Q3 2023 has once again seen payment processors see growth, but at more muted levels than during the pandemic. We look at the key trends from the latest earnings season among publicly traded payments processors.

Publicly traded payment processors saw another solid quarter in Q3 2023, although the industry continues to face tougher trading conditions than a few years ago. While not all investors responded positively and there are some signs of challenges, in general top-line results have been good for the sector.

In this latest instance of our report series, we review both the latest and historical quarterly earnings for the main publicly traded payment companies in order to get a sense of how the industry is evolving as a whole, where the key trends are and who is emerging on different metrics.

This sees us include a broad range of payment processors, including some who focus on specific niches as well as those that are consistently in direct competition. These are: Adyen, dLocal, Fiserv, Global Payments, PayPal, Paysafe, Worldline, Worldpay and Square. For some areas, we use data for Worldpay’s parent company FIS, which is currently in the process of spinning Worldpay out into a standalone company, while we also use data for Square’s parent company Block. We also only use Worldline data for some metrics as the company only provides full results on a half-yearly basis.

The report sees us compare all companies on each metric for whom there is comparable data available, as well as providing keyword analysis on available earnings calls for key subjects.

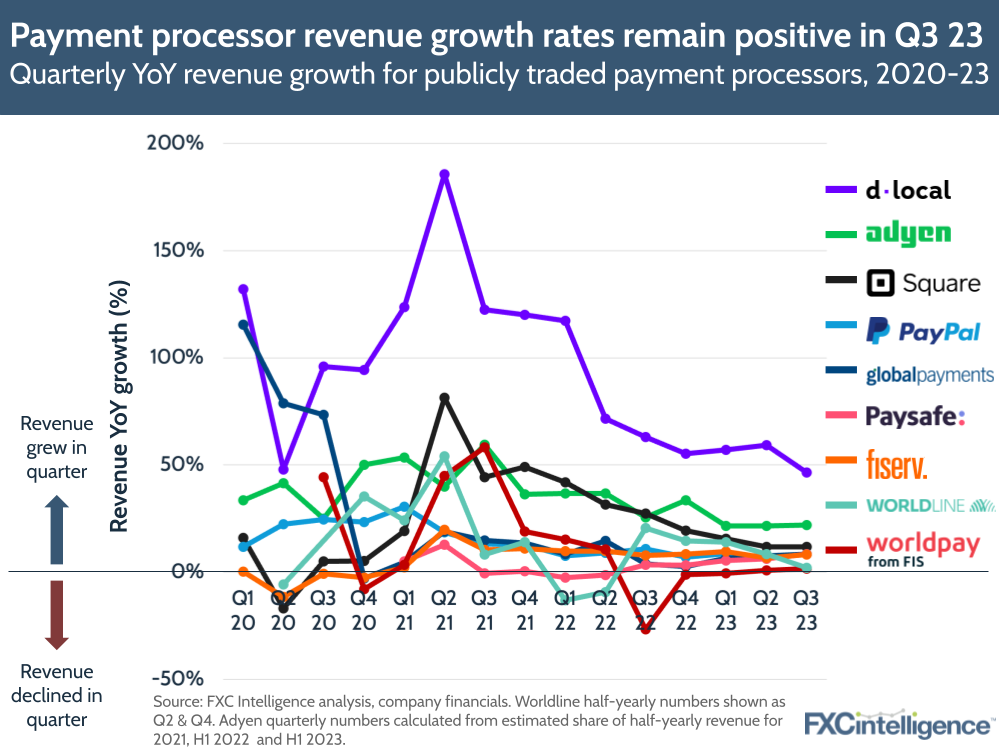

Revenue growth among payment processors in Q3 2023

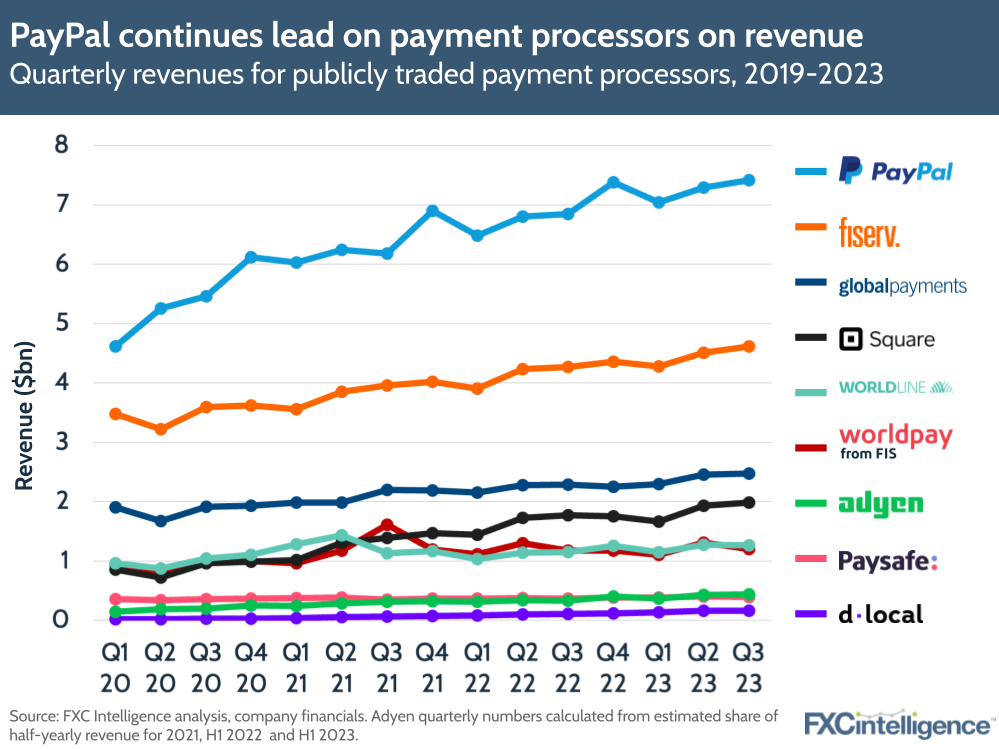

As is to be expected, PayPal continued to lead payment processors on revenue in Q3 2023, with its revenue greater than the next two players, Fiserv and Global Payments, combined.

Lower down the rankings, companies have largely retained their positions this quarter, although Worldline pulled slightly ahead of Worldpay in Q3, having been behind in Q2.

On growth, however, the picture is quite different. As the smallest player in the group, and also the most recent to list publicly, emerging markets-focused dLocal is still at a very different stage of growth to some of the more long-established companies. While it saw the lowest YoY revenue growth it has seen since it went public, this was still north of 45% in Q3. It was also 25 percentage points above Adyen, the company with the next highest growth, which took the unusual step of putting out a quarterly trading update in Q3 following investor concerns.

While the range of growth rates varied significantly this quarter, all were positive, which is often not the case. Four of the nine companies – Fiserv, Global Payments, PayPal and Paysafe – all reported growth of 8%, while Square sat above this on 12% and Worldline and Worldpay both reported 2% growth.

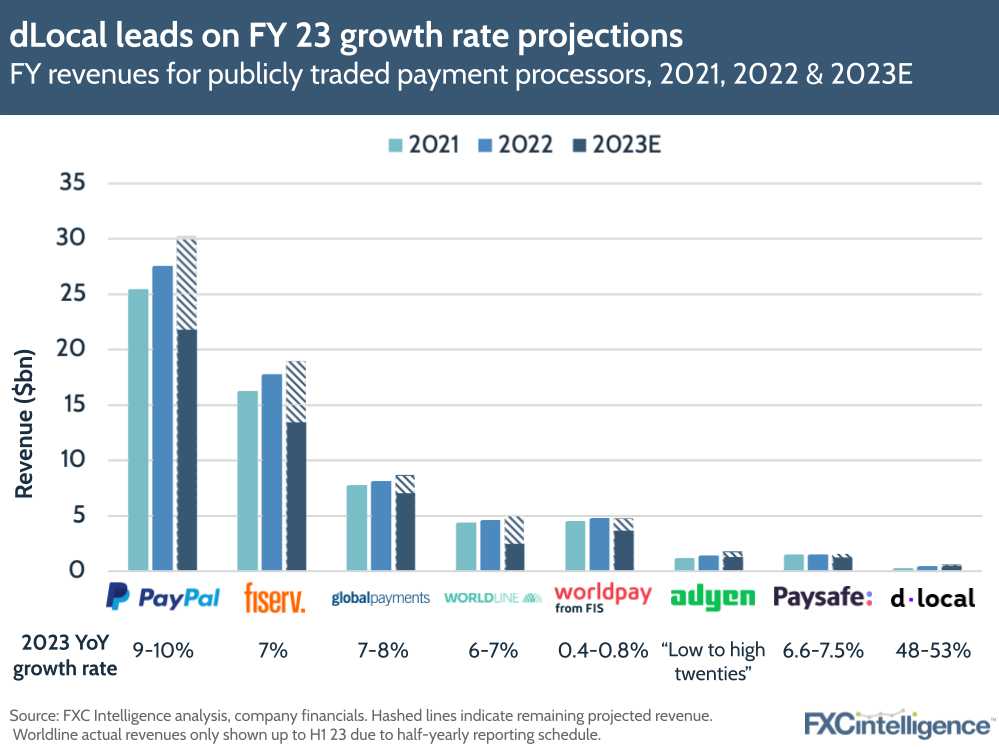

These results also saw companies review their FY expectations, providing an update on how each player anticipates performing over the course of 2023. While some, such as Paysafe, restated previous expectations, others, such as Fiserv, increased their full-year projections as a result of their Q3 results.

For many players, their full-year projected growth rates are expected to be similar to those for Q3, although many are anticipating slightly higher FY performance as a result of the expected seasonal uplift from Q4. Notably, Worldpay is the only company projecting lower FY performance than their Q3 growth; however, as the company is in the process of being spun out into a private organisation, this is a slightly different scenario to the other players.

Investor reactions to Q3 varied significantly between different companies. Paysafe saw an upswing in its share price on the publication of its result, possibly as a result of its reaffirmation of previous FY projections, while Block and PayPal also saw a warm investor response.

By contrast, Worldline saw a significant drop as a result of slower-than-expected growth, while dLocal also saw a decline. Notably, some players who saw a rise remain below their prices at the start of the year, including Block and PayPal, reflecting the tougher operating conditions this market is currently experiencing.

Earnings and profit metrics divide payment processors

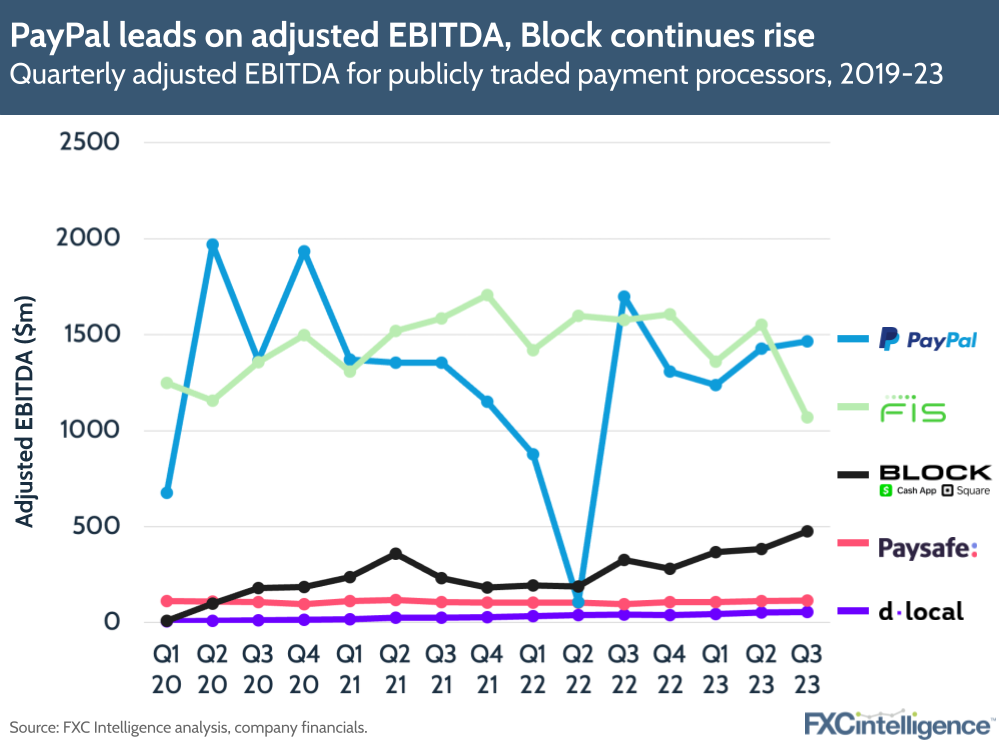

Looking at the companies through the lens of adjusted EBITDA provides quite a different picture of who the sector’s leaders are. Among companies who have reported this metric on a quarterly basis, PayPal has returned to the lead due to a dip by FIS, with Block coming in third after several quarters of consistent growth. As smaller companies, PayPal and dLocal unsurprisingly have smaller EBITDA.

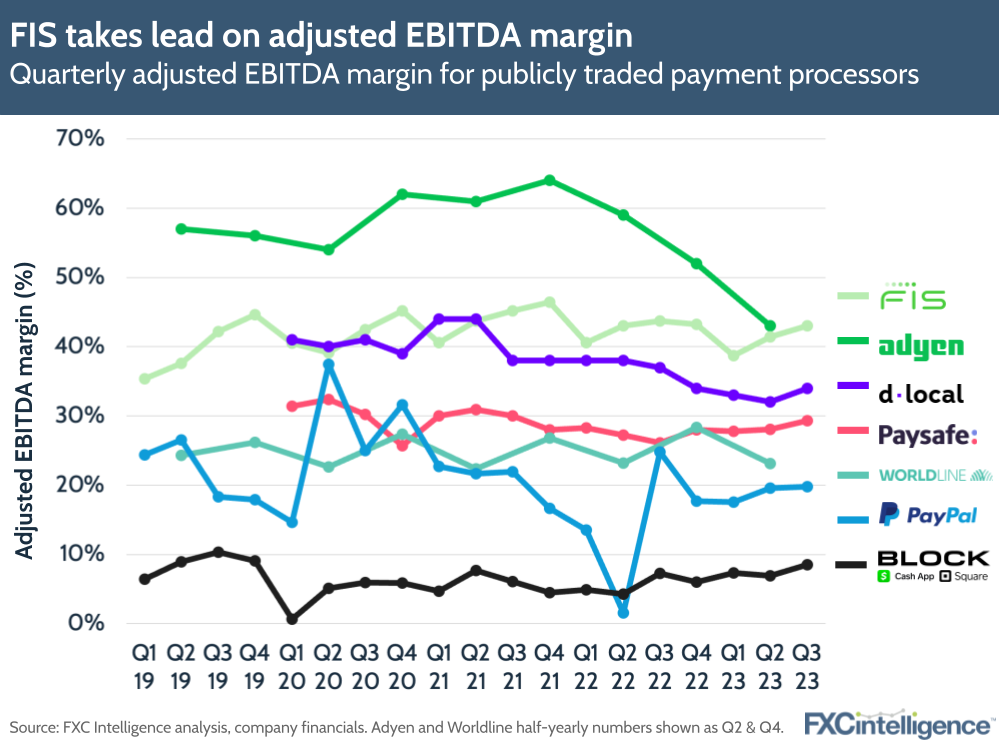

However, looking at adjusted EBITDA margin provides a very different view. dLocal has the third highest adjusted EBITDA margin after FIS and Adyen, which only reported this metric for H1 2023, with Paysafe coming in close behind. Meanwhile, PayPal’s margin is a full 10 percentage points lower than Paysafe’s, while Block is the only company below 10% on this metric.

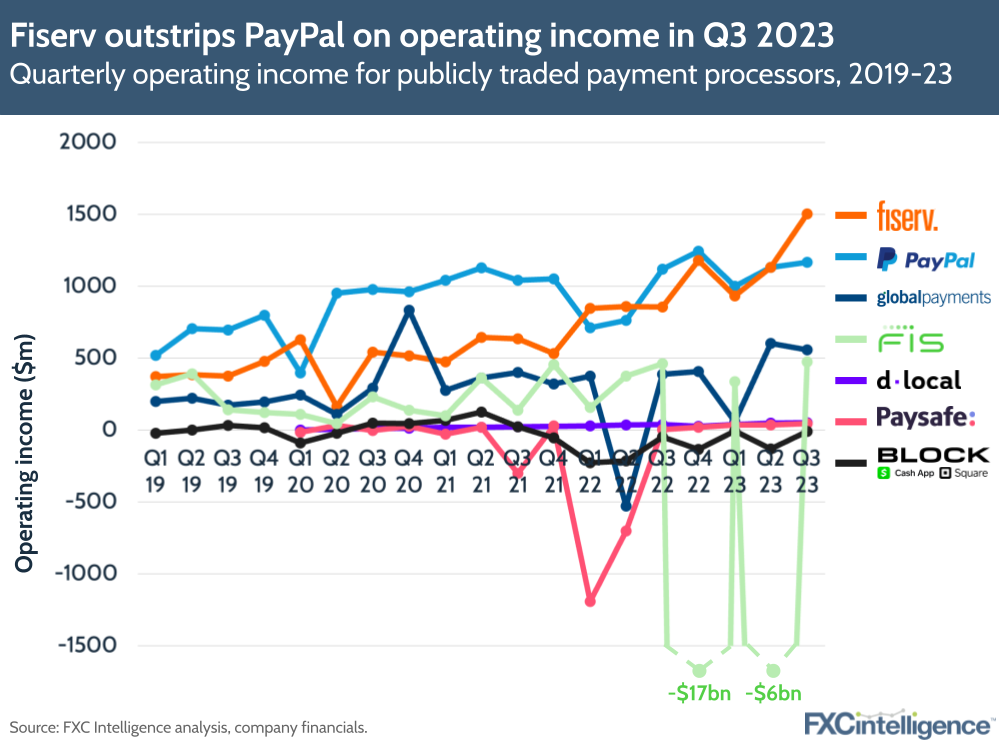

Meanwhile, operating income sees Fiserv take the lead from PayPal, having spent multiple quarters running close to one another. Whether this turns into a full breakaway from the online payments giant remains to be seen, and Fiserv will need to have a multiple-quarter run before this can be called a trend, but it is the strongest lead on PayPal the company has taken on this metric.

Elsewhere FIS has rebounded from significant one-off costs last quarter to take fourth place shortly behind Global Payments, while Paysafe has risen to be in line with dLocal and slightly above Block.

How is global card pricing impacting domestic and cross-border purchases?

Take rate, volume highlight areas of opportunity

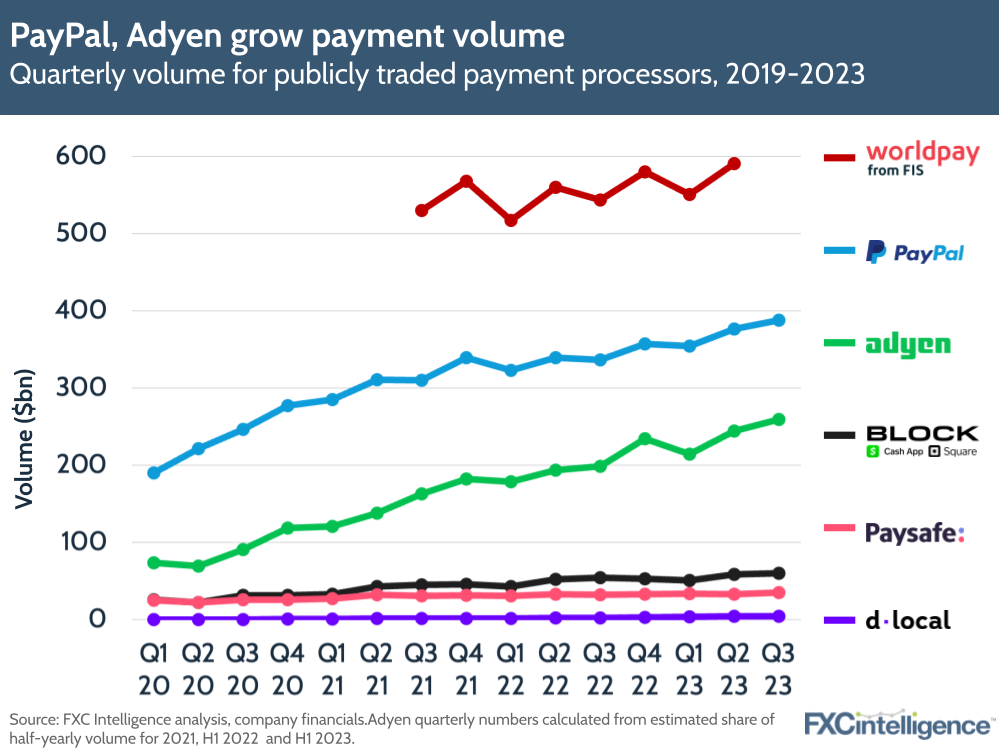

While not all companies report payment volume, those that do are continuing to see a consistent rise in the amounts spent, reflecting the wider increase in cost of goods that we have seen in most countries over the past few years.

While we do not have a Q3 2023 metric for Worldpay, we can assume that it likely retains its number one position among payments processors for volume. Beyond this, PayPal continues to run ahead of Adyen, although it is growing at a slower rate – 15% YoY for the quarter compared to Adyen’s 21%.

Here, dLocal’s growth rate remains the most significant, at 69%, while Block and Paysafe have the lowest at 11% and 8% respectively.

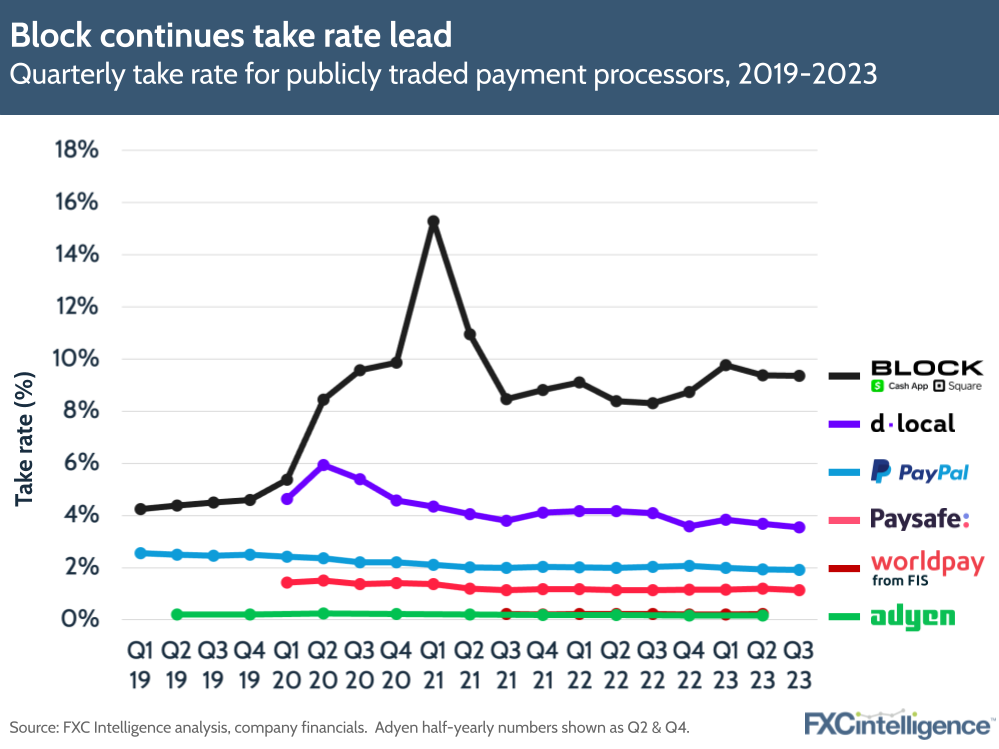

Meanwhile, on take rate, most players saw a slight reduction on both a QoQ and YoY basis. Leader Block saw one of the smallest contractions, reducing 3 bps between Q2 and Q3 2023, and increased by 105 bps YoY. This was followed by PayPal, which saw a QoQ drop of 3 bps and a YoY drop of 12 bps.

dLocal saw similar, with a QoQ reduction of 13 bps and YoY reduction of 54 bps, while Paysafe reduced 7 bps QoQ and was flat YoY.

The consistency of these reductions across different players suggests that this is far more reflective of the market conditions than the performance of each individual company.

How is cross-border pricing being approached by ecommerce players globally?

Headwinds on the rise as AI discussion drops

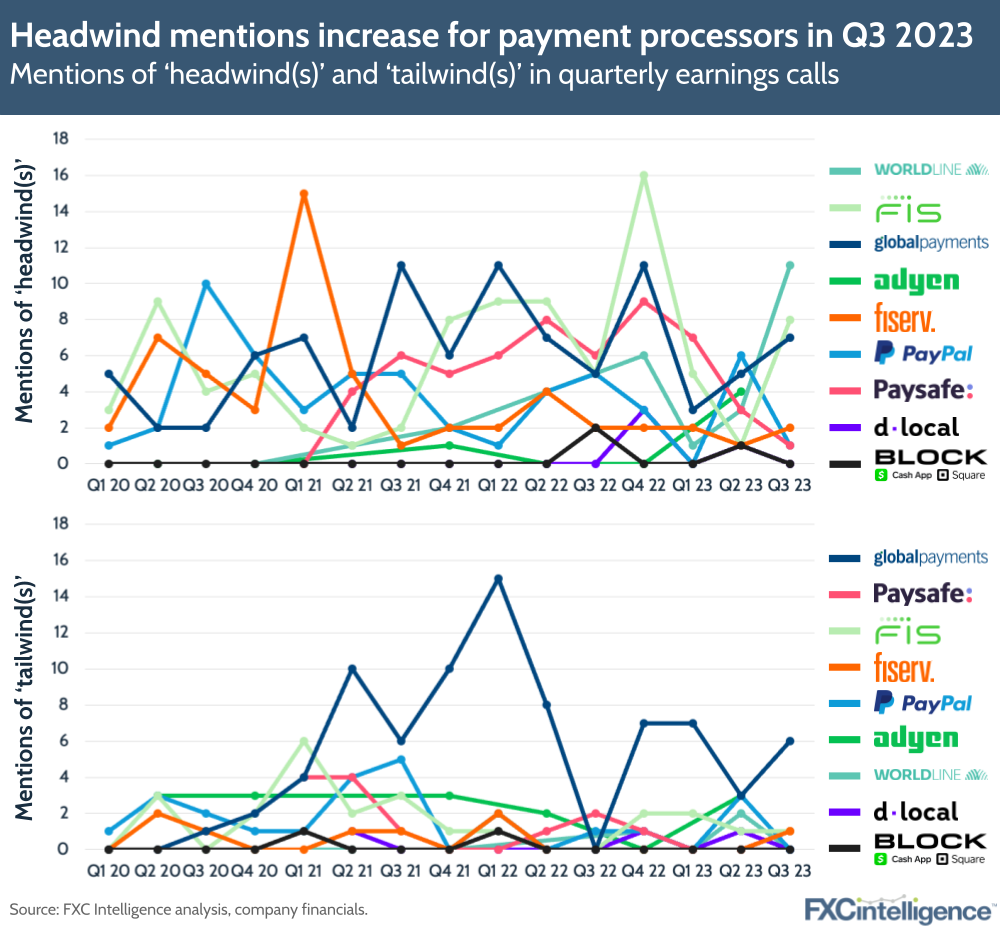

While the financial performance of the different players suggests some challenges in market conditions, this is also reflected in keyword analysis of the different companies’ earnings calls.

A review of the incidence rate of a selection of keywords across all of the players for all available earnings call transcripts between Q1 2020 and Q3 2023 does highlight some trends that have developed, with the past few quarters providing particular insights into the current market conditions.

The frequency of discussion around ‘headwinds’ and ‘tailwinds’ indicates that the former is more consistently used by almost all of the payments processors, with the possible exception of Global Payments. However, there has also been a notable uptick in mentions of headwinds in this last quarter among many players with little to no equivalent uptick in mentions of tailwinds – an indication that companies feel increasingly under pressure from external factors.

This is also reflected in the sharp increase in use of the term ‘macroeconomic’ and related words by some players, which had been on the decline prior to Q3 after seeing an upswing following Russia’s invasion of Ukraine.

However, there was not a sharp increase in use of the term ‘negative’ versus the term ‘positive’, suggesting that while companies are seeing increased challenges, this is not yet translating into significant performance-related concerns.

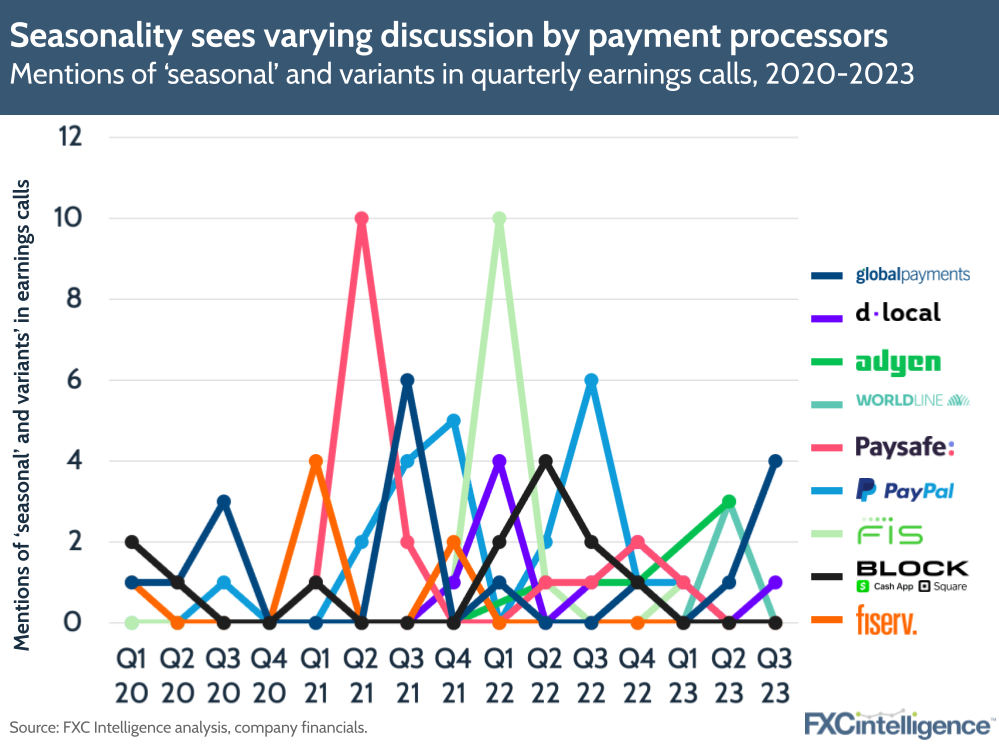

It is likely that some players will be relying on Q4 for strong results due to the sharp upswing that holiday season-related purchasing often has on the ecommerce and payment processing space. As a result, it was interesting to add a review of the term ‘seasonal’ and its variants this quarter. Here we were unsurprised to see that use of the word ‘seasonal’ was itself seasonal, although appears at different cadences for different players.

This suggests that companies choose to discuss the seasonal nature of their businesses at different times of the year from each other – in some cases likely to reflect on the performance of a seasonally improved quarter, while in others likely to be reflecting on season-specific weakness.

It will be revealing to see which companies see an upswing in this term in Q4 2023, particularly given the tougher economic climate.

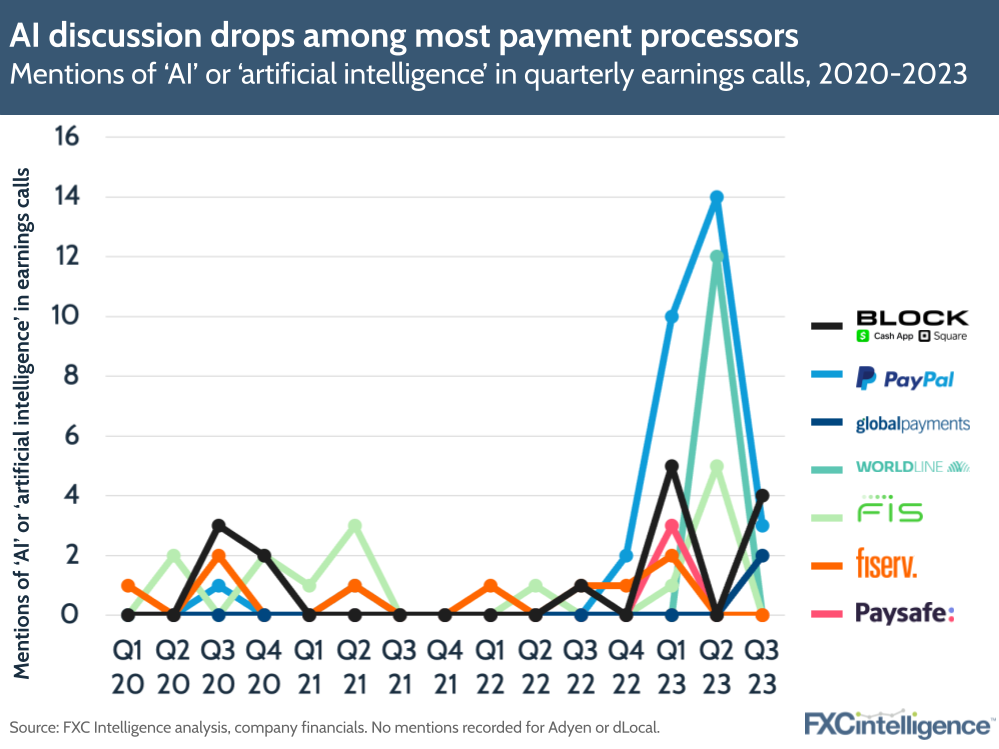

Finally, analysis of discussion of the term ‘AI’ or ‘artificial intelligence’ was particularly illuminating this quarter. While payment processors have seen a much sharper upswing in discussion of the topic than other cross-border payment companies, particularly remittances, Q3 saw a very significant downward trend in mentions from many players after a sharp jump earlier this year following the release of generative AI platform ChatGPT.

Whether this is a one-off quarter or reflective of a broader cooling of AI in the space remains to be seen, but it does suggest that companies do not perceive AI to be of as much interest to investors as they did a quarter or so ago.