With our Buyer’s Guide: Stablecoin Payment Infrastructure product now available (learn more about purchasing a subscription or read the executive summary), we’re continuing our series on the technical elements of stablecoin payments infrastructure. And following last week’s focus on the Travel Rule, this week we are turning our attention to Virtual Asset Service Providers (VASP) and their licences.

VASPs are, in essence, entities that provide services relating to stablecoins or other digital assets on behalf of clients, including activities relating to their custody, exchange, payment or receipt. As a result, any company that provides locally handled, stablecoin-based cross-border payments is likely to be a VASP, and therefore will need to be licensed appropriately.

Defined under recommendations set out by the Financial Authority Task Force (FATF), VASPs are typically subject to requirements similar to those that apply to money transmitters. They generally need to be licensed or registered in every jurisdiction where they onboard customers, are subject to the Travel Rule to support AML and fraud-prevention activities and need to follow appropriate procedures around governance, reporting and asset safeguarding. This not only means that, in many jurisdictions, any companies that cross-border payments providers use for stablecoin-based money movement need to be registered as VASPs, but that the payments providers may also need to be themselves.

While the process varies, VASP licences typically require an organisation to have a legal local entity, and in some cases local capital and data residency. They also need to provide extensive compliance and governance documentation and demonstration of technical solutions such as custody architecture and how they are solving for the Travel Rule. As with other licences, the time to approval varies significantly by market, with some markets taking just a few months while others take well over a year.

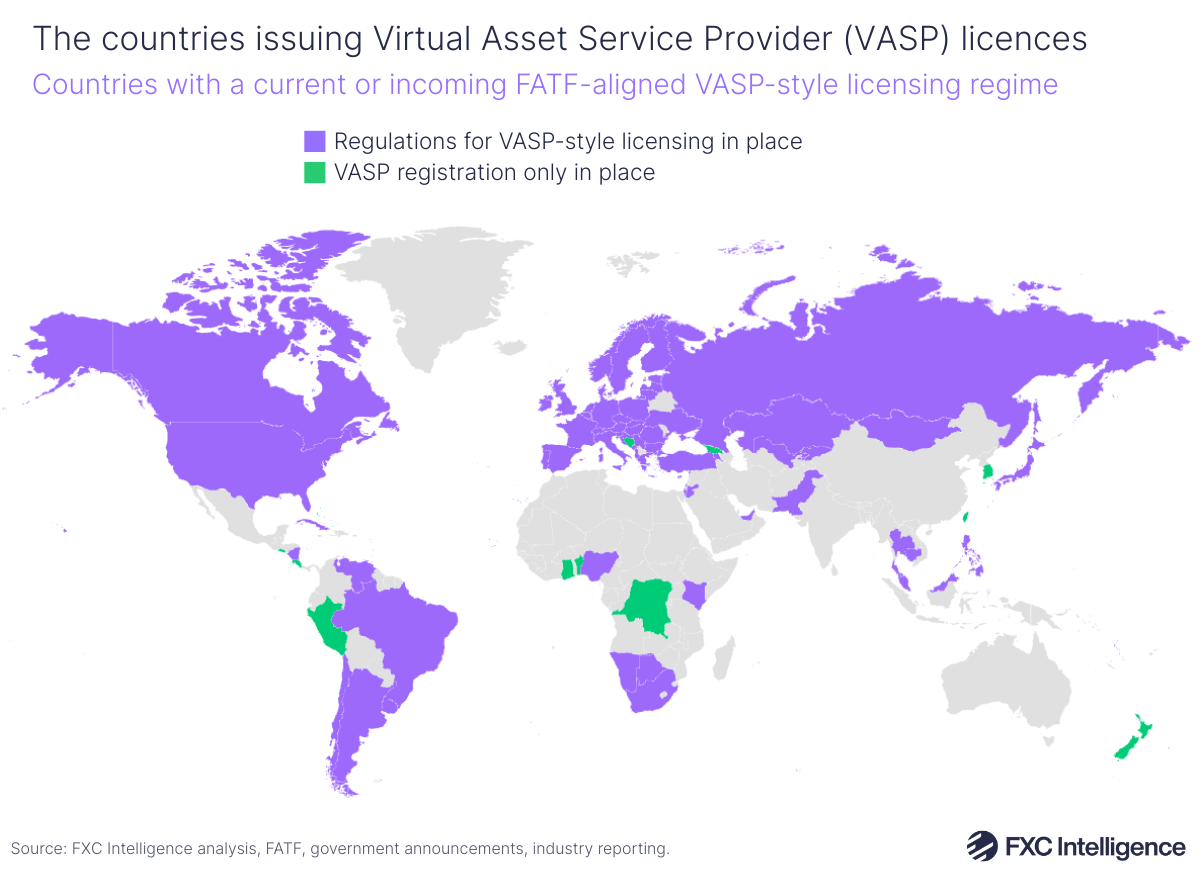

Not all VASP-type licences are referred to by this name, or follow the same precise format. For example, in the EU companies apply for a Crypto Asset Service Provider (CASP) licence under the region’s MiCA legislation, while in the US the FinCen Money Service Business (MSB) registration requirements and state money transmitter licences are functionally equivalent. In a significant minority of cases, countries have put in place legislation but have not yet issued any VASP licences, with a fair number of markets passing laws within the past 12 months.

Furthermore, not every market currently has a VASP licensing regime. Some simply require registration for AML purposes and there are many countries where stablecoins are legal in some form for payments, but where full FATF licensing and legislation recommendations are not yet in place or where stablecoin payments exist in an unregulated grey area.

However, the present reality is that many major players operate in some form in the majority of countries worldwide but hold only a small number of VASP licences – an approach that is arguably the current industry standard. This is achieved by structuring their product so that they are not a local VASP in most of the markets they serve, which they typically do by operating either as a pure provider of technology or infrastructure or as an offshore VASP that provides the non-local part of a given payment flow.

This is often realised by the provider not holding custody of the user’s funds locally, with providers prioritising gaining licences in their key send markets, as well as operating in markets where local VASP licences are not yet required. In some cases, companies also split their stack into regulated and unregulated components and deploy them strategically around the world depending on their licences. Others, primarily infrastructure-only providers, make their end customers the VASPs instead by requiring them to handle AML requirements and to acquire any local licences.

For companies looking to add stablecoin cross-border payments, VASP status can therefore be one of a number of reasons to use multiple infrastructure providers with different geographical expertise, rather than a single global provider. Next week will be our final newsletter of the year, where we’ll highlight what we’ve covered in this series so far. We’ll also be continuing the series in the new year as we mark the launch of FXC Buyer’s Guide: Stablecoin Payments Infrastructure. Learn how it can help you select the right partners and navigate the market.