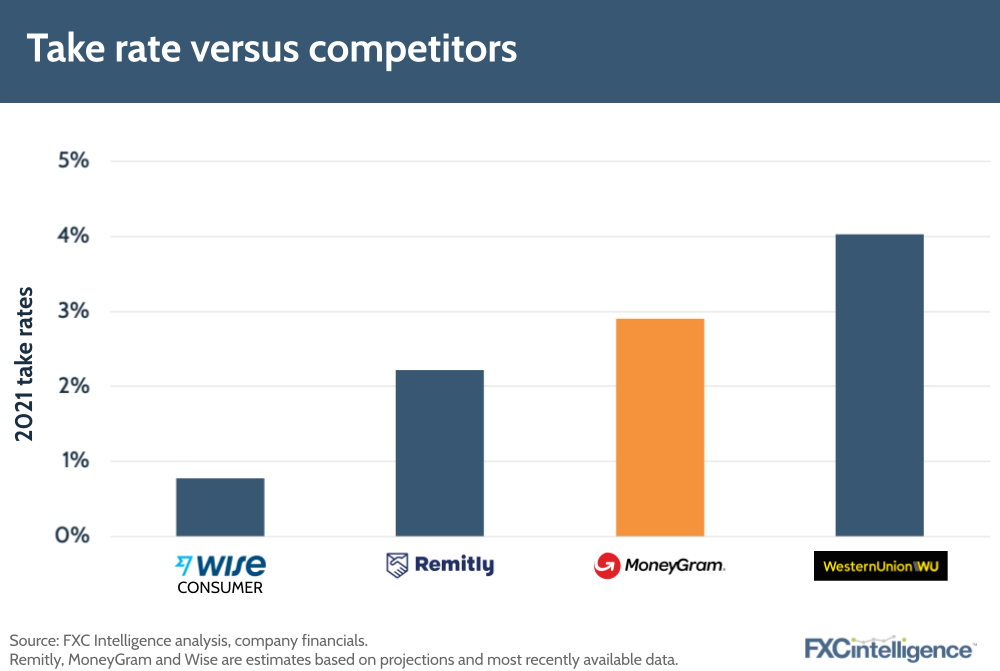

MoneyGram’s take rate is competitive

Although not the highest among its competitors, MoneyGram has a take rate that is above digital player Remitly and significantly higher than Wise who focuses on the consumer customer segment above remittances. Western Union, which has a much broader geographical reach, remains higher. We estimate Ria’s take rate to be similar to MoneyGram. MoneyGram has increasingly used lower pricing as a customer acquisition tool in the past few years, especially in the digital segment, and new owners will have the choice of profit or growth when they look to set pricing going forward.

Figure 16

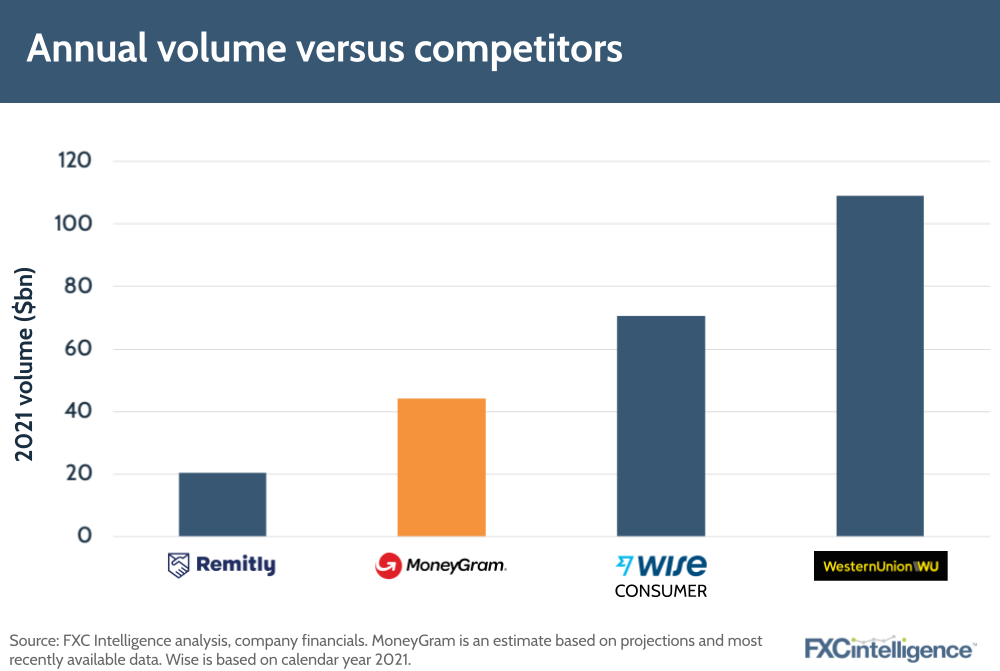

MoneyGram has plenty of room for growth in the market

While MoneyGram has higher revenue than Wise, its volume is around half that of the digital-only player, reflecting the significant difference in take rates and customer-type. MoneyGram still sits well behind Western Union, the remittance market leader. Other leading players such as Ria have an estimated similar flow to MoneyGram (Ria had c. $40bn of flow in 2020 and $54bn for the entire Euronet money transfer segment which includes XE). PayPal’s Xoom and Intermex do not report their flows. Zepz (WorldRemit and Sendwave) processed $10bn in 2020 but have not since updated this number for 2021.

Figure 17

Valuation and Revenue Multiples

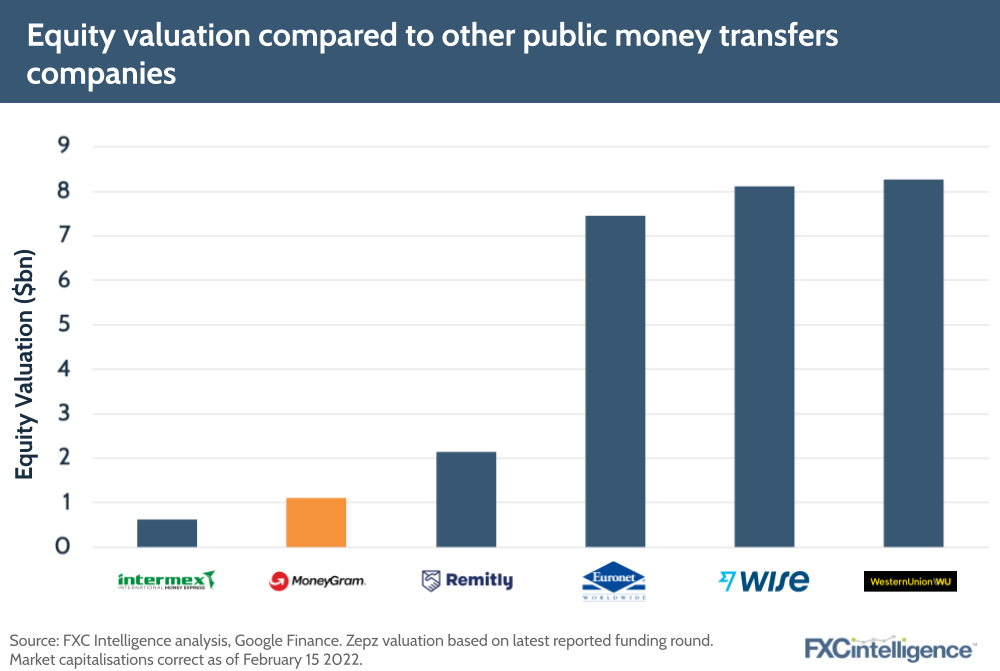

MoneyGram’s acquisition valuation is below most competitors

Based on the current acquisition price by MDP, MoneyGram has an equity valuation that is far below all but one of its competitors – Intermex.

Figure 18

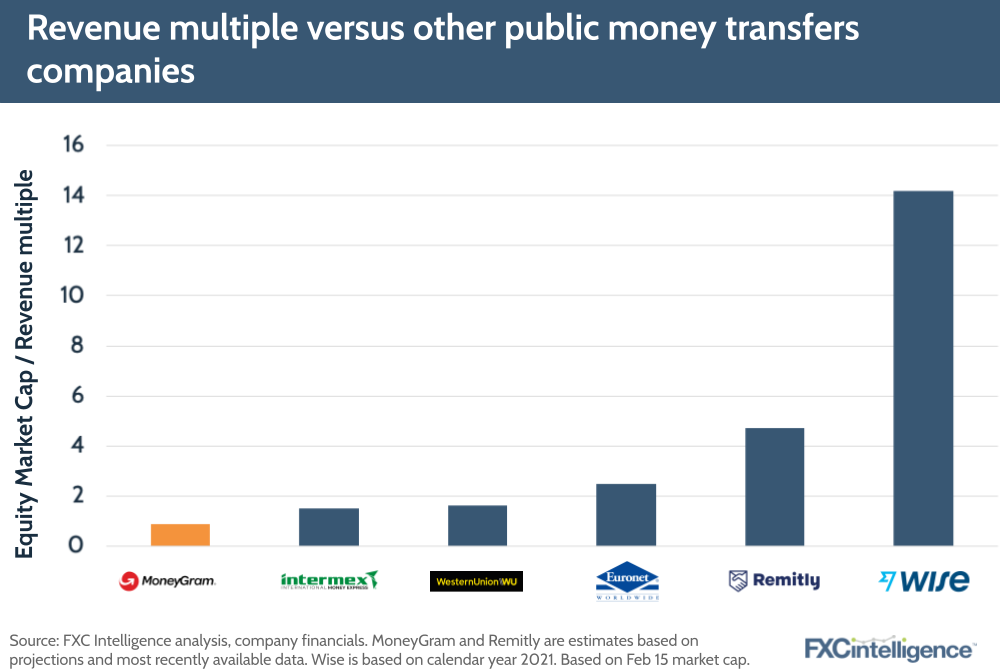

MoneyGram has the lowest revenue multiple of its competitors

MoneyGram’s revenue multiple is below all of its main competitors, with more digital-focused companies seeing the highest multiples. This is an indication that MoneyGram’s digital push has not yet translated into a digital-based valuation, likely as its overall revenue has declined in recent years. Note given the debt levels of MoneyGram, its multiples using enterprise value (including debt) look a little more favorable.

Figure 19

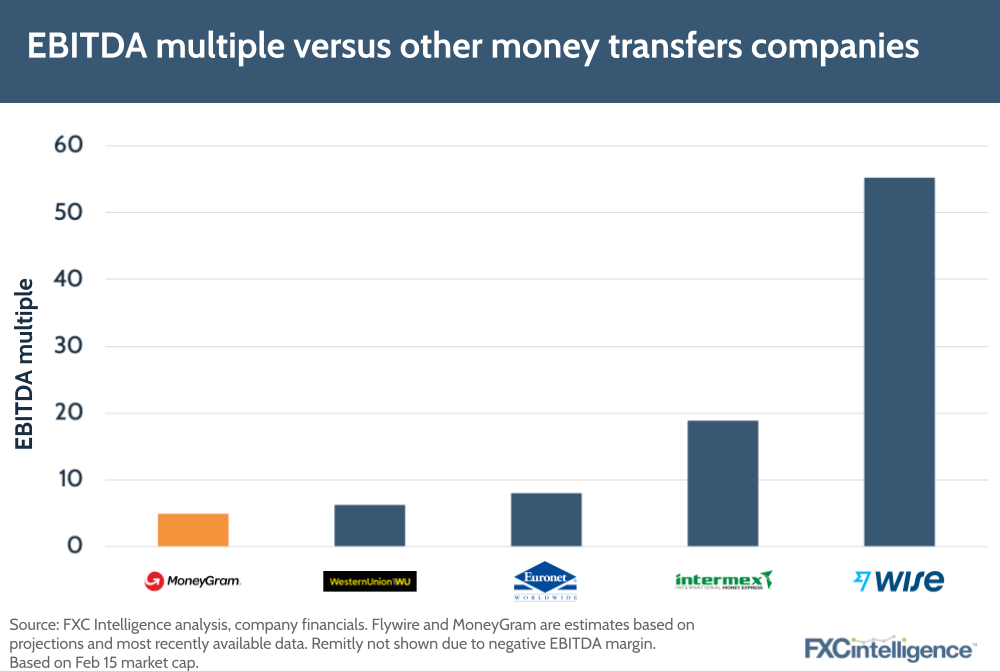

But its EBITDA mutiple is more competitive

However, MoneyGram’s Equity/EBITDA multiple is far closer to some of its rivals, including Western Union, suggesting the current valuation is based on EBITDA multiples for now. Again, if enterprise value is used, MoneyGram’s multiple moves up again too.

Figure 20

Upside Opportunities of the MoneyGram Acquisition

Ironically MoneyGram, one of the oldest players in the sector, may be going private at a time when everyone else is going public. This may give it a much-needed advantage to move away from a focus on quarterly earnings and EBITDA margins, allowing it to significantly invest in growth (trading short-term profitability) once away from the public markets spotlight. Going private may be the one way for MoneyGram to avoid the famous innovator’s dilemma.

There are a range of different upside opportunities a newly owned MoneyGram could pursue, all of them medium to longer term wins. Whilst MoneyGram has been working on some of these, public ownership has not provided a platform to aggressively pursue these as much as the company would like. Some of the opportunities include:

- Doubling down on digital and potentially even selling or splitting off its physical assets. The challenge here is that many digital transaction pay-outs are still to cash.

- Making crypto a centerpiece of the strategy, repositioning MoneyGram as a key part of the cryptocurrency ecosystem as an on and off-ramp.

- Utilizing the financials of the private equity backing to make more acquisitions. However, there are few obvious options with scale.

- Expanding outside of core remittance services to other financial services.

- Pushing the non-US part of the business, MoneyGram is still 41% a US business.

- Having a big customer acquisition push (ie very low pricing). However, this may be better done when there is even stickier customer proposition than just money transfers.

Key Acquisition Questions

Will anyone else be able to make a meaningful offer in just 30 days?

Go-shop periods often do not produce higher offers due to the short time frame and additional costs of replacing the first offer. A counter offer is likely to only come from someone already very familiar with MoneyGram and a clear strategy for its ownership.

Who else could make an offer?

This could fall into a number of groups:

- Western Union, the biggest player, has a playbook on this and has always been widely rumored to have courted MoneyGram. Could a deal be done this quickly?

- Ria tried several years ago and is unlikely to try again.

- Any of the higher growth digital remittance players. This would be a big acquisition for them and would require a partner to finance it.

- A crypto player. MoneyGram has some unique global money transfer assets and crypto players are long on cash.

- Another private equity player. Having likely already been through a process, a new private equity player that doesn’t know MoneyGram inside out would have a hard time making it happen.

- Another adjacent financial services provider, either in banking or the migrant services segment.

What’s next?

The next 30 days will determine if there is another twist in the story. Otherwise, MoneyGram and its new owners will begin the long path of regulatory and legal clearances and eventually delisting MoneyGram from the public markets. This is expected to be completed by the end of the year.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.