Big tech is making a big play into finance with plenty of recent news coverage (including in this week’s Economist featuring FXC Intelligence). We break down how this will affect the cross-border payments industry. Plus, insights from our pricing data in the UAE and after MoneyGram’s roller-coaster week, we take a look at the most volatile payments stocks.

Big tech’s clear approach

The news has been recently filled with big tech announcing products and strategies aimed at the financial services space. Some directly at cross-border payments, some indirectly. There’s been a lot of fear-mongering going on too – we try to get to the bottom of what’s realistic and what’s not.

The big picture

Big tech pushing into finance is not new but a renewed effort is certainly at play. Why?

- Big tech does not want to be big finance (the banks) and it doesn’t want to be valued like big finance. Big finance is too highly regulated, requires substantial balance sheets and infrastructure. Moreover, the competition authorities and regulators are simply not going to let it happen.

- Big tech does want to understand big finance and wants the data. Much of big tech still does not know enough about the day to day financial habits of consumers. Financial services and payments in particular are a very sticky way to engage with users.

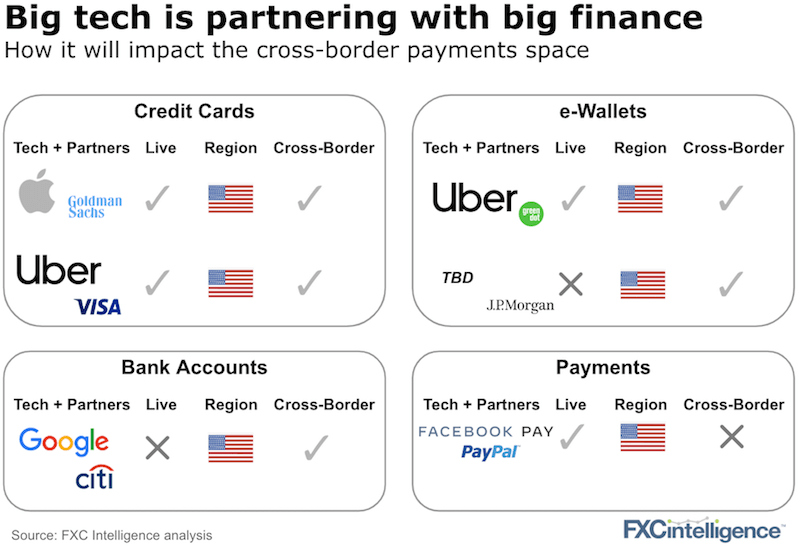

- Most of the companies and products in our graphic above can facilitate cross-border payments. Others like Facebook Pay could be expected to expand to cross-border at some point. So don’t think cross-border payments is out of scope.

Why big tech is pushing into finance

There are many reasons – the biggest as we see them:

- For data: Bank accounts (Google). But realistically, everyone wants the data.

- Launch new products and open new revenue lines: Credit cards (Apple & Uber).

- Engage with new customers: e-wallets (Uber), Libra (Facebook).

- Keep existing customers in the ecosystem: Google Pay and Facebook Pay.

Who could be most at risk?

- The new digital banks. Alone, these new players have been taking share from the traditional banks but big tech partnering with the big banks could give big finance a new boost.

- At any point, the tech companies could decide to grab market share by offering any of the services above for free (their upside is the data). Cross-border payments could be one of those products.

Overall, most of the big initiatives are at an early stage or yet to launch. The US is the primary testing ground as it is a known market and home territory for the tech players above. Should you fear Visa and Mastercard even more given the acquisitions they have been making in the cross-border space?

Cross-border payments will be impacted either directly or indirectly by virtually all the initiatives shown above. To what degree, it’s too early to tell.

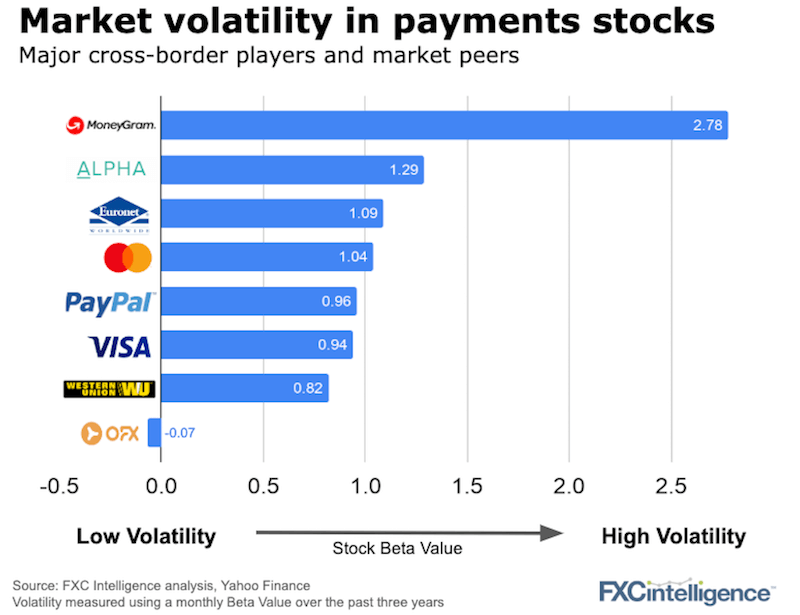

How volatile are public payment companies?

Last week was not for the faint hearted among MoneyGram’s shareholders. On 13 November, the stock fell almost 27% as its largest shareholder (private equity fund TH Lee) had a mass selloff via its limited partners. Two days later, MoneyGram announced some planned cost cutting at corporate in Dallas and the stock bounced back almost 10%.

Is MoneyGram the most volatile cross-border payments stock or was this just a busy news week?

To answer the question, over the last three years, MoneyGram is far and away the most volatile stock amongst its peers.

Note: We used the standard Beta value measure of stock market volatility. A Beta value equal to 1 means a stock moves in line with the market, greater than one means it is more volatile than the market and less than one, less volatile. A negative value (e.g. for OFX) means the stock moves in the opposite direction to the stock market.

Bill.com’s IPO plan and international focus

Bill.com’s filing document for its planned IPO mentions the word “international” 32 times. For a company that was until recently just focused on solving US companies domestic payables needs, the planned IPO gives a good indication of where Bill.com is going.

As we’ve covered previously, Bill.com competes with a range of other players in the small and medium sized businesses (SMEs) payment simplification area (e.g. Veem, Tipalti). It also competes with all the known accounting integrations that many other payment companies offer (e.g. TransferMate, TransferWise, WorldFirst with Xero, Sage, Quickbooks).

Bill.com says it has processed around $500m in international payments to date, having only launched a year ago. Expect this number to grow substantially as it wins share from the FX-only incumbents.

[fxci_space class=”tailor-633311ef768f8″][/fxci_space]