An established part of the cross-border payments landscape, multicurrency accounts allow users to hold, receive and send funds to other countries, reducing the need for instant conversion and giving businesses more control over how they hold currency while providing more convenient payments to their customers.

Multicurrency accounts are of specific relevance to businesses that trade and operate globally, including large multinational corporates, exporters and importers, ecommerce sellers and SMEs. As these businesses continue to expand into new regions, and as imports and exports have increased globally, this creates a demand for businesses to simplify their transactions to suppliers and from customers, as well as to enable easier payouts to staff and vendors abroad.

Our recent market sizing update showed that a significant portion of the $44tn in retail payment flows in 2025 can be attributed to B2B payments. Moreover, according to a March report from the World Trade Organisation, the volume of world merchandise trade rose by 4.6% in 2025, though this is expected to slow to 1.9% in 2026, with one potential headwind being conflict in the Middle East. In combination, this means that there is not only a significant opportunity for B2B payments providers to enable, capture and monetise these cross-border flows, but that there is a need for some of the world’s largest retailers and businesses to be able to hedge against FX volatility in a more unpredictable trade environment.

On the one hand, providing accounts that allow customers to hold multiple currencies that allow them to bypass some FX conversions, and thus the margins that may be captured on them, may appear counterintuitive. However, payment providers have moved to capture a customer need, better compete with banks and expose customers to additional financial services. If providers are holding customer funds, this then enables them to introduce features serving other business needs, spanning offerings such as mass payout solutions for staff, business cards and spend management products.

In this report, we explore how payments companies market their multicurrency solutions to businesses and how this exemplifies a greater shift to capture a higher share of the financial services output from banks.

Why do businesses need multicurrency accounts?

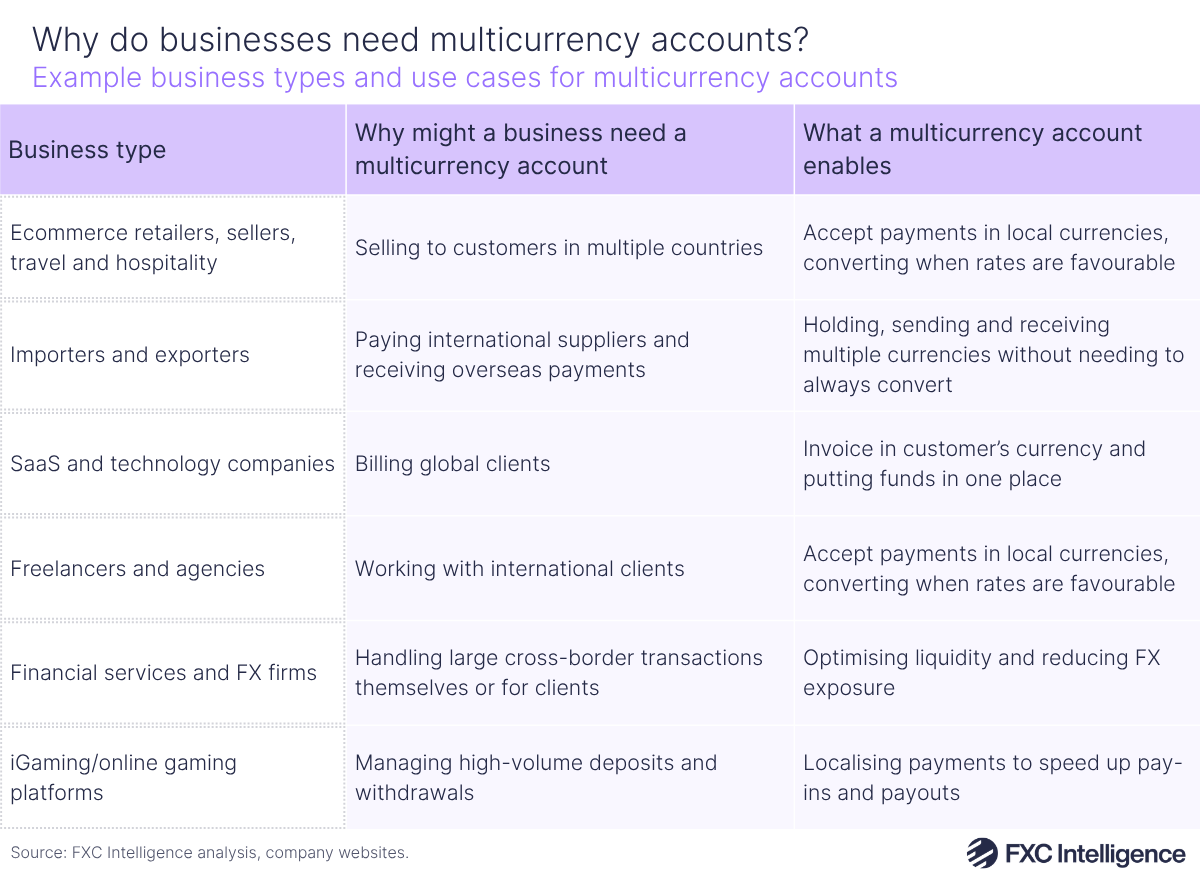

Businesses of different types may need multicurrency accounts for a variety of different reasons. A major example of this is online retailers and marketplaces, which sell to customers in other countries but need to be able to sell, receive and pay out in multiple currencies simultaneously.

Online retailers may price in their local currency but actually receive payouts in different currencies. If they are receiving payments into a bank account in their local currency, funds will be converted automatically, adding an FX fee that eats into the profit from the sale. This is also true for ecommerce sellers using large global marketplaces such as Amazon, Shopify and Etsy. Similarly, when online retailers need to pay suppliers in other countries, this then requires an FX conversion when paying in their local currency.

Those marketplaces are also global businesses themselves, so may need to move money across the different regions that they operate in. For example if they are based in the US but have a division in Europe, those funds may be held in a different currency in a separate account. If these businesses want to move funds between those accounts, that creates an additional FX conversion. It also creates reconciliation difficulties, as companies have multiple accounts and bank statements in different countries, making it harder to track their revenue and costs.

High delays and costs can stem from companies sending cross-border payments through a correspondent banking network, with funds sometimes needing to pass through multiple banks in a chain in order to settle in their final destination. This can create a bottleneck that adds additional costs and delays due to compliance checks, manual intervention and timezone differences.

However, if global retailers or SMEs expanding into other countries are using a multicurrency account, they are able to have a single, centralised place for managing currencies. A common feature connected to multicurrency accounts is a multicurrency international bank account number (IBAN). This is essentially a separate set of bank details that allows a payment to be accepted by a business as if it was being made domestically in its local currency, removing the need for conversion.

Rapyd is an example of a company that serves online retailers, digital goods and platforms through its multicurrency account offering. It allows clients to set up an unlimited number of virtual accounts, or vIBANS, to manage incoming payment flows and maintain a high-level view of their total account balance. These virtual accounts function like bank accounts in terms of receiving payments, but they are linked to a central account where the currencies are held, unlike traditional bank accounts that contain the funds directly.

“For businesses receiving payments in exotic or volatile (tier 2 or 3) currencies, Rapyd’s built-in FX system allows them to hold funds in more stable currencies like USD or EUR, which can help protect them from currency devaluation,” says David Rosa, GM of FX, Wallets & Payouts at Rapyd.

Across multicurrency accounts more widely, retailers are then able to hold the currencies they are collecting in one account, convert from one currency to another within the account and also make payouts to parties in other countries in their local currency (if they hold it within the account), meaning that they are avoiding a conversion fee. If the payment provider operating the account has access to fast local payment systems (e.g. SEPA in the EU), payers can also make payments through these systems from their multicurrency accounts.

Rosa notes the ability of Rapyd’s account to use a wide range of payout methods, including e-wallets, cards, bank transfers and stablecoin wallets. “Businesses can send a payment anywhere, in just about any currency, to any non-sanctioned country in the world, ensuring payouts reach their suppliers, vendors or end users in their local or preferred currency,” he adds.

In short, multicurrency accounts allow retailers to send and receive global payments more easily, faster and with fewer FX conversion costs, but they also make it easier to track their revenue and associated costs, as currencies from different parts of the world are all in one place.

This becomes even more significant in a challenging macroeconomic landscape. Convera, which serves businesses of all sizes as well as educational institutions, says it helps these businesses to navigate complexity as they scale.

“In 2026, FX-exposed businesses have already faced significant market shocks, from geopolitical conflicts to energy price spikes,” says a spokesperson from Convera. “With the US dollar surging 5% since January, CFOs are navigating a landscape where global business has grown more volatile, not simpler. Strategic planning now requires balancing the disruptions of AI, de-dollarisation and shifting trade policies.”

Many of these benefits for online retailers are just as applicable to other businesses in the space needing to receive, hold and send money across borders. This includes large import/export businesses, which need to ensure that they have the liquidity available to make and receive purchases, and travel and hospitality providers, which often have a global client base paying in different currencies from around the world.

Another specific vertical targeted by some providers in the cross-border multicurrency space is iGaming, which covers various companies providing online games related to gambling and betting. These businesses have a specific need to support high-volume, frequent pay-ins and payouts across players supporting a wide variety of payment methods. Operators in this instance typically serve customers across multiple markets, creating a constant need to serve inbound and outbound payments.

Another core use case of multicurrency accounts is businesses being able to pay out to freelancers and contractors in their local currency. With a 2025 report from employer of record provider Pebl found that 44% of business leaders planned to increase international hiring by H1 2026, businesses seeking to hire abroad need a way to effectively pay out to global workers. Meanwhile, from the workers’ perspective, holding multicurrency accounts also enables them to be paid in multiple currencies, giving them more flexibility over where they are paid and reducing the burden of having to automatically convert to one local currency.

How do multicurrency accounts serve businesses of different sizes?

Multicurrency accounts are promoted across the industry for businesses of various sizes. The core proposition is the same – making it easier to manage, receive and hold currencies and optimise cross-border payments. However the impact of this can be at different levels of complexity, and businesses of different sizes may need to be supported in different ways.

For example: smaller and medium-sized businesses that want to be able to serve users or interact with parties in other countries, but may not yet have established entities in other countries. Such businesses operate on much tighter margins than larger corporations, and even small percentage differences on FX conversions can therefore have a much larger impact on their profits.

These companies may not have the resources in place (i.e. treasury teams) to effectively manage their exposure to currencies and hedge against FX risks. Equally, they don’t have the same access to competitive FX pricing as larger companies, which have significantly higher cross-border volumes and are therefore able to negotiate pricing for more favourable rates.

“Thereʼs a growing shift in expectations of SMEs,” says Josh Goines, Chief Growth Officer at OFX. “They want a financial operations platform that serves their core needs such as multicurrency accounts, AP and AR with the ability to pay and receive from their global suppliers and customers, with intelligently automated workflows that integrate with their other core applications such as their accounting software.”

Multicurrency accounts can therefore help SMEs specifically to get more control over the payments they are receiving or making to a market they are seeking to move into, but where they may not yet have an established entity. They can quickly collect revenues from other countries and reduce FX impacts from those payments. They also have the power to choose when they convert currencies at a time where they can get the best possible rate, and are able to more easily track their revenue rather than having to open multiple accounts.

“Our recent customer interviewees estimate savings of five hours a week and thousands in annual bank fees, simply by bringing multicurrency accounts and financial operations into one platform,” adds Goines.

Larger businesses also see these benefits, but are operating at a different level of complexity. These businesses may have entities and a global workforce spread across multiple regions around the world. Without a centralised way of managing the different payments they receive, they could see capital potentially being trapped in different regions around the world, making it harder to deploy it quickly. Because they are receiving large volumes of payments from different countries, even small changes to FX pricing can have a significant financial impact.

In addition to reducing costs from conversion, multicurrency accounts can help larger businesses to optimise their treasury operations more effectively. It also helps them to be able to pay out to suppliers, contractors or staff around the world from one place, as well as reconciling its payments more easily, which in turn speeds up cross-border payments.

How are payment providers supporting businesses with multicurrency accounts?

Over the last few decades, new regulations have enabled fintechs and payment providers to shift from being able to offer transfers to allowing customers to hold money in accounts. For example, e-money licences offered in the UK and EU allow companies to issue and manage electronic money and offer a variety of additional solutions and services, such as prepaid cards, digital wallets and accounts.

“Many payment service providers (PSPs) are updating their capabilities as companies expand beyond traditional payment processing, with more of them integrating functions like multicurrency business accounts,” says a spokesperson for Singapore-based B2B payments provider Airwallex. “This competition will improve the quality of services and mean that multi-currency accounts will become a key part of firms’ finance stacks.”

While banks have offered multicurrency accounts primarily targeted at larger corporations for some time, both long-established and newer payments providers in the B2B space have evolved to offer multicurrency accounts that respond to the differing needs of businesses.

“We work with a broad range of businesses, but our multicurrency accounts are particularly popular among B2B companies – particularly those managing high volumes of international payments,” says the Airwallex spokesperson.

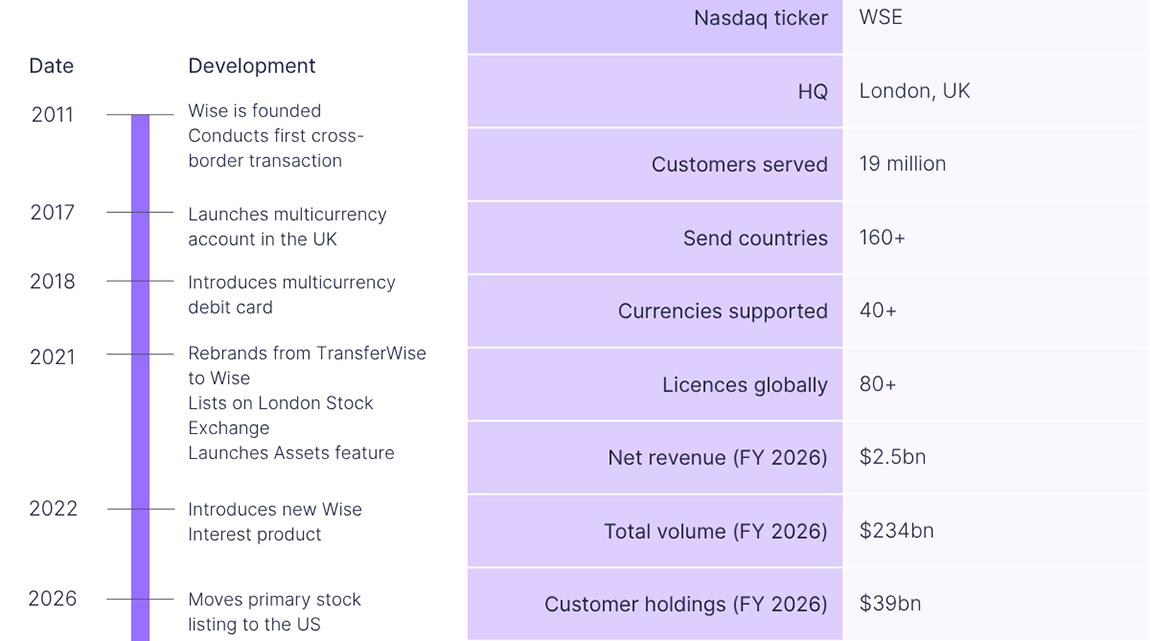

Some businesses, such as iBanFirst, launched with multicurrency accounts as a specific solution. Some providers have shifted into multicurrency accounts as they have moved to focus more on business payments; both Wise and Revolut, for example, launched multicurrency account offerings for businesses in the UK and Europe in 2017. Over time, a competitive landscape for multicurrency accounts has built up as fintechs have launched more solutions into the space.

Wise and Revolut are also examples of companies that offer multicurrency offerings across both consumers and businesses, though both are increasingly seeking to target business flows. In its model, Revolut has a tier pricing system for its business account that is tailored to capture businesses at a variety of different sizes.

iBanFirst, meanwhile, specifically targets small and medium-sized multinational businesses that face complexity in cross-border operations but don’t have the same treasury capabilities as large corporates.

The company says that giving clients autonomy over their financial operations, rather than needing additional parties to help with this, is a big part of its value proposition. “Nearly 97% of our client financial operations are now executed autonomously by themselves, small and medium multinationals (SMM),” says Pierre-Antoine Dusoulier, CEO and Founder of iBanFirst. “SMMs want control and transparency, not hand-holding. We give them institutional-grade tools on a UX built for their reality.”

Some companies target businesses across the spectrum. For example, Payoneer’s multicurrency accounts are used by both B2B and B2C sellers operating across borders, including exporters, digital service providers, marketplace sellers and SMBs with multiple legal entities across different regions. “These businesses see the greatest benefit in being able to collect locally in their customers’ currencies – reducing payment friction, avoiding unnecessary FX and speeding up settlement – while also gaining better control over liquidity and cash management across markets,” says Derek Green, Treasurer & SVP of Payments at Payoneer.

Another more recent entrant to the space is Corpay, which launched its multicurrency accounts for businesses last year and has since seen significant adoption. The company seeks to tap into money movement for significantly larger enterprises and differentiate itself from competitors in the multicurrency space by offering an additional range of treasury management solutions.

Corpay’s offering puts it closely into competition with banks, many of which have offered foreign currency accounts for years but often as part of a wider suite of treasury solutions being offered to larger companies. Only a smaller number of banks appear to frame these as integrated multicurrency accounts that consolidate multiple currencies into a single product.

HSBC’s Global Wallet and DBS’s Business Multi-Currency Account are among the clearest examples of this, while many banks appear to offer cross-border currency capabilities as part of a wider bank offering or offer individual accounts focusing on specific currencies.

Examining payment providers in the multicurrency account space shows that they focus on a variety of features, with some of the key focuses being the number of currencies they allow users to hold and the number of markets they allow businesses to easily send money to.

Many of the non-bank providers in the space explicitly focus on how their multicurrency offerings give businesses a more seamless cross-border experience than banks. For example, Airwallex allows businesses to open local currency accounts with local bank details around the world quickly, instead of having to set up local entities. The company states on its webpage that customers can avoid “bank queues, paperwork or needless fees”, while offering international transfers and the ability to offer multicurrency corporate cards.

“Modern business requires a financial operating system that moves as fast as digital trade,” says the Airwallex spokesperson. “The global account is the logical evolution of the business bank account, connecting collections, spend, corporate cards and accounting software in one place. This means finance teams can maintain full visibility without the manual work that typically slows down month-end close.”

Similarly, Rapyd refers to its multicurrency offering on its website as the “‘better than a bank’ account”, allowing businesses to hold payments in multiple currencies and send them to vendors and clients overseas, eliminating the time and expense of setting up bank accounts.

A common theme across the companies is targeting the global aspect as the key facet of a wider financial platform offering for clients. Wise, for example, promotes its Business Account as “the business account for going global”. Convera, meanwhile, pitches its solution as multicurrency holding balances, which are part of a wider suite of global FX tools that it provides to businesses.

Meanwhile, OFX frames its solution as “one financial platform” for businesses and their FX needs, offering payments and transfers, corporate cards, AP & bills automation in one centralised offering.

“Even modern businesses often revert to their traditional bank for international transfers,” says OFX’s Goines. “This brings a separate, complex workflow, as well as increased costs. More businesses are seeing the value of moving from individual payment transactions to multicurrency capability. They can skip the hassle and expense of relying on their bank, avoid unnecessary currency conversions and pay and get paid faster.”

Why are multicurrency accounts significant for cross-border payments company strategies?

Multicurrency accounts give businesses access to platforms to hold currencies but also open them up to the money transfer capabilities of providers, which often span a much larger set of currencies than can be held in accounts. This means that the payment provider is able to monetise transfers to additional countries where a business may need to pay other suppliers/contractors or may seek to expand in the future.

Payment providers aim to provide additional benefits aside from just sending and receiving payments, such as expense management, corporate cards and offering additional yield or interest on balances held in customer accounts. This is building into companies’ strategies to offer services to global businesses that make them more attractive to use than banks as comprehensive financial global platforms. Aside from external benefits, multicurrency accounts can also help make payment providers’ internal operations more efficient.

“Multicurrency accounts are a core pillar of Payoneer’s B2B strategy, enabling SMBs to collect and hold funds in local currencies via domestic payment schemes,” says Green. “This opens new B2B trade corridors by reducing cost, friction, and FX for payers and receivers, while also strengthening Payoneer’s treasury efficiency through local netting.”

For example, several providers in the space offer corporate card solutions and spend controls on top of their multicurrency businesses. This is particularly useful to smaller businesses that may lack the capabilities to manage expenses in-house, but can also have use for larger businesses with teams that regularly need to make payments abroad.

For iBanFirst, the goal is to enable cash management, AI-based FX intelligence and accounting synchronisation (capabilities long reserved for large corporates) across small and medium-sized businesses. “Our mission is to make [these features] standard for every SMM we serve, across Europe and beyond,” says Dusoulier.

In some cases, companies also focus on the ability to enable businesses to effectively track their money. Moneycorp, for example, allows users to track live exchange rates directly from their multicurrency accounts, while Convera’s cloud-native platform automates workflows and provides real-time tracking and analytics. Other companies directly allow businesses to connect their multicurrency accounts with external accounting tools, or link their multicurrency account tools to their own accounts payable solutions.

Stablecoins mark another significant ongoing development related to multicurrency accounts, with some payments providers either integrating these into their offerings or launching specific wallet solutions that allow businesses to hold digital currencies for money movement. For example, Stripe has introduced Stablecoin Financial Accounts, which allow businesses across 101 countries to hold dollar-denominated stablecoin currencies, with one of the specific benefits being being able to reduce FX costs. At the infrastructure level, companies like Circle are providing underlying wallet infrastructure so that other payment providers can offer stablecoin balances.

Many of the B2B payment providers we examined in this space have not yet fully committed to stablecoins, though several are actively exploring them and others have already launched solutions. Rapyd, for example, has launched a platform specifically for businesses looking to accept and make payouts in stablecoins, as well as enabling settlement in both fiat and stablecoins.

Meanwhile, payments providers that were originally on the consumer side of the spectrum are also seeing numerous benefits from offering account solutions specifically to businesses.

Wise, for example, was originally a consumer-facing company but has since launched payments offerings for businesses, including a specific multicurrency business account product in 2017. Its multicurrency offering now includes debit cards that enable spending across 231 countries and businesses can also sync up their Wise accounts with third-party software providers to make global accounting processes easier.

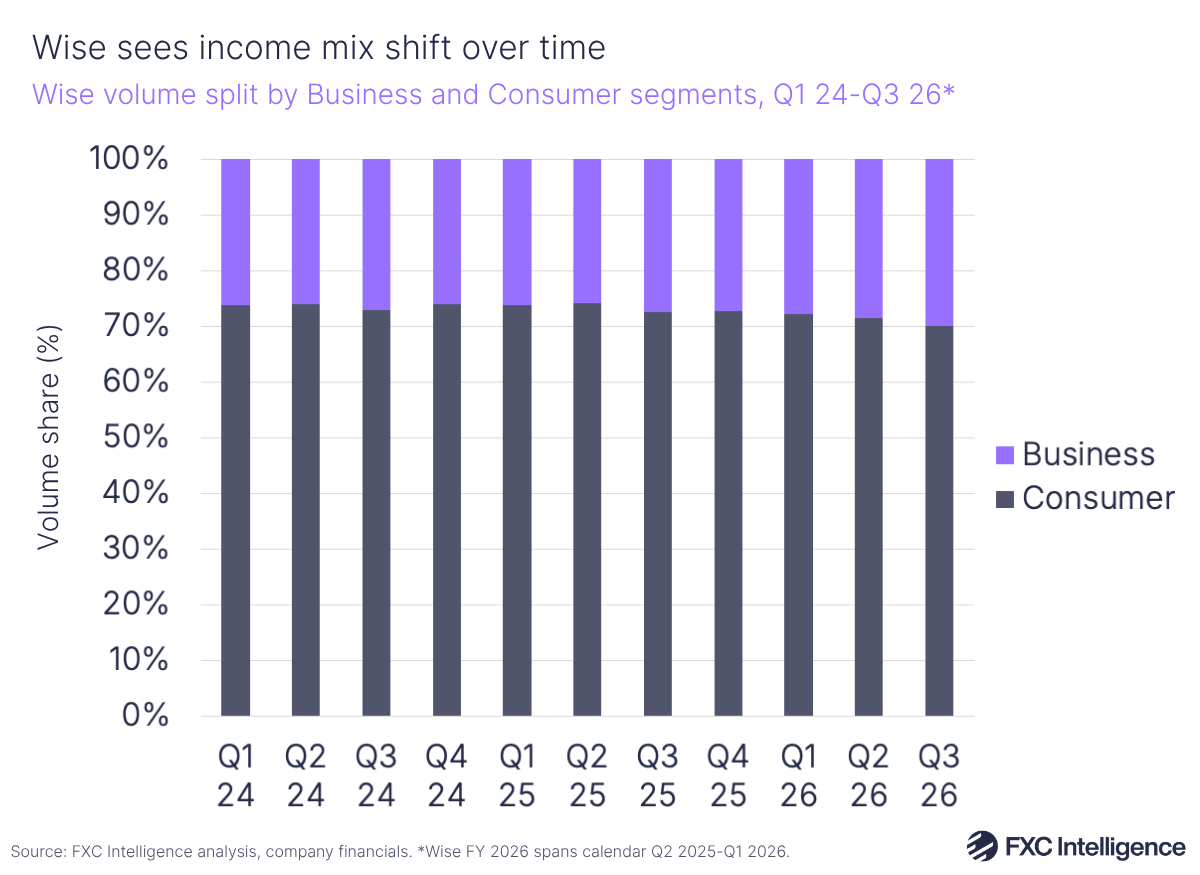

The ability to hold currencies in accounts can have a significant impact on companies’ earnings. Wise saw businesses take up a significant portion of the company’s volume and revenue mix in Q3 2026 (spanning calendar Q4 2025) and Payoneer has seen significant growth in the amount being held by customers in its accounts, with a 13% rise in customer funds to $7.9bn by the end of Q4 2025, outpacing its volume growth. The company said that this reflected the trust customers place in its platform and the utility it provides through its multicurrency accounts receivable and payable capabilities.

In a blog on the company’s progress in 2025, Airwallex’s CEO Jack Zhang noted how the company had worked to expand the depth and reach of its Business Accounts infrastructure, growing the number of countries its wallet covers, currencies users can hold and markets they can pay out to. Zhang also noted strong adoption of the company’s multicurrency Yield product, with funds under management having grown 6% YoY to $1bn, as well as introducing new features for scheduling transfers and FX conversions.

How are companies further expanding into business payments?

For payments companies, a key goal has been expanding their networks to serve more and more markets, with multicurrency accounts fitting into a wider goal to capture more market share. For example, Rapyd’s Rosa says that historically 80% of the company’s volumes have been in the most liquid global currencies: EUR, USD and GBP. However, its acquisition of PayU is changing that balance and introducing more volumes across emerging markets.

Similarly, Payoneer is continuing to expand its currency coverage and local collection schemes based on customer demand and key trade corridors. Green says that the company expects to see B2B multicurrency accounts evolve from primarily collection facilities into full local business accounts that support capabilities such as direct debits, local payouts, and richer AR and AP workflows.

“This evolution is driven by trends such as the globalisation of SMBs, the rise of SMBs with multiple legal entities across different regions operating models, and growing expectations for local payment experiences in B2B trade, positioning multicurrency accounts as a foundation for broader cash‑management and financial operations capabilities,” he adds.

Artificial intelligence is also serving to enhance multicurrency propositions, and also helping providers to compete with banks in their offerings. Convera, for example, is using AI to enhance its risk monitoring across 10 million annual transactions through its platform globally. Elsewhere, iBanFirst now offers its AI-enhanced payments assistant, iBanPay, which allows businesses to automatically compile data required for making payments invoices as a draft that they can review before sending the payment.

“It moves us from automating transactions to anticipating them, helping SMMs make smarter FX decisions, streamlining AP workflows and ultimately act more like a corporate treasury, without needing one,” says Dusoulier. “For SMMs relying on business multicurrency accounts to navigate fragmented markets and volatile currencies, the question is no longer whether AI will transform treasury management, but whether their provider is truly built for it.”

OFX has continued to develop its solutions to support SMEs growing and seeing more complexity. “Invoices pile up, managing spend becomes more important and opaque, more core systems are employed to manage tasks and currency risk management heightens,” explains Goines. “This results in significant manual effort from finance and accounting teams, and it leads to an increasing number of errors and missed opportunities. This balloons into a massive frustration for finance leaders that want to focus their time on responsible growth strategies.

“Built over many years of deep understanding of these pain points, OFX has designed a more advanced solution, called Full Suite, to help SMEs automate their AP and spend controls and reduce complexity through deep two-way sync integrations with accounting platforms.”

Rapyd’s Rosa says that AI and stablecoins will be key trends affecting how multicurrency accounts evolve in the future. In particular, he says that these accounts will evolve into intelligent, “always-on” liquidity engines focused on two areas: democratising treasury management across a broader range of businesses and enabling “next-generation” settlement for stablecoins, which he argues will allow for faster and more efficient global treasury operations.

“Rapyd envisions a future where AI agents, rather than just human accountants, interact with these accounts,” he says. “Leveraging smart contracts, money becomes programmable, enabling atomic payments via advanced APIs where funds are released only when specific conditions are met and verified by data.

“In addition, AI will continue to be incorporated into the account infrastructure for automated reconciliation, matching complex global B2B invoices with fragmented payments in real-time, solving the ‘reconciliation headache’ that currently plagues cross-border payments.”

Some payment providers have made stronger moves to own the primary financial relationship with businesses. Revolut recently received a banking licence in the UK, allowing it to launch new accounts for both retail and business customers. This also gives it the potential to offer a wider array of banking products to businesses in the future. This week, Wise launched current accounts in the UK for consumers and businesses in the country, though this currently appears to have more of a consumer focus.

A common theme across multicurrency products has been their ability to serve payments across local rails to bypass Swift and banking channels. Wise has been consistently growing its access to domestic payment systems across market and recently claimed to be the first non-bank to receive the licences needed to operate in Thailand, allowing it to issue foreign currency wallets and cards in the country.

The company’s expansion to add more local payment rails to its network is also serving Wise Platform, its white-label infrastructure service for banks and financial institutions. This platform highlights a wider shift within the industry for money transfer players seeking to tap into larger business flows by supporting infrastructure, reflecting the business models of companies such as Thunes and fitting into a wider picture around non-bank providers increasingly looking to serve businesses with an alternative financial platform to banks.

While banks provide access to multicurrency offerings as part of a wider array of features for businesses, non-bank providers continue to build platforms that are designed to capture more business payments activity. As a result, there is a continued movement in the payments space to own the primary financial relationship with global businesses, which in turn puts them in a better position to capture more of payment flows.