Under the leadership of new CEO and President Enrique Lores, PayPal has announced a strategic realignment that will see the company reform in three distinct operating units. But how do its cross-border payments solutions fit into the mix?

Just three months on from his appointment as President and CEO of PayPal, Enrique Lores has set out his vision for the company, in a wide-reaching strategy unpacked during the fintech’s Q1 2026 earnings call.

While the strategic realignment retains some of the previous administration’s plans for increased interoperability and integration, it also takes a sharply different approach in other areas. Alongside this comes a significant cost-cutting plan that is set to drive upwards of $1.5bn in gross run-rate savings within two to three years.

This will impact many areas of the business, not least its cross-border payments solutions, including its money transfer products in PayPal P2P and Xoom, as well as its cross-border checkout products. It will also see a change to how the company approaches its domestic P2P-led brand Venmo.

During the earnings call, Lores framed the initiative as putting PayPal on a “more durable path to long-term growth and shareholder value creation”.

“We have a strong foundation, and we are now organised to move with greater urgency.”

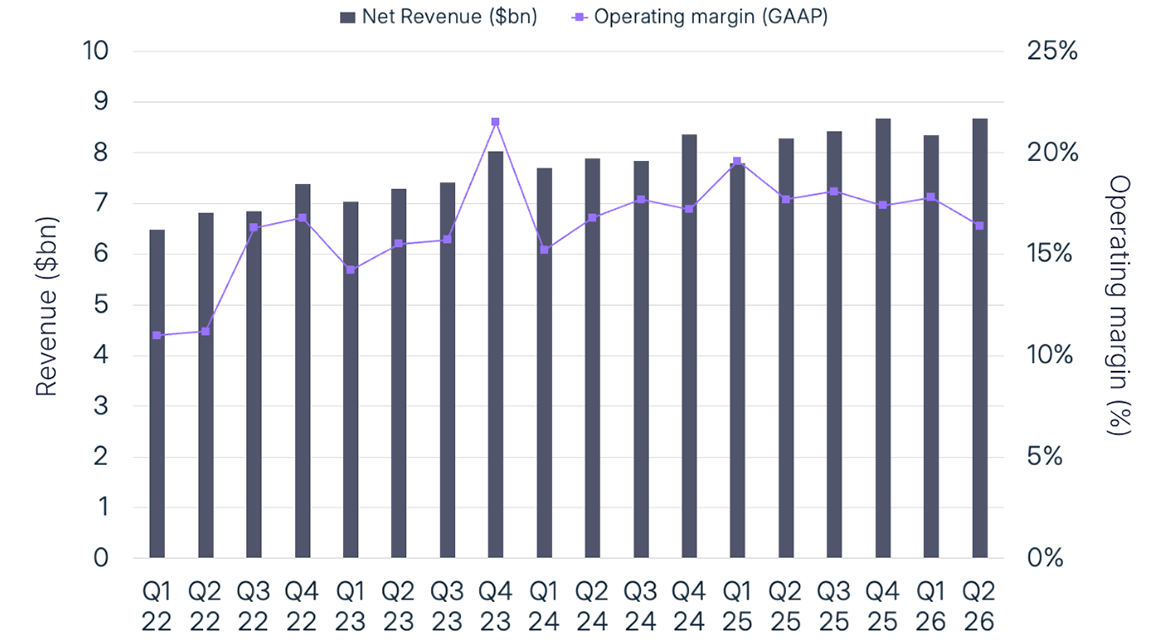

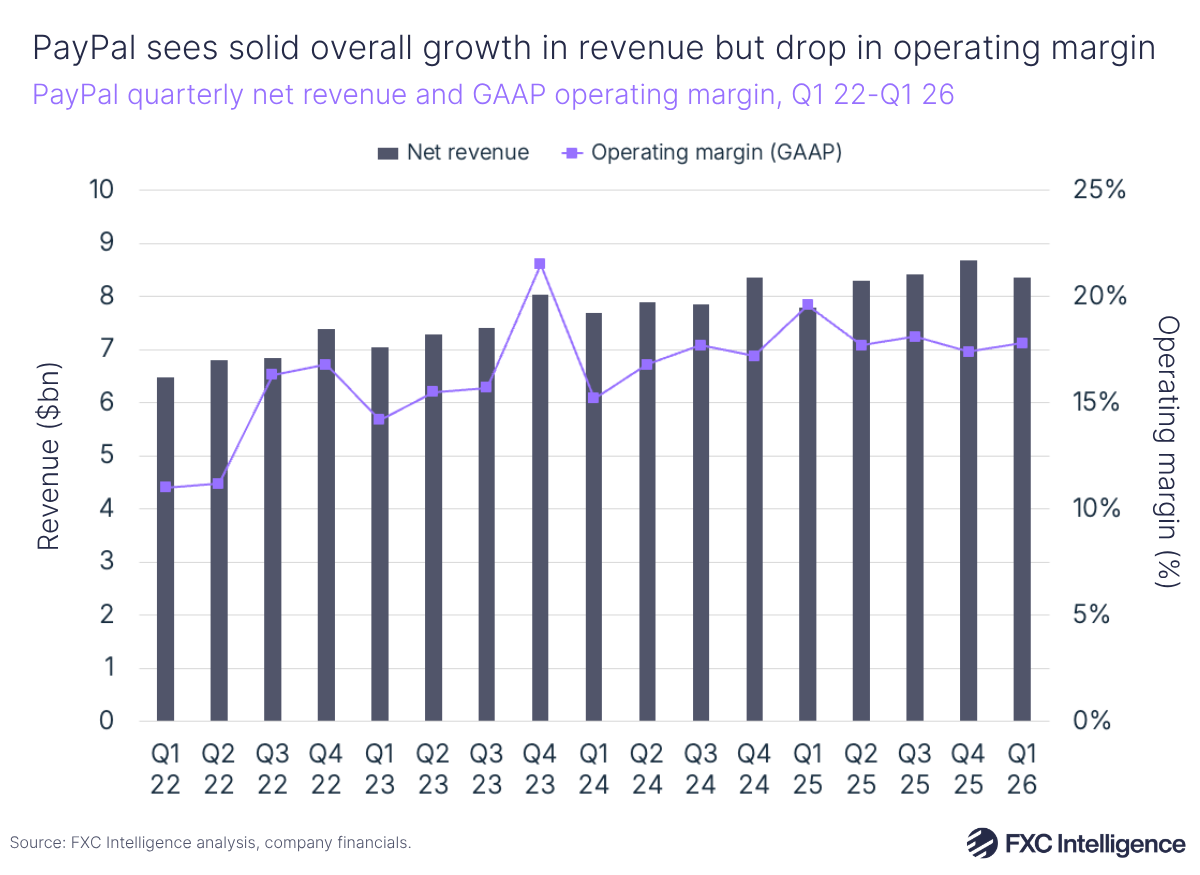

The announcement, which was accompanied by solid top-line results but a weaker operating margin, was met with a negative response by the market, with the company’s share price dropping sharply.

PayPal’s Q1 2026 results deliver modest growth

The realignment was announced shortly before PayPal delivered its first results under Lores, in which it reported solid top-line results. Net revenues saw an increase of 7% to $8.4bn, or 5% on an FX-neutral basis, while transaction margin dollars grew 3% to $3.8bn, including $0.3bn of interest on customer balances, slightly ahead of the company’s guide.

This was attributed to monetisation of Venmo, unbranded card processing profitability and credit performance, as well as a loss improvement across a number of different product areas.

US revenues also increased their already dominant share of overall revenue – climbing 9% YoY to $4.9bn while international revenue grew 4% YoY to $3.5bn – but were flat on an FX-neutral basis. Jamie Miller, PayPal’s Chief Financial & Operating Officer, attributed this to increased international pressure from higher oil prices and an impact from travel in Europe.

However, PayPal also saw a 182 bps contraction in GAAP operating margin to 17.8%, driven by a 3% decrease in operating income to $1.5bn. This was attributed to increased investment expenditure, with the company having decided to accelerate the timeline for investments in technology, marketing and product under Lores’ leadership. Despite the reduction, the company has reaffirmed the full-year 2026 guidance it gave in its FY 2025 results.

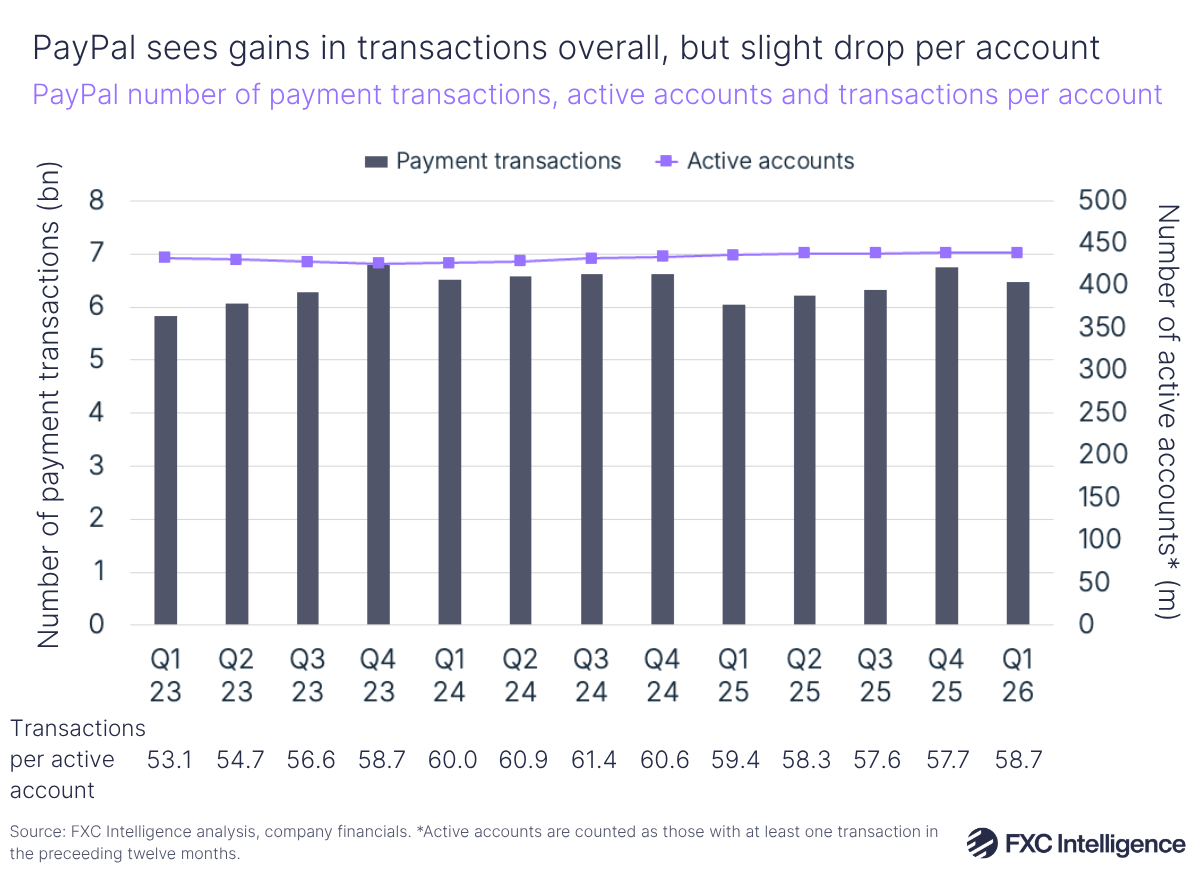

The company has seen a slight increase in active accounts, defined as those with at least one transaction in the past 12 months, which increased 1% YoY to 439 million, although did contract marginally – by 0.04% – versus Q4 2025.

Monthly active accounts, which are those with at least one transaction in the past month, inevitably dropped versus Q4 2025, but were slightly higher than Q1 2025.

Meanwhile, the number of payment transactions increased 7% year-on-year to 6.5 billion, meaning that the number of transactions per active account has seen a 1% drop year-on-year to 58.7. Excluding unbranded card processing, however, transactions per active account grew 6% YoY to 37.2.

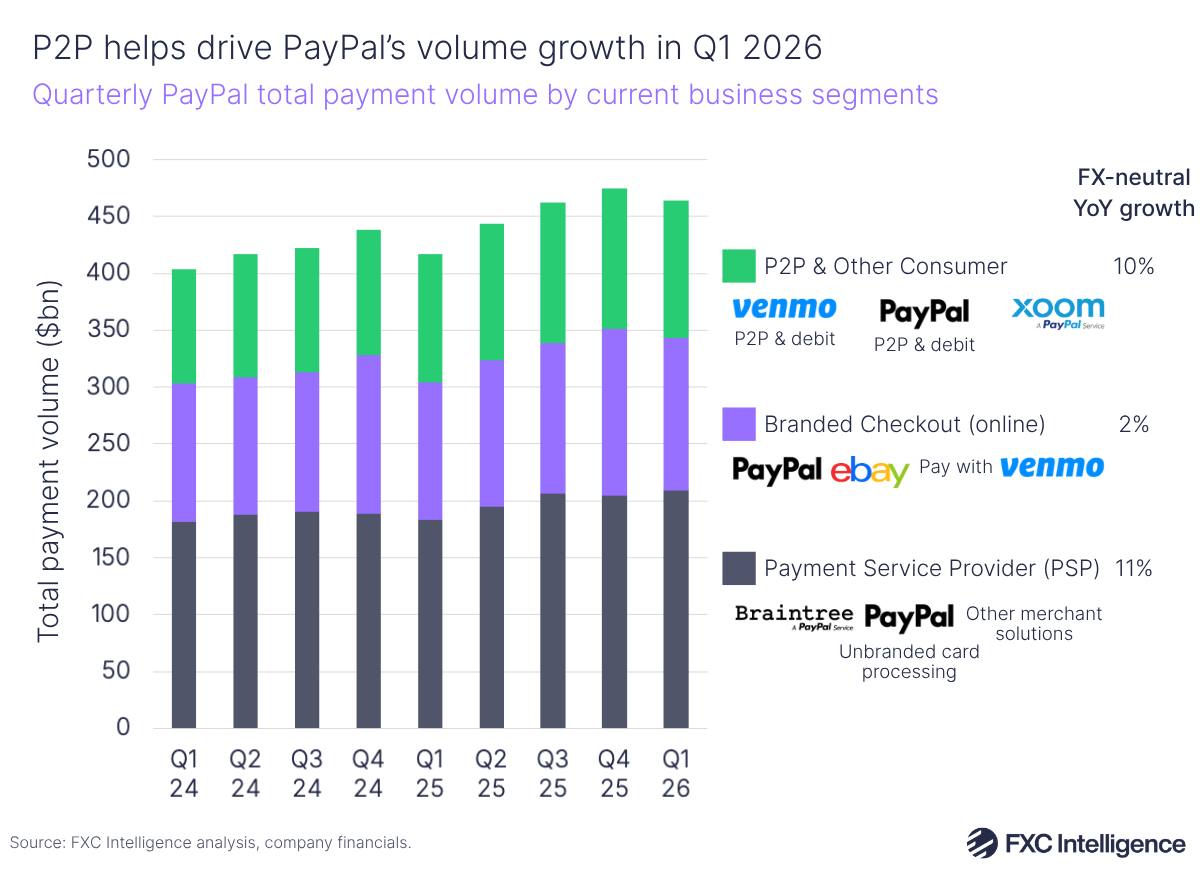

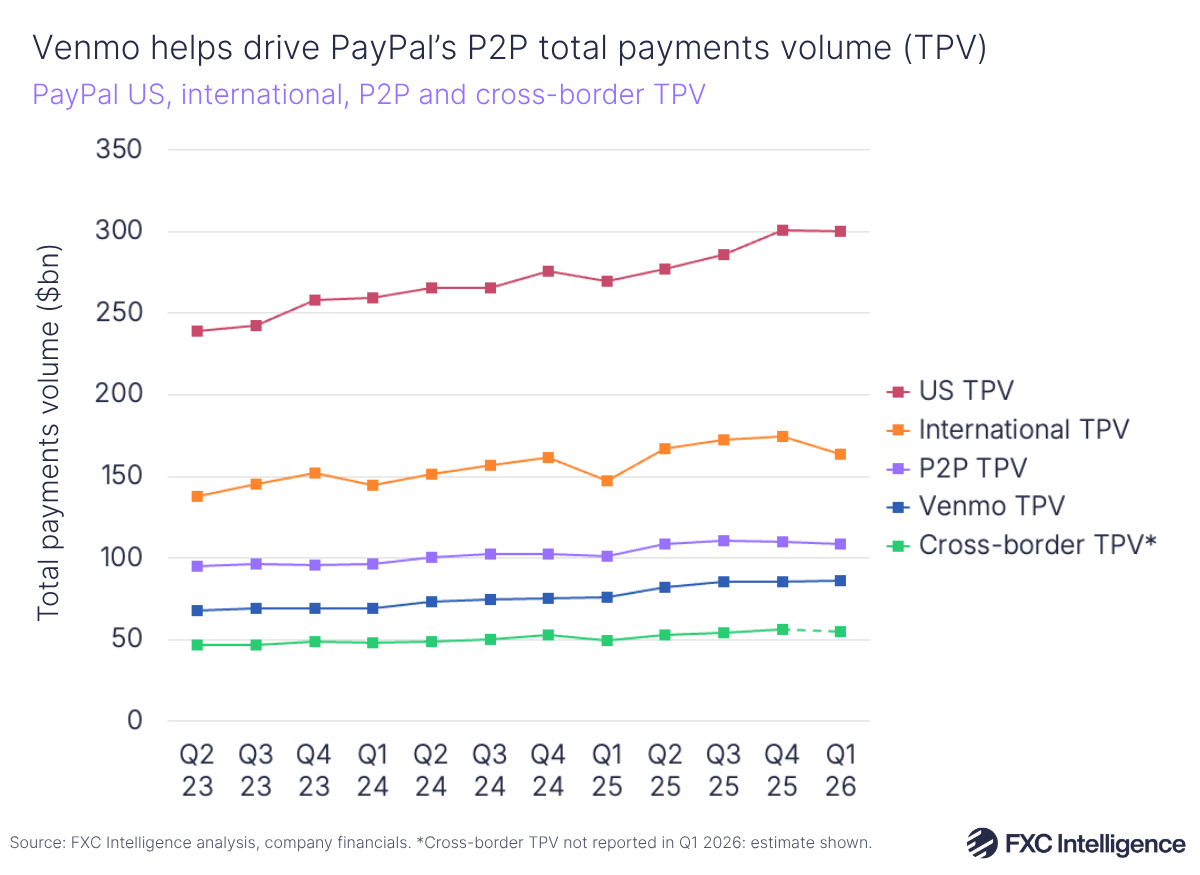

P2P is a key driver of PayPal’s volume growth

Total payment volume (TPV) saw its strongest growth in two years, climbing 11% YoY to $464bn, or 8% on an FX-neutral basis. Both US and international TPV also saw 11% growth, though international TPV stood at 2% on a FX-neutral basis.

This reflects how much of an impact foreign currency fluctuations have had on the brand this quarter, with foreign currency hedges also being highlighted as a key driver of a 6 bps drop in transaction take rate to 1.62%.

Along with a number of other key metrics, PayPal currently breaks out TPV into three top-level segments. These are P2P & Other Consumer, which covers PayPal and Venmo’s P2P and debit segments as well as money transfers brand Xoom; Branded Checkout, which covers PayPal branded checkout, Pay with Venmo and eBay; and Payment Service Provider (PSP), which covers unbranded card processing across PayPal and Braintree, as well as other related merchant solutions.

While P2P & Other Consumer is still the smallest of the three segments, accounting for 26% of all TPV, it was a key contributor of growth, seeing an FX-neutral increase of 10%, which was partially attributed to Venmo. PSP’s 11% growth, meanwhile, was attributed to enterprise payments.

Cross-border payments in PayPal’s volume reporting

Cross-border TPV, a metric that covers cross-border payments for both branded checkout and P2P payments but excludes those for unbranded checkout, has been reported by PayPal for every quarter for at least a decade. However, it was notably absent in these latest results, and there was no mention of cross-border payments during the earnings call.

However, the company did continue to report P2P TPV, which is a subsidiary metric of the larger P2P and Other Consumer line that covers domestic and cross-border P2P payments for Venmo, PayPal and Xoom. This saw a 7% YoY increase in volume to $109bn, although less than half of this is likely to be from cross-border P2P payments.

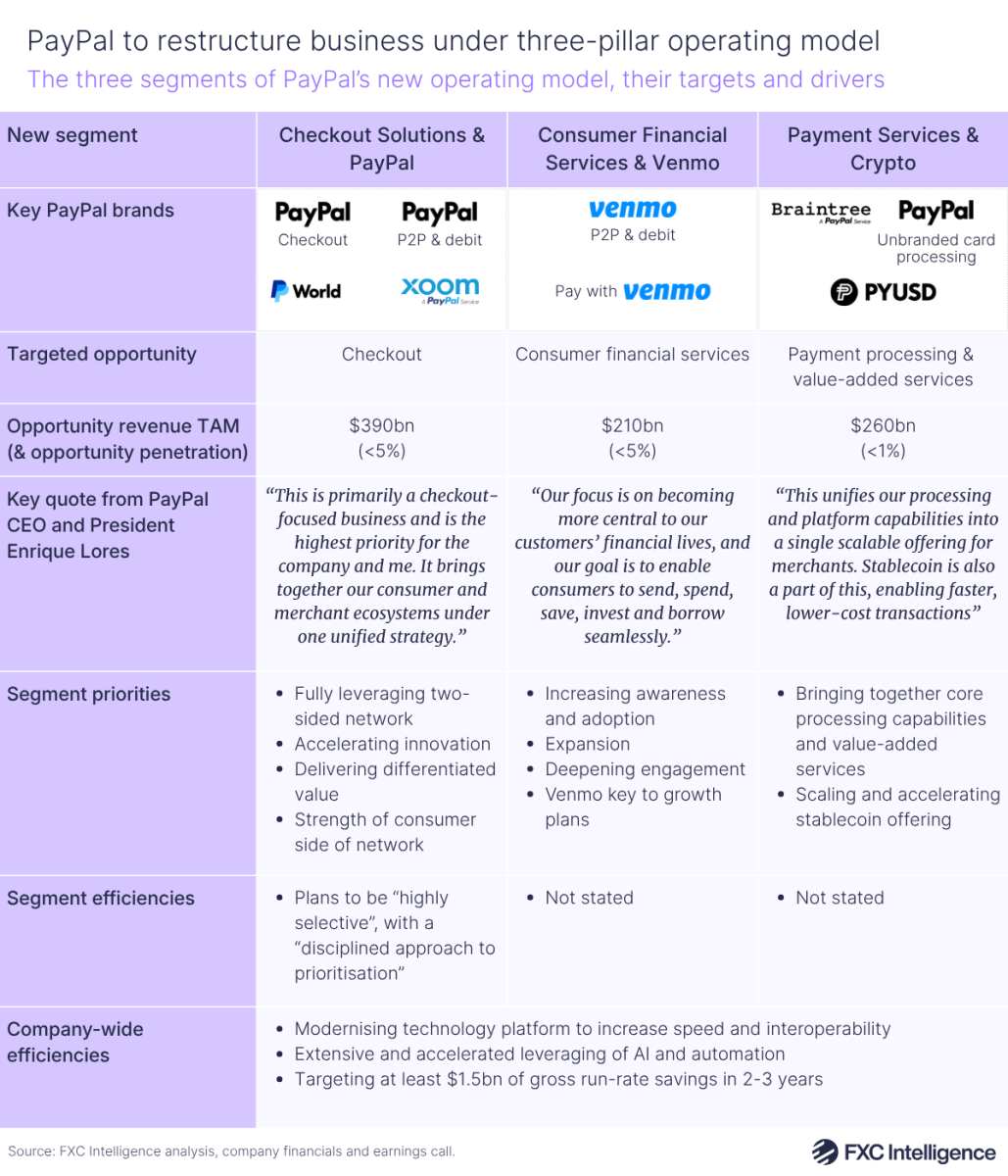

PayPal’s strategic realignment: Understanding the three business units

Despite only being three months into the role, Lores focused much of the call on his planned strategic realignment, which he said was built to address three “distinct, attractive and in many ways complementary market opportunities” that the company sees worthy of “focused investment and sharper execution”.

These are checkout, consumer financial services and payment processing services, and are being used as the foundation for each of the three new segments. Checkout Solutions & PayPal will target checkout, Consumer Financial Services & Venmo will target consumer financial services and Payment Services & Crypto will target payment processing services.

“We are aligning the organisation to unlock these growth opportunities,” Lores told investors.

“Previously, our teams were organised primarily around the customers we serve: consumers, small businesses and large enterprises. That structure resulted in organisational complexity, with multiple dependencies and hand-offs that slowed decision-making and weakened execution.

“The changes we announced last week will organise the company into three lines of business, each with a single leader. Simplifying our operating model and clarifying accountability means that each leader will own clear outcomes, and our teams will be able to focus on our most important growth priority.”

While the company has set out initial plans for each segment, which we go into more detail on below, there is still much that the company has yet to share, and in some cases that it is still to determine. Miller confirmed that the company would be launching the “full scope” of plans in the “coming months”, at which point it would share more details, while external reporting covering the new segments is planned for “some time next year”.

Notably, PayPal also acknowledged that there were some products that may not fit into its strategy, which it will also be reviewing.

Checkout Solutions & PayPal

Checkout Solutions & PayPal is framed around the checkout opportunity, which the company says has a $390bn revenue TAM and is the “highest priority”, according to Lores.

“This structure will enable us to fully leverage our two-sided network and accelerate innovation across both sides of the platform,” he told investors.

“Our intent is not to chase transitory share in any given quarter, but rather to focus on segments and verticals where we can deliver differentiated value to our customers.”

This is likely to see the company enhancing consumer financial service offerings such as buy now, pay later, as well as building on its PayPal+ loyalty programme, which launched in the UK in late 2025.

Crucially, however, this segment does not just include PayPal’s core checkout services, but the wider solutions under the branded PayPal umbrella. As a result, it will also include PayPal P2P and Xoom, separating these from Venmo P2P where they are currently reported together. Wallet interoperability solution PayPal World, announced in July 2025, will also come under this segment.

How these wider solutions will ultimately play into the wider PayPal brand remains to be seen. Lores said that there are a “number of compelling, innovative initiatives underway” over the medium to long term, but also warned that the company plans to “take a disciplined approach to prioritisation” within the segment that will see high-potential products and services being prioritised.

“Within this portfolio, we will be highly selective as we evaluate our broad set of initiatives, including digital wallet interoperability, biometric functionality and additional programmes under consideration,” he said.

Consumer Financial Services & Venmo

Consumer Financial Services & Venmo, meanwhile, is set to build awareness and adoption around the company’s Venmo-led financial services solutions, with the company eyeing a $210bn revenue TAM.

“Venmo will be a key component of our growth plans moving forward, supported by its strong brand and younger demographic,” said Lores.

“We are in a strong position to expand in this space, deepen engagement and increase customer lifetime value.”

There have been questions about whether this will ultimately see PayPal sell off Venmo as a standalone unit, including one put to Lores during the earnings call. However the CEO responded by saying that his number one priority was “maximising shareholder value”, adding that there were “significant synergies across the three businesses that make them stronger together”.

Payment Services & Crypto

Finally, Payment Services & Crypto is designed to bring the company’s merchant offering into a single platform, with an estimated $260bn revenue TAM.

“We will bring together the company’s unbranded processing capabilities, including Braintree, and value-added services such as fraud management, authorisation optimisation and global payment infrastructure,” said Lores.

“They are designed to support businesses of all sizes with flexible, high-performance payment solutions. We are also well-positioned to capture and monetise this growth.”

A notable inclusion in this segment is crypto, with the company’s PYUSD stablecoin being the third largest globally by market capitalisation, and the company seeing “much more opportunity to scale [its] offerings and accelerate growth in this space”.

This represents a notable realignment for its stablecoin offering, which previously had been increasingly connected to its remittances offering. However, by placing it under payment services, the company is focusing far more on checkout-based applications for its crypto solutions, and separating them more from its wallet-based offerings on the branded PayPal side.

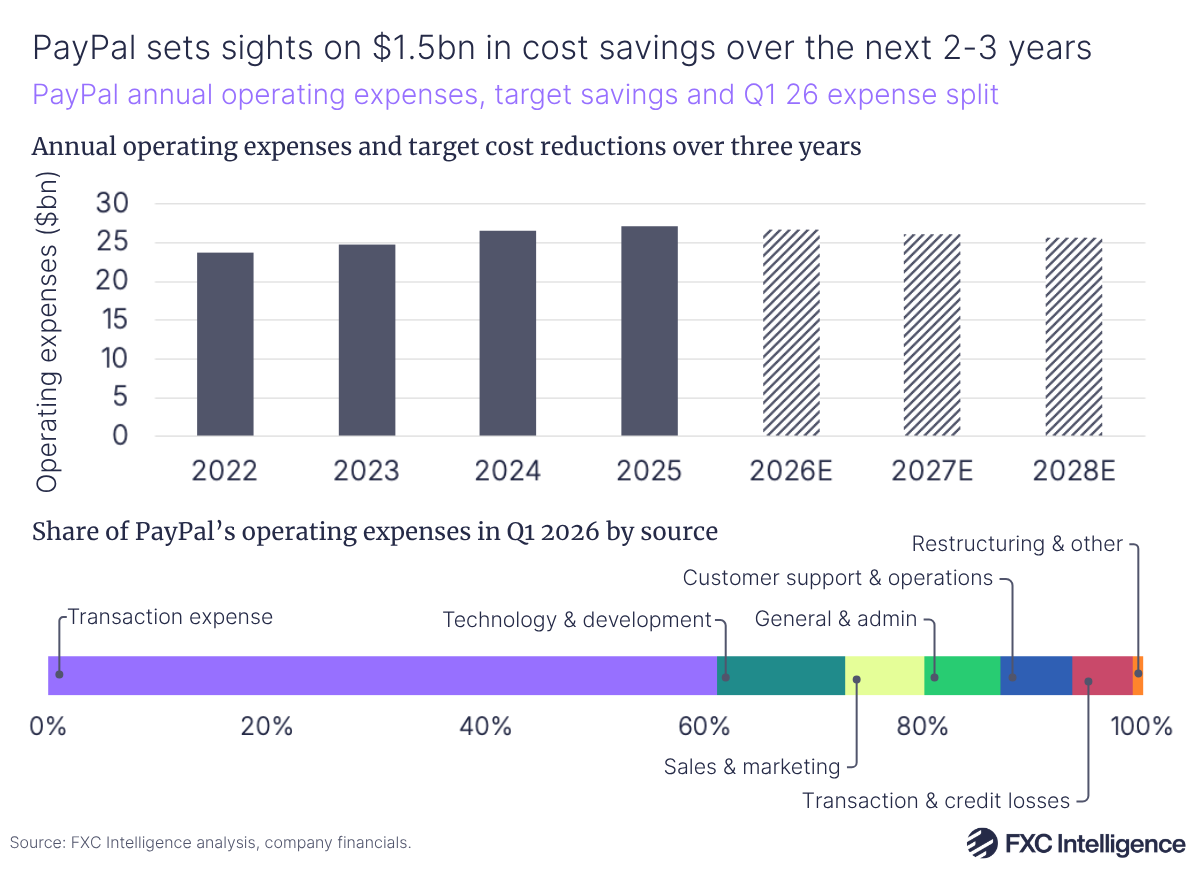

PayPal’s plans to achieve $1.5bn in cost efficiencies

Along with the strategic realignment to this three-pillar operating model is a broader focus on increased efficiency. The company has announced plans to achieve at least $1.5bn of gross run-rate savings within two to three years, which is set to see efficiencies realised across many different parts of the company.

“These efficiencies will come from organisational realignment, process redesign through AI and automation, procurement and vendor rationalisation and optimising our local footprint,” said Miller.

This will be achieved through two main parts. The first is seeing PayPal “simplify and de-layer” the company as part of the strategic realignment, as well as modernise its technology platform to increase speed and cross-solution interoperability.

The second is to speed up and build upon AI and automation initiatives, some of which were already detailed in the previous quarter’s earnings.

“Together, these represent two distinct waves of savings: the first from structural realignment and the second from accelerating AI adoption and automation, to comprise the vast majority of the more than $1.5bn cost savings program we will execute over the next two to three years,” said Miller.

“Looking ahead, we expect to deploy these cost savings to reinvest in growth and respond to business headwinds, improving our overall financial profile over time. During 2026 and into 2027, we will be transitioning teams, establishing new ways of working and building systems and processes to run the business aligned with the structure we have announced.”

How PayPal is looking to AI for cost savings

The company’s AI initiatives are expected to reach a wide range of areas across the business and are intended to drive improvements in both internal processes and the customer experience.

“This is aggressive deployment of AI with respect to customer experience; in support; in operations; and equally with respect to our risk platform and how we deploy AI as we do that,” said Miller.

“AI has a really across-the-board opportunity, particularly in customer support and operations but, candidly, across the company.”

She acknowledged that the company had already made “really good inroads” in its use of AI, particularly around areas such as engineering productivity, but argued that a “full top-to-bottom acceleration is going to be really important”.