Earlier this month, the US Federal Reserve Board announced it was inviting public comment on a proposal that would allow US banks and credit unions to use intermediaries to transfer funds through FedNow – the US central bank’s 24/7/365 instant payment service. This could be a potentially important milestone for the system, which is rapidly scaling adoption across US banks.

Launched in 2023, FedNow is the US’s attempt to help make payments significantly faster for businesses and individuals across the country. It arrived years after the US’s other instant payment system RTP, launched by private bank consortium The Clearing House in 2017. It also came long after private, branded P2P payments offerings such as Zelle and Venmo, launched in 2017 and 2009, respectively, to make it easier for consumers to make payments digitally to each other. However, unlike Zelle and Venmo, which are consumer-facing payment apps, FedNow is a payment rail operated by the US Federal Reserve to allow banks to offer real-time payments.

FedNow’s design remains focused on enabling fast transactions between banks in the US, and this doesn’t change with the new proposal. However, the Fed highlighted that by allowing banks and credit unions to use intermediaries to transfer funds through FedNow, this could include banks transacting with correspondent banks to facilitate the international portion of cross-border payments – similar to what is offered by its Fedwire Funds services. By enabling fast domestic settlement, FedNow could reduce delays on the US leg of cross-border payments – but the movement of money across borders would still rely on a connected third party. If the proposal goals ahead, cross-border payment providers could speed up pay-outs in the US, but would still need to handle FX separately.

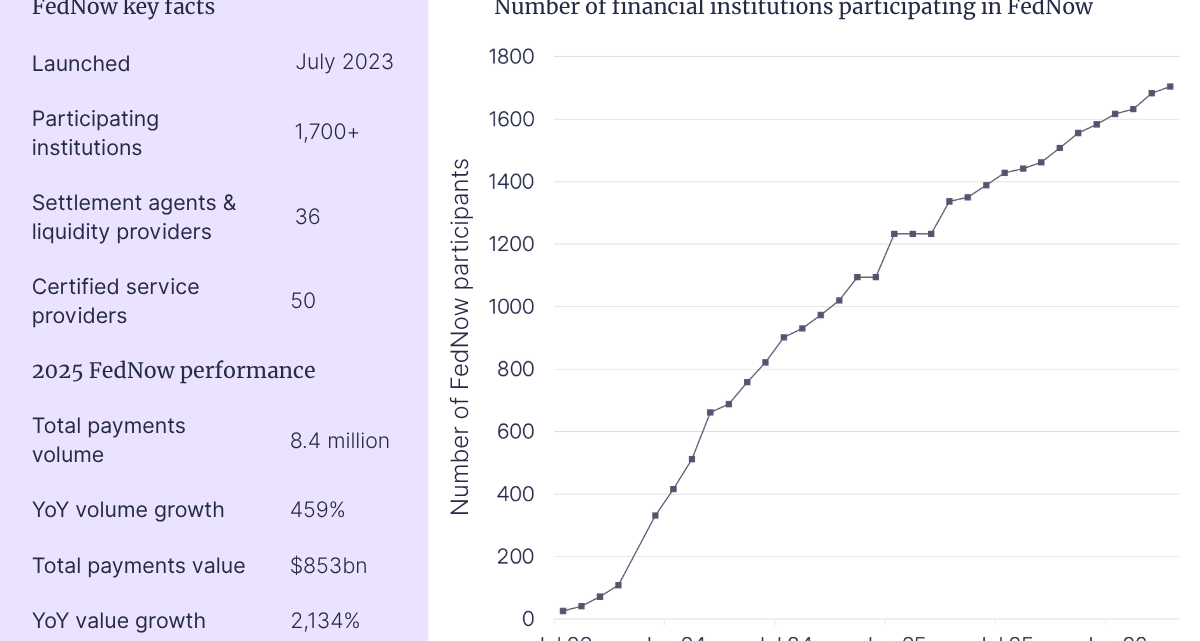

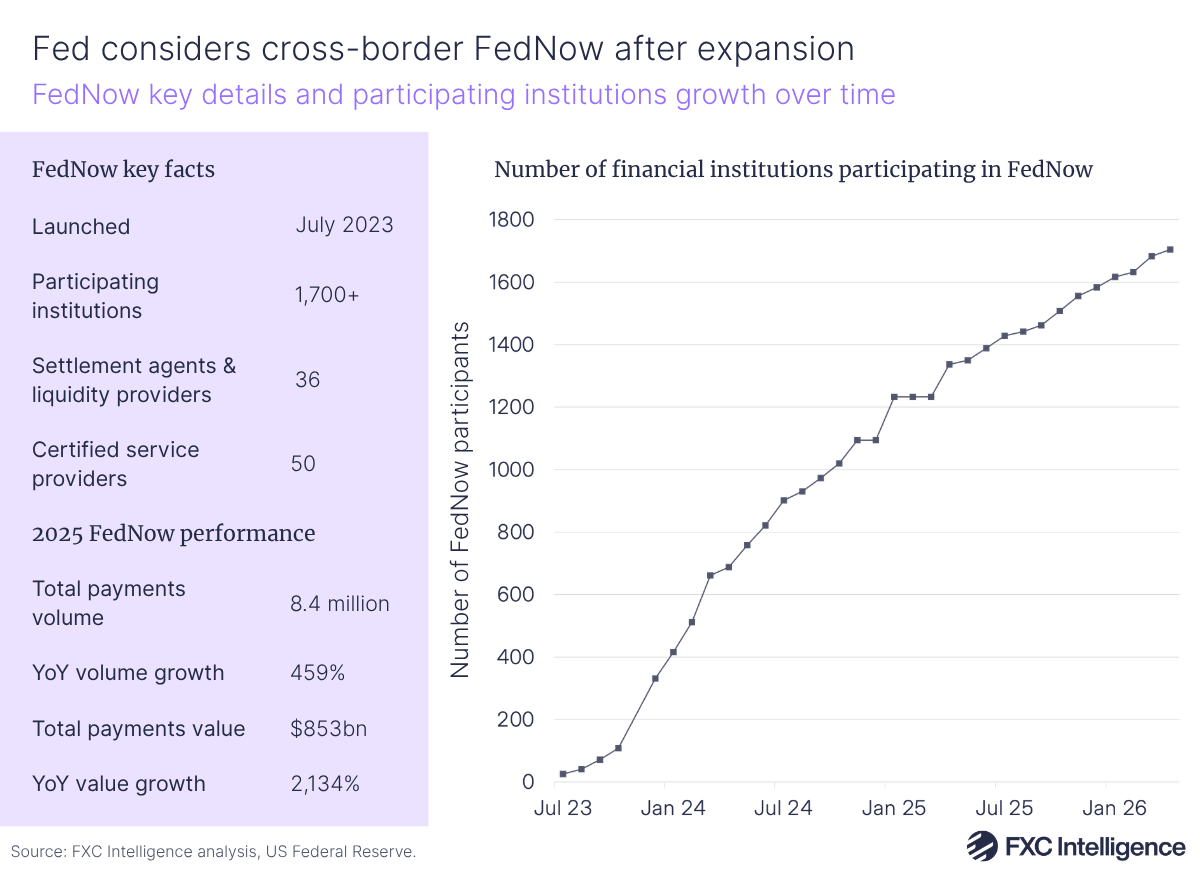

The number of financial institutions – including banks and credit unions – participating in FedNow has grown from 20+ at launch to over 1,700 as of April 2026. This means it now serves a higher number of institutions than RTP, which currently serves just under 1,200 banks. However, it is still a small share of the 9,000 institutions that the Federal Reserve originally committed to working with in 2023.

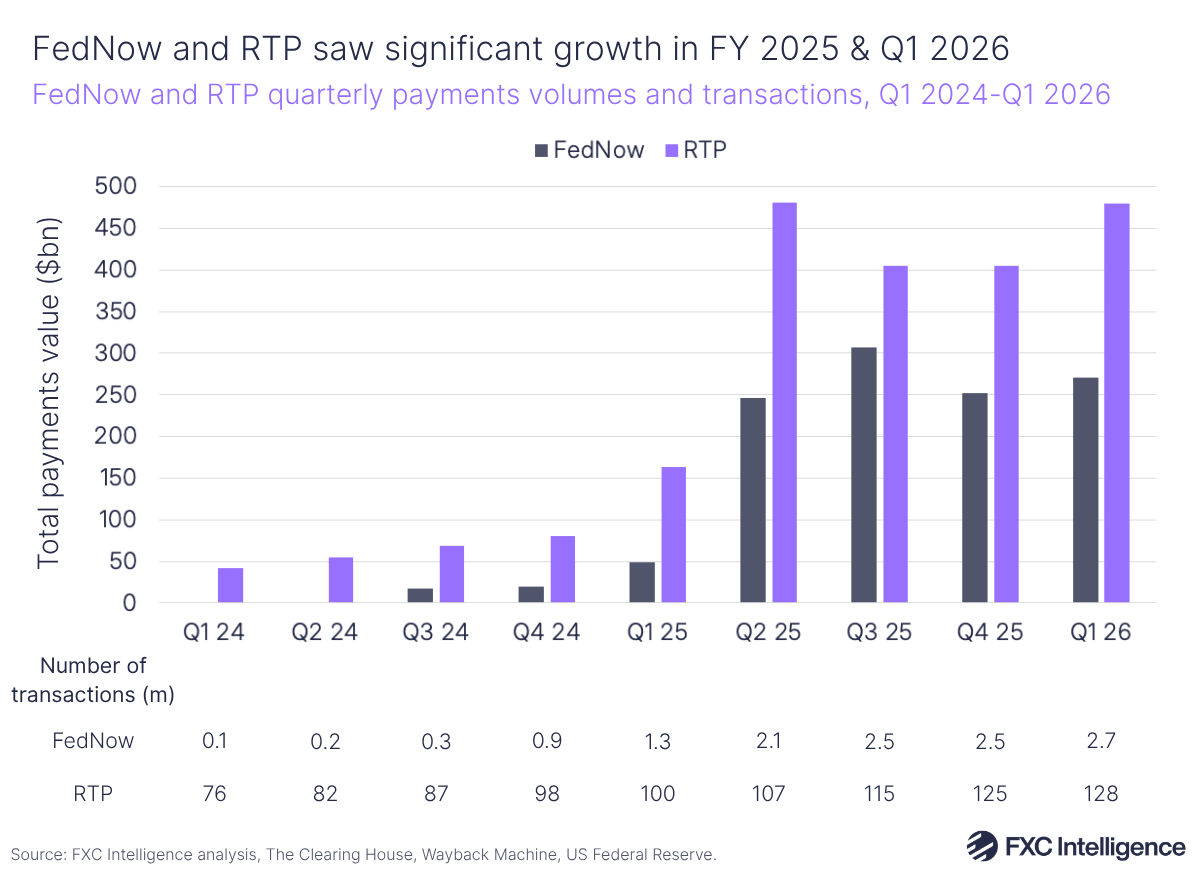

FedNow has also seen growth in the number of transactions and total payments value moving through the system. In Q1 2026, the number of transactions rose 108% YoY to 2.7 million, following a FY 2025 annual rise of 459% to 8.4 million transactions. Payments value through the system has seen a larger increase, with transaction value rising by 458% to $271bn in Q1 2026. Across FY 2025, the annual transaction value rose by 2,134% to $853bn.

By comparison, The Clearing House’s figures for RTP show that transactions passing through the system rose by 28% YoY to 128 million in Q1 2026, with total value rising by 194% to $480bn. However, the figures also highlight that FedNow has a significantly higher average transaction value than RTP, with FedNow seeing an average of around $99,000 per transaction in Q1 2026, while for RTP this figure was $3,750.

Although the number of transactions passing through FedNow is still a very small share of those passing through US banks, those that are transacting through the system are trusting it with high-value payments. In November 2025, the Fed raised FedNow’s transaction limit from $1m to $10m in response to growing commercial demand, with the Fed saying this would help it serve high-value use cases including treasury, payroll, vendor and real estate payments.

While the figures show FedNow is growing in usage, the system still has significant challenges, particularly around achieving critical mass among US banks. While participation is growing rapidly, integrating FedNow is a significant challenge for banks, which have to move from infrastructure built for batch processing onto a real-time operating model.

Having said this, the growth of FedNow and its recent proposal add to an ongoing trend to connect real-time payments in the US that we’ve seen from other private players. Venmo, for example, recently announced an integration with PayPal allowing users to send and receive money through PayPal accounts across more than 90 markets, while Zelle launched a new stablecoin-powered offering in October.