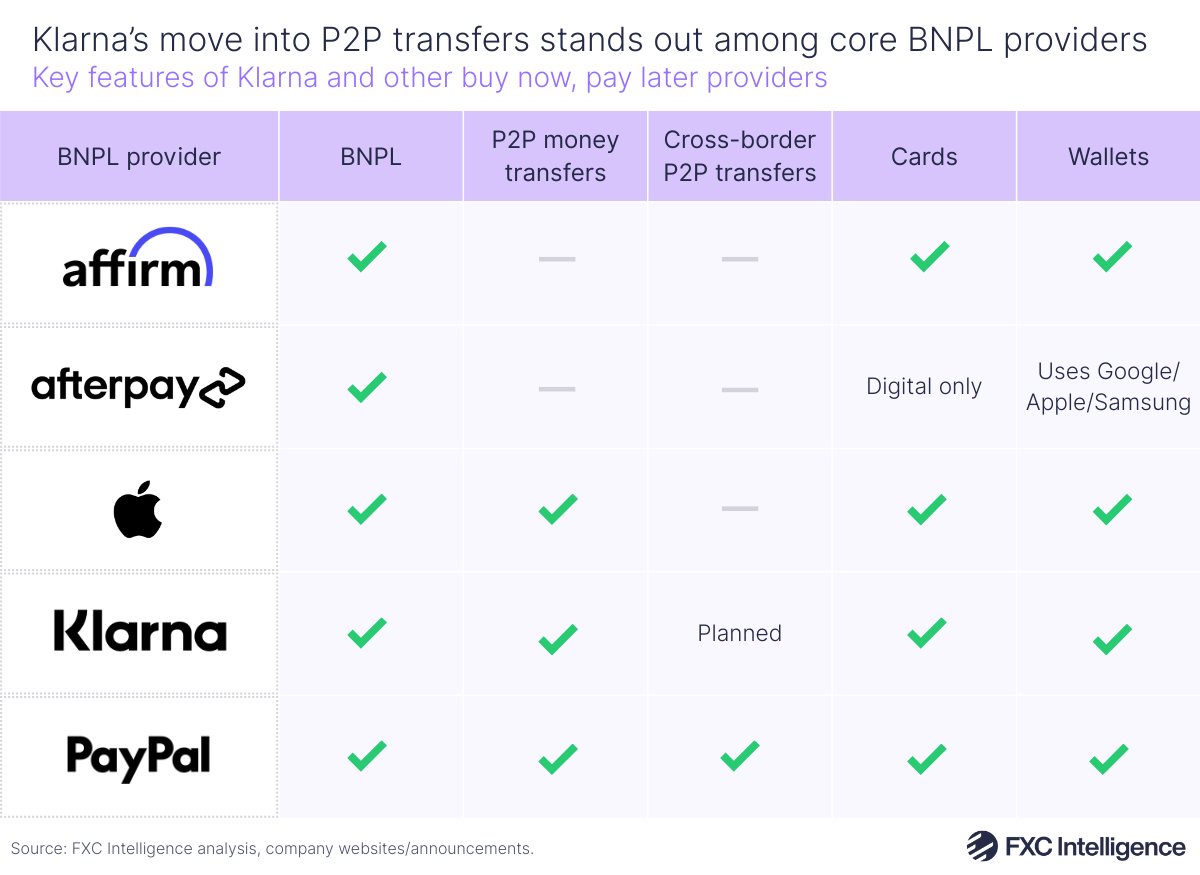

Last week, BNPL provider Klarna launched P2P payments in 13 markets across Europe, enabling its customers to send money to each other. While initially focusing on domestic transactions, the company has said it will soon expand to non-Klarna customers and cross-border payments.

Klarna’s entrance to P2P transfers makes it stand out among other core providers in the space. Its cross-border plans bring it into a new arena of P2P payments providers such as Remitly and Wise – both of which are themselves looking to capture more volume from users with new features.

The move comes a few months after Klarna launched its stablecoin, KlarnaUSD, on the Tempo blockchain, and follows the company’s IPO in September 2025. As part of its launch of P2P transfers last week, the company said that it was currently exploring stablecoin-based options to enhance the speed, reach and efficiency of payments.

Before the company listed, it saw rapid growth across its other banking products, having seen global deposits into Klarna balance – its digital wallet feature – grow from $9.5bn after the wallet’s launch in August 2024 to $14bn. Klarna’s debit card also saw four million signups in the first four months after its launch in Europe last September, with card payments reportedly now making up 15% of total volume.

In its Investor Presentation in November 2025, Klarna made clear its intentions to continue becoming a next-generation digital bank, having seen active consumers grow 32% to 114 million in Q3 2025 and merchants growing 38% to 850,000. This drove gross merchandise volume (GMV) up 29% to $32.7bn and revenue up 29% to $903m in the same quarter, with quarterly revenue expected to have surpassed $1bn in Q4 2025.

Klarna has secured higher revenue while achieving significant operational efficiency, with large contributions by AI enabling it to curb expenses. This puts the company in good stead to move into new markets. Although Klarna said in November that it only accounts for 0.6% of a $520bn serviceable addressable market, it sees room to potentially expand into other new markets that could effectively double this TAM.

Klarna has made significant gains from a booming BNPL market and its moves to capitalise on the growing amount that consumers are depositing with fintechs reflect a wider trend. However, whether it can translate this success to a competitive money transfer market remains to be seen.