Joining our post-earnings call series for the first time, dLocal Co-CEO Pedro Arnt discusses the company’s Q3 2023 performance and ongoing emerging market-focused strategy.

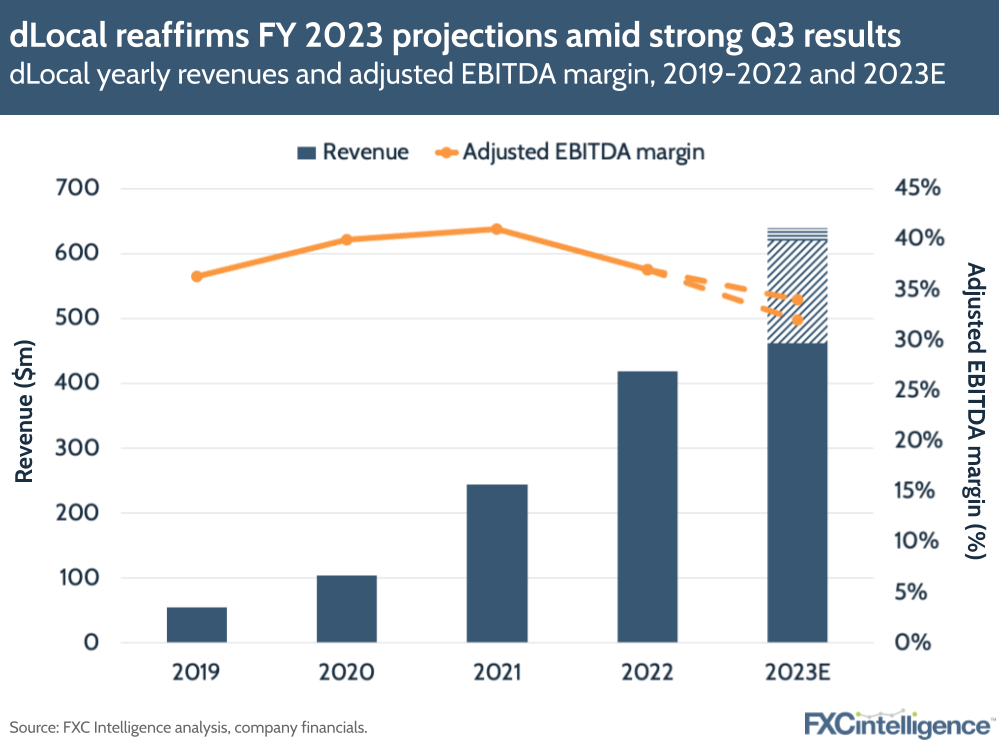

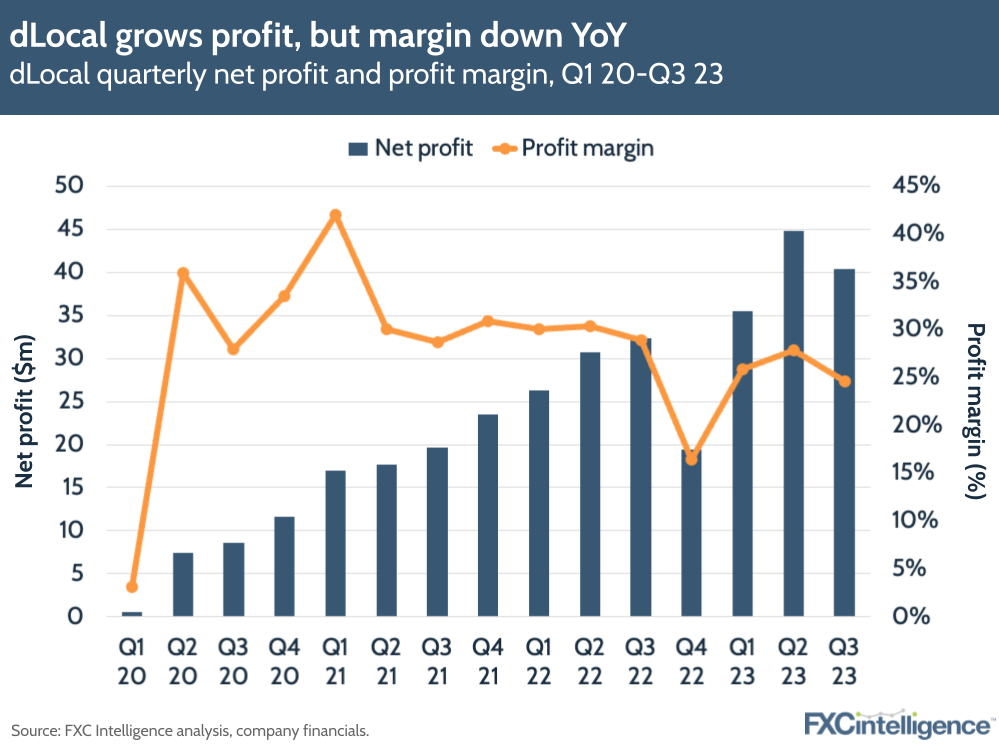

Focused on providing payments services to merchants catering to emerging markets, dLocal has been growing rapidly since its 2021 IPO, and its Q3 2023 results are no different. The company reported a 47% YoY increase in revenue to $164m, while its adjusted EBITDA grew 34% to $56m, giving an adjusted EBITDA margin of 34%.

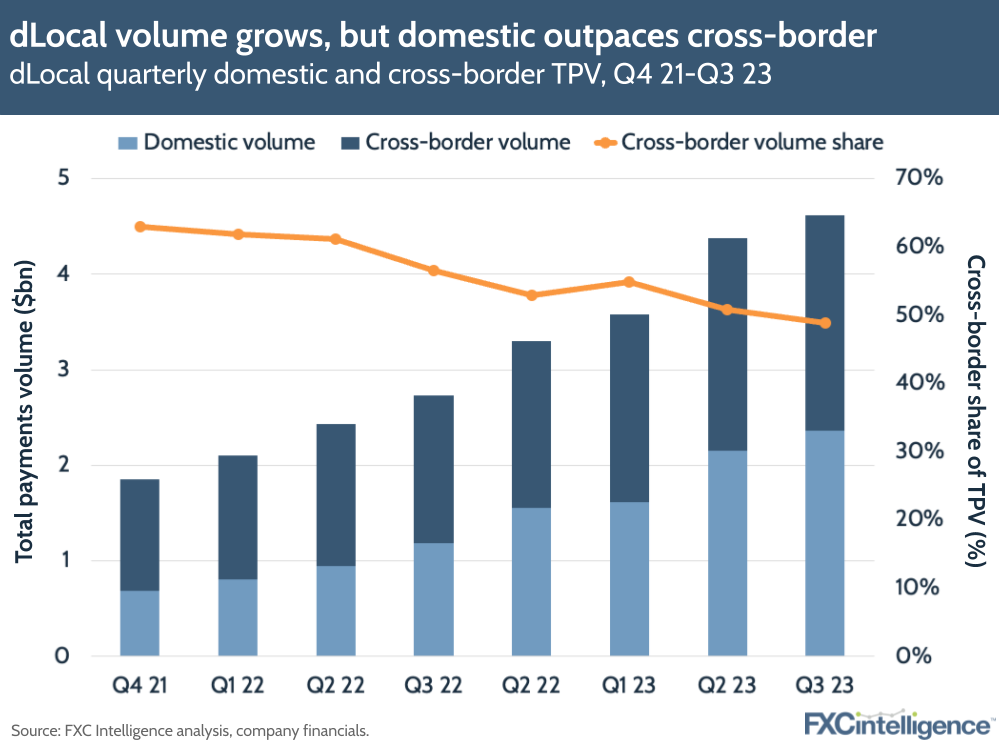

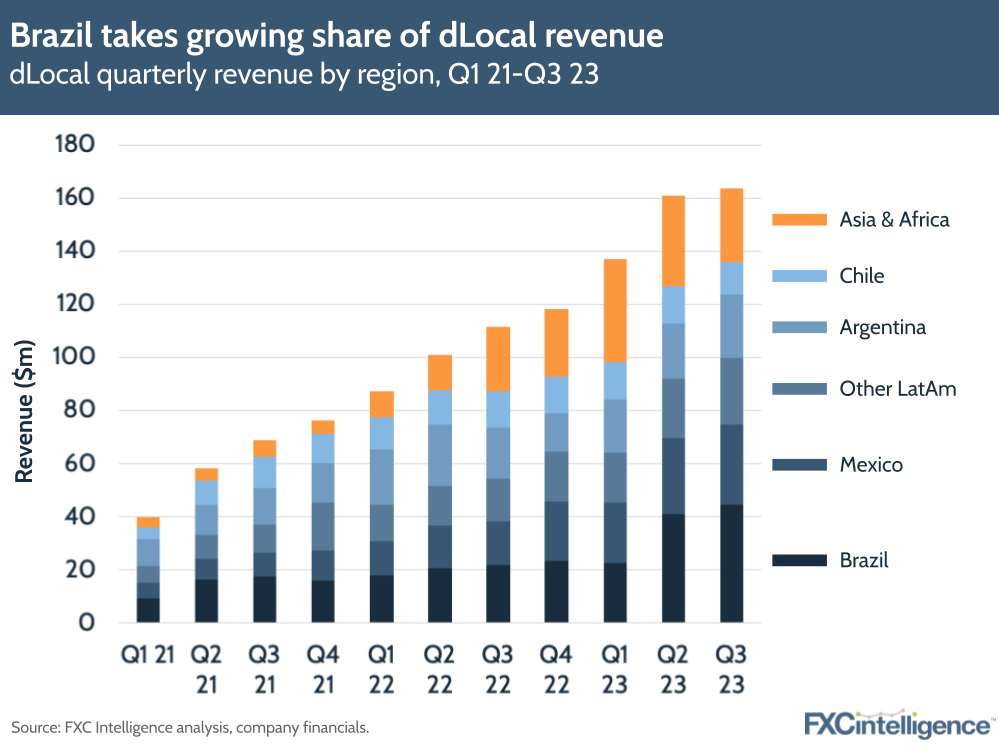

On volume, dLocal saw an increase of 69% YoY to $4.6bn. 49% of this was cross-border, although here growth was 46%. The company also reported a gross profit margin of 45%. Here it was aided by lower expatriation costs, as well growth in some African and Asian countries where dLocal has higher profit margins. However, it faced challenges in Nigeria, its largest non-LatAm market, as a result of the devaluation of the naira. While the company’s revenue from Africa and Asia increased 14% overall, this includes a 39% drop in Nigeria.

The company’s biggest market, Brazil, remains its strongest driver of growth, with revenue for the country increasing 105% YoY. Its second largest, Mexico, grew 82%, followed by Other LatAm (55%) and Argentina (25%). Chile was the only LatAm market to contract this quarter.

dLocal’s commerce platform, which launched in April of this year, is now its biggest vertical, with triple-digit growth this quarter, aided by its marketplace solutions, which have seen particularly strong adoption in Brazil and Mexico. Other focuses are ride hailing, which grew 81% YoY, followed by streaming, SaaS and financial services.

With the company expecting sustained commerce growth in Q4 as a result of the festive season, dLocal has reaffirmed its expectations for FY 2023, which would translate into YoY growth of around 50%. With this in mind, we caught up with Co-CEO Pedro Arnt, who took the role in August following a 12-year stint as CFO of Mercado Libre, to find out how he plans to take the company forward.

Pedro Arnt’s motivations for joining dLocal as Co-CEO

Daniel Webber:

Before we get into strategy, as this is our first conversation, can you share what motivated you to join dLocal?

Pedro Arnt:

Absolutely. It was a combination of two things. [The first is] a business opportunity that I find unique and incredibly attractive: how do we enable the digital revolution to occur in emerging markets? How do we make sure that billions of emerging market consumers will actually be able to access and pay for everything that will occur in the digital space?

Payments in emerging markets – we operate in Africa, in Southeast Asia, throughout all of Latin America – are extremely complex. This is very far away from your world of card schemes and BACS transfers. This is a world of UPI and Pix and digital wallets.

I truly believe dLocal empowers the world’s most relevant digital companies – Chinese, American, European – to gain access to billions of emerging and frontier market consumers, which presents enormous growth for us going forward.

Then, on a personal level, I had spent the last 20 years of my life building out an incredibly successful company – the largest Latin American company by market cap after Petrobras – and I wanted to be able to do that over again. I wanted to go to an earlier stage company this time as a CEO, not as a CFO, and do what I do best, which is to help organisations scale and grow.

Drivers of growth in dLocal’s Q3 2023 earnings

Daniel Webber:

What has been driving your really strong growth numbers and profitability, both from the top line and on a regional level?

Pedro Arnt:

Our growth algorithm continues to deliver and we continue to gain share from existing merchants in our core markets. Brazil and Mexico are our two largest markets. They drove most of the growth, which goes to show that in addition to an extremely successful business in emerging Africa, our core Latin America market continues to drive growth.

Some of that has also been driven by product innovation. We always say our growth algorithm has three prongs: it’s more merchants; it’s increasing the share of our existing merchants through offering them more geographies and gaining more share in their orchestration; and it’s product innovation.

If we look at this quarter in particular, our platform payments product – the one built for platforms, whether it be commerce platforms, ride-hailing platforms – has really been a significant driver of our growth in Brazil and Mexico.

As we go down the P&L, margins have improved somewhat. If we look at adjusted EBITDA to gross profit, that’s just scale kicking in. dLocal has always had a culture of pursuing profitable businesses and profitable opportunities. The fact that we operate in emerging markets and there’s an FX component to what we do in addition to traditional payment processing, enables us to have this very attractive margin structure.

Catering to the unique dynamics of emerging markets

Daniel Webber:

There aren’t many emerging markets payments companies, particularly in the cross-border payment space. What’s so different about the market dynamics in emerging markets?

Pedro Arnt:

The principle difference is that when we look at emerging and frontier markets, this is rapidly evolving, but these are still primarily cash markets. Anywhere between 50% to two-thirds of all transactions in most of our geographic footprint are done in cash.

Over the last five to 10 years, as many of these markets have begun to digitise, not all of them are following the same footprint as the developed world where a lot of those digital payments went the way of the card schemes. We see the emergence of alternative payment methods like Pix and UPI, which generates a whole different set of payment providers, different pipes, making it a lot more complex.

When you look at dLocal, our typical foot into our global merchants is not through traditional card acquiring for them in our markets. It’s much more common that we will win a client initially because we are providing some sort of alternative payment method for them. From there, we show them the robustness of our technology, our servicing quality, and then we typically expand into the full suite of processing both cards and APMs for them.

Daniel Webber:

You operate in about 40 markets, many of which are very different and require different expertise to get up and running in. Can you provide some insights into how difficult it is to get set up in these markets?

Pedro Arnt:

That is such a big part of the competitive moat of dLocal, which is that there is no regional or global scale in payments if you really look at it. Even if you’re running the traditional card schemes, these markets have specific acquirers that don’t port over to the next market if you want to avoid the cost of processing everything cross-border.

To set up the ability to offer your merchant’s card acquiring alternative payment mechanisms in Ecuador is very similar to the cost of doing so for Brazil, except Ecuador is a tiny country where that investment might not be justified. You multiply that by 40 and that’s the magic of dLocal. We’ve already invested over the past eight years in building out those multiple pipelines across all of these markets.

Then when you look at the dynamics of the markets, they’re also very different: how working capital flows, how credit flows, what the APMs are. Even if you look at Africa, Francophone Africa, English-speaking Africa, Eastern Africa, with things like M-Pesa, each of these have developed in a very different way.

We’ve already built all of those pipes across those 40 markets. We operate in those 40 markets, so when things work or don’t work or change – either from a regulatory perspective or from the perspective of the PSPs we operate with – we’re already there and we can adapt very quickly to that.

If you’re a global merchant looking to enter some of these markets, which typically at first will not be a core market for you, all of that complexity – technological, regulatory, cash management – is what we’re solving for you, across 40 different markets and through one single API. To replicate that is extremely complex.

Drivers of dLocal’s higher take rates

Daniel Webber:

Your take rates are substantially higher and different to the take rates of a payment processor in a developed market. Is that the result of what you’ve just talked through, versus large-scale processing in a market like North America?

Pedro Arnt:

Absolutely, and because of our pricing charts, to keep it simple for merchants we essentially tell them, “Look, there’s an FX component if you want repatriation of your funds, and then there’s a payments component”.

Sometimes people will try to equate that payments component with the equivalent in developed markets of acquiring and it’s not, it’s everything I’ve just walked you through. It’s dealing with regulation, dealing with compliance, dealing with alternative payment methods, dealing with complexity.

In many instances, our merchants don’t even need to set up local operations. We can offer them a merchant of record model, so all of that obviously generates higher take rates because we’re dealing with significantly higher complexity on the payment processing piece.

Then the FX piece, if you were to compare our take rates with most FX players globally that deal with exotic currencies or less common currencies, we’re not doing euro to dollar as the Adyens and the Stripes of the world are, we’re very far from that.

We’re dealing with either exotic or much less liquid currencies. When you look at our take rates for the FX piece, they’re very competitive, but they are higher than if you try to draw an analogous comparison to what a European cross-border payment processor and FX company might potentially charge.

Why merchants move to dLocal

Daniel Webber:

Why do merchants move to your platform? Is it the potential of significantly more revenue than if they were accessing these markets via an alternative platform?

Pedro Arnt:

That’s absolutely true, but I think that’s true of our entire industry. Merchants are choosing based on price conversion and, at the end of the day, reliability.

Optimising conversions on credit card is a science in and of itself, but a fairly well-known science by this point. When you’re starting to optimise around the different APMs in different markets, where fund flows and user experiences are significantly less developed than on credit cards, then that’s an even bigger differentiator.

dLocal’s customer segmentations

Daniel Webber:

How do you group your different customers? You mentioned that the commerce platform is the biggest area – who is in that?

Pedro Arnt:

There are two segmentations. The one that we disclose is by industry, and we’ve done a really good job of being very diversified.

Commerce is our largest category and it’s also the fastest growing one, but it represents less than a quarter of our business. We’re very well diversified around commerce, financial services, ride-hailing, streaming, on demand delivery, advertising and a few others.

That’s one piece, then the other cut is just the size of our merchants. We clearly have an enterprise B2B focus. Most of our merchants are very large global merchants. The top 10 merchants this quarter accounted for almost 60% of our volume, so if you look at how much TPV that is, you very quickly realise that the merchants that we are dealing with are really the Facebooks, Apples, Netflix, Googles, DiDis, SHEINs, Temus of the world.

Then as you move to tier one and tier two, we really stay within the large company segment. We do very little SMB, which could potentially be an untapped opportunity for us in the future and that will be for a future conversation. But today it’s well diversified geographically, very much focused on large global enterprises that have operations with us in at least four plus markets, and on average use us in more than 10 markets.

New products and merchant renewals

Daniel Webber:

You explained previously that you renew merchants more from existing and new products. What role do new products play in your strategy?

Pedro Arnt:

It’s interesting because our new products really are variations on one core thing that we do incredibly well, which is process payments, but as we’ve expanded into more verticals, obviously we’ve realised that there are payments experiences that our merchants require that are distinct and specific to what they’re doing.

One of the new products that we’ve launched, that is driving a significant portion of our growth, is our platform approach. That’s basically where payment flows are not the traditional consumer-to-merchant one flow, but with the emergence of alternative commerce models and marketplaces and ride-hailing, you have the situation where the merchant might be the marketplace – which in itself has multiple merchants that sell goods or services or offer their carts through that platform – and then the consumer.

When you think about that, the fund flows become more complex. You have to split payments, you have to retain commissions, you have potentially one shopping cart that then has a partial return, so which of the merchants do I return it to? Which means more complex conciliations and that drives the need for innovative solutions from our merchants.

Daniel Webber:

Do you find these products can roll out across many of your markets?

Pedro Arnt:

They absolutely can, and this is also something we’re very pleased with. If you have a marketplace product that you offer a Brazilian or a global merchant that has a Brazilian marketplace, and you try to port that as-is to their Mexican operations, you’re not really satisfying all their needs because Mexican regulation will be slightly different, and so there will be tweaks around the edges of how funds have to flow and how account balances have to look.

That’s all fantastic for us because since we focus on the parts of the world we focus on, there really aren’t other competitors at our scale that are doing the same. It’s very likely that the marketplace solution we offer in Mexico is the most tailored to the Mexican market.

The flip side of that, just to paint the whole picture, is we don’t yet have our marketplace product rolled out everywhere. As a matter of fact, we only have it rolled out in three or four geographies because you need to adapt for each one of the new markets you go into.

Daniel Webber:

We’re almost out of time. Is there anything you’d like to add that we haven’t covered?

Pedro Arnt:

No, I think your team has prepped you well. Those are the key themes and the key questions. Phenomenal traction, we’re seeing some really good trends as we exit what was a very successful 2023, given how turbulent 2022 ended for the company and some things that happened in the first half of this year. We’re really excited to flip over a new page and get going with 2024, because we’re ending 2023 on a bang.

Daniel Webber:

Pedro, thank you.

Pedro Arnt:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.