Singapore has grown to become one of the biggest cities in the world for cross-border payments companies, but who are its key players? We look at MPI licence holders in Singapore to build a broad picture of the market.

Singapore has long been important for the cross-border payments industry, and is more so than ever in 2024.

A highly skilled international workforce, long-established support for innovation and a well-developed reputation as a global finance hub have combined to provide a strong market for sending both consumer remittances and cross-border B2B payments, as well as providing a space for companies seeking to disrupt the payments landscape to flourish.

Add to this its critical position to serve the rapidly emerging wider Southeast Asian region, and the nation is rapidly becoming one of the most important global cities for cross-border payments, both as a source of new companies and as the headquarters for established and rising players in the industry.

With a combination of a strong domestic and regional cross-border payments market, as well as strong infrastructure, skills and a robust regulatory environment, Singapore is not only producing growing numbers of leaders, but is also attracting many international cross-border payments players to its shores.

But who is operating in the market, and what can it tell us about the trends within the region? This report looks at the companies with Major Payment Institution (MPI) licences from the Monetary Authority of Singapore – an essential requirement to operate in the country – to get a picture of the market both as a whole and within key segments.

Singapore’s MPI and SPI licence holders

All payments players in Singapore are required to obtain a licence from the Monetary Authority of Singapore in order to operate. For most, this takes the form of a MPI licence, although a small number of companies instead obtain a Standard Payment Institution (SPI) licence.

Both MPI and SPI licences require companies to be incorporated in Singapore or, in the case of foreign corporations, have a branch in Singapore. They also require companies to have a minimum base capital – S$100,000 (c.$75,0000) for SPI licence holders or S$250,000 (c.$186,000) for MPI licence holders – and include an executive director who is a Singapore citizen or permanent resident. This last requirement can be waived if the company instead has a Singapore citizen/permanent resident as a director and an executive director who has a Singapore employment pass.

SPI licences are permitted if a company meets the thresholds of S$3m (c.$2.2m) monthly payment transactions for non e-money issuance/money changing; S$6m (c.$4.5m) monthly transactions for two or more such payment services; and S$5m (c.$3.7m) daily outstanding e-money. For MPI licences, companies can operate multiple payment services without facing those same threshold limits.

For both, licence holders apply for specific sub-licences that allow them to provide specific types of payment services. These sub-licences are:

- Cross-border Money Transfer Service

- Account Issuance Service

- Domestic Money Transfer Service

- Digital Payment Token Service

- E-money Issuance Service

- Money-changing Service

- Merchant Acquisition Service

While most companies have multiple such licences, very few have all seven.

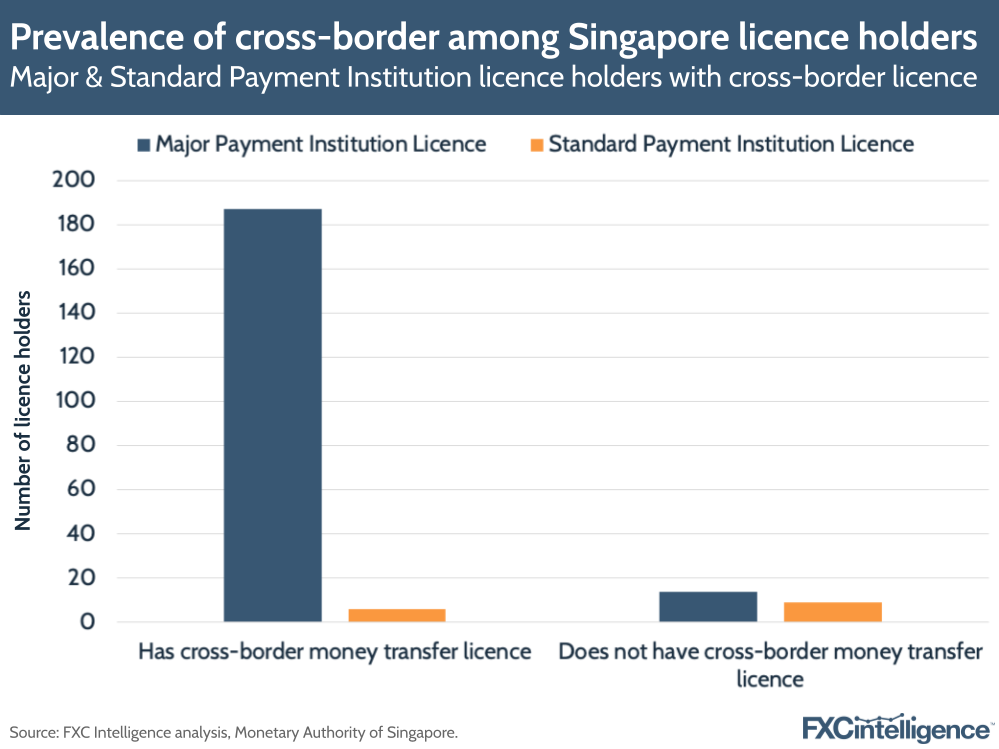

Overall, the more restrictive SPI is considerably less popular than the MPI. At the time of writing this report, the Monetary Authority of Singapore currently lists 15 companies with SPI licences and 207 with MPI licences, although only 201 of these appear to be active.

The SPI is also more popular with smaller, domestic-only companies. While 93% of MPI licence holders have a cross-border money transfer licence, just 40% of SPI licence holders do.

However, there are a small number of larger players who have opted for an SPI licence rather than an MPI licence. As shown below, among active companies with some form of Singaporean cross-border money transfer licence who have outbound customers in multiple countries and more than 50 employees, while the majority are MPI holders, three are SPI holders, including remittances major MoneyGram.

How big is the market opportunity in Singapore and other countries in Southeast Asia?

Business focus of cross-border payments companies in Singapore

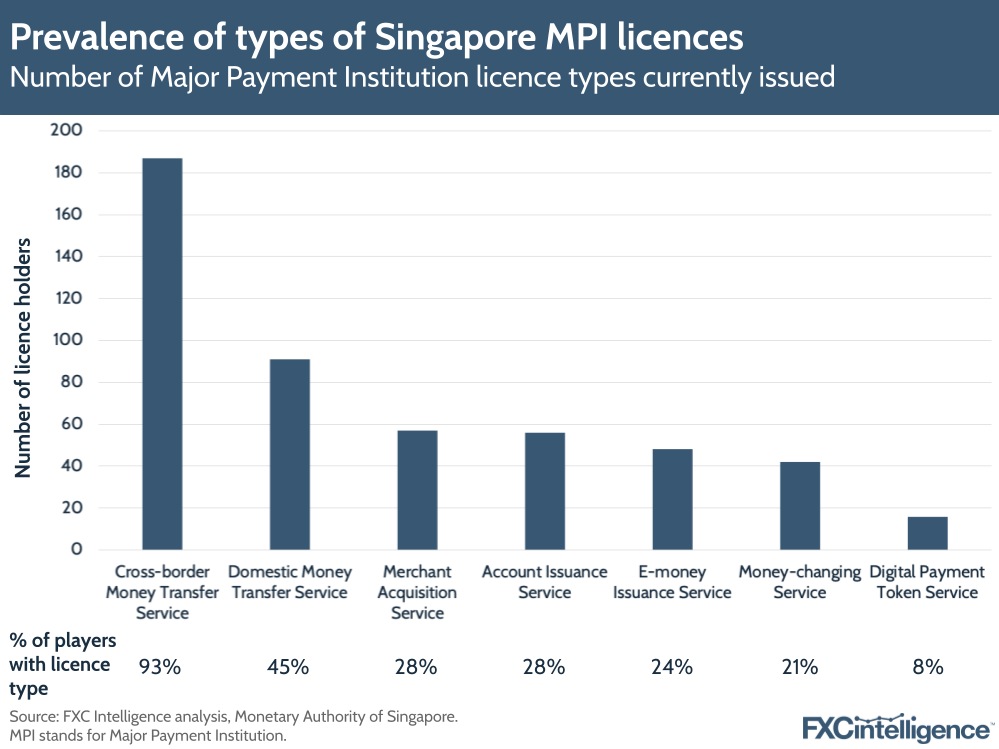

Looking at active companies with MPI licences, while more than 180 of the 201 analysed have a cross-border money transfer service licence, other additional licences were considerably less prevalent.

Slightly less than half also hold a domestic money transfer licence, while just under a third hold merchant acquisition service or account issuance licences. Less than a quarter hold e-money issuance service or money-changing service licences. Digital payment token service licences, which are required for cryptocurrency-related activities, are the least common type held by MPI licence holders.

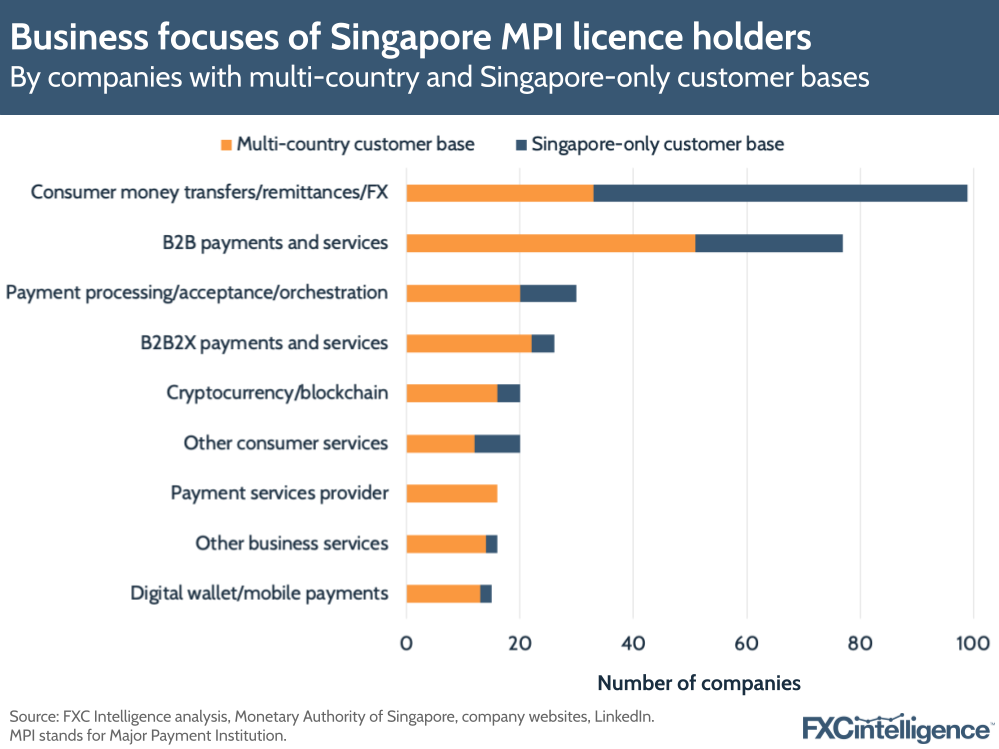

This variation reflects the significant diversity of products and services offered by the cross-border payments industry operating in Singapore, and is also reflected in the range of business focuses of the 201 companies we analysed. While those offering consumer money transfers and related services were most common, followed by B2B payments and payments processing, there were also a wide range of other companies operating in the space.

Companies providing B2B2X services for example, who are typically providers of payment infrastructure, are by their nature less common than players serving consumers or smaller businesses; however, there are a significant number operating in Singapore, the vast majority of which cater to customers in multiple countries.

Key demographics of MPI licence holders in Singapore

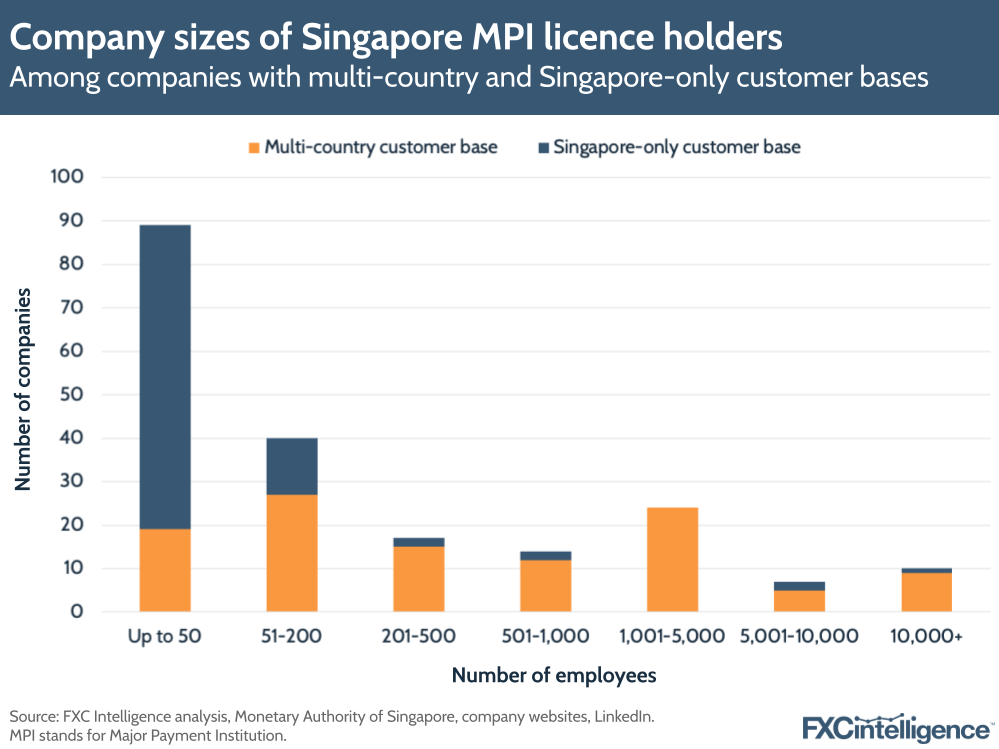

When it comes to the typical size of MPI licence holders in Singapore, and therefore the companies offering cross-border payments in the country, there is a clear distinction between those serving only Singapore-based customers and those operating internationally.

Domestic-only companies are disproportionately small and micro-businesses, with 78% employing under 50 people, compared to just 17% of multi-country players being this size. By contrast, around just 8% of domestic-only businesses had more than 200 employees, with only 3% having more than 5,000. In these cases, these are typically large Singaporean companies that provide multiple services to significant numbers of the country’s population, including cross-border payments.

However, for international-serving companies, there is a broad range of company sizes, with all but one segment (5,001-10,000) representing at least 5% of the total. Companies with 51-200 employees are the most common, which may indicate scale-up companies – a reflection of the long-standing focus on providing a supportive environment for startups to develop that Singapore has cultivated.

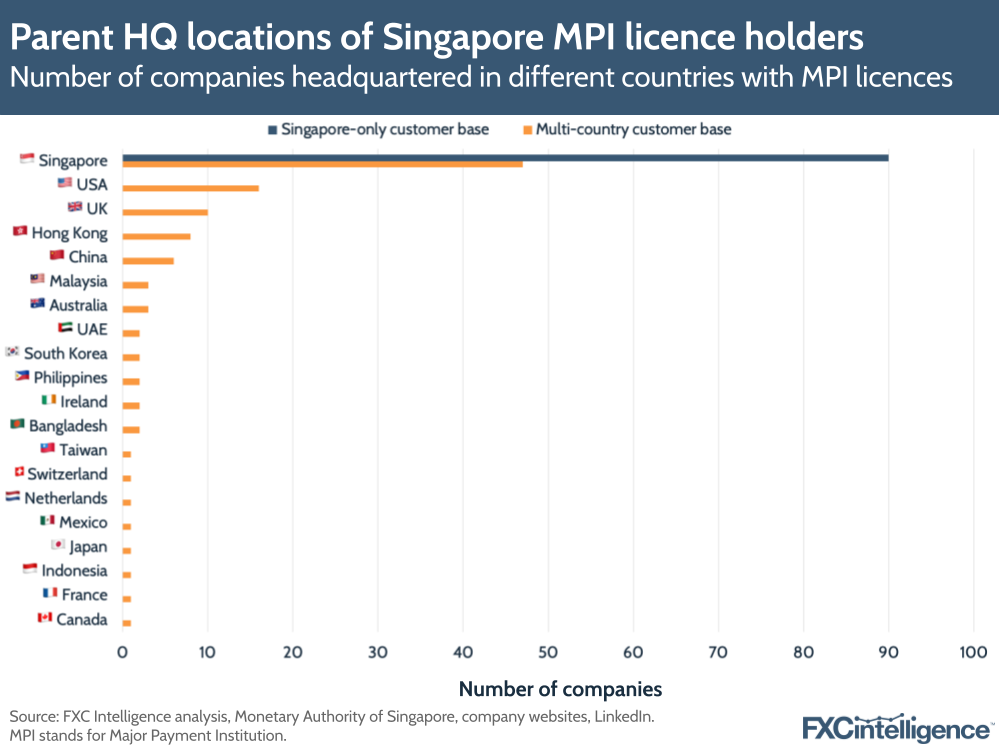

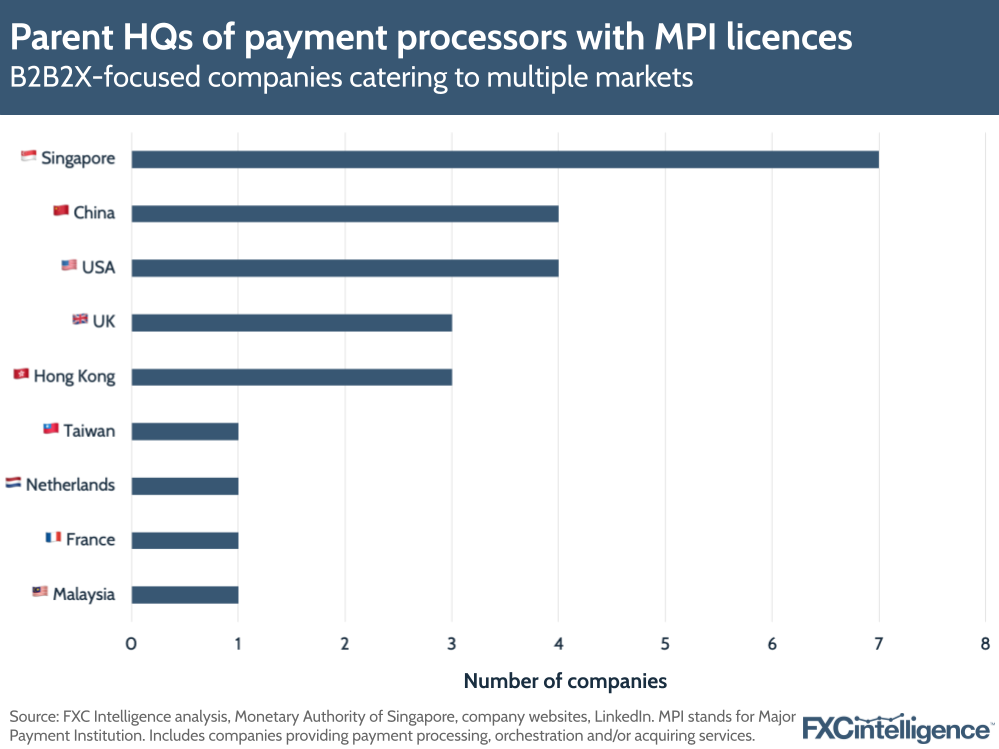

When it comes to the headquarters location of the MPI holders’ parent companies, while Singapore is in the lead, there is a wide variation in countries, reflecting the broad international appeal of the country as a cross-border payments market.

Long-established payments hubs lead, in the form of the US and the UK, but there is also strong presence from international companies headquartered throughout Southeast and East Asia, as well as the wider Asia-Pacific region, Middle East and Europe and North America.

In some cases, such as Bangladesh and the UAE, these reflect the strength of payment flows between these corridors, in particular as a result of large numbers of migrants.

What is currently lacking, however, is a notable presence from many companies headquartered in the emerging markets of Latin America and Africa, the one exception being a single company headquartered in Mexico. With players in these regions seeing significant and rapid growth, we would expect this to change in the coming years.

Consumer remittance companies operating in Singapore

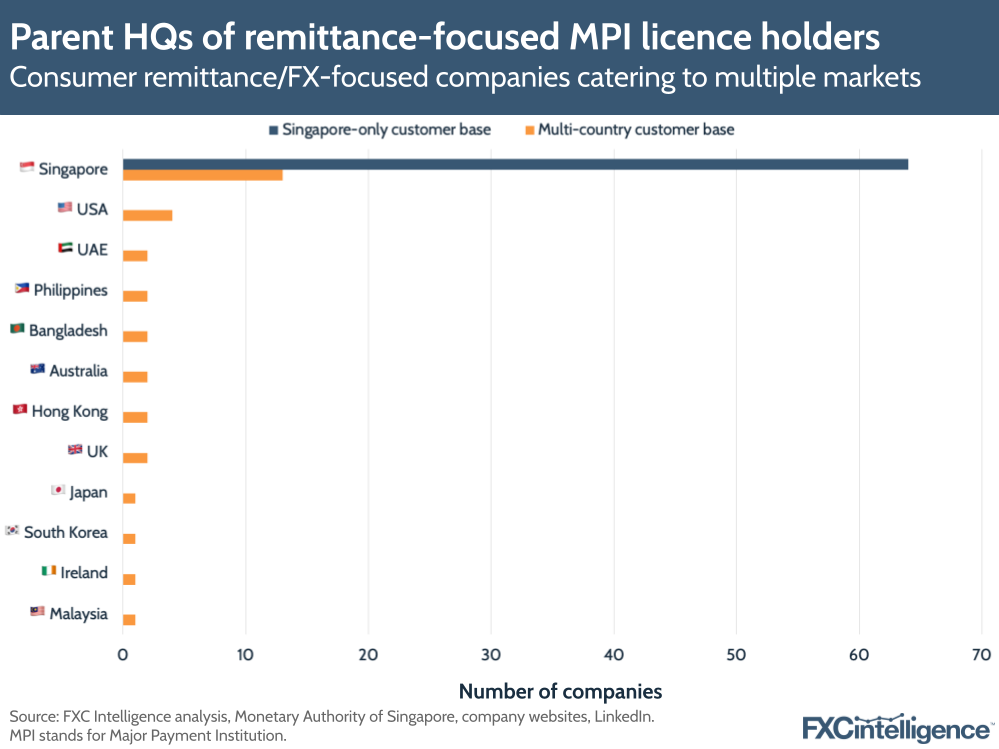

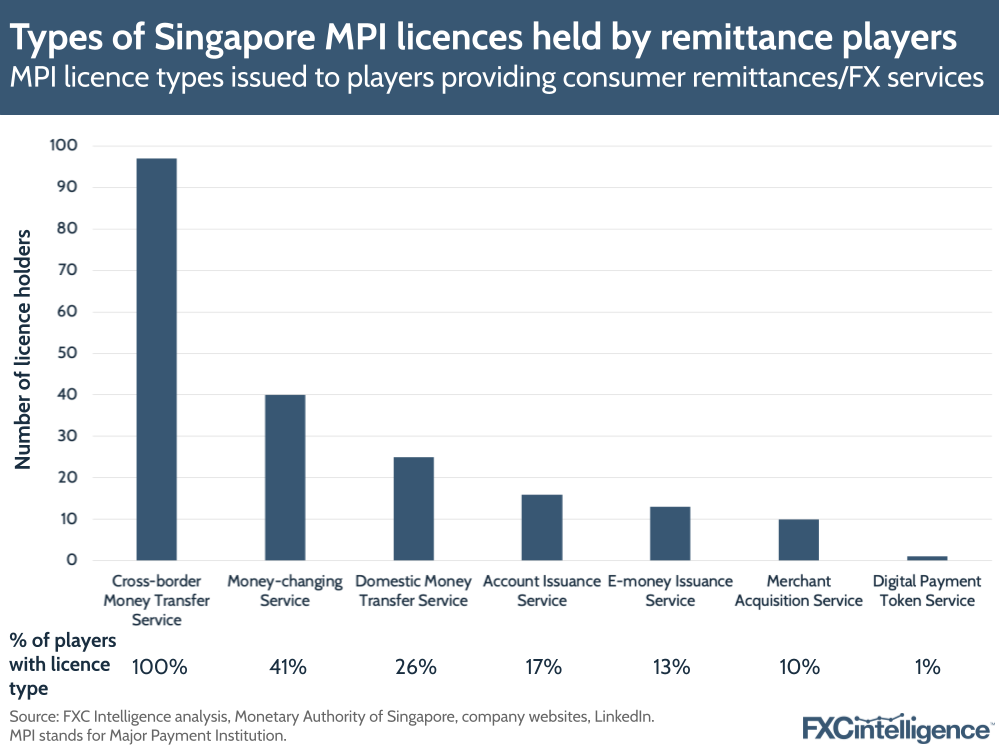

Looking specifically at MPI licence holders providing consumer remittances, money transfers or foreign exchange services provides a view into this segment of the market, which is considerably more domestic than the rest of Singapore’s cross-border payments industry.

Within this sector, 66% of companies only serve outbound customers in Singapore, with the rest largely being headquartered in key remittance corridors with the country.

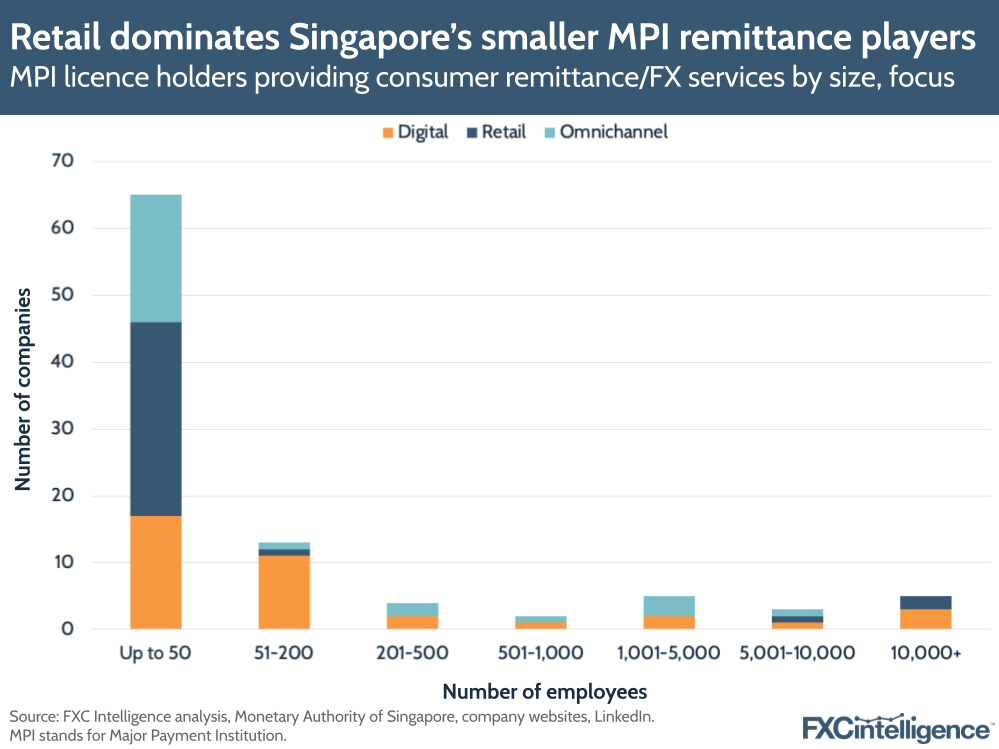

Many of these players are small companies with single retail units, often without their own dedicated websites, which is reflected in the fact that most companies have under 50 employees. However, providers of all sizes cater to the market, with some serving the traditional migrant remittance market while others focus on the expat money transfers space.

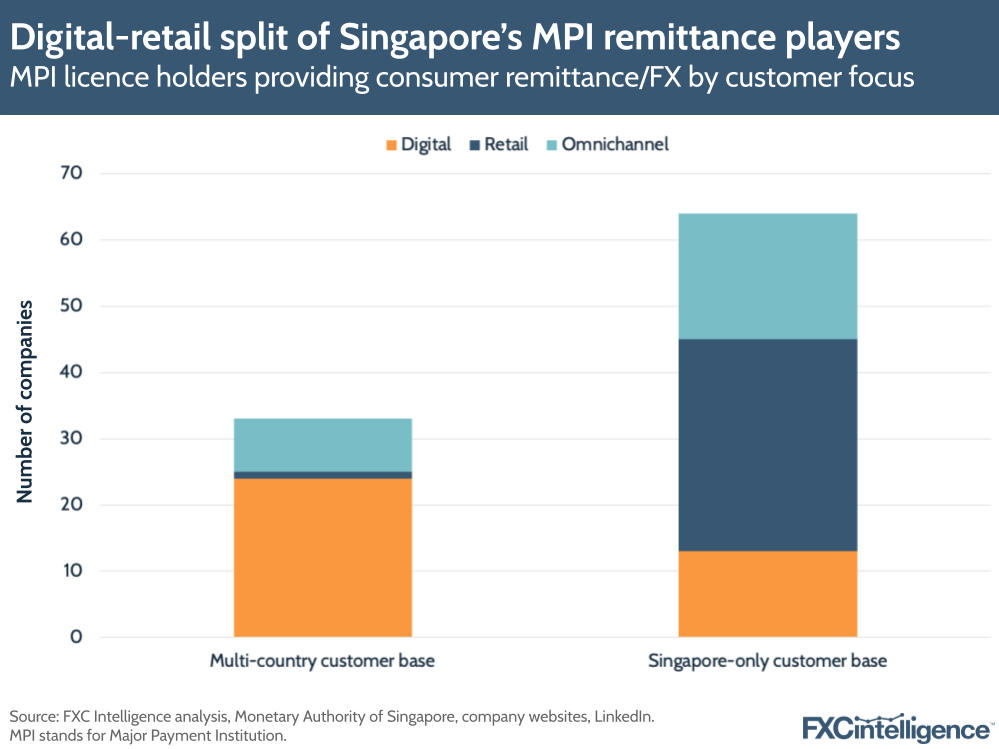

The split of companies that provide digital-only, retail only or omnichannel services also reflects this. International companies are far more likely to provide digital-only services, with the remaining minority mostly offering omnichannel services. However, retail is the largest segment for domestic-only players, followed by omnichannel, with digital-only offerings in third.

Most retail-only small players generally only hold two MPI licences: a cross-border money transfer service licence and a money changing service licence, allowing them to offer both remittances and currency exchange services to walk-in customers.

However, the broader range of companies means that all types of licences are held by some companies within the sector. This generally reflects companies that offer services in addition to remittances or money transfers. Here the most common secondary service is B2B payments, with 31% of players in this space in Singapore also providing cross-border payment services to businesses.

How are Singapore’s remittance players competing on price?

B2B payments companies operating in Singapore

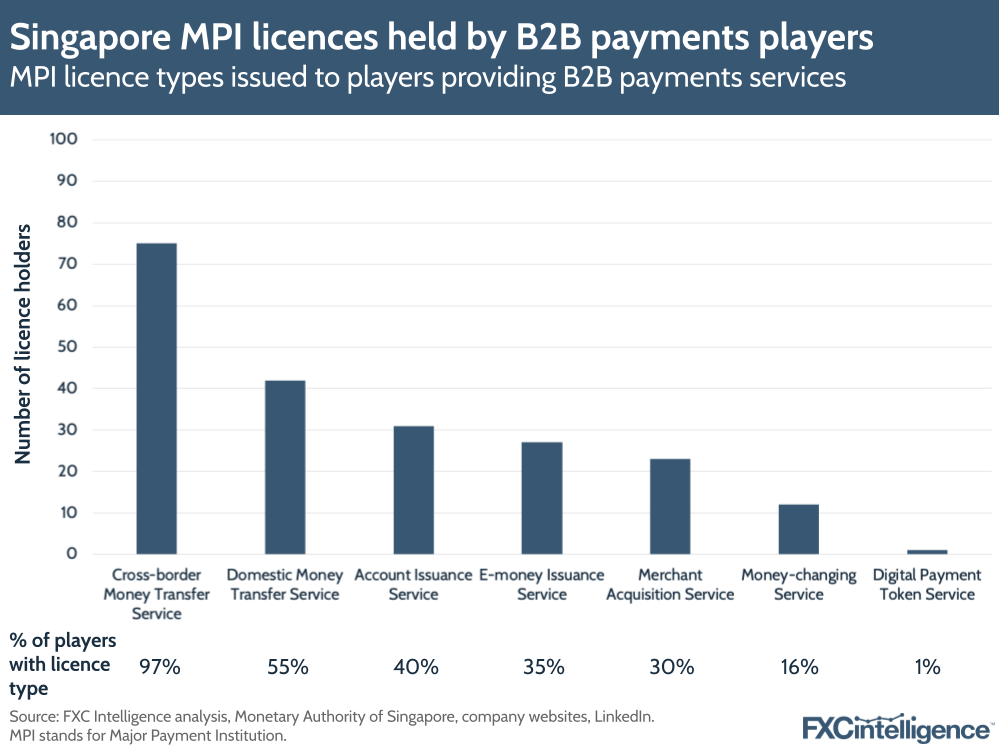

Meanwhile, among Singapore’s B2B payments sector, its second largest part of the payments industry, while cross-border money transfer service licences are held by 97% of companies, over half also have domestic money transfers licences.

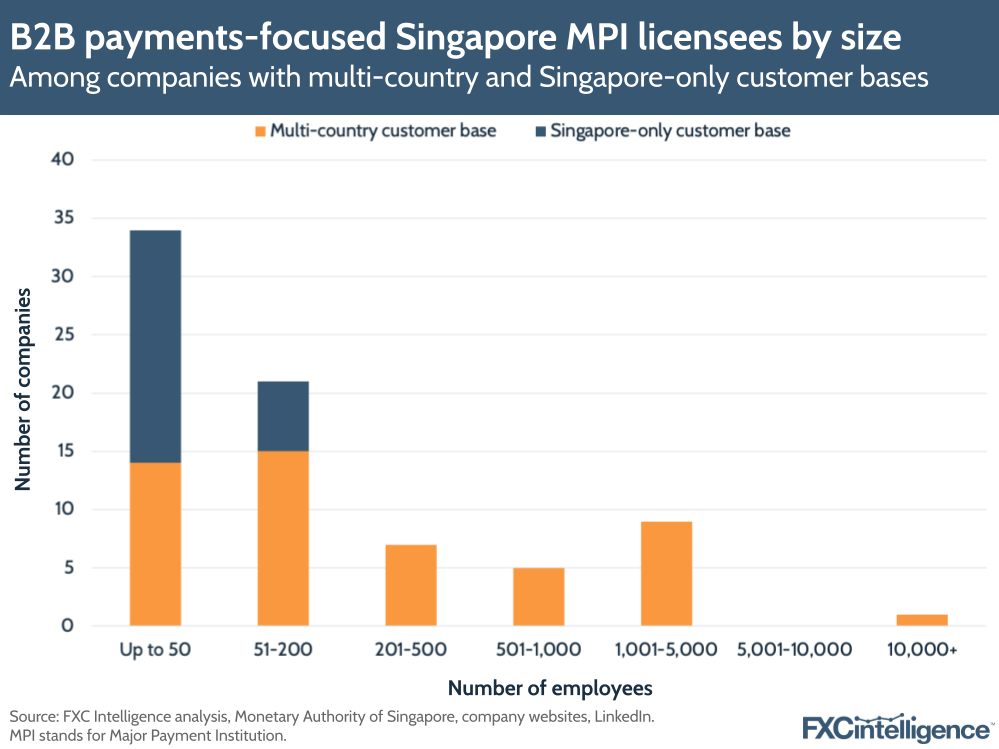

Here, there is again a division between domestic and international companies when it comes to size. All of Singapore’s B2B payments companies serving only customers in the country have less than 200 employees, with most employing less than 50 people. Meanwhile, international companies providing B2B cross-border payments in the country are a wide range of sizes, although 80% of the market is made up of companies with less than 1,000 employees.

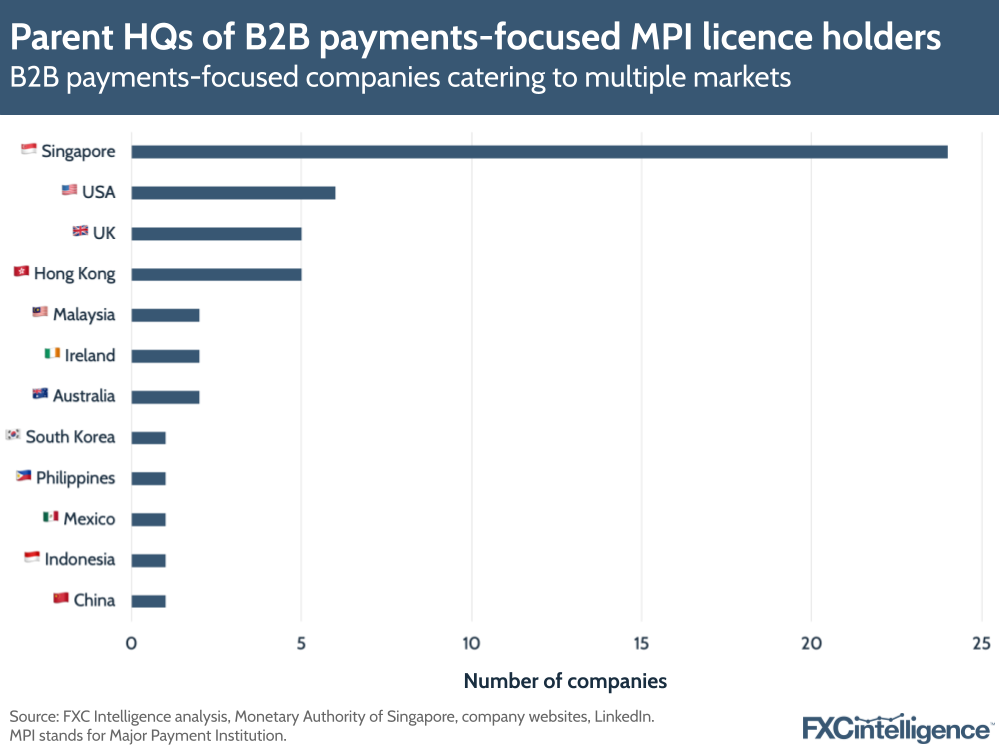

Among those who are serving customers in multiple countries, the US and UK are again the most popular locations, with the UK being more prominent in this sector due to its strong presence in B2B payments in particular. However, beyond this, B2B is largely represented by countries with strong developed economies and significant trading interests with Singapore.

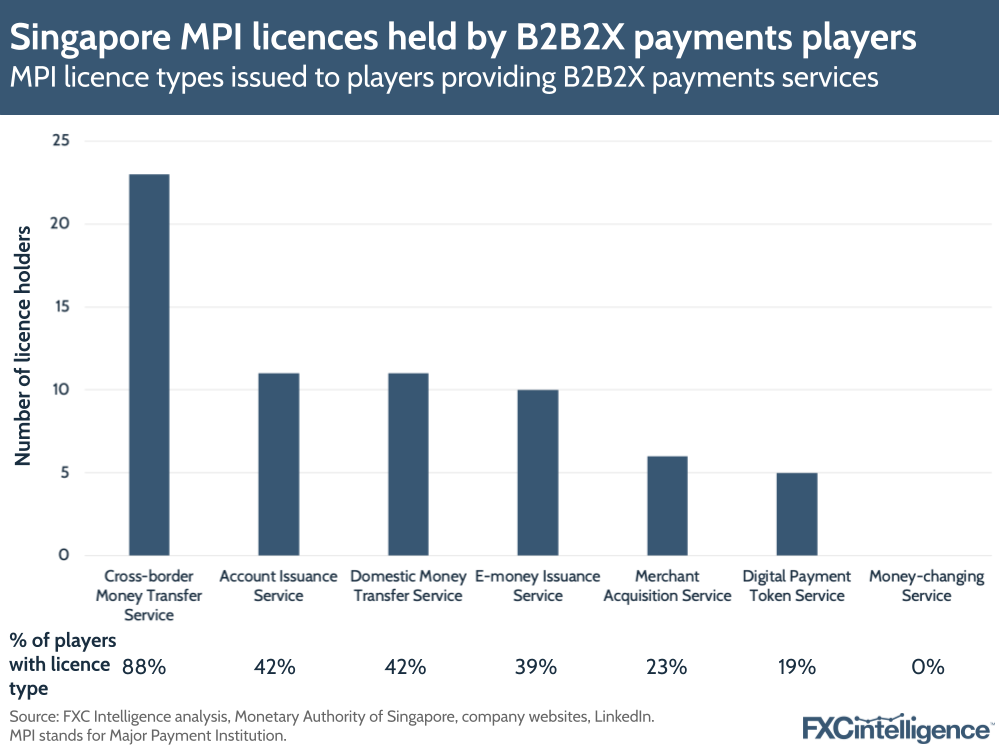

B2B2X payments companies operating in Singapore

Meanwhile, B2B2X players also represent a strong market in Singapore. B2B2X typically represents infrastructure providers and others providing domestic or cross-border payment services to other businesses to sell on to their own customers. It is a category that has seen numerous newer players emerge over the past decade or so, as companies either look to disrupt traditional payment networks or diversify their revenue streams by offering their own networks to other players via white label services or similar.

Here the precise nature of the service varies the licences required significantly, with all but money-changing presenting potentially strong utility.

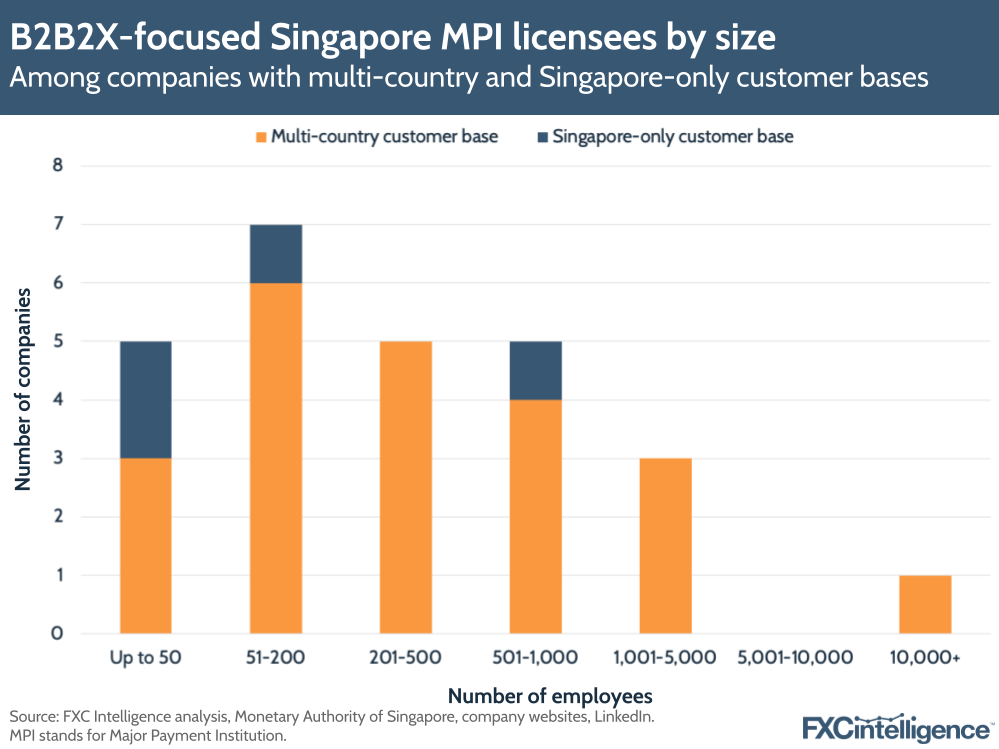

While there are a minor number of smaller players in the B2B2X space, the average company size in this sector leans larger than in a sector such as consumer remittances, as customers are often large enterprises or other larger corporations.

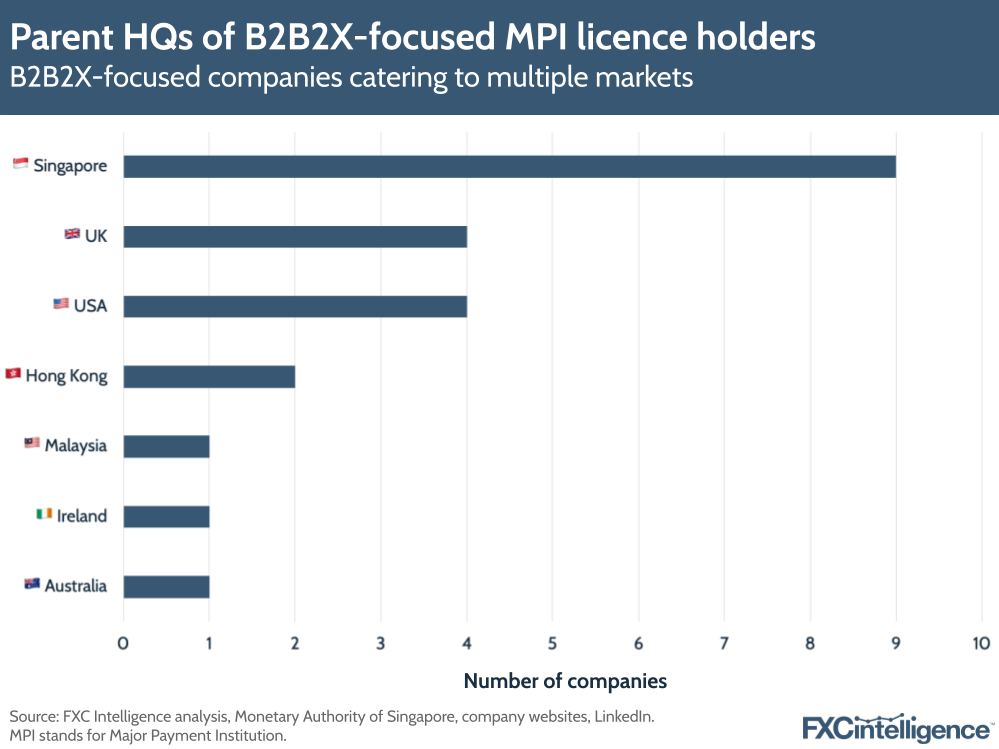

Singapore-headquartered companies represent a lower percentage of B2B2X players serving multiple markets than for B2B payments or consumer remittances, however there are a significant number, with Nium among those headquartered in the country.

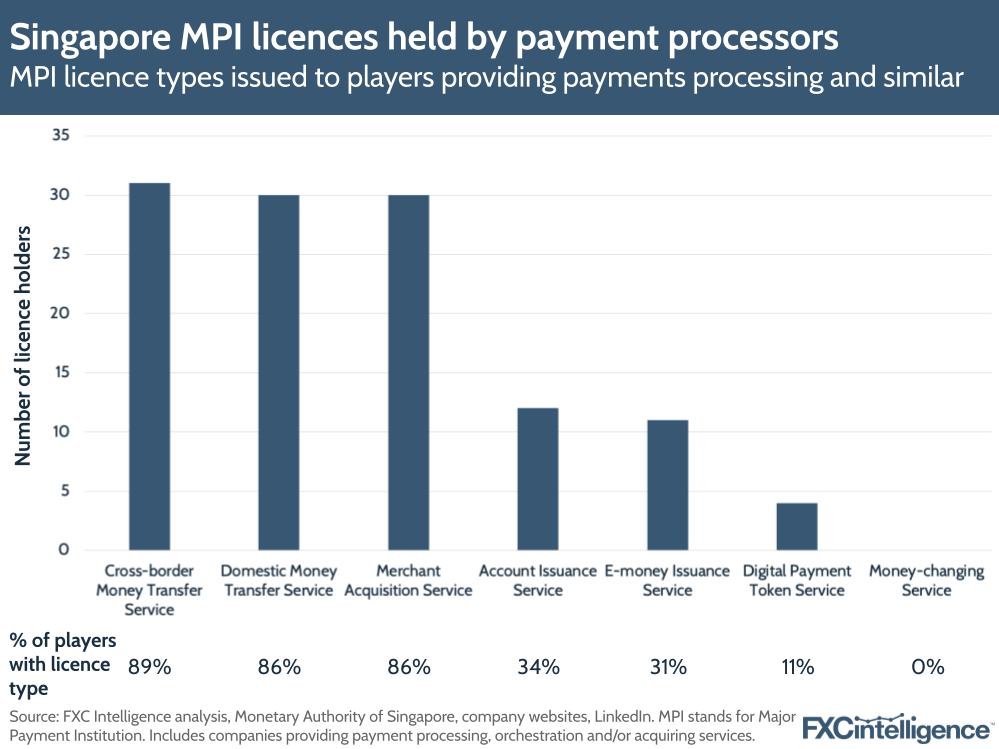

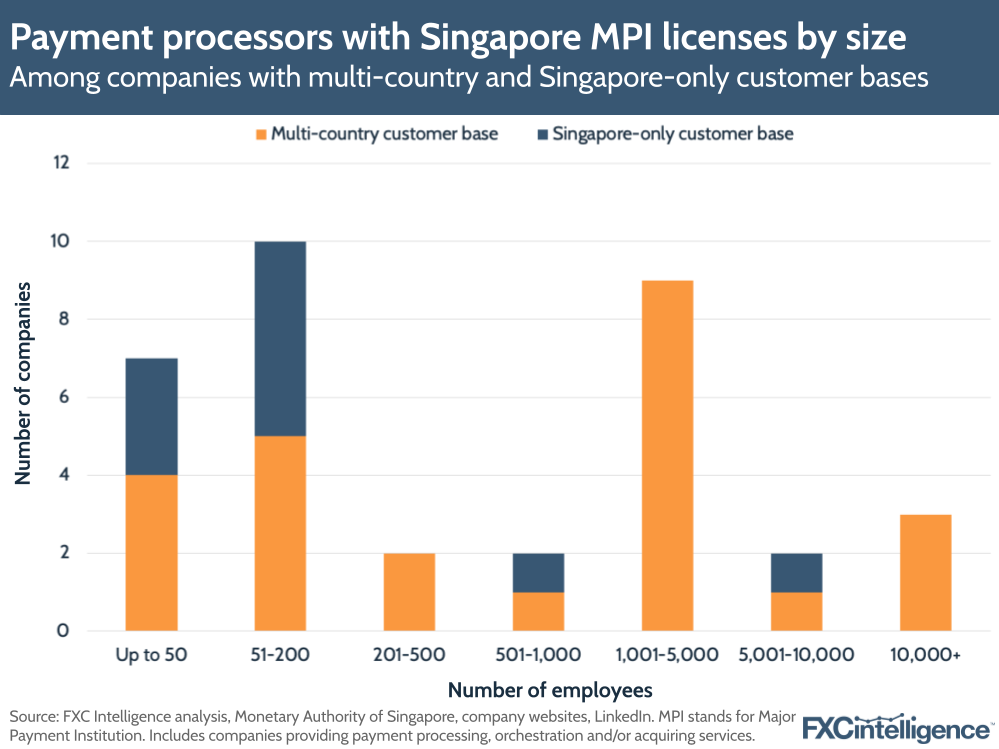

Payments processors in Singapore

For companies offering payments processing, acceptance or orchestration services meanwhile, the most common combination of licences is cross-border money transfer services, domestic money transfer services and merchant acquisition services, all of which are held by over 85% of companies in the sector.

Here, domestic-only companies again lean smaller, although there are a few larger companies only catering to the Singapore market, largely providing solutions related to widely used services within the country. There are also a large number of bigger players overall than in other cross-border payment sectors.

Among those players serving multiple countries, the US and UK remain in leading positions, but are joined by companies headquartered in China and Hong Kong, reflecting the significant difference in payment types preferred in retail settings in the East compared to the West.

Potential for future developments

The Singaporean payments landscape is dominated by cross-border payments, and while there are large numbers of small domestic-only players, among those companies catering to markets internationally, there is significant variation in the business profiles and market focuses of players.

As a market, Singapore produces large numbers of home-grown cross-border payments players and is also attracting large numbers of players from abroad, particularly from highly developed markets and those with strong flows to and from the country.

However, with the wider Southeast Asian market developing rapidly, and more and more companies from the West now looking for a foothold in the region, Singapore’s presence and impact within the global payments landscape is only set to grow. Expect broader profiles of companies, as well as an increased shift to international players, over the next few years, alongside the maturing and development of the country’s own payments players.