SMB-focused Payoneer surpassed $1bn in annual revenue for the first time in 2025. We spoke to CEO John Caplan to find out what’s driving the company’s revenue and how stablecoins are setting the stage for further growth in 2026, with additional commentary from VP Investor Relations Michelle Wang.

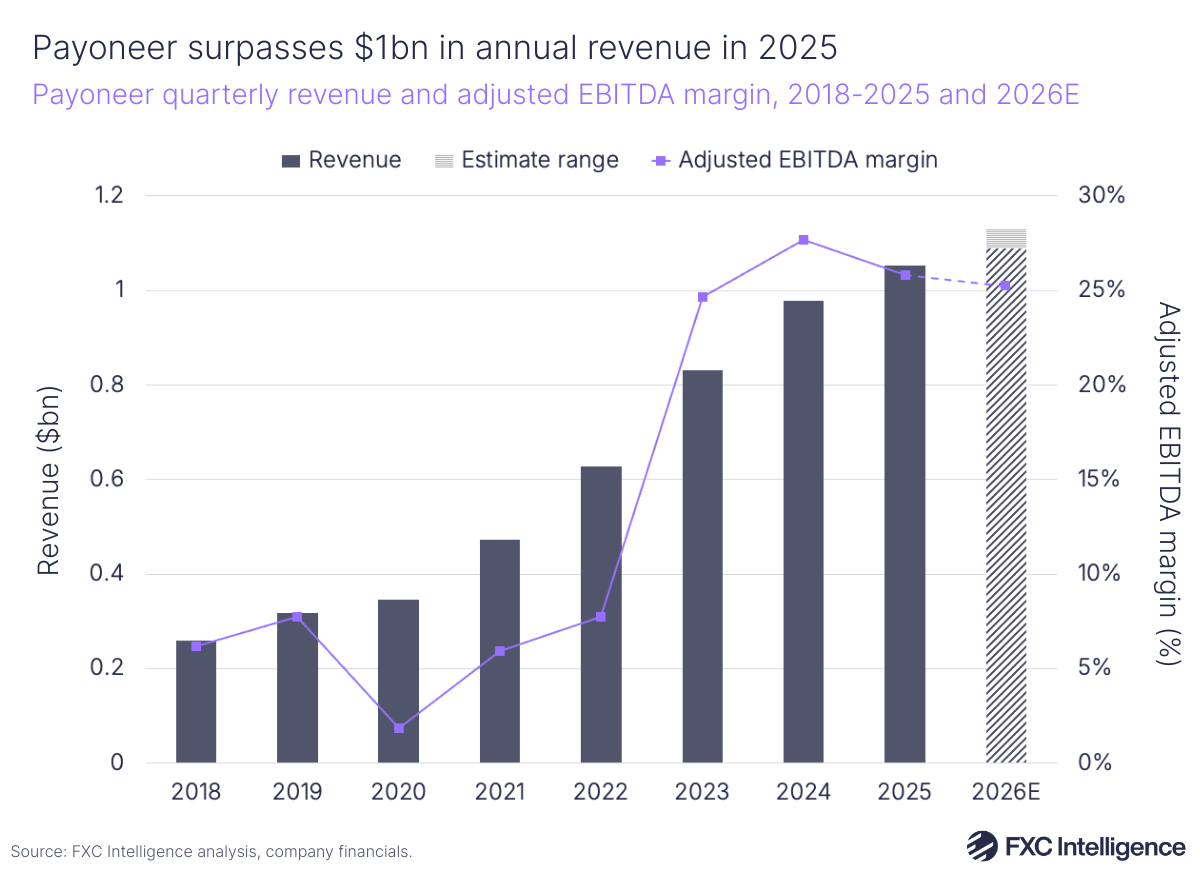

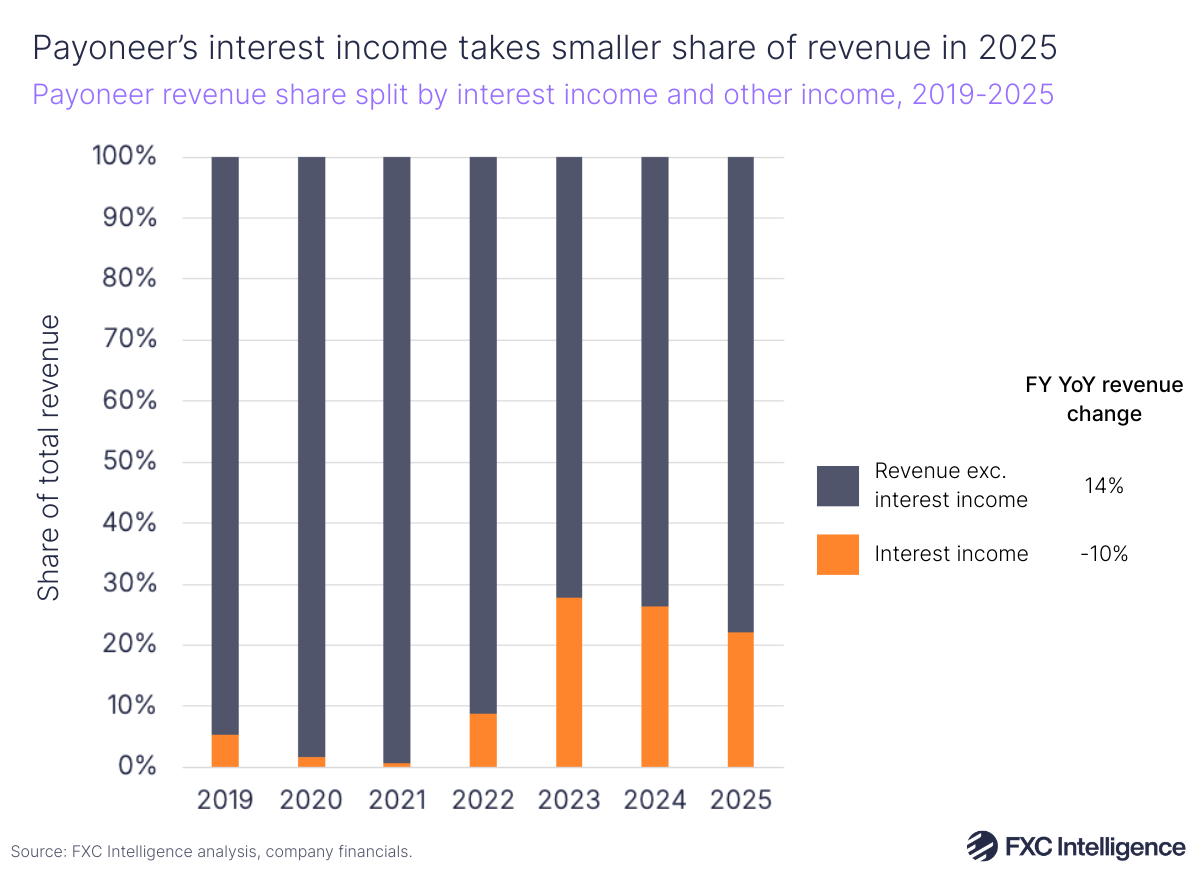

Payoneer reported revenue had grown by 5% in Q4 2025 to $275m, driving overall revenue for the full year up 8% to $1.05bn. Revenue excluding interest income rose 9% in Q4 2025 to $219m, driving 14% growth to $821m in FY 2025.

Payoneer continues to look to diversify and is now focusing on serving “larger, more sophisticated” customers with complex cross-border requirements. It is increasingly making targeted investments to do this, including expanding its capabilities in Mexico, Indonesia and India. It is also moving the company towards an “AI-first strategy” in 2026, with the goal of using agentic AI to help speed up product delivery and workflows, improve customer experience and drive its go-to-market return on investment.

The company is also targeting the growing cross-border stablecoins opportunity, having recently announced a partnership with Stripe-owned Bridge that will allow businesses to receive, hold and send stablecoins overseas using Payoneer’s platform.

Connected to this, Payoneer has followed the example of a number of payments providers in filing an application for a US national trust bank charter. If the application is successful, Payoneer would be able to issue its own stablecoin, PAYO-USD, that customers can hold in Payoneer wallets, with Payoneer able to then hold reserves for the stablecoin through a federally regulated financial institution.

We spoke to Payoneer CEO John Caplan and VP Investor Relations Michelle Wang to dig into Payoneer’s profitable growth in 2025, as well as how it is tapping into the B2B stablecoins opportunity.

Payoneer’s key revenue drivers in 2025

Daniel Webber:

Let’s start at the top: What have been the key drivers for Payoneer’s growth this year?

John Caplan:

Payoneer had a great year in 2025. We had $87.5bn of volume, 9% volume growth and 14% revenue excluding interest growth.

We powered through declining interest rates to deliver adjusted EBITDA of $272m. But the most important number is that we took $12m of core EBITDA in 2024 and grew that to $40m in 2025.

If you think about the transformation of Payoneer and where we are in our journey, we have taken the business and delivered 17% CAGR for each of the last 14 quarters and made the business materially more profitable.

Delivering growth and profitability is a really powerful part of the story of Payoneer, and the profitability growth is really the narrative that’s probably the most important. Secondly, as we’ve looked at our portfolio, 100% of Payoneer’s customers are profitable today. When I joined Payoneer it was 25%, so we’ve materially strengthened the quality of the portfolio of customers we’ve had.

We’ve driven really strong volume growth and we’ve achieved profitability dynamics. The guide for this year is $90m of core EBITDA, basically doubling 2025 EBITDA, while we continue to grow the topline revenue. When you think about the fintech landscape and the companies you pay attention to, we’re delivering growth and profitability. Not everybody’s expanding margins while they’re driving the growth, and so I think it’s really important to recognise that’s the way we’ve approached 2025 and into 2026.

I feel really confident about what we’ve guided for this year. The market’s tough and unforgiving, but the strength in our results is real.

Payoneer surpasses $1bn in annual revenue

Payoneer’s processed volumes rose by 10% in Q4 2025 to $24.8bn, driving a 9% rise to $87.5bn for full-year 2025. Key drivers for the company were accelerating B2B and SMB volumes, strong enterprise payout growth, customer expansion and continued (though slower) marketplace seller activity.

Payoneer’s full-year adjusted EBITDA of $272m gave the company an adjusted EBITDA margin of 26%, slightly down from 28% in 2024. For FY 2026, Payoneer expects revenue of $1.09bn-1.13bn in 2026, which equates to 4-7% growth, with adjusted EBITDA expected to rise to $275m-285m (growing 1-5%), which would give an adjusted EBITDA margin of 25%.

Payoneer estimated a 300 bps headwind to 2026 core revenue growth due to anticipated churn relating to its transition to Stripe’s Checkout solution, as well as changes to Payoneer’s acquisition focus and onboarding flows. The company projects high single-digit growth for revenue excluding interest in H1 2026, with this ramping up to mid-teens growth in H2.

Payoneer targets large customers driving high volume growth

Daniel Webber:

How is Payoneer continuing to drive that underlying profitability, and what would your message be to investors after Q4?

John Caplan:

One of the figures I think people are missing is the 17% growth in our enterprise volumes this year, which is a really powerful number. [This is driven by] our larger customers – the $50k+ volume customers plus those with over $600,000+ of annual average volume. These are not freelancers, these are true SMB businesses.

We’ve seen north of $25,000 a year in average revenue per user (ARPU) [from these businesses], meaning their ARPU is four times greater than the balance of the portfolio. So we’ve moved the company upmarket. We’ve seen really strong 20% ARPU growth and 60% of our revenue growth coming from larger customers and they’re our fastest growing population.

Michelle Wang:

Our B2B volume growth in Q4 2025 was 21%, versus 11% growth in Q3. We continue to see really nice traction there. The B2B market, as we’ve talked about for many years, is significantly bigger than the marketplace opportunity, and there’s a lot of greenfield opportunity to take share from traditional financial institutions.

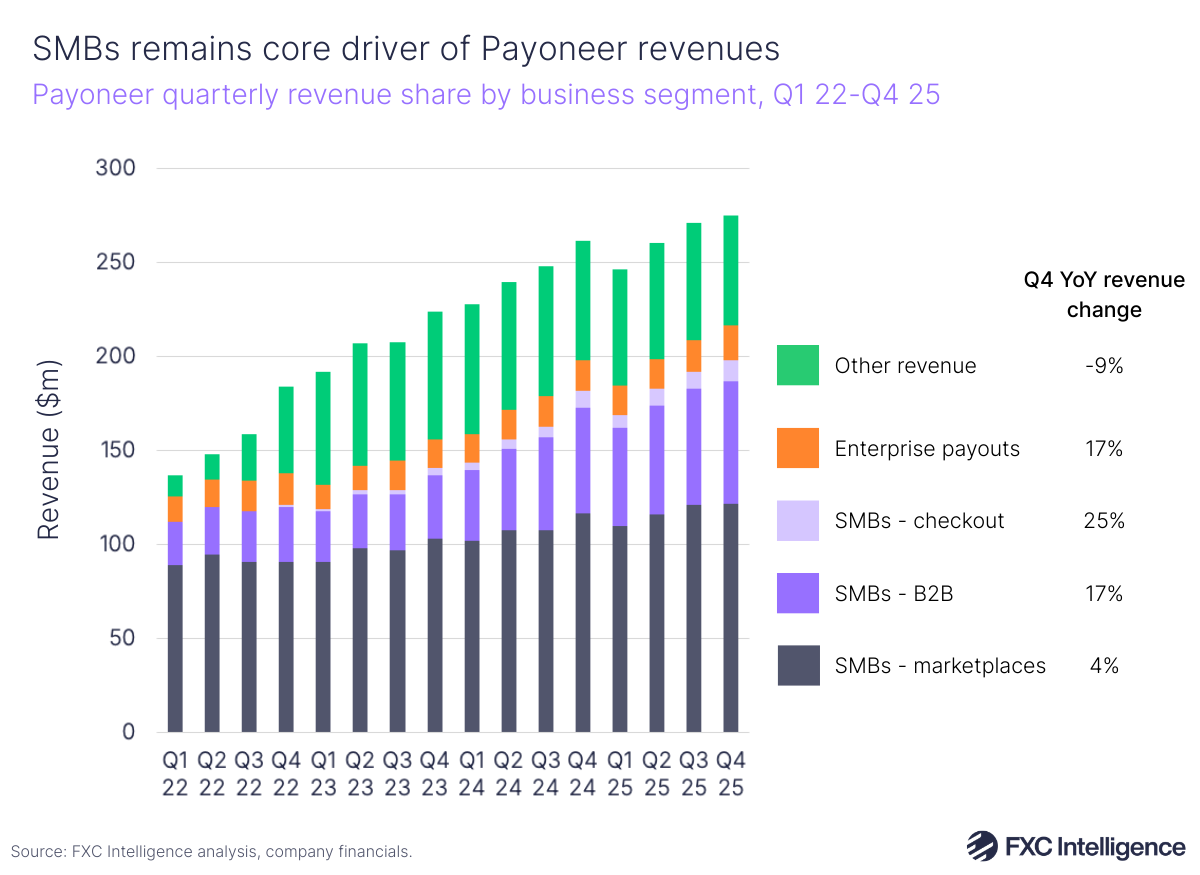

SMBs remain core driver of Payoneer revenues

The SMB segment continues to drive growth for Payoneer, with SMB revenue rising 9% to $197m in Q4 2025 and growing 15% to $742m for the full year.

Marketplaces – which tracks revenues from SMBs who sell on global marketplaces – is still the largest division for Payoneer, with revenue rising 4% to $122m in Q4 2025, driving 8% revenue growth to $469m over FY 2025. In Q4 2025, marketplaces volumes rose by 1%, which was slower than 14% growth the previous year. However, Payoneer noted a strong holiday season with mid-single-digit marketplace volume growth in December, as well as modest acceleration in volume coming into January and February.

The company also notes that certain non-volume revenues it had previously allocated to marketplaces, including those related to banking partnerships and FX, were re-classified to B2B SMBs to “better reflect the customers supporting those revenues”.

Payoneer saw faster growth in its B2B segment in Q4 2025, which tracks services it provides to businesses paying and getting paid by other businesses globally. In Q4, volumes for B2B SMBs grew by 21% to $3.6bn, driving 17% revenue growth to $65m. Checkout, which tracks revenues from Payoneer’s checkout product that enables direct-to-consumer sales (ie. from business’ webpages), grew revenue by 25% to $11m, while enterprise payouts grew by 17% to $19m in Q4 2025.

Based on our calculations, faster growth in B2B and Checkout have slightly lifted their share of Payoneer’s overall revenue mix in 2025, with B2B seeing 23% of Payoneer’s revenue in 2025, versus 19% for the year before, and Checkout rising from 2% in 2024 to 3% in 2025.

How Payoneer continues to grow revenues while adding larger businesses

Daniel Webber:

How are Payoneer’s take rate dynamics boosting the business?

John Caplan:

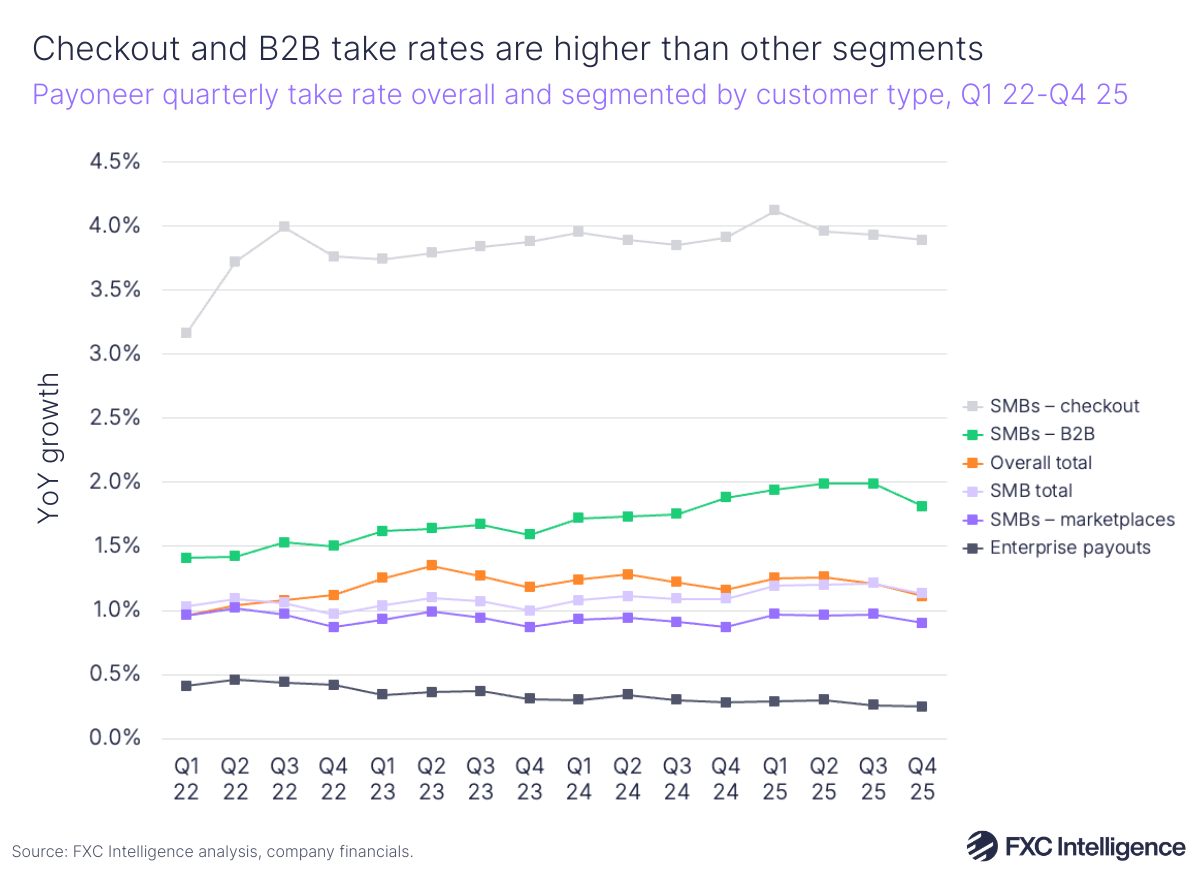

Everybody thinks financial services companies see their take rates go down. Actually, what we’re seeing is larger customers, with more volume per customer, and very solid take rate dynamics across the business over the last couple of years.

From 2022, when I came to Payoneer, our revenues are up 70%. Our total EBITDA is up by more than 5x, while core adjusted EBITDA has gone from -$255m to $40m. So when you look at all of that, we are a very strong company in a very big market. A third of our revenue is now our B2B business and with the stablecoins and the bank charter, we’re moving fast in that.

How does Payoneer’s volume shift affect its take rates?

Payoneer continued to see higher take rates for its SMB Checkout (3.89%) and SMB B2B (1.81%) segments, than its overall take rate for Q4 2025 (1.11%). Meanwhile, take rate for SMB marketplaces was lower than these figures at 0.9%, with enterprise payouts at 0.25%.

Transaction costs were 15.6% of revenue in Q4 2025, down 90 bps YoY, and 19.6% excluding interest, down 180 bps, which the company said reflected improving margins driven by its portfolio.

Going forward, Payoneer aims to boost profits and cut costs by investing in agentic AI-driven solutions and further diversifying the distribution of its labour footprint, including by increasing its presence in India. It projects transaction costs for 2026 to be approximately 15% of revenue, down 70 bps YoY as a result of optimising its bank and processors network, as well as partnerships with Mastercard and Stripe.

How Payoneer is cutting transaction costs as it scales

Daniel Webber:

You’re also significantly driving down transaction costs. How is that helping you scale?

Michelle Wang:

That’s often an underappreciated part of how we’re unlocking leverage in the platform. As you’ve seen, even though we’ve been growing B2B and checkout – higher transaction cost areas of the business – we’ve actually guided to lower transaction costs in 2026. That’s on top of $40m+ of lower interest income.

[Lower transaction costs are] driven by our move to Stripe in our checkout business. Near-term that’ll create a little bit of lumpiness in the growth we’re going to see in 2026, but it’s meaningfully better on transaction costs and adjusted EBITDA. So again, we think this is the right strategic move. It’s also better for customers since they’ll benefit from the full set of capabilities that Stripe offers.

We also announced last year that we had renewed our Mastercard partnership. That also improves economics for us. Broadly, we’re leveraging our scale as we continue to grow with all of our partners to drive more leverage unlock in that line as we go into 2026 and beyond.

Payoneer sees strong growth in APAC despite tariffs

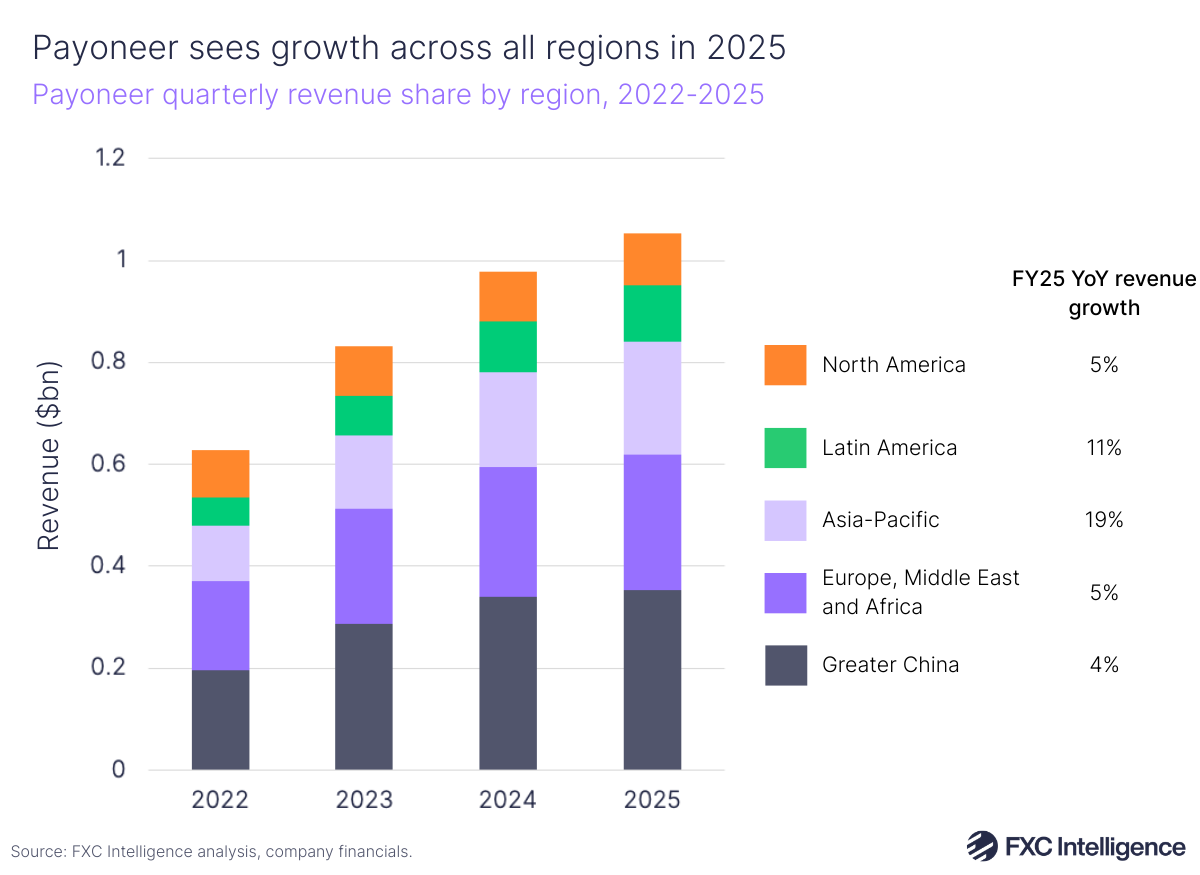

Payoneer’s global network spans 7,000 trade corridors and the company has an on-the-ground presence across more than 35 countries. Payoneer saw growth across all its reported regions in 2025, particularly in Asia-Pacific (APAC), which grew 19%, and Latin America, which grew 11%.

Greater China continues to take the largest portion of revenues, accounting for 34% of Payoneer’s FY 2025 revenue, followed by Europe, the Middle East and Africa (EMEA) with 25%; APAC excluding China with 21%; Latin America with 11% and North America with 10%.

Payoneer sees strong demand for stablecoins proposition

Daniel Webber:

What’s your strategy around stablecoins, and what will the bank charter enable for the business?

John Caplan:

The GENIUS Act gave us a regulatory framework to operate within. Our last mile gives us a value proposition that’s unique, as is the multicurrency account that we’ve had for 20 years and that we’re trusted for. Adding stablecoin rails into that multicurrency account actually turns assets that are being traded into assets that’ll be commercialised. And that’s our role: to turn the potential utility into real utility.

We have over a thousand people that have signed up for Payoneer stablecoin accounts in a week, out of nowhere, with no marketing. People hear that we’re doing it and are joining a wait list to get access to a trusted compliant multicurrency wallet from us. That’s step one.

Then we have the bank charter application, which we made last Monday. If people are connecting the dots, the infrastructure that we offer isn’t just participating in the Swift world. It’s us actually leveraging the network we’ve built and stablecoin rails to drive super speed and lots of utility for the SMBs around the world.

Central banks are not giving up their currencies. So the promise of stablecoin runs through a company like Payoneer. It’s hard for the world to conceive of it because we’re 20 years old and we were born in the marketplace era. We innovated in the B2B arena and now we’re innovating with stablecoins.

Does Payoneer have permission to be that entrepreneurial and innovative at $1bn in revenue? The answer is yes, and we’re delivering. I first talked to you about this 90 days ago and 90 days later, we’re live and we’ve applied for the bank charter. We have $416m of cash on our balance sheet, zero debt and we generated a hundred odd million dollars of free cash flow last year.

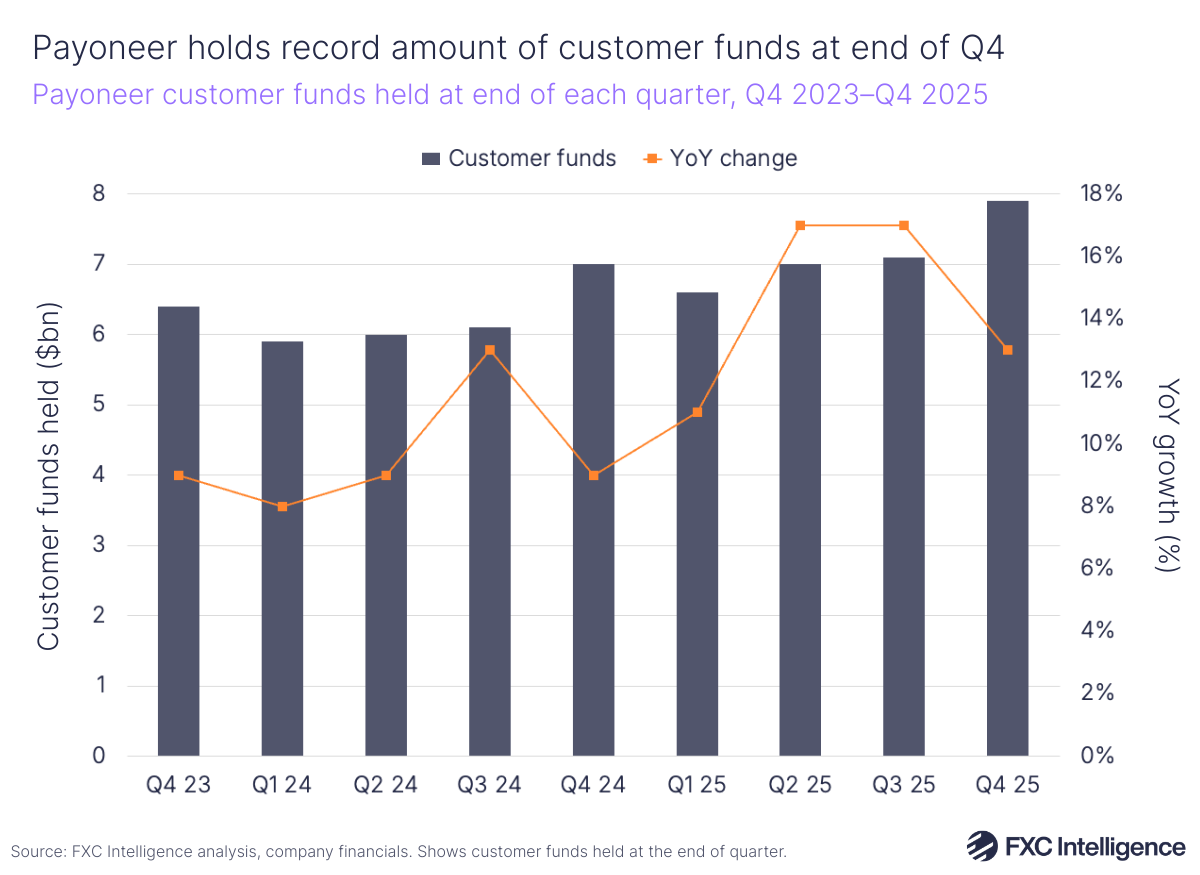

Payoneer grows customer funds on the platform

Connected to Payoneer’s larger customer focus and stablecoins strategy, the company has continued to see more customers storing money in Payoneer accounts. In Q4 2025, the company saw customer funds rise by 13% YoY to $7.9bn by the end of 2025. Payoneer also noted that more than 85% of customer funds are interest-bearing, with around 75% being USD-denominated.

This is significant, as a large portion of Payoneer’s revenue (22% in FY 2025) currently stems from interest income deriving from the amount its customers are holding on the platform. In 2025, interest income declined by 10%, though Payoneer offset this with a 14% rise in revenue excluding interest income.

While customers holding a higher total amount on Payoneer’s platform has offset the impact of lowering interest rates in 2025, the company noted that it has hedged 50% of balances being held in accounts and that the company is expecting more than $130m of interest income for 2026, though it also expects an approximately $42m decrease in interest income for the year.

How stablecoins supports Payoneer’s upmarket strategy

Daniel Webber:

What type of customers will stablecoins add for your business compared to your current customers?

John Caplan:

It’s bringing larger businesses doing more cross-border B2B trade into more geographies. They’re not just selling to the US. They’re an entrepreneur in Germany selling to Colombia and Bolivia and Mexico. It’s the other parts of the globe besides just the developed West that we’re seeing in that.

What’s fascinating about it is we make this, we tell people we’re doing this and 1,000+ people join the waitlist. Everybody wants it, and the overwhelming majority of them are bigger and net new. So, it’s TAM expanding for our $1bn revenue business, and that’s really exciting for us.

Daniel Webber:

John, Michelle, thank you.

John Caplan and Michelle Wang:

Thanks very much.