Payoneer, the cross-border player servicing SMBs, has reported strong growth across the business in Q1, sharing significant updates across its AI and digital asset strategies. We caught up with CEO John Caplan and VP Investor Relations Michelle Wang to discuss the company’s performance.

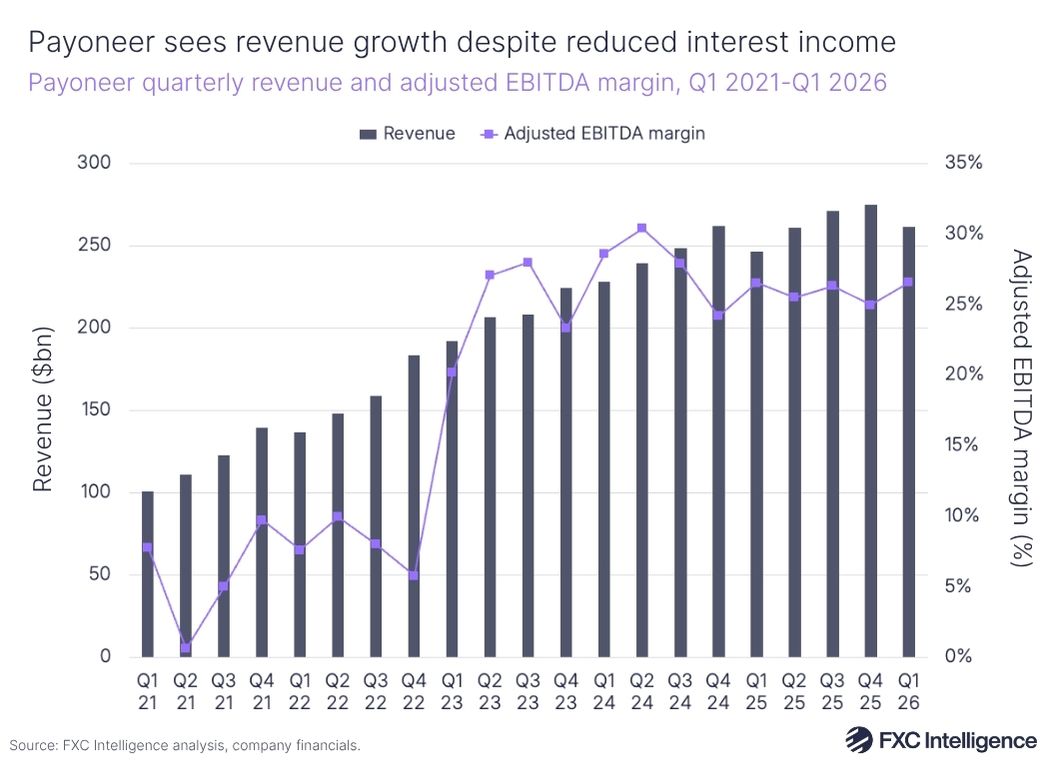

Payoneer reported 6% YoY revenue growth in Q1 2026 to $262m, while revenue excluding interest income increased more quickly, rising 11% to $210m. This comes as Payoneer continues to diversify its income by serving a greater number of “upmarket” customers with more complex cross-border needs and reducing reliance on interest income.

The company is investing further in its stablecoin capabilities, having partnered with stablecoin infrastructure platform Bridge in Q1 to enable its business customers to receive, hold and send digital assets. By leveraging stablecoins, Payoneer hopes to expand its total addressable market (TAM) – sharing during its latest earnings call that around 80% of the businesses that have signed up to the waitlist for these capabilities are new customers. This comes after it applied for a US national trust bank charter in February.

Payoneer has also been piloting AI-powered agents and customer support to accelerate customer resolution time and reduce its overall number of support tickets at any one time. This makes up one part of the company’s AI-strategy, as it also leverages AI-driven insights and lead generation to bolster customer growth, and experiments with AI tools to develop new products more quickly and efficiently.

We caught up with Payoneer CEO John Caplan and VP Investor Relations Michelle Wang, discussing the company’s Q1 results, strategy and stablecoin developments, as well as the early impact of AI on the business.

Payoneer reports profit growth in Q1

Daniel Webber:

You reported very strong Q1 results; what were the key drivers behind continued profitability at Payoneer?

John Caplan:

We delivered $17.9m of core business profitability in Q1, which is $5.1m more than we saw in Q4 and represents our record adjusted EBITDA excluding interest income result. We’ve guided this value to $90m in 2026, whereas last year we saw around $40m.

In 2024, we saw $13m of core EBITDA (ex. interest), in 2025 we saw $40m and this year we’re targeting $90m. So that curve is unlocking a lot of margin for our shareholders and the reality is in Q1 I believe around a third of our total EBITDA was core EBITDA. While I don’t think interest rates are coming down anytime soon, our hedging plus us unlocking greater core EBITDA shows that this is a highly profitable, cash-flowing business that is only going to unlock more leverage as we keep going.

Daniel Webber:

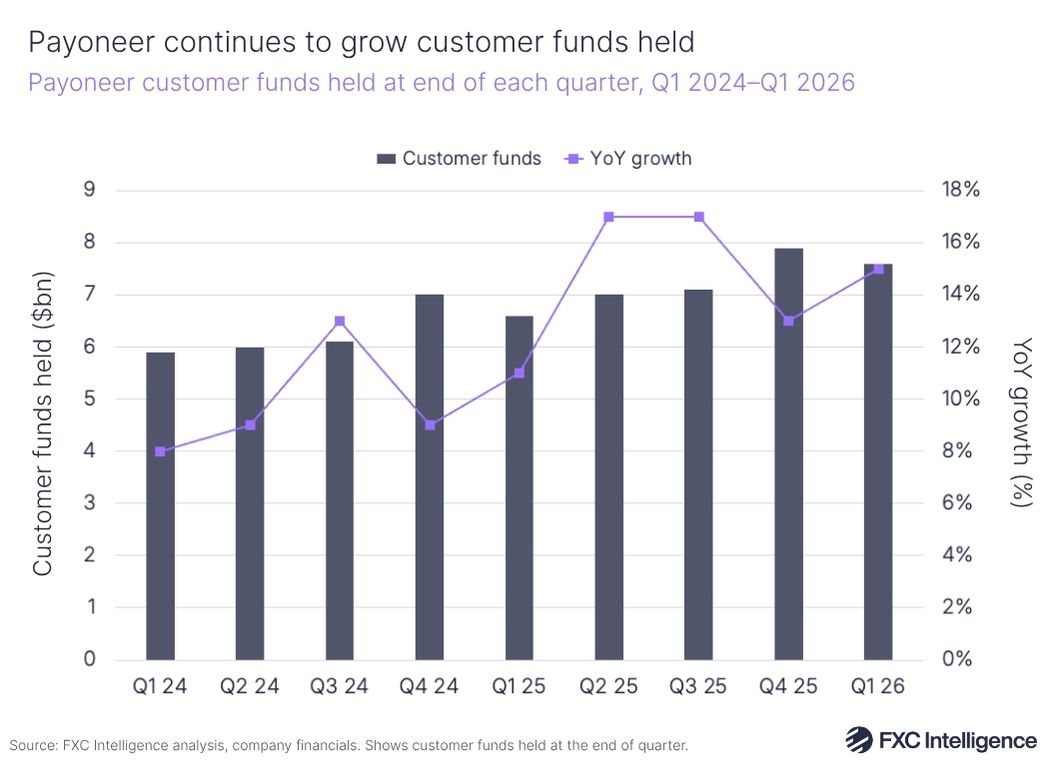

You also saw a significant increase in customer funds, continuing a growth trend in that respect. What can you tell us about the customer behaviours causing this?

John Caplan:

I think it shows that our customers have figured us out better than the market has honestly. Our customers recognise that we’re as much an AP company as an AR company. So they move money from the billion dollars they added incrementally year-over-year that they’re pulling out of their local banks to put in their Payoneer account to use our AP products. The fact that Payoneer’s customers are so happy with our AP products that they’re pulling their balance sheet from their traditional bank and putting in their Payoneer account is proof that we’re as much an AP company as an AR company.

Payoneer’s Q1 2026 earnings highlights

Payoneer saw its adjusted EBITDA grow 6% YoY to $69m in Q1, while its adjusted EBITDA excluding interest income grew 140% to $18m. The company’s processed volumes also increased 16% compared to Q1 2025, rising to $23bn. During the latest earnings call, Caplan attributed revenue growth to increasing momentum in its B2B franchise, alongside strong performance for its checkout division.

Overall, Payoneer saw net income fall 5% YoY to $20m as the company invested more into its stablecoin and AI capabilities, as well as its product roadmap.

Payoneer has also increased its 2026 guidance, outlining a new range for total revenue between $1.1bn and $1.14bn – a $10m increase to both ends of the range.

Payoneer sees strong B2B volume growth

Daniel Webber:

Payoneer reported standout B2B volume growth in Q1 earnings, what drove that?

John Caplan:

The first big driver there was our China B2B business saw exceptional growth in Q1 YoY. We have good product market fit. We have a big brand and the export of wholesale distribution of goods from China is a very big opportunity and we are super well positioned.

Second, as we’ve moved upmarket in services companies, our customer acquisition is exceptionally strong and we have seen the activation of them quickly. This is particularly true in EMEA and in APAC, where we have seen really exceptional growth from those.

The third is that we have become an AR and AP company in equal measure. As a result, marketing services firms in Dubai, for example, choose Payoneer because we’re the best solution for them to use to manage their global spend for their marketing services clients. They’re buying ads all over the world and they use the Payoneer virtual card and other products to manage that spend. That is acquiring a tremendous amount of volume onto our platform.

On the B2B AR side of things, our invoicing capability continues to scale and we’re seeing more and more of our global customers use Payoneer to invoice their customers around the world. So, we’re growing on both sides.

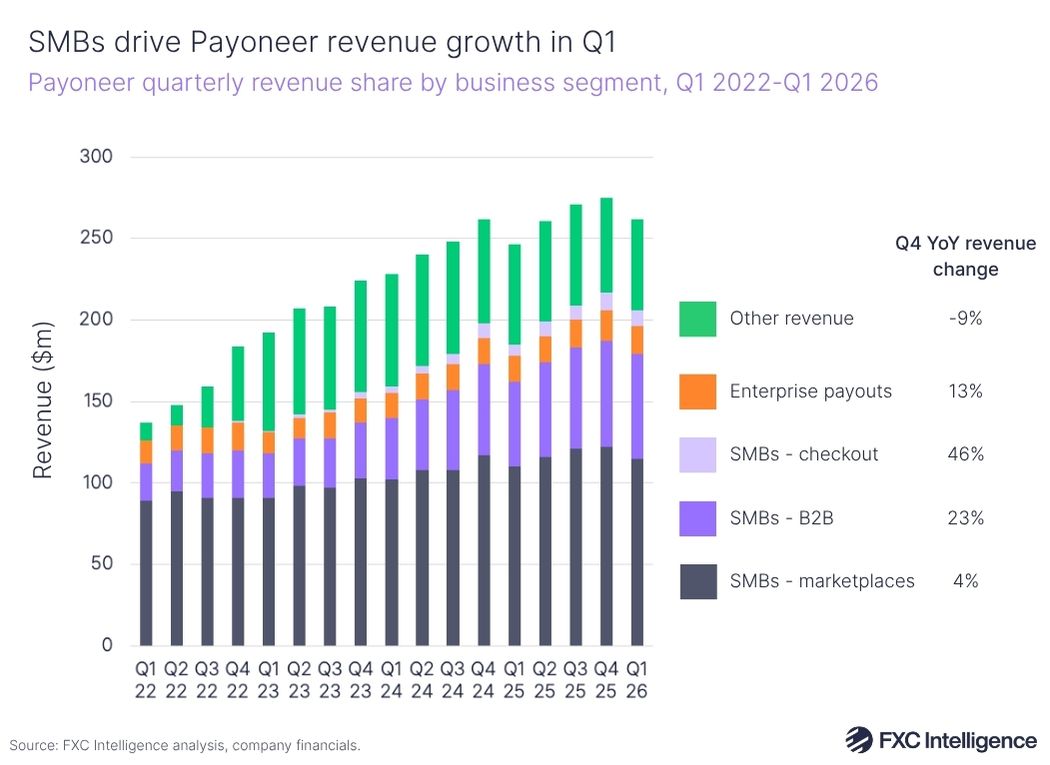

SMB divisions drive revenues in Q1

Payoneer’s SMB segment remains a key growth driver for Payoneer, growing 12% YoY overall to $189m for the quarter.

Within this, marketplaces, made up of revenue from SMBs which sell on global marketplaces, is the largest division – growing 4% to $115m. Payoneer’s checkout division (formerly known as merchant services), which tracks revenues from Payoneer’s checkout product that enables direct-to-consumer sales, saw the fastest growth – increasing 46% to $10m.

Payoneer also reported strong growth in its B2B segment (revenue made from services it provides to businesses paying and receiving payments from other businesses) in Q1, seeing it increase 23% to $64m. It also reported 13% growth for enterprise payouts to $17m.

SMB growth has resulted in its overall share of revenues growing 361 bps from Q1 2025 to 72% in the latest quarter.

Stablecoin capabilities bolster Payoneer’s offering

Daniel Webber:

Payoneer has a sophisticated digital asset strategy, can you bring us up to speed on the latest developments there?

Michelle Wang:

We’re really excited about the progress we’re making in stablecoin and we have made a lot of progress in only six months. In January we partnered with Bridge, a Stripe company, to leverage their wallet capabilities and offer them to our customers. We have already seen thousands of customers show interest in this and sign up. We are now beginning to onboard the first group of customers and we’re trying to do that at pace.

What’s really interesting is a large portion of these customers are new to Payoneer, which validates our thesis that this will actually expand the TAM for us. Second, the majority of these customers are also large businesses, proving the value of the product beyond just speculation. This is really demonstrating that there’s real business use cases, from customers that are doing hundreds of thousands to millions of dollars of monthly average volume cross-border volume.

We have also applied for the bank licence to eventually bring these capabilities onto our own platform, which will enable better economics for us – both from a transaction cost perspective and also for us to be able to earn interest income on the funds held in stablecoin assets down the road. So we’re really excited.

We’re also trying not to get ahead of ourselves here. Right now, it’s about learning, testing and pivoting quickly. You could almost think of this as a startup within Payoneer and we’re trying to enable it to move fast, adapt and pivot as needed as are still at the very forefront of real-world stablecoin use cases.

John Caplan:

I was reflecting on this over the weekend following our earnings because they were obviously very good and the response was really positive, but one of the questions that came up was about why we aren’t hyping it the way others do. And the truth is because we have a profitable cash-flowing business growing.

As Michelle described it, we’re not trying to build a flash in the pan venture-backed stablecoin company. We’re trying to take the unique assets we built over 22 years and introduce digital assets into that network. This will enable us to add new customers that we currently don’t have and add new capability for the customers that we do.

Payoneer grows customer funds held on its platform

Part of Payoneer’s plan to develop its strategy to target larger customers revolves around holding a larger amount of customer funds on its platform. In Q1 2026, it saw the amount of customer funds it held at the end of the quarter grow 15% YoY to $7.6bn. Caplan explained that this is also up over $1bn on the total it held at the end of Q1 2025 – highlighting the rapid pace of growth it is seeing in this respect.

This growth helped Payoneer to offset the impact of lower rates on its interest income revenue, having generated $52m of interest income in Q1 – an 11% decline YoY.

Making Payoneer AI-native

Daniel Webber:

You also shared that Payoneer is piloting AI agents to drive customer growth. What can you tell us about this and the other ways that AI is having an impact across the business?

John Caplan:

I’d say we’ve entered our second phase of AI. The first phase was deep inside of our platform and engineering organisation. We’re undergoing a great deal of experimentation to drive velocity, which is working really nicely. We have strong proof points of AI-enabled engineers and product organisations delivering higher quality output more quickly.

The second phase, which we’re just beginning to enter, is becoming an AI empowered company. What that means is looking at the workflows of our 2,500 people around the world, from operations, compliance, finance, marketing, sales and operations – the entire company – and supporting them with AI to help them do their jobs faster.

For example, we have a prototype in place with our operations team supporting all of the workflow our customer care organisation does globally to support customers. That is already reducing costs and improving speed. We’re also working with Oscilar, which is a great firm partnering with us on AI-enabled risk scoring.

Ultimately, we’re now moving from experiment to empowerment. I think it will take us a couple of quarters before we become fully AI-native. We are headed towards an AI operating model but it will be a journey of steps over several quarters for us to get there.

My view about AI is that it is AI’s job to make our talented people more productive. We’ve hired the world’s best people to work at Payoneer and they are not disposable. We actually believe they’re exceptional and we want to use AI to help them be even more exceptional. There are also certainly opportunities to unlock meaningful cost leverage in our business.

Payoneer reports strong growth worldwide

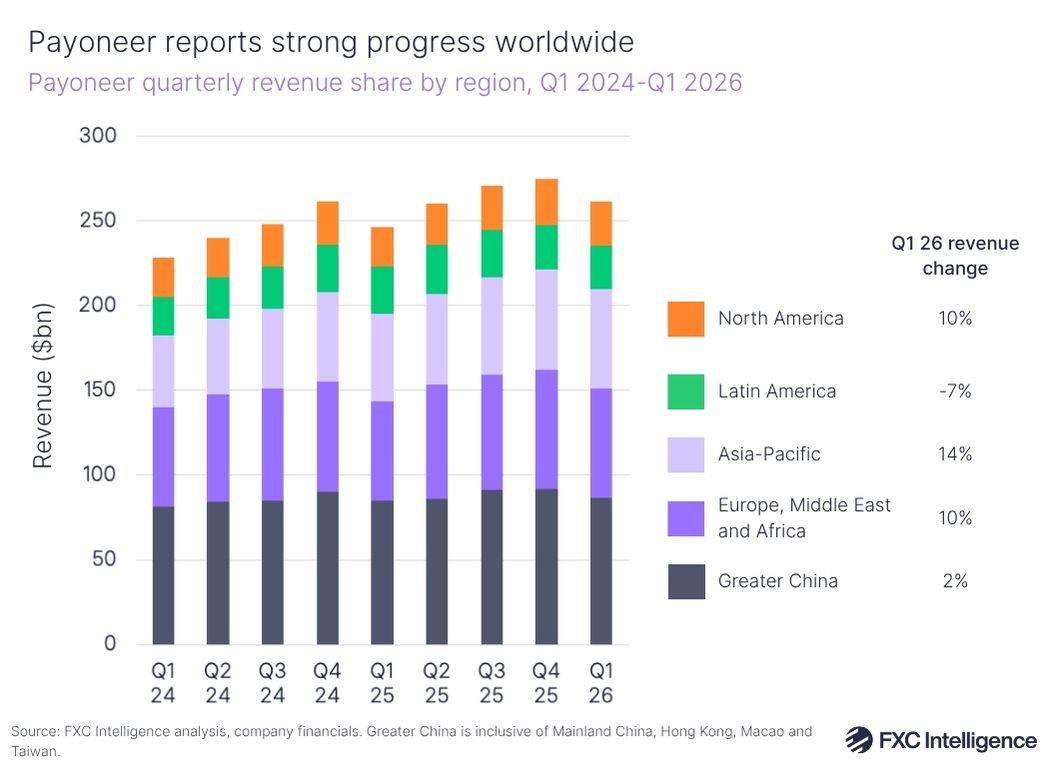

Greater China – covering Mainland China, Hong Kong, Macao and Taiwan – continues to provide the largest share of Payoneer’s revenues of any region (34%), growing 2% YoY to $87m.

Asia-Pacific saw the fastest growth of any region in Q1, with revenue from the region increasing 14% to $58m – growing its share of overall revenues to 21%. EMEA and North America revenues both increased 10% YoY to $65m and $26m respectively, while Latin America revenue fell 7% to $26m but its share of overall revenues remained at 11%.

The company also shared that it has seen strong growth across the globe for its B2B business, with particular strength in China, APAC and EMEA. Caplan also shared that Payoneer has seen good progress in Latin America, where it is seeing strong growth as it moves upmarket in the region.

Payoneer completes Stripe migration

Daniel Webber:

Is there anything else you’d like to share before we go?

Michelle Wang:

I would add the success of our checkout business. We made the strategic decision at the end of 2025 to move those capabilities onto Stripe’s platform. They’re providing all of the underlying infrastructure to power the checkout product while we still own the customer relationships and the distribution.

We completed that migration at the end of April and it has gone phenomenally well – better than even we had anticipated. It’s not an easy process by any means to move all of your customers from one platform to another and it’s the first large-scale migration we have done, so we naturally expected some level of customer churn. We assumed that the friction associated with the migration would result in some customers not coming along.

However, we have retained over 90% of those customers and we’ve updated our assumptions of where that business will be this year.

John Caplan:

Absolutely, we’re starting to see what happens when we help our customers get paid from their customers as well as helping them pay out to their suppliers or pay their contractors and source their raw materials.

Daniel Webber:

John and Michelle, thank you.