In the world of remittances, no major company is doing more on crypto than MoneyGram. Through key partnerships, MoneyGram is increasingly entering the cryptocurrency space not only for money transfers and settlement, but also to increase access for potential purchasers.

“We’re certainly bullish on the sentiment that from a consumer perspective crypto is here and it’s here to stay,” says Alex Holmes, CEO of MoneyGram.

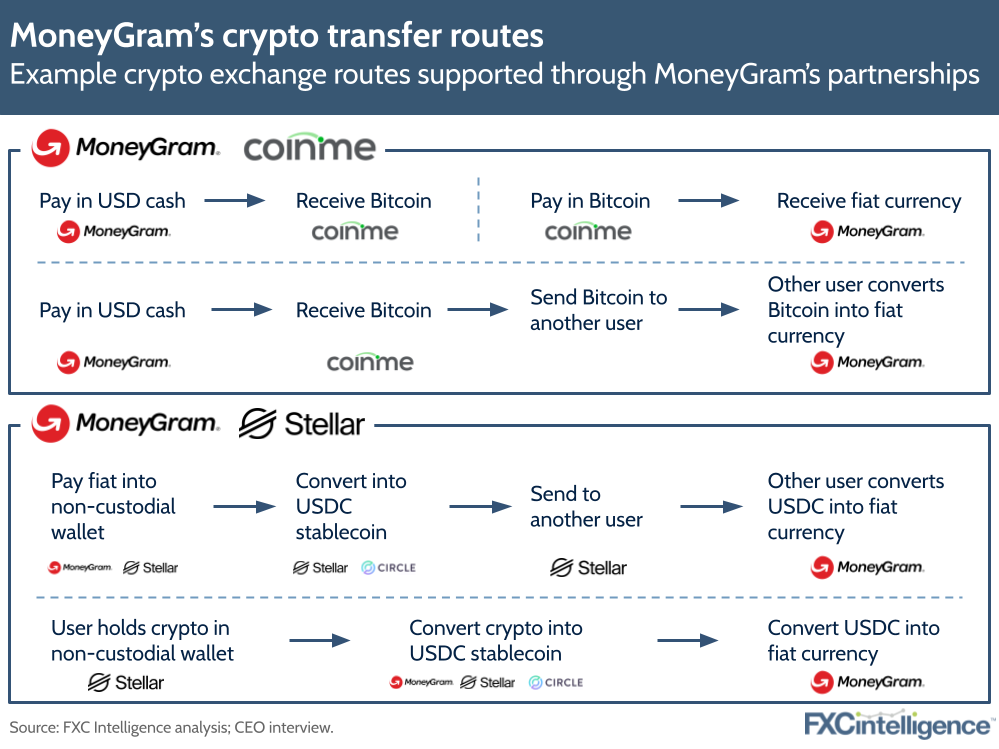

Having previously partnered with Ripple for cross-border payments and foreign exchange settlement before an SEC investigation into the blockchain startup ended the deal, MoneyGram now is exploring crypto money transfers through a partnership with Stellar. Launched in October 2021, this pilot is enabling MoneyGram customers to send cross-border payments using the Stellar blockchain network in Circle’s US dollar-backed stablecoin USDC. Customers can send money from MoneyGram outlets, with near-instant settlement and the ability to pay in and out in cash.

Meanwhile, the remittances player is also enabling customers to purchase cryptocurrencies using cash from its retail outlets through a partnership with Coinme, which in January this year advanced to see MoneyGram take a 4% stake in the company.

“We’re not betting the farm [on crypto],” says Holmes. “[But] it’s nice to be forward-thinking and forward-leaning in the space, and I think it’s something that we’ll continue to push and continue to do.”

MoneyGram’s place in crypto: Enabling interoperability

Crucial to MoneyGram’s approach to crypto is that it does not take a stance on whether cryptocurrencies are a tradeable security or a currency-like asset – in fact, the company does not at any point handle crypto directly.

“We’re only touching fiat, and then we’re interacting with others that hold crypto,” explains Holmes.

“So we’re a pass-through from crypto world to the fiat world, where we don’t have to buy, sell, and own crypto to offer it to the consumer. We’re enabling cash-in and cash-out of wallets, and the wallets are then linked to the ability to buy/sell crypto.”

This approach is reflective of what Holmes sees as MoneyGram’s opportunity in cryptocurrencies: to handle the currently under-served issue of interoperability.

“Cryptocurrencies continue to gain interest, gain share of wallet around the world, [but] we think there’s an important missing element to that, which is its ability to interoperate back into the fiat world,” he says. “We think MoneyGram is uniquely positioned to enable that effect.”

Interoperability is a continual refrain throughout MoneyGram’s crypto efforts, in what Holmes characterizes as a contrast with the wider cryptocurrency industry.

“Everything being created in crypto, blockchain is designed to make this whole fiat world better, yet no one’s really thinking about how to interoperate. They’re thinking about how to replace,” he says.

“In that space, it works beautifully. If you’re willing to take this coin for this coin, if you’re willing to trade with me, if we do it with a smart contract, it is an absolutely wonderful, beautiful application.

“Where it falls down is lack of interoperability back into the fiat world because of lack of integration, lack of platform stability, lack of any sort of backing behind the currencies, and then also it’s just very, very new. Most front-end payment platforms are not really designed today to integrate with crypto.”

Settlement with crypto: Benefits and challenges

MoneyGram first explored the potential of crypto-based settlements through its partnership with Ripple, which Holmes says was “incredibly successful” but also “brought to light a lot of challenges”, particularly in the settlement space.

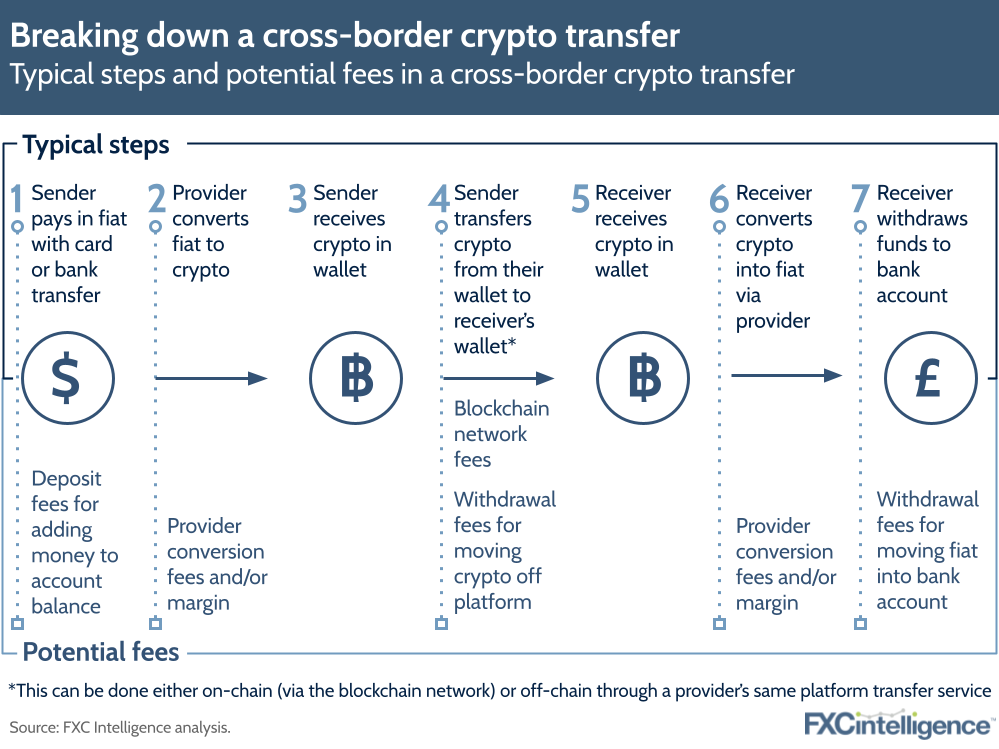

Among crypto experts, it is often taken as read that blockchain provides a faster, more efficient approach to settlement than established fiat solutions, although the reality is considerably more complex. Our own data at FXC Intelligence shows the costs of remittance transfer utilizing a digital currency can often be more expensive than traditional fiat methods, while regulations are also a concern.

“The less understood element of how MoneyGram works is that we preposition cash all around the world to run a net settlement engine; therefore we have real-time settlement,” he says.

“There’s a view from blockchain, a view from crypto, that that’s a little bit slow and antiquated. I think there’s a view from blockchain and crypto that traditional consumer money movement or business money movement through bank wire transfers is slow and antiquated and that crypto can help accelerate that.”

Holmes says that while he believes “that exists down the road in the future”, there are roadblocks.

For example, during the company’s Ripple partnership, MoneyGram faced considerable issues around eliminating unnecessary FX spreads on volumetric trading. This meant that sending money on a given corridor, for example US to Mexico, could be more expensive via crypto than without.

“Part of that was related to a two-step process,” says Holmes. “If you’re taking US dollars and trading for MXN, it’s one trade. If you’re taking dollars, trading them for [Ripple’s cryptocurrency] XRP, trading XRP for MXN, you’re getting what they call that two-step settlement process, and it actually adds a lot of unnecessary volatility.”

One potential solution to the two-step issue is the use of stablecoins, which unlike XRP are pegged to a fiat currency. However, the project also did identify benefits, namely that the crypto-based real-time settlement was “much more effective” than the fiat models in use at present, enabling trades to be executed faster than through today’s traditional FX models.

“If you could actually match your settlement through the blockchain with every transaction you were doing, you would be actually buying and selling real-time and matching off your transactions,” says Holmes.

“So as someone sent $300, you could actually do what a lot of people think we do today, which we don’t do today, is actually move that particular $300 real-time, which you can do on the blockchain and you can do through crypto and you cannot do in the fiat world today.”

Holmes says there is “a long way to go” before this could become standard, but argues that there would be significant potential benefits to the approach.

“If you could begin to pair things off real-time, that would free up quite a bit of liquidity, not just in MoneyGram, but in the financial system in general,” he says, adding that this would be in sharp contrast to today’s standard of overnight settlements, which are “how everything runs today”, meaning implementation would “take quite a bit of time and quite a bit of global coordination”.

“That efficiency that could be gained through real-time connections and real-time settlement of individual transactions could actually take away a lot of friction points and a lot of challenges on a global settlement basis.”

To understand the full range of data coverage we have on crypto, please contact us

De-risking corridors

While blockchain settlement has potential benefits for companies, Holmes also sees it having benefits for markets with greater levels of fiat currency volatility.

“Ideally, a blockchain crypto settlement platform would help support the more volatile currencies and actually help stabilize that and create much more seamless operations in those markets,” he says.

“If you could somehow de-risk the Turkish lira or you could de-risk the Bangladeshi taka on a trading volumetric basis, the results of that could be incredibly powerful.”

Here he warns that there are potential “geo-economic political interoperability challenges”, where currency moves come as a result of political actions, military activities or other large-scale events.

“Big drops in oil prices or other commodities can drive currencies to fluctuate quite rapidly,” he says. “Conceptually, if you were in a blockchain stable currency-type world, that volatility would go away.”

However, there are potential challenges in the form of national interests. Many cross-border movements of money are slowed by protections put in place by sovereign nations looking to avoid dollarization, mass outflows or mass inflows that create the threat of destabilization. And Holmes warns that crypto creates potential threats here if not properly controlled.

“As much as the purest idea of a crypto is to create democratization for consumers, it also potentially could create destabilization for governments as well, which is not where you want to be.”

Coinme: Buying and selling crypto through MoneyGram rails

While some aspects of crypto’s potential remain a long way off, MoneyGram is already involved in projects aimed at democratization for consumers, notably in the form of its partnership with Coinme.

Established to combat issues around access to cryptocurrency, Coinme provides US-based users with a way to convert cash into cryptocurrency without needing to link bank accounts or require a user to have access to a credit or debit card. As a result, it widens access to crypto, including to underbanked users in the country.

Coinme has provided this service initially through Coinstar machines, which are normally used to consolidate spare change and are found at supermarkets and other major retail outlets across the US. Through the partnership with MoneyGram, the number of outlets customers have to convert cash to crypto has increased significantly, with the added ability to convert crypto back into cash.

“The idea behind Coinme and the idea behind the partnership was to expand the interest, expand the reach of something like Bitcoin to more mainstream Americans,” says Holmes.

“So we enter the scene with the idea of, how do we take that kind of model with Coinstar, extrapolate it, expand it into MoneyGram for cash in, but then also now if you want to sell your Bitcoin and go pick up your cash, that becomes an interoperable feature that didn’t exist before.”

The ability to cash out immediately is a key benefit, says Holmes, who contrasts this with his experience using Coinbase, one of the world’s biggest crypto exchanges.

“I think it has a lot of wonderful features. But one of them that’s not so wonderful is when you load a thousand dollars, they’ll tell you can’t have that money back for four, five, six, seven days. When you sell your Bitcoin, you don’t just get to put that money back into your bank account – it takes a couple of days,” he says.

“So the ability to say, “Click here. Go pick up $500 at CVS in five minutes,” is, I think, a really nice add-on feature and that’s an important part of making cryptomore interoperable for consumers.”

Increasingly, widening ownership of crypto is also translating into its use for remittances, with Holmes pointing to the US-Mexico corridor as an example.

“$40bn goes into Mexico every year from the United States. I think they estimated in 2020 or through the first half of ’21, $1bn to $2bn across the border in crypto,” he says, adding that this is so far in addition to the traditional fiat remittances, rather than as a replacement for it.

“They’re supplementing that and sending Bitcoin home so that they can have access to a new financial savings platform so that they can look at and become part of a system that I think they otherwise feel left out of, meaning the traditional fiat markets,” he says.

“There’s a huge correlation between consumers in the remittance space and those that are also interested in the crypto space.”

MoneyGram, Stellar and Circle: Adding payment rails to crypto

Given this growing interest, it’s perhaps no surprise that MoneyGram has opted to explore the potential of crypto-based remittances through its partnership with Stellar, which enables near-instant transfers of Circle’s USDC stablecoin.

However, Holmes highlights key differences between the typical customer profile in MoneyGram’s partnerships with Coinme and Stellar – and therefore the difference in opportunity.

“On Coinme one, we’re talking more about mainstream consumers that are at the lower end of the economic spectrum. When you think about Stellar, it’s almost the opposite,” he says.

“These are people now that are really sitting in the coin world, in the crypto space, that have oftentimes non-custodial wallets, meaning they own the keys to their crypto. They’ve either gotten it through trading, they’ve gotten it through mining, they’ve gotten it through staking, they’ve done something.”

Such non-custodial wallets are an effective way to store all forms of crypto, but they lack any form of connections, and therefore interoperability to the wider payments world.

“Stellar is one of the leading providers of non-custodial wallets on the Stellar blockchain. They sort of act a little bit like a Linux platform where they’ve got free software; people can build wallets on their Stellar platform and you can hold your crypto,” he says.

“What Stellar believes, however, is very similar to MoneyGram believes: that interoperability back to fiat can be a key component of expansion of non-custodial wallets and create the opportunity for those non-custodial wallets to actually have more formalized payment rails. So as you think about the world at large and you think about the proliferation of crypto and blockchain, that opportunity is big.”

The current trial is Stellar and MoneyGram’s first efforts to add payment rails to these wallets, in the form of USDC.

“If you can take your crypto and actually convert it to a stablecoin, and then through USDC you can actually exchange that now on the MoneyGram platform into cash or load cash into your non-custodial wallet, suddenly your non-custodial wallet isn’t so non-custodial anymore,” he says.

“It’s still non-custodial because you haven’t given your keys to somebody, but now you actually have a payment rail and a way to sort of get money in and out.”

This is significant because although it can be used for remittances, it has far broader applications for transferring money between fiat and crypto – whether across borders or domestically. Companies that have built wallets on the Stellar blockchain can even integrate these rails into their own wallets via an API, adding support for instant pay-outs via MoneyGram’s services.

“Say you’re holding Stellar Lumens in your wallet. The first step is convert to USDC coin. Then you say, ‘Cash out’,” explains Holmes.

“Those USDC coins are sent to Circle to expire, and Circle simultaneously notifies MoneyGram to create a transaction so that that consumer can access their funds.”

Meanwhile, compliance processes are happening alongside, with Elliptic providing chain analytics to ensure the coin is genuine and automatic connections to MoneyGram’s KYC ensuring this is run as normal. Furthermore, as an added bonus for the company, MoneyGram is sent the money before the consumer collects it – something that Holmes says is a first.

“Usually we’re the last ones to be paid,” he says. “So from a settlement perspective, it’s really slick and takes away a lot of that settlement risk. But secondly, the consumer then has access to their funds instantly.”

MoneyGram at the intersection of crypto and fiat

While MoneyGram’s efforts in crypto are at a relatively early stage, these connections have, says Holmes, the potential to give the company unique capabilities on a global level.

“MoneyGram operates all around the world, and effectively we’re a money transfer remitter, but we’re also in many respects kind of a foreign exchange outlet. If you start to think about interoperability between crypto and fiat, you think about the Stellar platform and you think about what Coinme’s doing, MoneyGram can play a really interesting role in many, many markets around the world,” he says.

“You could lay in crypto in a foreign market, convert it to local fiat, and cash it out. You could put local fiat in, convert it to crypto, move it around the world. That becomes super interesting and something that’s very different from what others are capable of doing today.”

This could potentially see MoneyGram become a “global exchange” between crypto and fiat, enabling the easy movement between the two, whether domestically or cross-border.

“That’s quite a bit of a way out, but it’s on the doorstep of the next thing you can do.”

Contact us to find out how our crypto data can help your business