Remitly reported continued growth in Q1 2026 and outlined plans to target new customer segments, further improve efficiencies and utilise new technologies. We caught up with the company’s new CEO, Sebastian Gunningham, for more insight.

Remitly has seen strong results in Q1 2026, exceeding previous revenue and adjusted EBITDA expectations and once again reporting record numbers.

These results come off the back of a busy first quarter for the remittance player, having appointed former Banco Santander executive Sebastian Gunningham as CEO in February after co-founder Matt Oppenheimer stepped down to begin leading Remitly’s board as Chairman.

Remitly has also looked to further expand its reach, extending its country support for its WhatsApp Send offering to 14 new countries, including India, Mexico and the Philippines. This supports part of Remitly’s plan to capture growing demand in Latin America, particularly following the implementation of the 1% federal tax on cash remittances in the US – seeing WhatsApp Send as a uniquely positioned offering that can help convert previously offline senders to using its digital offerings to send money home.

We caught up with Remitly’s new CEO Sebastian Gunningham to discuss his first three months in the role, the company’s Q1 earnings and how it is approaching the coming year by expanding its capabilities and reach.

Remitly’s opportunities for growth

Daniel Webber:

Sebastian, you’re around 90 days into your role now, how do you reflect on the beginning of your time as CEO?

Sebastian Gunningham:

To begin with, I’ve had no downside surprises. When you join a company, one of two things happen – you start to peel the onion and either uncover some surprises or things are even better than you were told and joining Remitly has definitely been the latter during my first 90 days. My predecessor Matt Oppenheimer and the team have built a very strong company.

But I have come across a few positive surprises. The first is that the markets are bigger than I thought. These are very large markets and there is plenty of space for more than one winner. We only have three or four percent of our core market, while we have no share of other markets – so there is plenty of room to grow.

To capture this opportunity, I have organised the company to focus on four key customer segments for our new growth framework. Our core product is focused on remittances and people sending money home, but we started to see people sending $5,000, $10,000 or even $50,000, which is a completely different type of customer. Even though our product isn’t perfect for that, our volume has been growing – so we’ve organised ourselves to make that a big part of our business.

Remitly reports record financials in Q1

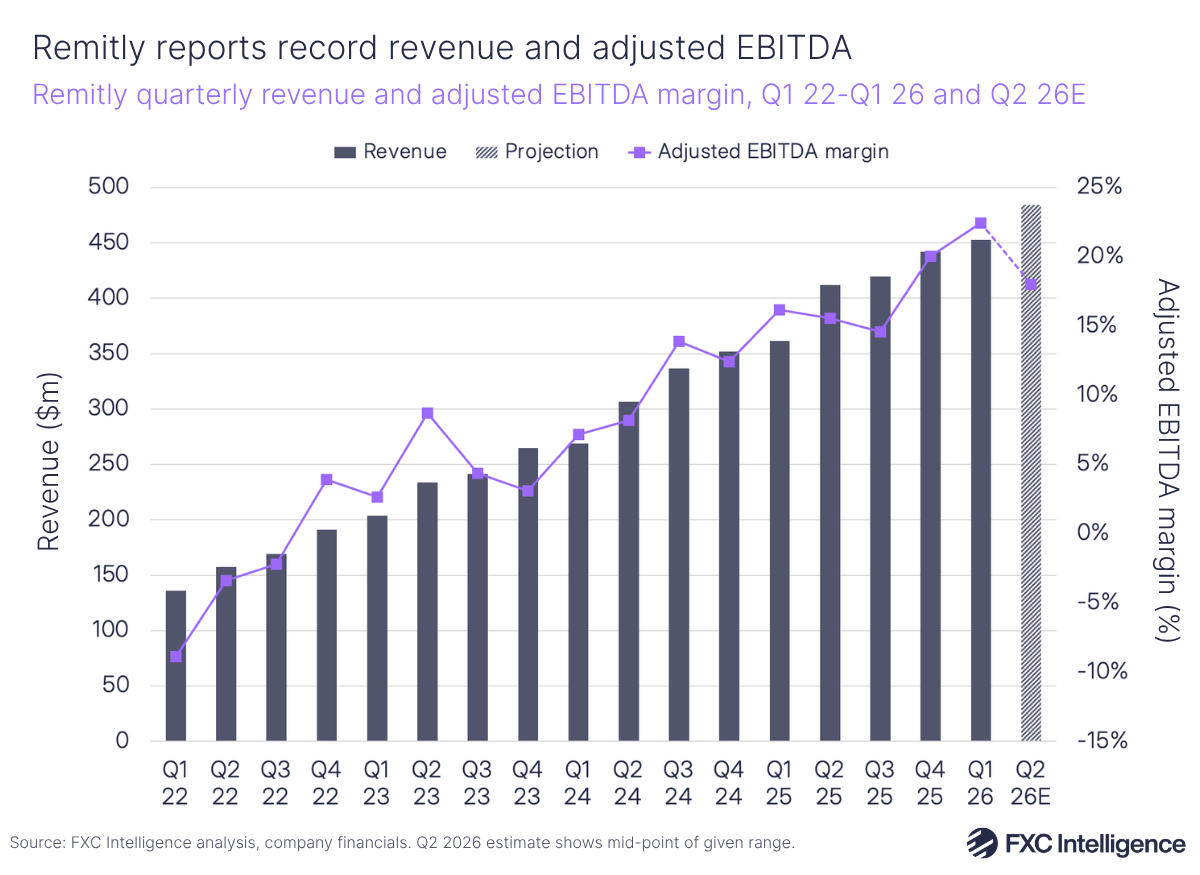

Q1 2026 saw Remitly report a 25% YoY increase in revenue to $452.8m, matching the growth rate seen in the company’s last two quarters. This was $14.8m more than the top end of its projected revenue range for the quarter, which it had outlined to be between $436m and $438m.

Remitly also saw its adjusted EBITDA increase 74% to $101.6m, far exceeding its projected range of $82m-84m for Q1 and resulting in an adjusted EBITDA margin of 22%.

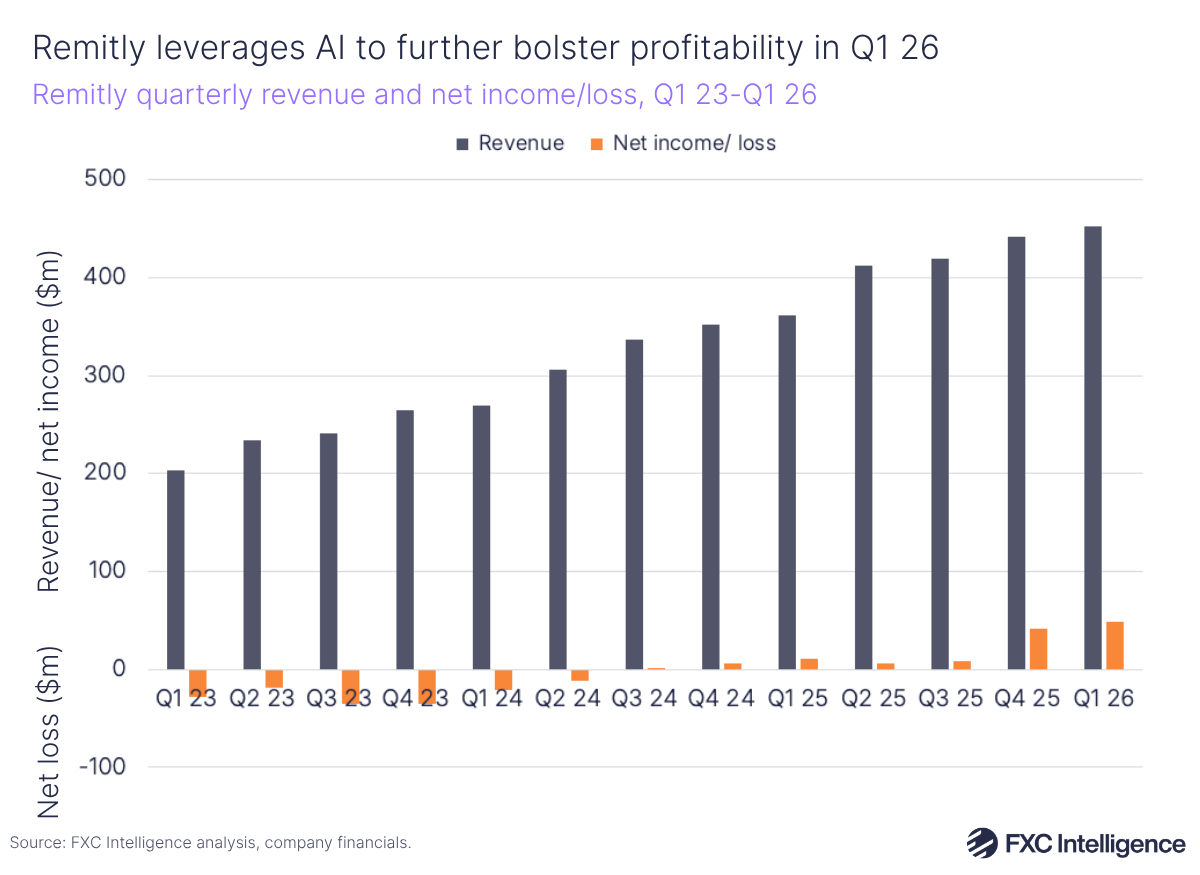

The company also reported its seventh consecutive quarter of positive net income, with this figure reaching $49m in Q1 2026. Remitly explained that disciplined cost management and AI-driven efficiencies were key drivers in the growth of its profitability during the quarter.

Remitly’s new growth framework

Daniel Webber:

You’re introducing a new growth framework to Remitly, what more can you share about it?

Sebastian Gunningham:

We have a new 4×4 growth framework, where we’re targeting four big customer segments. One is the core sender who sends an average of $250 once or twice a month and this is usually people sending home. Another is the high-value sender, who sends anywhere between $5,000 and $100,000 – we’re drawing the line at $5,000 for now. Then there are businesses, ranging from the largest businesses to the huge amount of small businesses.

Finally, there are the receivers – hundreds of millions of people around the world receive money in one currency and then spend it locally. In many cases, those customers don’t even know it was Remitly that sent them the money. Now, we’re starting to test the waters and last month we saw our first set of receivers around the world signing up to get money from Remitly, we’re issuing them cards they can use to spend locally. We don’t know exactly how big that market will be, but we know that the infrastructure that we have built to move money across 170 countries and thousands of corridors is very applicable to other very large markets.

On the horizontal part of the grid, we’re focusing on what customers need to do: send money, borrow money, spend money and save money – making up our 4×4 framework.

We’re launching a loan product for the core business – send now, pay later – which is a short-term, small loan for specific liquidity crunches that our customers get into and we’ve attached it to a card. So we’re trying to combine a few ideas: a card that’s got a membership to it where you can borrow money.

Then you’ve got the spend, where we’re starting to issue debit cards across all our categories. We’re early on in the development of our save proposition, where we have a wallet. Over time, we want more people to leave money in their Remitly account and we can give them all kinds of loyalty points and interest.

Remitly reports consistent customer and volume growth

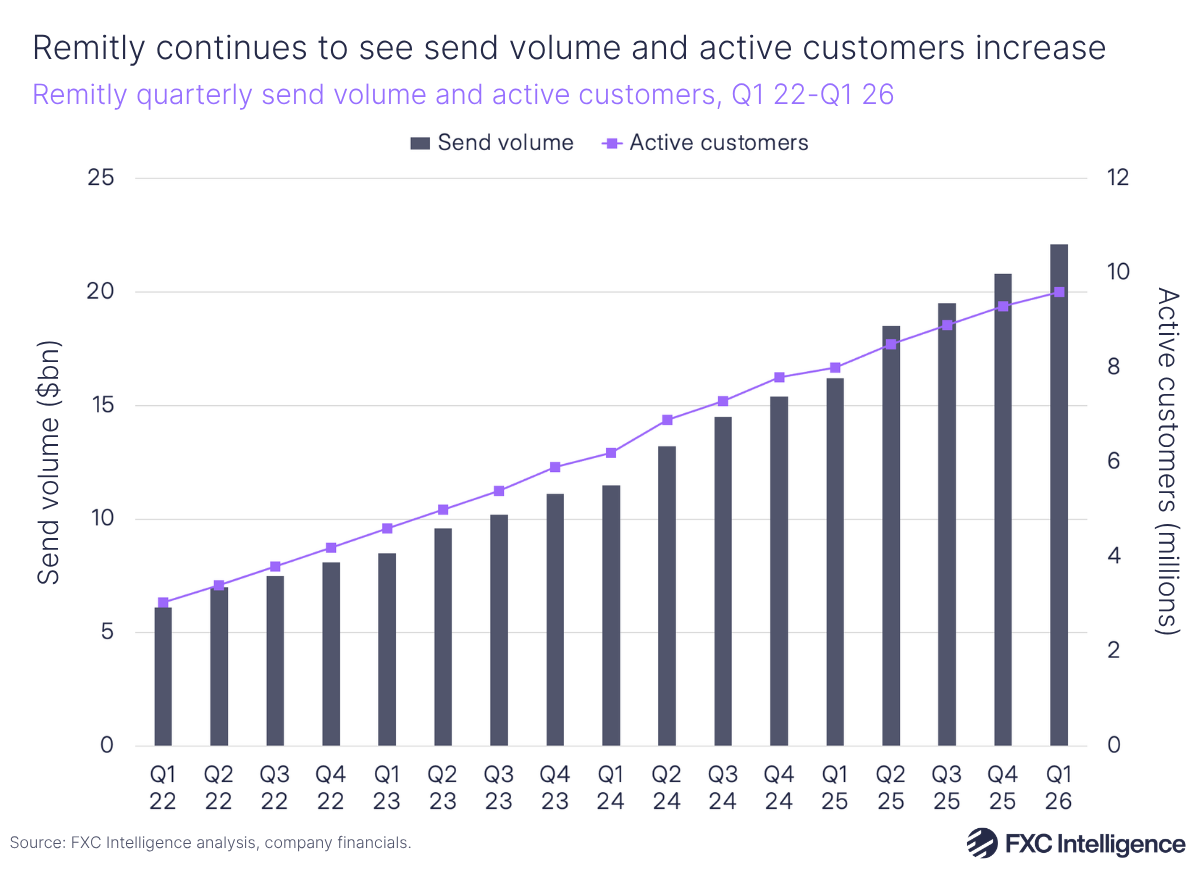

Remitly also reported record totals for its number of active customers and send volume in Q1 2026. The company saw its active customers reach 9.6 million, up 20% YoY, while send volume increased 37% to reach $22.1bn.

This resulted in Remitly’s average send volume per active customer climbing 14% YoY to reach $2,302 – another record total for the company. Meanwhile, average revenue per customer rose 4% to $47.17.

Remitly weighs up stablecoin and AI capabilities

Daniel Webber:

What are Remitly’s plans regarding stablecoins?

Sebastian Gunningham:

Remitly delivers money in under a minute at a very low price today. So if you compare stablecoins to Remitly’s existing capabilities, plus or minus a cent, we’re already there. There are a few corridors where using crypto infrastructure could help to move money, but in most cases stablecoins are not a great needle mover for us.

The piece where that does change is that there are many customers around the world who want to hold money in dollars. There is demand for the ability to hold USDC on the receiving side, such as in Argentina. We currently issue a credit card there through a partnership with Bridge, which enables consumers to spend that money, where it automatically converts from USDC to pesos. Currently, as far as I can see, the sending customer has little to no interest in stablecoins because they already live with stable currencies in the US, Canada, UK and Europe.

We are also exploring some treasury use cases for some corridors. For example, for US to Mexico, we’re testing holding money in USDC versus local currency. There is likely value down the road, but for our customer base it is still early days.

Daniel Webber:

What impact is AI and agentic having across the company?

Sebastian Gunningham:

With AI, I’ve got a math background and I built some of the ML [machine learning] teams at Amazon in the early days, so this is within my wheelhouse. I’d say that the killer application of AI right now is obviously to do with software building and product building.

For a growth company like Remitly, AI enables us to build a lot more products faster, while also improving efficiency elsewhere. We have also launched in ChatGPT and are interested to see how the customer wants to interact through chat, but ultimately, I’m bringing in all of the skills I can to combine the silos of the past into one very efficient process.

Remitly sees efficiency gains bolster revenue

Remitly saw a 28% increase in revenue less transaction expenses to $307.9m in Q1, which outpaced the 19% YoY growth in transaction expenses to $144.9m. This has come as the company has continued to improve efficiencies, partly driven by implementing AI into its processes.

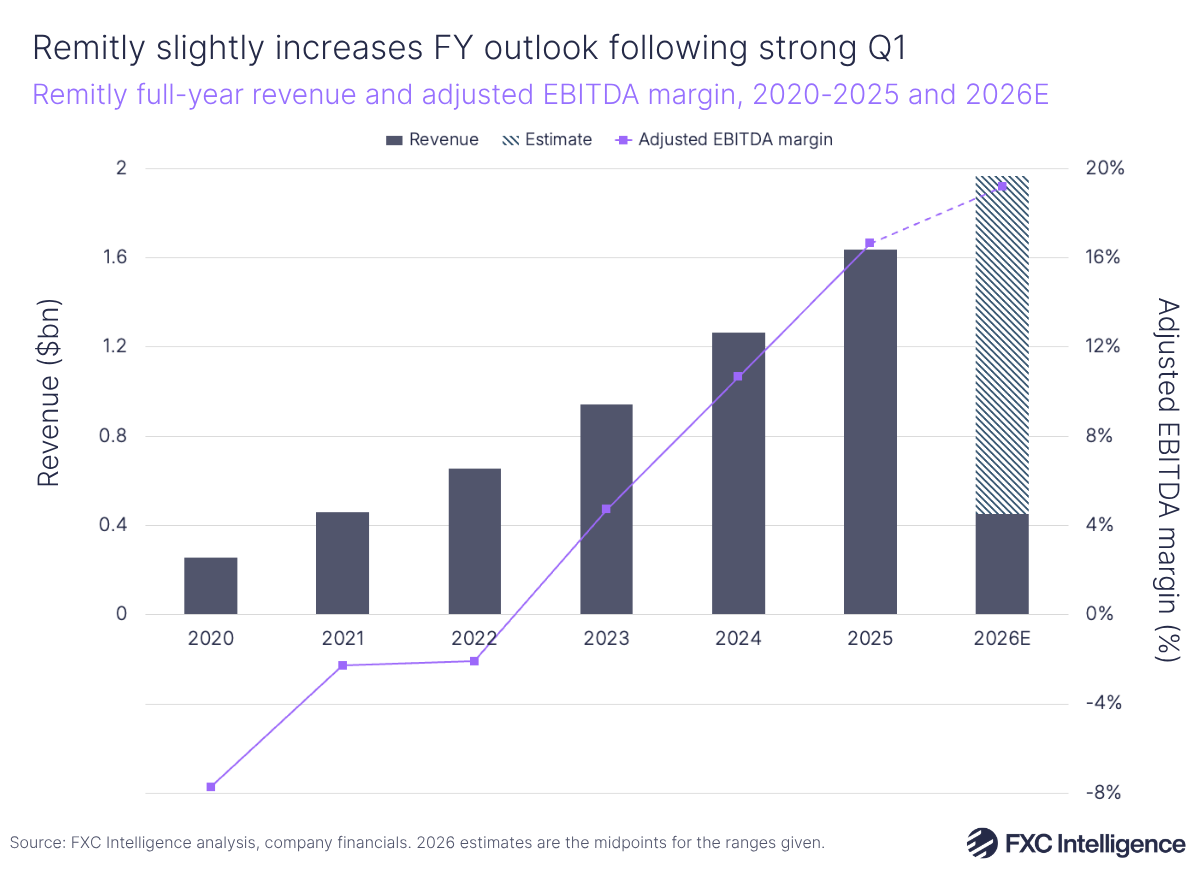

Following strong results in Q1, Remitly has slightly increased its revenue projection for FY 2026 to between $1.96bn and $1.975bn, up from the $1.94bn-1.96bn the company outlined during its Q4 25 earnings call. It has also said that it expects its adjusted EBITDA to be in the range of $370m to $385m, up from the $340m-360m mentioned in its previous earnings call.

US remittance tax drives growth in Q1

Daniel Webber:

What impact has the 1% tax on cash remittances in the US had on Remitly?

Sebastian Gunningham:

This 1% tax was a tailwind for us that we didn’t manufacture. We had very good growth in customers and saw 37% growth in send volume, which slightly outpaced revenue growth. We’re attaching some of this growth to those tailwinds.

To make the most of this, we launched our ‘skip the line’ marketing campaign aiming to convert offline senders by advertising the cost advantages and convenience of digital money transfers, which worked very well.

Daniel Webber:

Is there anything else you would like to cover?

Sebastian Gunningham:

We still have a lot of growth in Europe and Australia, we have launched in Japan and have plans to launch in Brazil. So overall, our core business seems to be very strong. We continue to believe that the upside is very large because these are very large markets. So we’re working towards capturing some of the business market and our capacity to invest has been increased by some of those AI tailwinds.

Matt built a great company and I’m standing on the shoulders of everything they built. Now, I’m seeing how much we can take this into the future.

Daniel Webber:

Sebastian, thank you.

Sebastian Gunningham:

Thank you.