Worldline bore the brunt of market slowdowns in Q3 23, having reported YoY organic revenue growth of 4.8% to €1.2bn – slower than the 10% growth during the same period last year. The company’s share price more than halved as a result of the report, and its warnings about a slowdown in the European market also catalysed share price declines for several other Europe-focused payments players.

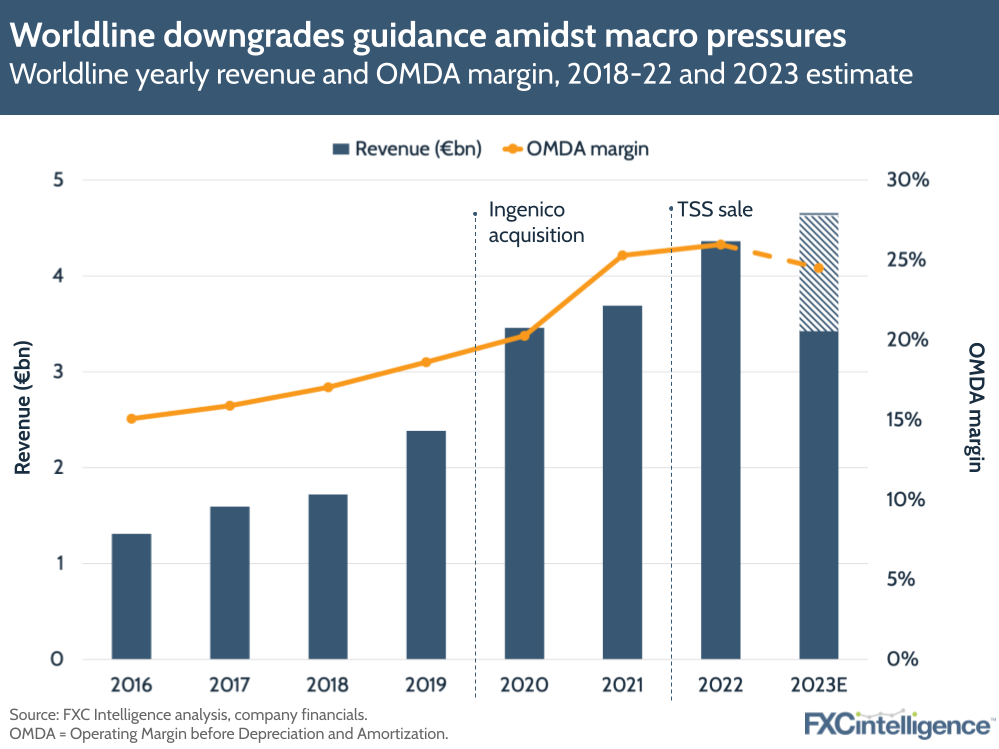

As a result of slower growth, Worldline has downgraded its guidance with a lower revenue growth expected (now between 6-7%, compared to 8-10% previously) and around a 150 bps decline in its OMDA margin, which it previously forecast would rise by 1%. However, the company has still seen some notable wins during the quarter.

Worldline sees deterioration in core markets

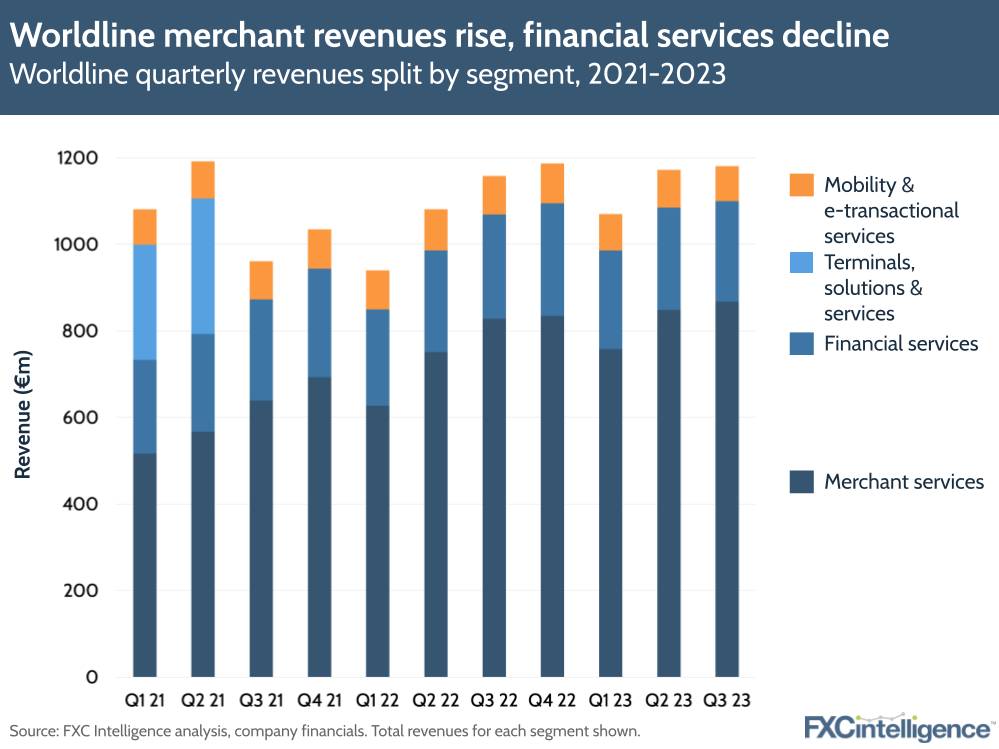

Merchant services rose 7.6% (10% without Germany) to reach €868m, driven by 7% growth in transaction volumes. Worldline noted however that there has been a macroeconomic slowdown that has led to much lower discretionary spending in Germany and other core markets. As a result, revenue and transaction growth were slower than Q3 2022.

The company also terminated some merchant relationships after it updated its risk strategy following an increase in cybercrime and ‘market constraints’. These relationships, it said, could lead to a €130m impact on H2 23 and H1 24 revenues going forward.

Having said this, the company saw high single-digit growth in commercial acquiring and double-digit growth fuelled by digital commerce and some big new customer signings, including German flag carrier Lufthansa.

Breaking down Worldline’s revenues by segment

Looking at the company’s other segments, financial services declined by 2.9%, which the company said was down to delayed signings across card-based payment processing activities, though it did see strong growth across its digital banking offering in Belgium and France. Meanwhile, its smaller mobility & e-transactional services division remained stable, compared to a slight increase last year.

Worldline’s slump runs contrary to some of the other successes it has seen in Q3 2023, including signing a new partnership with Credit Agricole to create a new major merchant payments player in France and launching a €600m five-year bond issue. The latter of these is interesting, as Worldline has seen a record fall in its share price, so it will be prescient for investors to monitor if the European slowdown continues into Q4.

Moving forward, Worldline aims to focus on its OMDA and expect this to improve by €100m in 2024 vs 2023. It continues to integrate cloud-based PoS platform Ingenico and is also launching Power24 – a new plan to effectively boost the company’s products and business model, which it expects to create run-rate cash cost savings of €200m in 2025. However, it did add that the plan would cost €250m to implement, so the company must expect this plan to have long-term value going forward.