PayPal has continued to report growth in Q4 and FY 2025 on the back of significant gains in its Venmo and buy now, pay later (BNPL) businesses. However, the company’s share price declined significantly in response to slower-than expected growth in its Q4 results and upcoming guidance, as well as a change in its CEO.

The morning of its earnings call, PayPal announced that CEO Alex Chriss would be departing, with former board chair Enrique Lopez taking over from 1 March 2026. Interim CEO Jamie Miller said that the change will “accelerate execution and bring greater discipline” to how PayPal approaches its strategy, adding that the company had “not moved fast enough with the level of focus required”.

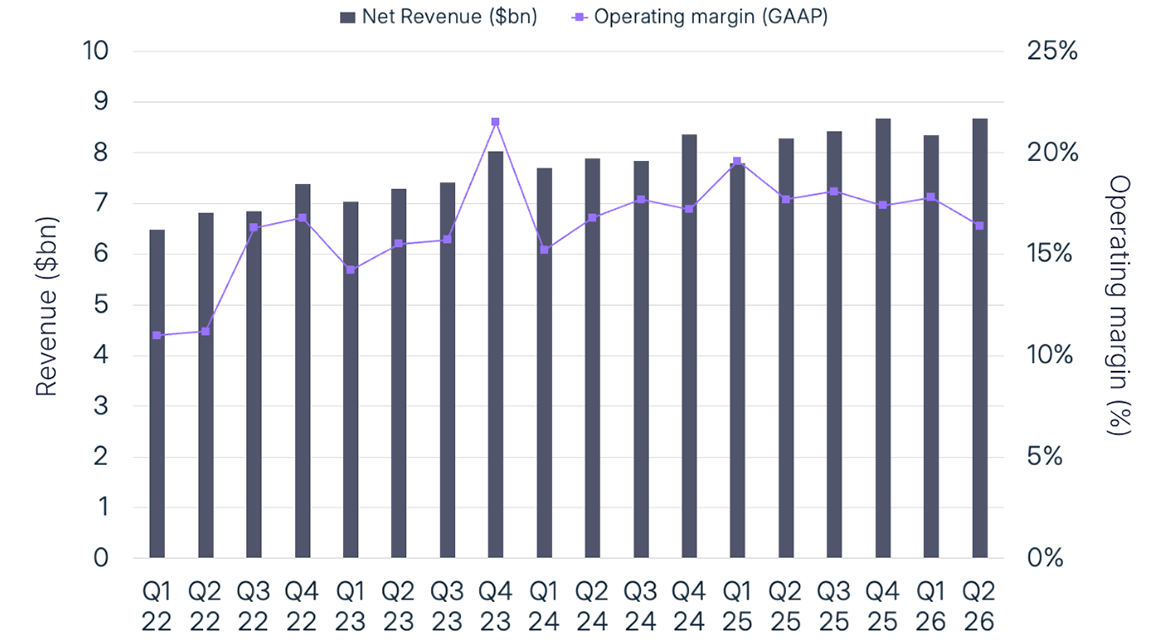

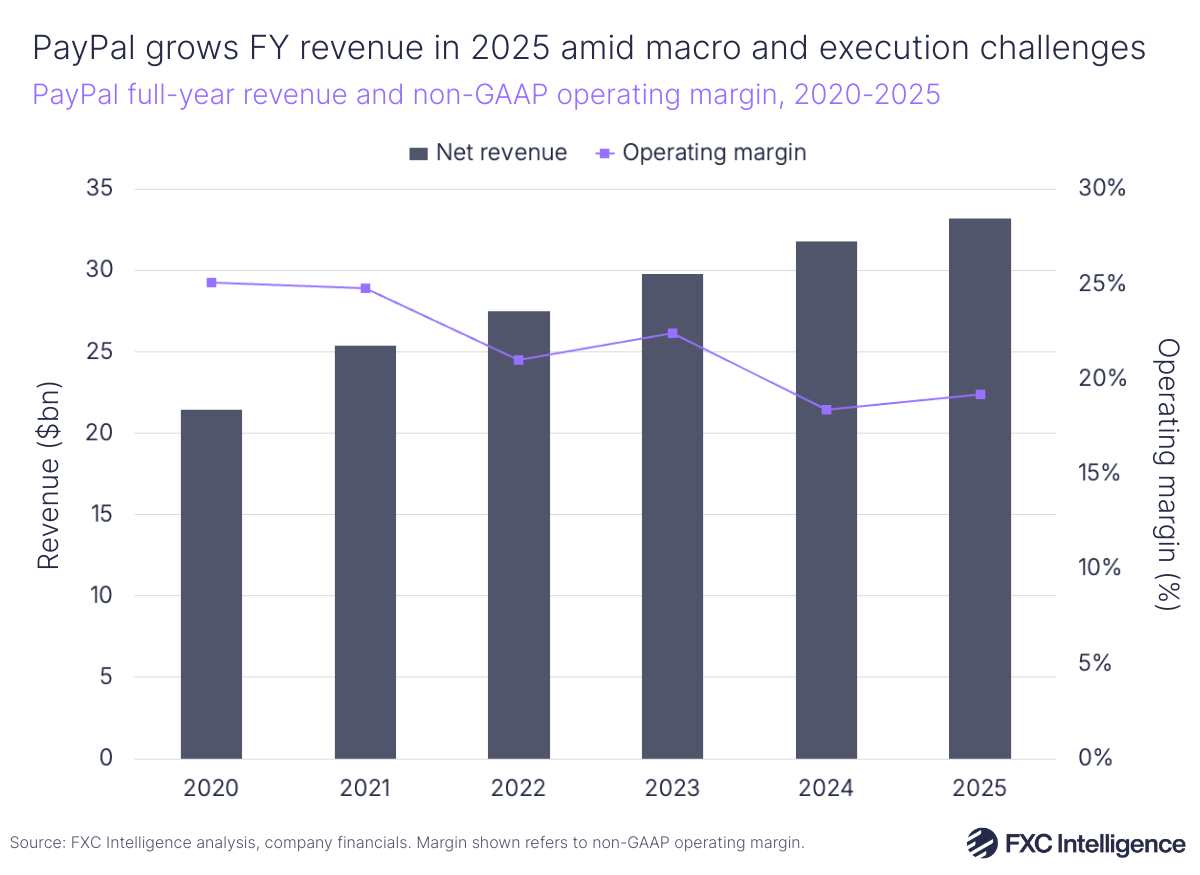

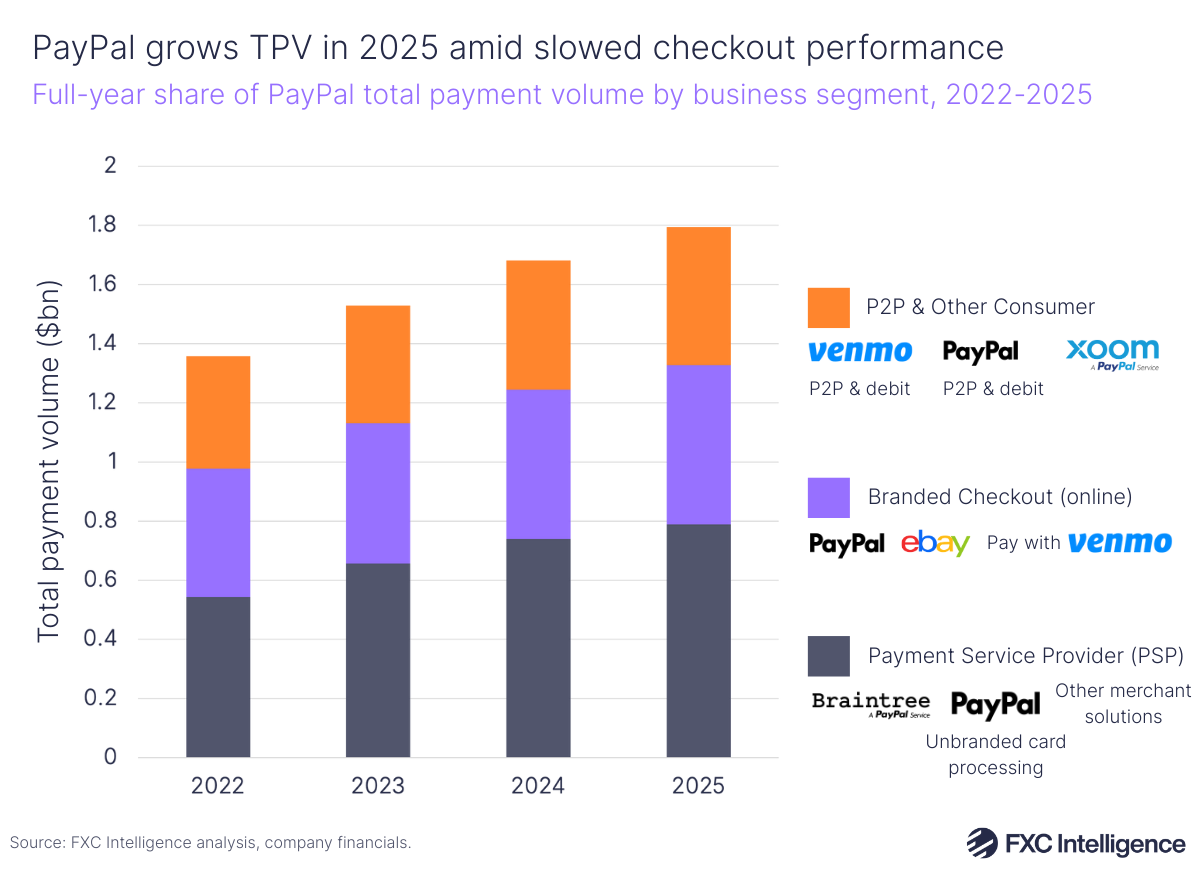

Despite this, the company’s diversification strategy has offset some of its losses and it continues to report positive revenue growth for the year. PayPal’s net revenues grew 4% year-on-year to $8.7bn in Q4 2025, driving full-year revenues up 4% to $33.2bn. Total payment volume (TPV) increased by 9% YoY (6% on an FX-neutral basis) to $475.1bn in Q4 and 7% to $1.8tn across the full year as the company made significant gains across its Venmo, BNPL and enterprise payments businesses.

For the full year, the company saw a 6% rise in transaction margin dollars – which tracks total revenue less transaction expenses and transaction and credit losses, and is PayPal’s metric for tracking profitability from its core payments business – to $15.5bn. It also noted an adjusted operating margin of 19.2% in 2025, up from 18.4% the previous year. However, based on our calculations, slower revenue growth meant that PayPal also saw its take rate for the full year decline, from 1.89% in 2024 down to 1.85% in 2025.

PayPal is no longer committing to the growth guidance for 2027 it had laid out at its investor day last year, due to macroeconomic headwinds, competition and slower-than-expected adoption of its new products. Instead, the company said that for 2026 it was expecting a slight decline in its transaction margin dollars, while it expects its non-GAAP earnings per share to range from a low single-digit decline to slightly positive growth.

PayPal’s checkout arm declines on back of growing competition

PayPal saw lower than expected growth in Branded Checkout – its product enabling customers to pay directly using PayPal via a merchant’s website or app. This segment saw TPV growing 1% on a currency neutral basis in Q4 2025, down from 6% in Q4 2024.

PayPal attributed the slowdown to retail weakness in the US; international headwinds in Germany, where the company saw macroeconomic softness and competition from some alternative payment methods; and decelerated growth across some key verticals, including ticketing, crypto and gaming.

Overall, Branded Checkout took a 31% share of PayPal’s TPV in Q4 2025, down from 32% in Q4 2024. This makes it a larger segment than PayPal’s P2P and Consumer business, which accounted for 26% of TPV and comprises PayPal and Venmo’s P2P and debit businesses, except when used to fund a Branded Checkout (online) transaction and remittances. However, PayPal still saw the highest volumes from its Payment Services Provider business, which accounted for 43% of TPV and grew 8% YoY (currency-neutral) in Q4 2025 on the back of double-digit growth in Enterprise Payments.

Aside from driving profitability through its PSP business, PayPal also mentioned how it had begun to target other ‘next-gen growth vectors’ in 2025, including stablecoins and PayPal World, its company’s global digital wallet interoperability network announced in the middle of last year.

Venmo and BNPL offset checkout declines

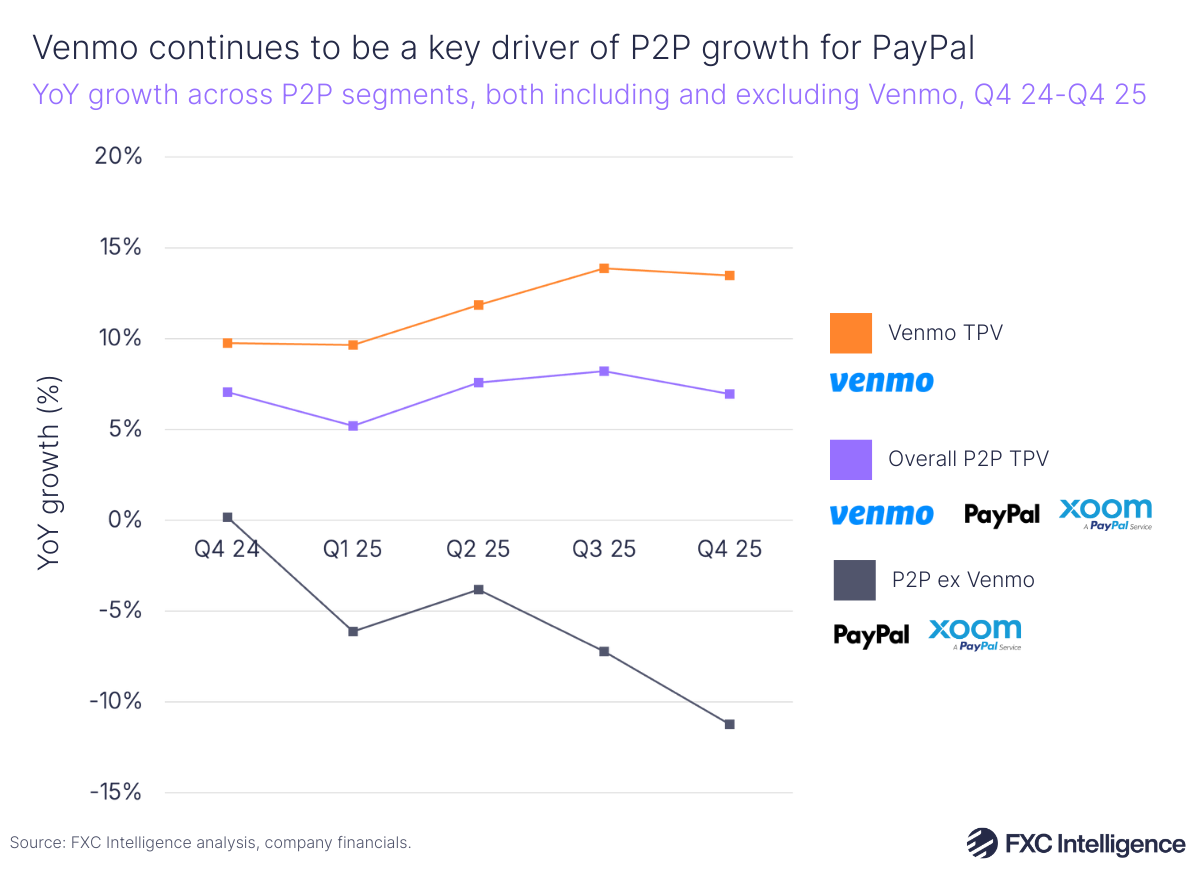

Venmo has been particularly critical for PayPal in its standalone P2P segment, which includes Venmo, PayPal and Xoom. P2P TPV overall grew by 7% in Q4 25, driven by 13% growth in Venmo; excluding Venmo, P2P declined by 11%.

Focused on domestic P2P transfers in the US, Venmo is rapidly growing users and also seeing strong growth in its recently launched debit card, which saw TPV growth in Q4 25 accelerate by over 50% YoY. Separately, PayPal is also seeing success in its BNPL product, with TPV surpassing $40bn in 2025.

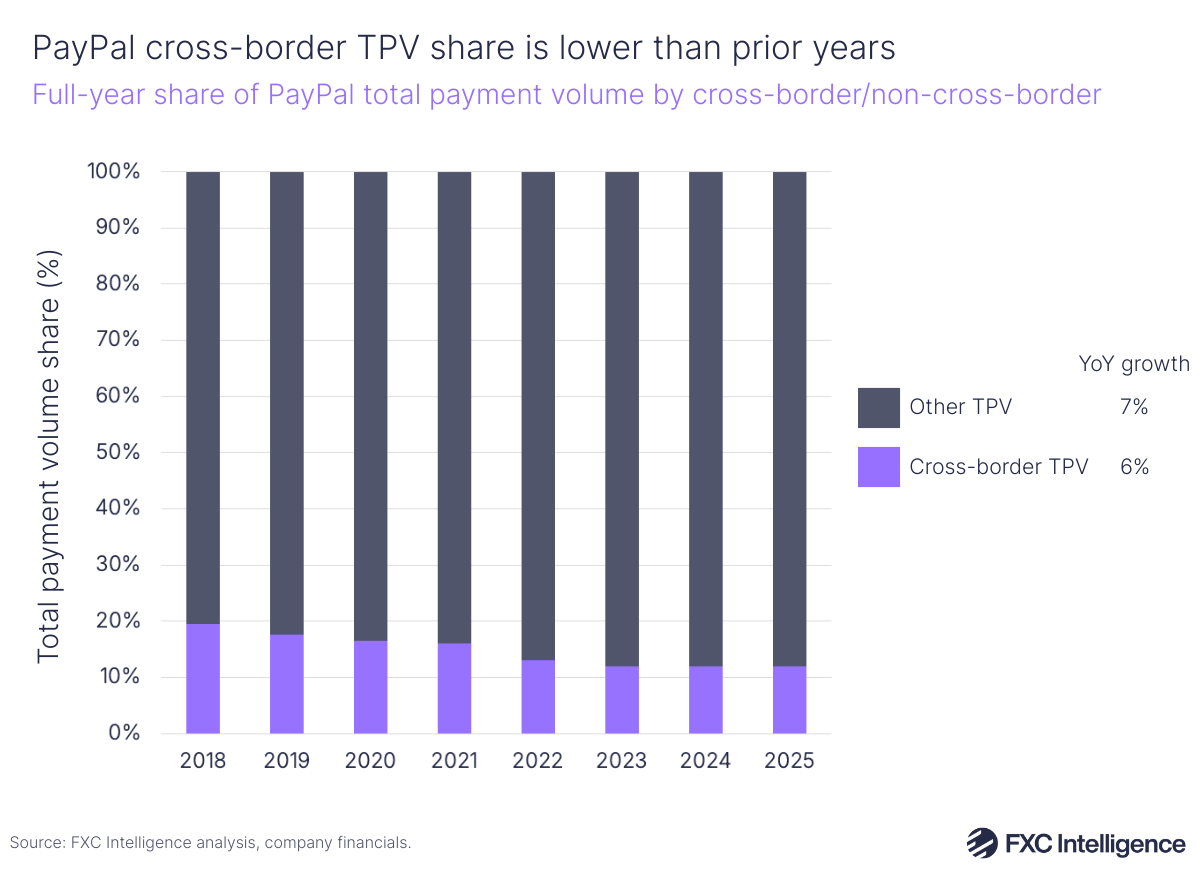

The decline in Branded Checkout in Q4 was likely a contributor to slowing cross-border TPV for the quarter, as cross-border TPV contains both Branded Checkout and P2P volumes. On a currency-neutral basis, cross-border TPV grew 1%, versus 9% in Q4 2024, with PayPal reporting that the 1% growth was driven predominantly by intra-European corridors.

Altogether, success in Venmo, debit cards and PSP drove US TPV up by 9% in Q4 2025, while international TPV, hampered by headwinds in Germany despite “continued growth in Europe”, grew by 2%. Overall, the US remained PayPal’s core market in Q4 2025, accounting for 63% of TPV.

Based on PayPal’s Q4 performance, cross-border TPV accounted for 12% of PayPal’s total volumes in 2025, flat on the year before, though historical earnings results show that this share has decreased over time.

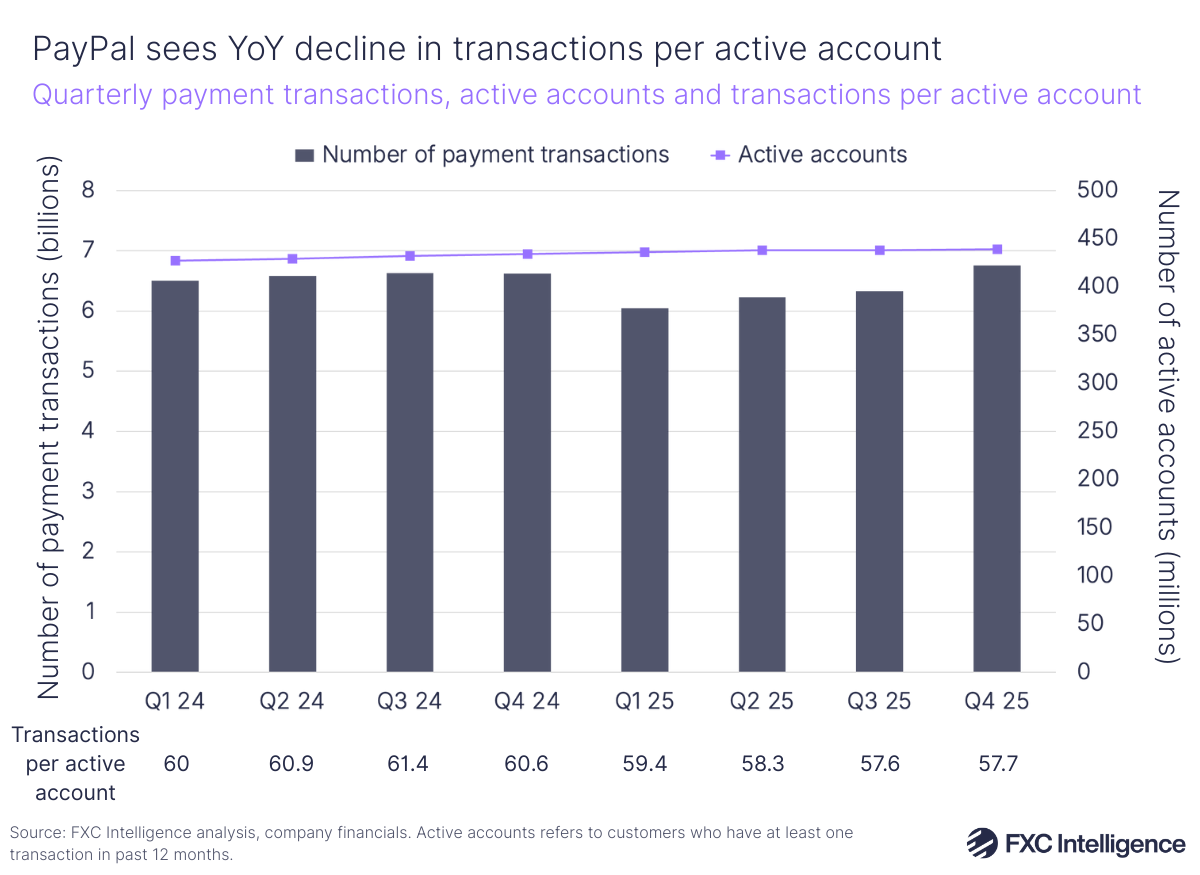

PayPal noted that its number of transactions grew 2% YoY to 6.8 billion in Q4 2025, though the company saw this number decline by 4% to 25.4 billion in FY 2025. Based on figures given, the average volume per transaction through the company rose by 6% YoY in Q4 2025, however the number of active transactions per customer was down 5% YoY.

PayPal’s strategy moving forward

Diversification was a key word in PayPal’s earnings as the company looks to build in more resilience this year, and particularly as it saw strength from Venmo and its PSP business offset many of the headwinds from its Branded Checkout business.

The company expects its investments to create a three-point headwind to profit growth in 2026, with two thirds of this investment spending going towards Branded Checkout and BNPL, with the remainder focused on Venmo, loyalty and agentic commerce. The company gave a specific update on the last of these, through which it is enabling AI agents to access and transact with merchants on behalf of customers, with early adopters including Abercrombie and Fitch, Fabletics, PACSUN and Wayfair.

Going forward with a new CEO, PayPal’s goal will be to show investors it can overcome impacts from competition while accelerating growth, particularly in cross-border ecommerce and P2P payments, as well as withstand challenges faced by soft retail in its core markets.