Rapyd has launched Stablecoin Payment Solutions, making it one of several cross-border B2B payments providers to formally launch a new stablecoins solution in the space. In this exclusive interview, we speak to Rapyd CEO Arik Shtilman about how stablecoins fit into the company’s global strategy.

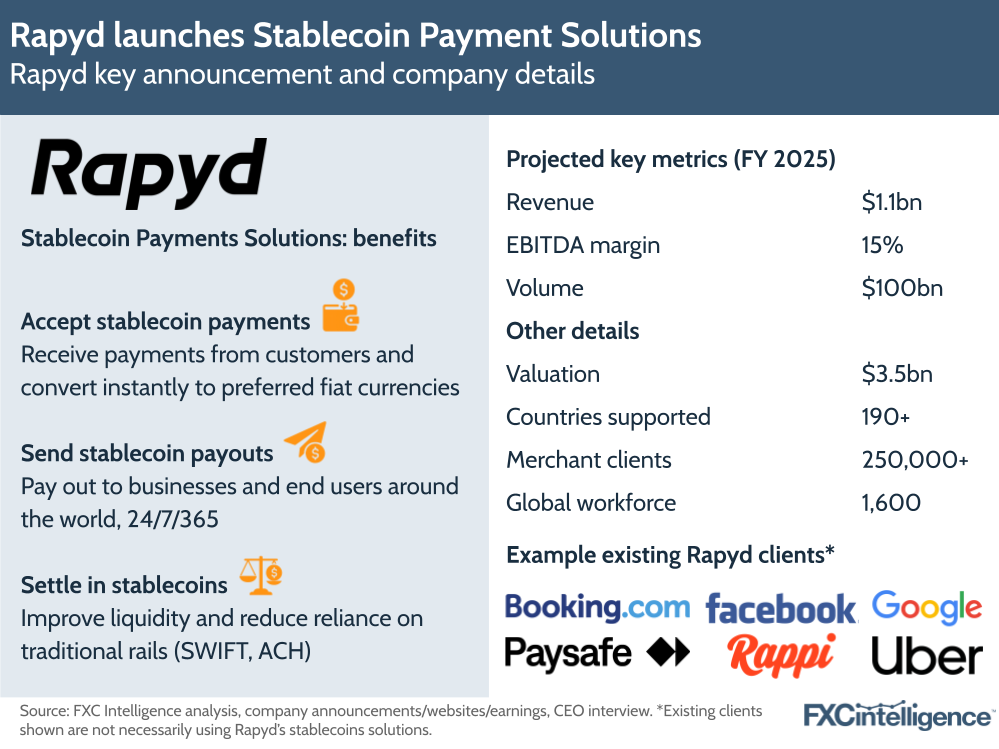

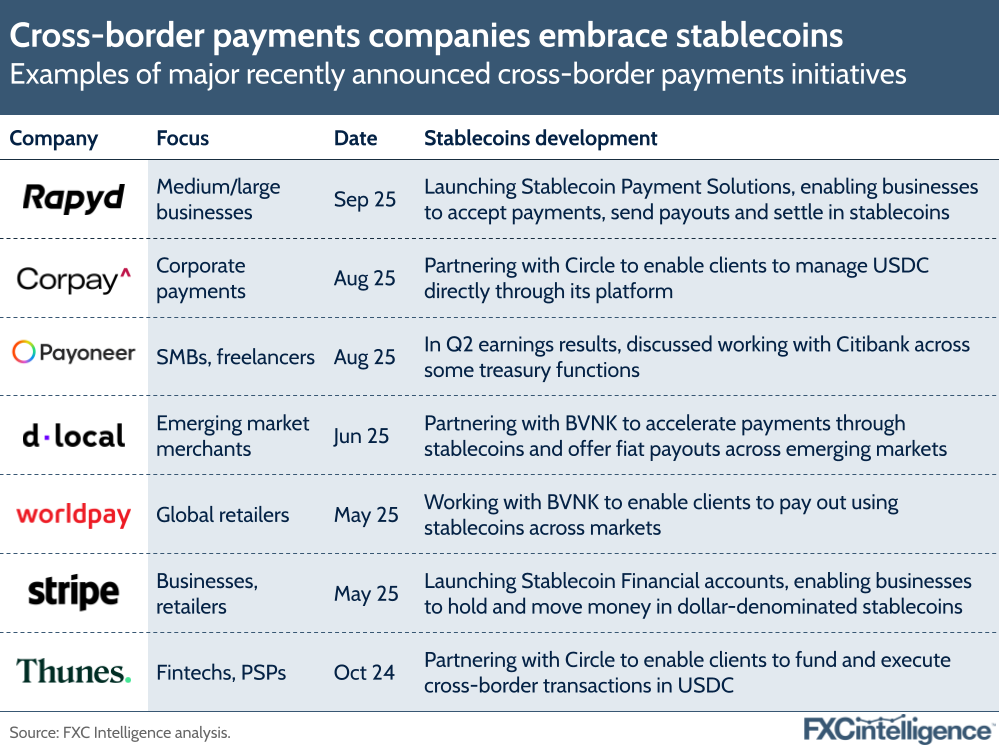

New acquisitions, partnerships and the passing of regulations such as the GENIUS Act are spurring a wave of cross-border payments companies to launch new solutions in the stablecoin space. Today, Rapyd has launched Stablecoin Payment Solutions: a new suite of offerings enabling businesses to accept, send and settle stablecoin payments around the world instantly.

Specifically, Rapyd’s new offering will allow platforms and marketplaces to accept stablecoin payments from global customers and instantly convert them into their preferred fiat currencies. It will also allow business to send stablecoin pay-outs securely to other businesses and end users globally 24/7/365, bypassing intermediaries and fragmented systems that can cause delays. Businesses will also be able to settle transactions instantly, allowing them to improve their liquidity and reduce reliance on traditional rails such as Swift or ACH.

Rapyd’s launch further embeds digital assets into the company’s already sizeable global payments network, which spans 190+ pay-out countries and enables payments across more than 900 payment methods. As a major growing player in the B2B cross-border space, the product launch reflects the continued relevance of B2B to stablecoins – our industry primer found that the B2B stablecoins cross-border payments market accounts for around $13tn of baseline opportunity, with a series of new players cropping up specifically to target this opportunity.

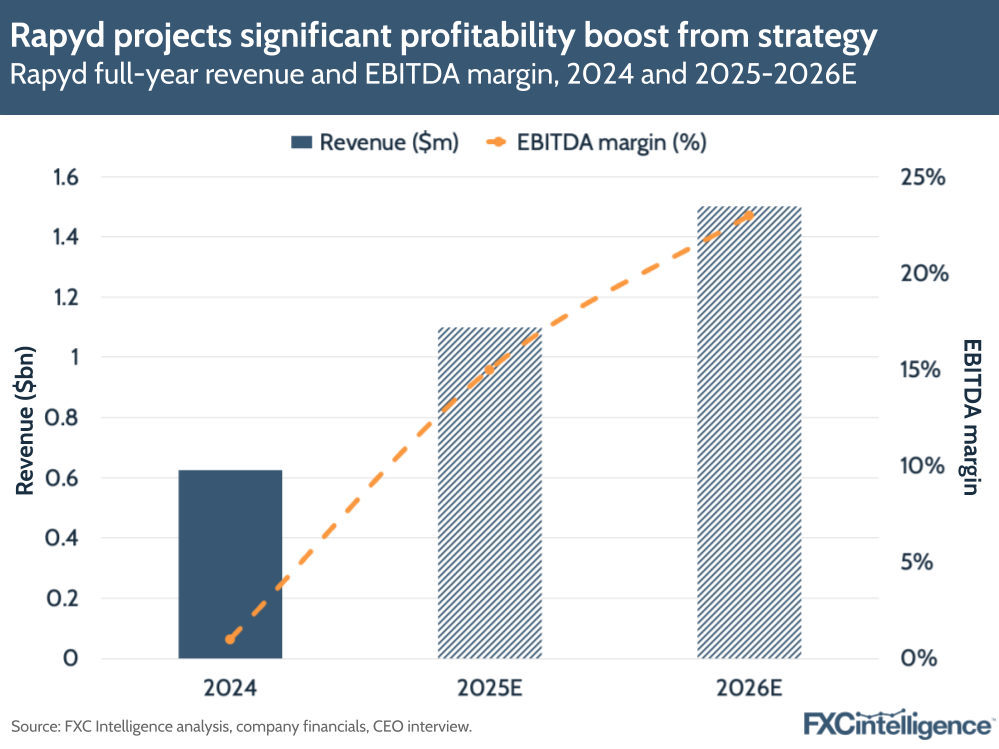

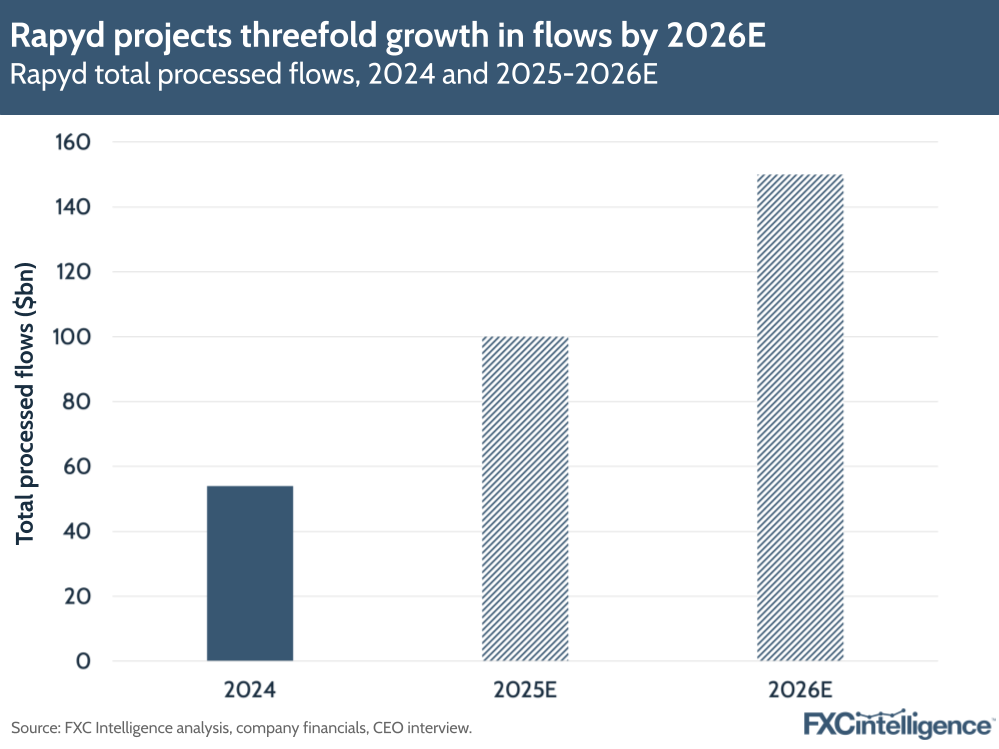

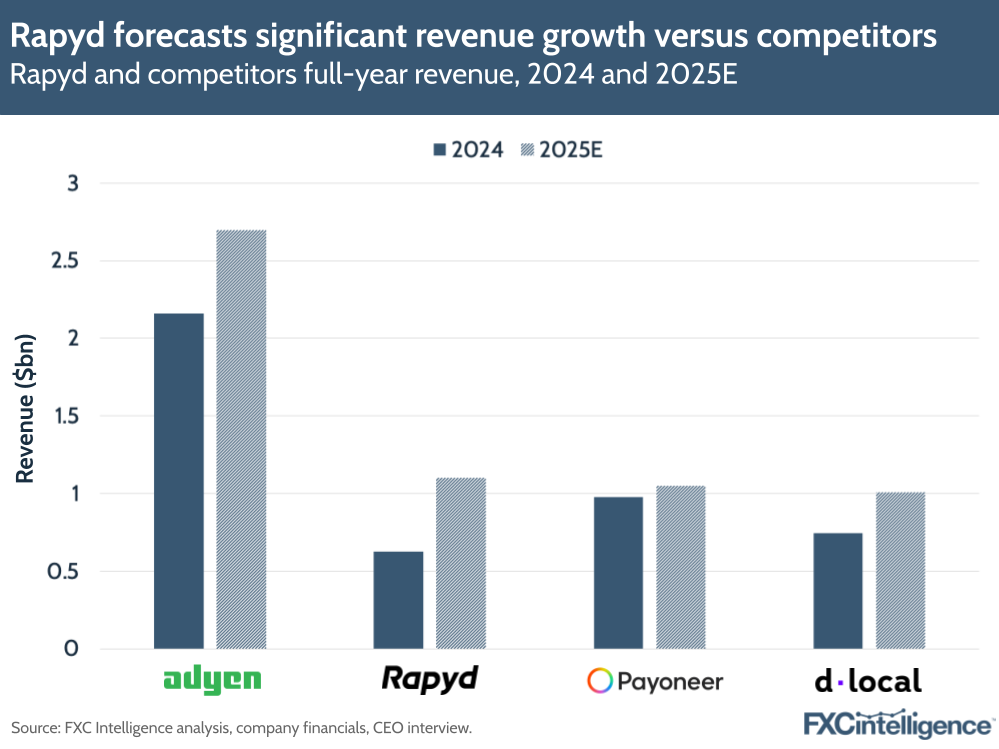

In an exclusive interview, CEO Arik Shtilman told us the company remains on track to grow the company’s revenue to around $1.1bn in 2025, a 76% increase on its 2024 revenue, largely driven by its PayU acquisition – completed in March 2025. He added that the company also expects a significant increase in its EBITDA, which will be around 15% of total revenue, with processed volumes currently expected to grow to around $100bn in 2025 and $150bn in 2026.

Rapyd sees stablecoins as being a key driver of its profitability going forward. We asked Arik what’s driving Rapyd’s move into stablecoins, how it aims to integrate the technology with its existing payment rails and how the company sees the space evolving in the coming years.

Inside Rapyd’s wider stablecoins strategy

Daniel Webber:

What is leading Rapyd to do something with stablecoins now, and where does it fit into your overall strategy?

Arik Shtilman:

Rapyd for years has been around traditional payments, fiat payments, operating across the globe in many countries, including some emerging markets. Crypto was always something we looked at, but our banking partners believed crypto is something they don’t want to be involved in, it’s dangerous.

Every time there was anything crypto-related, our banking partners were hesitant to support it. Due to this reason, we focused on fiat. In 2024, when we started to see the stabilisation of stablecoins and also the election of Donald Trump to become the president of the US, this turned stablecoin into something mainstream.

We saw overnight after the elections in the US that all the banks we operate in, not only American banks but all banks, became very pro-crypto and especially pro-stablecoin. This opened the door for Rapyd to be involved more in crypto and especially in stablecoin.

As a company that specialises in cross-border payments, for us, stablecoin is a completely new way of moving money and creating treasury hubs from a liquidity perspective. It changed the way we operate across the globe.

In the past, we had settlement hubs in Singapore, the UK, Europe, Brazil, Mexico – moving money, holding money in local currencies and moving it over Swift, trying to use liquidity ports to net funds between places.

Now we have a more sophisticated backbone based on stablecoin that allows us to convert funds into stablecoins and move them immediately. It significantly reduced our working capital (by tens of millions of dollars) because we needed less working capital to operate the business. And it allowed us to offer our clients stablecoin settlements.

At the beginning, we were sceptical about how many of our clients would like stablecoin settlements, and we were surprised that a lot of our clients were interested in getting paid in stablecoins: to reduce the time to get money, especially over Swift in some long-tail [complex] markets; increase their liquidity; and reduce their working capital and cost of capital by getting settled in stablecoin. We started to offer this a year and a half ago.

In the first six months of 2025, we generated $10m in revenue only from stablecoin settlements to our clients – this is our revenue, not the volume. This volume is doubling every quarter. There is huge demand for stablecoin settlements, even from the largest merchants that you wouldn’t think have any interest in doing anything with stablecoins.

Because funds move significantly faster and you can reduce your cost of hedging against some volatile currencies by using stablecoin, it opened the door and appetite for some of these clients to work with us.

We have also just launched stablecoin pay-outs, which is different from settlements where you pay out [in fiat]. In stablecoin pay-outs, we had around 1,000 clients jump on our beta offering after launching – [they were] immediately interested in using it, because they prefer to pay out invoices or pay out to contractors through our platform in stablecoins. The popularity is growing exponentially. It is very interesting for the payments industry, not only because you can circumvent Swift and move money much faster, but because you can offer something quite unique in the space that traditional payments and traditional banking companies don’t do.

In the past, if somebody wanted to do it, they had to partner with a crypto company and move money to the exchange and transfer. Now, when you get it all in one inside the Rapyd system as part of the treasury we provide, it allows you to be very flexible with your money.

Key use cases for Rapyd’s stablecoin products

Daniel Webber:

What are the key benefits to clients and use cases? You’ve mentioned faster speeds, lower costs, less working capital, lower volatility, holding alternatives to currencies that may be inflationary – is there anything else? Talk us through what’s resonating and who your main client targets are.

Arik Shtilman:

Latin America has the biggest traction and the second biggest region is Southeast Asia.

Clients operating with us in Latin America who want to get settled into European Union hubs – for example, the Netherlands – used to collect payments in Latin America and get settled by converting Colombian pesos or Peruvian currency into US dollar or euro domestically in Latin America with very high margins from local banks, and then send the money over Swift, which can take two to three days to arrive. They’re waiting for the money.

We switched the settlement system so we don’t use the banks anymore. We just convert local currency into stablecoin and settle the same day immediately. This reduced the two to three days [to instant] and increased the margins because you don’t use local banks for FX – you use exchanges on the crypto side. The exchange rate is dramatically better than what the banks provide in some of these countries.

Everybody’s happy. The payments company is happy because the margin is better. The client is happy because he pays less for FX and gets the money two days earlier. A super simple use case is long-tail markets. This is why stablecoin was born. Stablecoins such as USDC and USDT were not born to allow money movement inside the US – it is not interesting. You can move money in the US dollar domestically.

But when you’re in a long-tail market – Indonesia, Thailand, Colombia, Peru, Chile or wherever it is – and you need to move money in euro or US dollar to Europe, it’s a nightmare using the banking system. That’s one amazing example.

Daniel Webber:

How much are you seeing people want to hold on to the stablecoin as a way to hold USD?

Arik Shtilman:

A lot. They prefer to hold it. We’ve seen it with many clients. They move out around 60% of the money because they need to pay invoices, suppliers, salaries and so on, but [the rest] they keep.

How stablecoins fit into Rapyd’s revenue mix

Daniel Webber:

What’s the mix of stablecoins you are seeing used most? And what proportion of Rapyd’s flows are being taken up by stablecoins?

USDC and USDT are the most commonly used. In the first six months of 2025, you’re talking about something in the range of $500m worth of stablecoin settlements out of around $50bn of processed volume. It’s still a small subset. The impact on revenue is significant because we generated $10m of revenue, all of which is basically gross profit because costs are so small, and it all goes to EBITDA. It has a very big impact on profitability.

Stablecoin settlements will probably contribute around 15-20% to profitability this year, and we’re going to be above the forecasted EBITDA by around 20% – almost all of it from stablecoin settlements. Overall, we will be at around $1.1bn in revenue this year. EBITDA will be around 15% of the revenue.

Daniel Webber:

Explain the revenue model for your stablecoin solutions – how do you charge people?

Arik Shtilman:

It’s very simple. We don’t charge for the stablecoin. Instead of the bank charging us the FX fees for converting currencies and sending them over Swift, we do the FX on our own by converting fiat into stablecoin.

How stablecoins could change the cross-border payments market

Daniel Webber:

How do you see this evolving in two year’s time? What’s going to stay in fiat, and what’s going to move into stablecoin?

Arik Shtilman:

I believe everything related to cross-border money movement is going to be in stablecoins. To say it will be USDT and USDC – no. At a certain stage there will be a new stablecoin that will be regulated to replace Swift to allow money movement. I think it will come in a five to seven-year timeframe, so not quickly.

I don’t think the existing stablecoins as we know them will be the ones used by banks to move money. Something will come like a digital version of Swift based on stablecoins. The stablecoins that we are familiar with today, USDC and USDT, are the ones that will survive in the long term to provide, especially in emerging markets, a solution for holding the US dollar without exposure to very volatile local currencies.

An update on Rapyd’s PayU acquisition

Daniel Webber:

Aside from stablecoins, what else is driving Rapyd this year?

Arik Shtilman:

Rapyd completed the acquisition of PayU in March 2025, six months ago. We are migrating the PayU tech stack into the Rapyd tech stack, which we would like to complete by the end of the year – this is ambitious, but we’re working hard to do it. We have already introduced Rapyd capabilities and technologies to PayU clients, including stablecoin settlements, which is purely Rapyd technology.

Our plan is to migrate the PayU portfolio into the Rapyd tech stack by Q1 2026. This will allow us to serve these clients better and offer them Rapyd products, such as the disbursement, the issuing, the wallet, the pay-outs and stablecoins. This will significantly increase Rapyd’s profitability.

We believe profit next year will be 3-4x higher, due to the migration of the PayU tech stack and cost savings, plus cross-sell capabilities. We believe the company will be on track next year to do $1.5bn in revenue and around $350m of EBITDA. This will lead us into Q1 2027, our target date to go public in the US.

How AI is driving efficiency and lower costs

Daniel Webber:

Aside from stablecoins, what are the other big changes in the cross-border payments market? Is AI having a significant impact on your company?

Arik Shtilman:

AI is a big thing. AI completely changes the way payments companies and financial services institutions operate. Around 95% of our compliance and risk operations work is done by AI. It’s a big cost reduction, because you need fewer people, and it is a dramatic revenue accelerator because you can onboard clients in less than an hour or less than a business day, compared to when it used to take three to seven business days or sometimes a month to get the client live.

AI changes the backend of financial services and payments, streamlines a lot of the operations, and reduces a lot of the cost. If you look at our projected headcount expenses versus revenue, the headcount is flat and going down while the revenue goes up. This is the big thing in payments in the next three to five years – AI adoption and building on top of AI financial services capabilities.

Who are Rapyd’s competitors?

Daniel Webber:

What other companies should we think about comparing Rapyd with, particularly considering your upcoming IPO plans?

Arik Shtilman:

In payments, there are not many publicly traded companies. The comps are complicated. The comps we mainly see (and this is also from the conversations with banks I’ve been talking to) are Adyen, PayPal, dLocal and sometimes Shopify, because many see Shopify as a payments player and less as an ecommerce plug-and-play.

I hope Stripe will go public soon, because then there will be another comp. At the current stage, if they don’t go public, they’re not a comp.

Daniel Webber:

Finally, have the US tariffs had much impact on your business?

Arik Shtilman:

Nothing. I think 0.59% of the total volume, plus PayU, is related to tariffs.

Daniel Webber:

Arik, thank you.

Arik Shtilman:

Thanks very much.