The US Federal Reserve’s instant payments system, FedNow, welcomes its first anniversary in July – but how are banks doing on adoption, and what are the remaining challenges ahead?

This July welcomes a major milestone for the Federal Reserve: the one-year anniversary of FedNow – the US central bank’s instant payments rail that is gradually being adopted by banks up and down the country.

Equipping financial institutions with 24/7, 365 payment clearing and settlement services, FedNow is enabling banks to facilitate real-time payments for customers. This makes it similar to the country’s existing RTP system, though this is privately owned by the Clearing House while FedNow is owned and operated by the Fed.

As of the end of June, more than 800 financial institutions across the US have adopted FedNow (versus 570+ on RTP), meaning they can add the service to apps and websites so that customers can send instant payments from their bank accounts. According to a May 2024 survey from the Federal Reserve, consumers are rapidly taking up instant payments, with 86% of businesses and 74% of consumers using faster or instant payments in 2023.

While these figures are promising, there is still some way to go as the Fed reportedly strives to bring FedNow to around 8,000 out of 9,200 financial institutions using the Fed’s services across the country. Aside from RTP, FedNow is competing for relevance amongst several other major legacy payment rails in the US, including the Automated Clearing House (ACH), cheques and major card payment networks such as Visa and Mastercard.

This report explores FedNow’s progress so far, as well as the challenges it is facing on the continuing path to adoption and reiterating a question we first asked in our report on FedNow last year – is FedNow any closer to going cross-border?

FedNow: The story so far

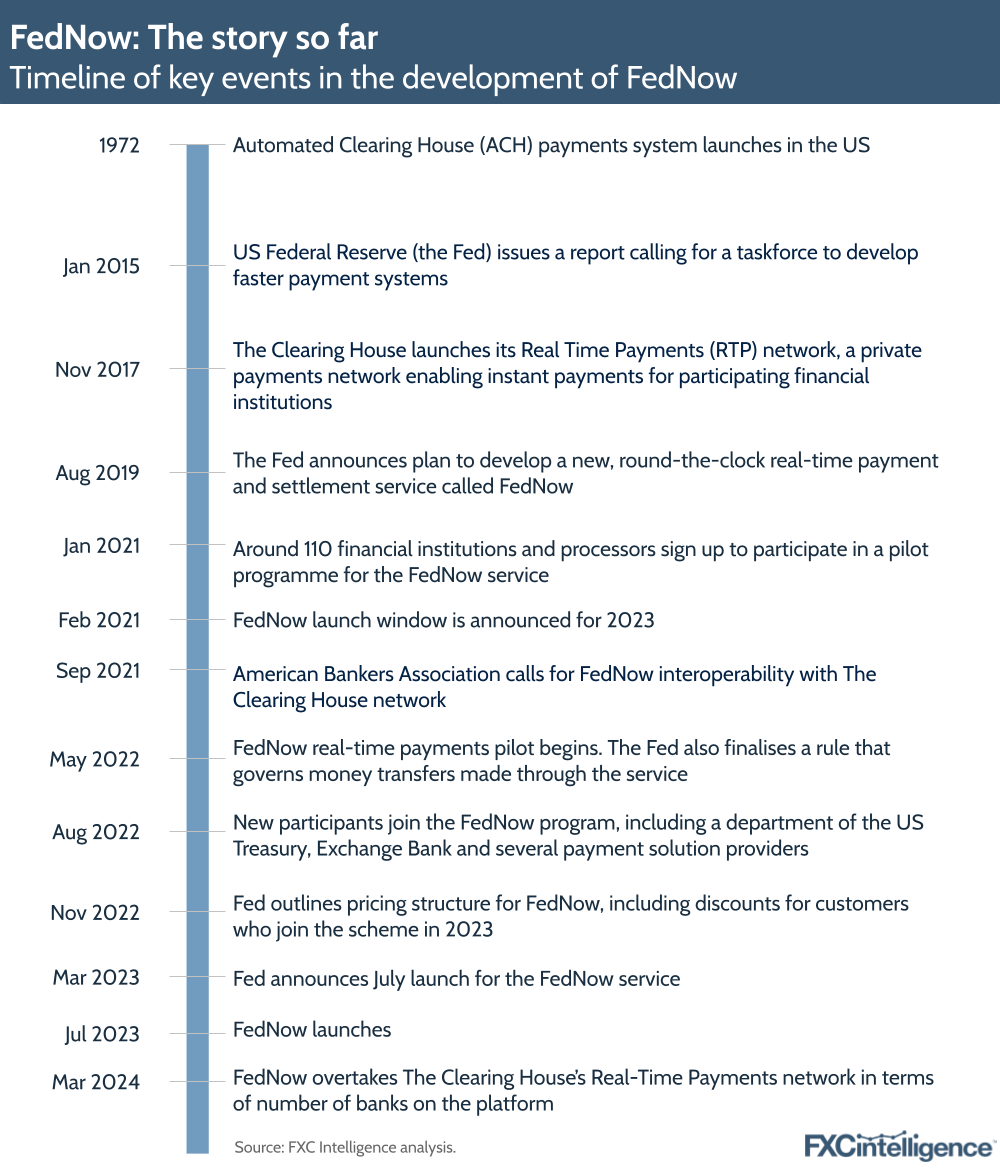

Back in 2015, the US Federal Reserve first issued a report calling for a taskforce to develop a faster payment system than ACH – the country’s batch settlement system that has been in place since the 1970s. However it wasn’t until 20 July 2023 that FedNow finally launched after an extensive testing period amongst 110 financial institutions and processors.

There have been several reasons why the US has looked to develop its own federal instant payments system. Reduced transaction times help consumers get paid and pay businesses quicker, while businesses have more control over cash flow. FedNow can also reduce the costs for financial institutions to process payments, which they can then pass on to customers.

Real-time payments already existed in the US through RTP, but FedNow is aiming to make instant payments more accessible to smaller banks and credit unions, boosting financial inclusion. The system could also stimulate more competition – not just with the existing RTP system but also with traditional card networks, as well as across banks and fintechs looking to create innovative payments products that run on FedNow.

FedNow comes after a number of countries had long since launched their own publicly owned system (such as the UK, India, Brazil and several countries in Southeast Asia), as well as RTP’s launch in 2017. As we noted in our previous report on FedNow, the country has seen several private solutions pop up in response to growing demands for digital payments, such as Zelle and Venmo – P2P payment apps that run on the RTP network.

With real-time payments still gaining traction in the US, the Fed’s goal has therefore been to drive adoption of FedNow amongst institutions in the country, but this will take time – particularly in a US payments landscape in which several other rails already exist.

FedNow’s place in the US payments landscape

FedNow is carving out a space within a legacy payment system, with ACH settlement already integrated into the infrastructure. Some of the different rails include ACH, which can take one to three days to clear; Same Day ACH, where ACH payments are received on the same day, but have a lower maximum payment limit; and wire transfers, which are faster payments but at a significantly higher cost than an ACH payment.

Meanwhile, cheques are still seeing a relatively high amount of usage in the US compared to countries like the UK, with more than three billion cheques collected by the Federal Reserve during 2023 – amounting to a value of $8.4tn. However, it is notable that the volume of cheques collected was down by 6.7% compared to 2022 and has consistently declined since 1999.

Where FedNow and RTP are setting themselves apart is with the promise of low-cost payments for financial institutions at a faster speed. This has particular benefits, for example, for individuals being paid and also paying their bills in the US – two processes that previously have been made fraught by slower processing times. Another strong use case for FedNow is for small businesses, which can immediately access funds when invoices are paid, thereby giving them quick access to working capital.

In terms of how FedNow charges fees, the service charges the sender’s financial institution a flat fee of 4.5 cents for transactions made through the FedNow system. This is on top of a $25 monthly fee for participation, though the Fed notes on its fees page that this has been discounted to $0 in 2024. Having said this, there are differences in the maximum payment amounts – for example, FedNow has a lower max payment limit than RTP.

How many financial institutions have adopted FedNow?

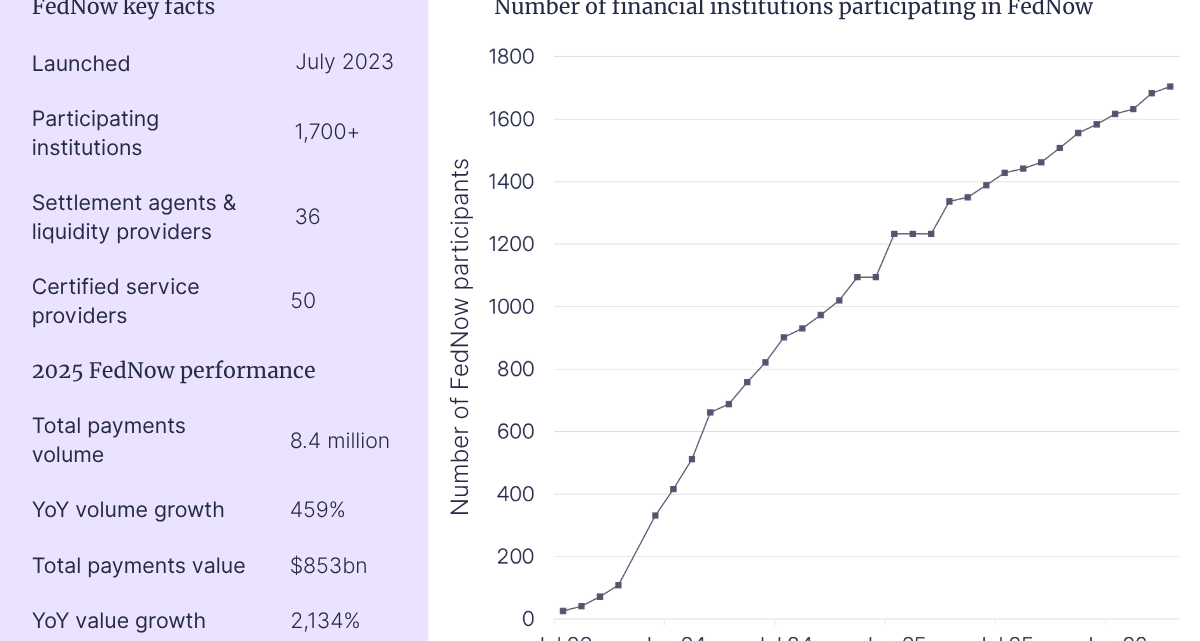

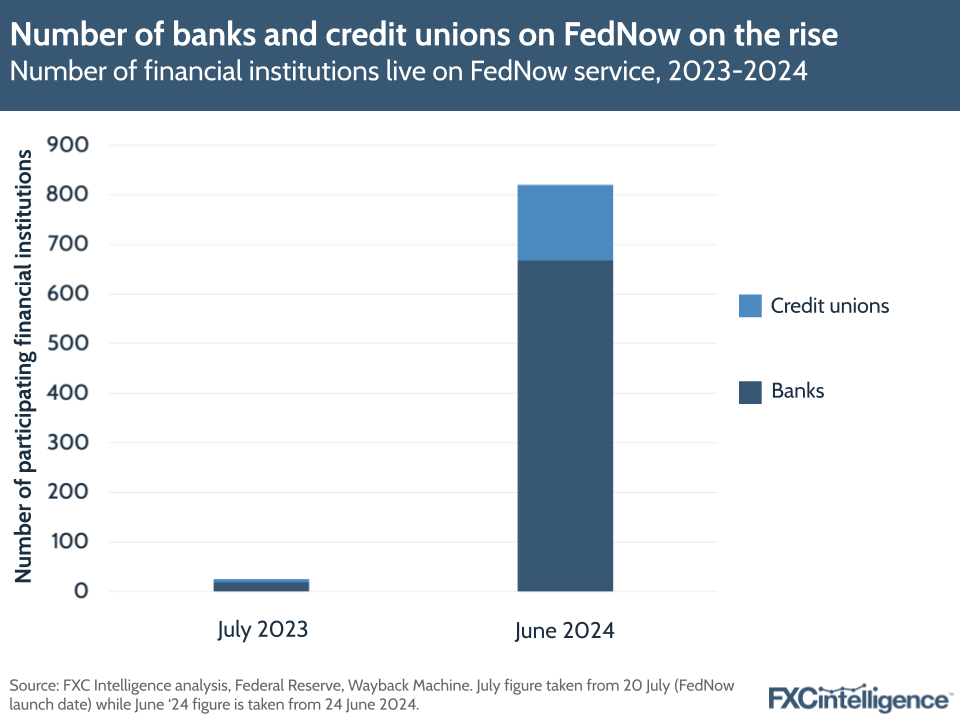

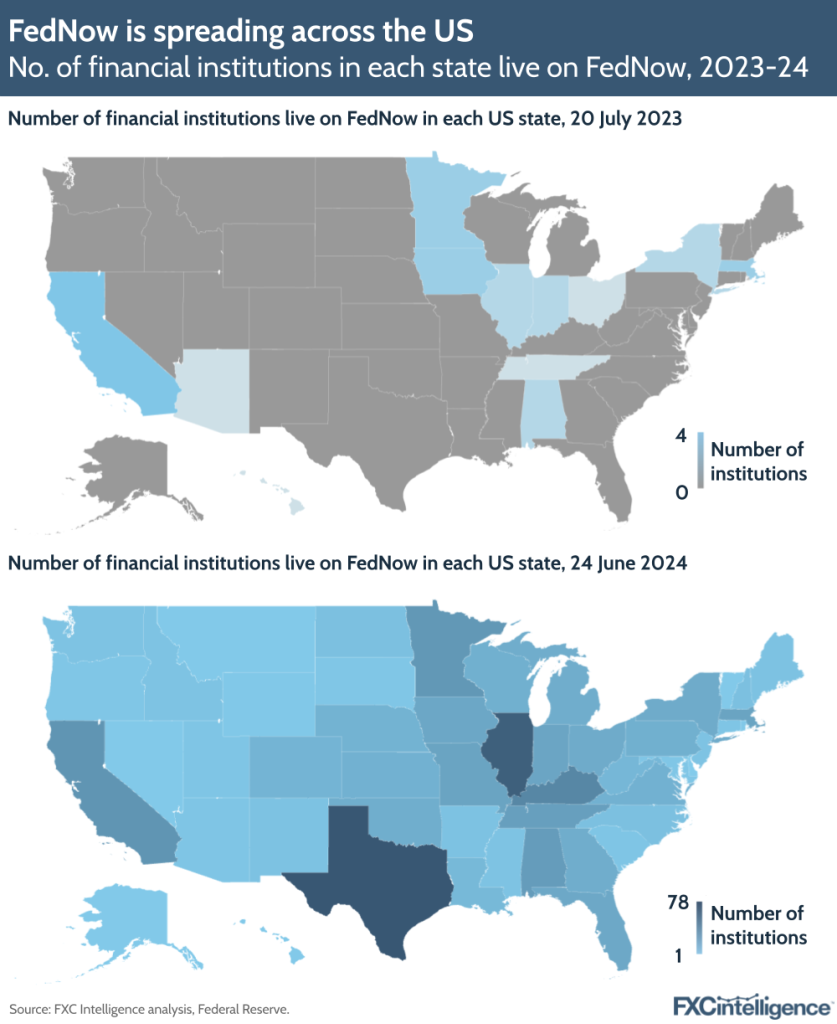

According to the Fed, there are more than 820 financial institutions currently live on FedNow, more than 80% of which are banks, with the remainder being credit unions (not including the U.S. Department of the Treasury’s Bureau of the Fiscal Service). This is up significantly from the 35 participating institutions that FedNow launched with in July 2023, though it is still only around 9% of the 9,000 financial institutions in the US.

The Federal Reserve features a regularly updated list of participating financial institutions on its website. Analysis of this list shows that the number of FedNow institutions has consistently been growing month-on-month but has picked up pace in the last few months, and in March overtook the TCH RTP in terms of institutions adopted.

Notably, the list shown by FedNow only includes banks and credit unions that have completed testing and certification for the services. Should adoption carry on at the current rate, it is likely that this list will have expanded to more than 1,000 banks in the coming months.

When looking at how these financial institutions are mapped out across the country, the progress of FedNow since launch becomes much clearer. Based on the latest data, Texas is currently home to the highest number of financial institutions, followed by Illinois, Kentucky, California and Minnesota.

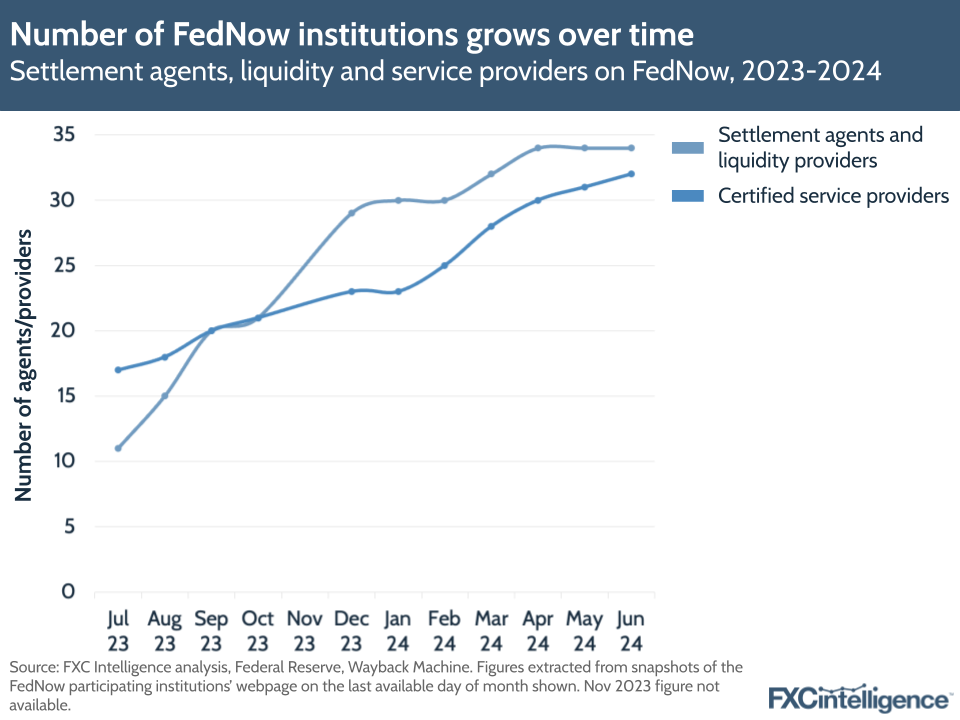

Separately, FedNow also lists financial institutions that are serving as settlement and liquidity providers to the FedNow service – which have grown from 26 at launch to 34 by the end of June – as well as certified service providers, which have completed testing certification to support payment processing for financial institutions – the number of which has increased from 17 to 32 since launch.

These providers are included in a list of more than 130 vendors that advertise an ability to help financial institutions and businesses implement instant payment services, such as bill payments, payroll processing, digital wallets and API development. This list is featured as part of the Fed’s Service Provider Showcase, but not all of them are included on the central bank’s list of certified providers, which only includes providers that have completed testing and operational readiness certification to specifically support FedNow payment processing. Despite being in the showcase, not all of these companies are endorsed by or have a relationship with the Fed.

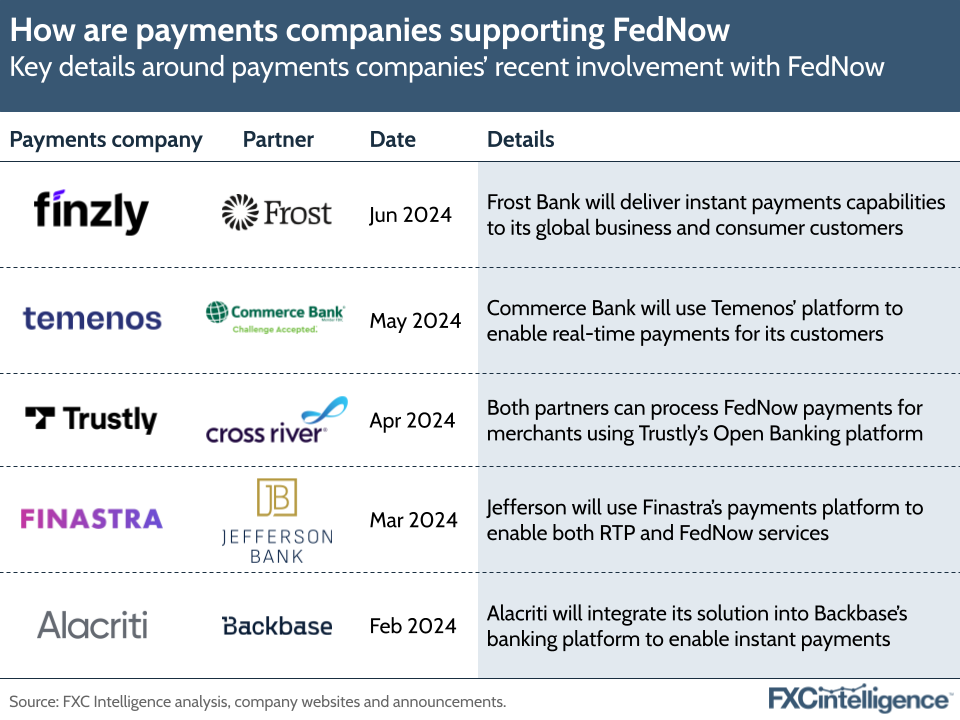

There have been numerous recent examples of new developments of payment companies supporting banks with FedNow payments, including Finzly and Frost Bank; Finastra and Jefferson Bank; and Trustly and Cross River Bank.

As more of these partnerships appear over time and more innovative products are launched on the back of FedNow, current leading payment methods in the US could see a shift in volume towards instant payments – but growing adoption and a shift in consumer behaviour would be important for this.

Where is FedNow already making a difference in the US?

As it stands, FedNow is currently being implemented across a variety of use cases, including account-to-account payments, funding digital wallets, instant insurance disbursements and B2B payments.

According to the Fed’s May 2024 survey, the majority of businesses and consumers are already using faster payments, with 66% of businesses and 61% of consumers saying they are more likely to use faster payments more in the future. However, the Fed has yet to publish figures that show the volume and value of transactions passing through the FedNow service.

Bridget Hall, Leader of Real-Time Payments, Americas for ACI Worldwide, says that FedNow is still “at the beginning stages” of providing significant value to the US economy. However, the impact on financial inclusion and economic growth in countries with strong real-time payments has been very positive, and the US has the potential to reap similar benefits.

One of these benefits is allowing companies to build payments products to better support payment use cases in the US, says Independent Community Bankers of America Vice President Scott Anchin, who says that FedNow is “absolutely making a difference” in the US.

“Financial institutions and payment service providers are rolling out new use cases like earned wage access and business-to-business payments, and consumers and businesses are beginning to realise value,” he adds.

Wages, payroll and the gig economy have been a big part of the FedNow conversation. Reed Luhtanen – the Executive Director of the US Faster Payments Council – says that a lot of use cases for FedNow have come from a small number of big senders dispersing to lots of smaller receivers. He gives the example of companies like Uber, which has been a big user of the RTP network for paying drivers.

Luhtanen adds that demand for faster payments was bolstered in the wake of the Covid-19 pandemic breaking, when many businesses in the US faced a worker shortage. “One of the ways that businesses began competing for labour was to be able to say, ‘hey, we’ll pay you at the end of every shift within seconds’,” he says. “That’s a real benefit to somebody who’s used to having to wait two weeks.”

Another key shift from FedNow could be a change to the way so-called ‘me-to-me’ payments work in the US. At the moment, money transfer apps like PayPal-owned Venmo have increasingly grown their share of P2P payments (Venmo, for example, saw total payment volumes of $69bn in Q1 2024). However, for a user moving money from Venmo – a closed loop system – back to their bank account, this has historically taken longer.

A growing use case, Luhtanen says, will be enabling instant movement of money from one account to another. Another potential area could be in government payments, such as tax refunds and social security benefits, which Luhtanen says would account for a “big chunk of volume” for the network.

David Lebryk, Fiscal Assistant Secretary of the U.S. Department of the Treasury, said on FedNow’s website in October 2023 that more than 90% of recurring and regularly scheduled payments (including social security payments) are currently made electronically, through ACH and other settlement networks, with employee salary payments. He said that this figure would likely not be immediately impacted by the Treasury’s participation in FedNow, but in the near term it could be used for “some types of revenue collections”.

Similarly, a spokesperson for payments infrastructure company Arf says that FedNow will have an impact, but ultimately existing ACH systems still dominate across many areas.

“The availability of the FedNow platform is just the first step; banks must also prioritise and implement the solution effectively,” said the spokesperson. “Although adoption is slow, the benefits, such as reduced chargebacks and instant, irreversible payments, are substantial. As more customers recognise these advantages, we anticipate a gradual increase in FedNow usage, leading to new payment options and programs that leverage its unique capabilities.”

FedNow’s impact on the US fintech space

Complimenting benefits for the end consumer, experts also commented on how FedNow is contributing to greater innovation and competition in the fintech space.

“In terms of ecommerce, PayPal, Venmo and Zelle will benefit from improvements in infrastructure, as well as players like Klarna and Trustly that are gaining market share, “ says PPRO VP Account Management Therese Hudak.

“It will be a competition for the best consumer experience and proposition, but as it looks right now, it will be more of an evolution than a revolution like what we saw in India with UPI and Brazil with Pix.”

In addition to making existing payment services better by reducing risk elements involved with processing delays, Luhtanen says that entirely new services and business models will come to exist that could be made possible by the fact that transactions are moving in real time.

“I liken it to the way the internet enabled Amazon and Netflix,” he adds. “They couldn’t have existed without the infrastructure. I think there are things like that that will come around because of this payments infrastructure existing.”

What are the challenges facing FedNow?

An instant payments-led future would come with plenty of benefits for the US, but there is a reason real-time payments have taken time to come to the country. Many of the country’s thousands of banks are embedded in existing rails and moving to a new system will cost a great deal of time and money.

Of the 9,200 financial institutions that are actively using the Fed’s services, the Fed is looking to onboard up to around 8,000 institutions which it (a) believes are willing to use the new system and (b) believes it can make a business case to for using the system. This is according to an interview with FedNow Head of Payments Product Daniel Baum conducted by Payments Dive in April.

While some big banks have adopted the system – for example, JPMorgan Chase, U.S. Bank and Wells Fargo – others have yet to join the charge. Baum told Payments Dive that while about 60% of institutions have signed up to receive FedNow payments, only around 40% have signed up to send payments – so there is still some way to go to achieve the intended network effect.

According to Scott Anchin, many of the banks that have expressed interest in the system so far have been community banks, which are relationship-oriented and work with customers to understand their needs. However, further support for these players is needed.

“Community banks have found some offerings easy to implement and cost effective, while others have been complex and costly,” he says. “Work to streamline the implementation process and bring costs down would help to accelerate adoption.

Anchin says that many financial institutions are going receive-only as an “initial foray” into adoption, as adding send capabilities brings additional fraud and liquidity concerns. However he says there has been “significant momentum” to develop first and third-party liquidity management and fraud detection and mitigation tools. “As these products and services offerings come to market, financial institutions will likely begin to send instant payments in increasing numbers,” he adds.

Ultimately, joining a new payment rail takes time and, crucially, resources; as banks are juggling numerous priorities, it makes it easy for FedNow to slip through the cracks.

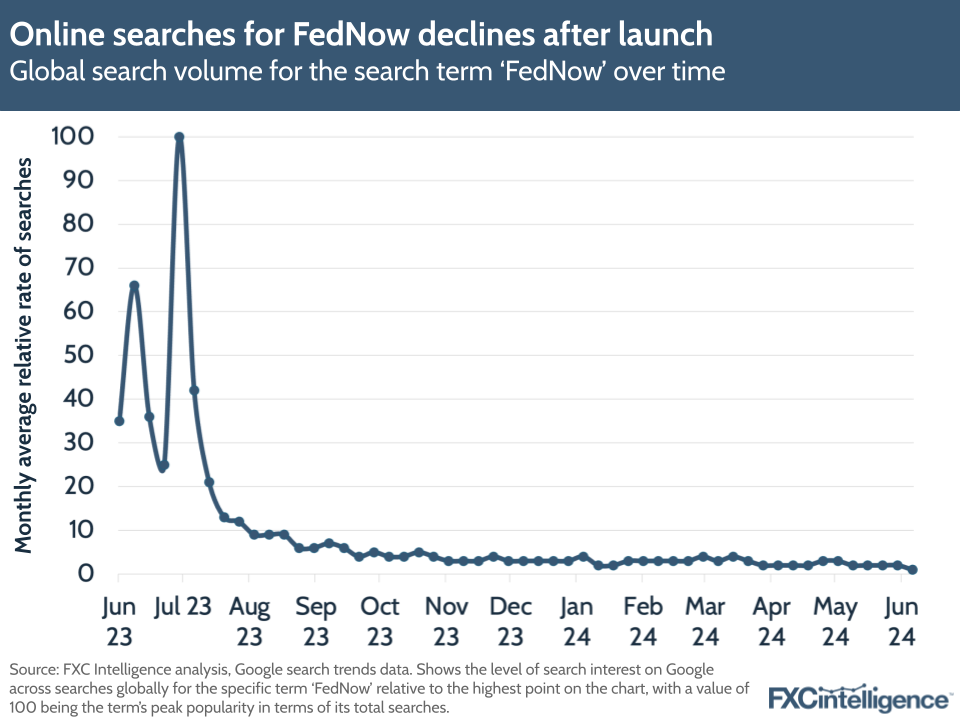

Google search trend data highlights a decline in the relative rate of searches for the term “FedNow” since July last year, which indicates that interest in the topic has waned since the initial hype around the system’s launch.

Looking at the transcripts for earnings calls across the top 10 banks in the US by market capitalisation (including banks that have adopted FedNow, such as JPMorgan Chase) shows almost no mention of FedNow, instant payments or real-time payments at all since the start of last year.

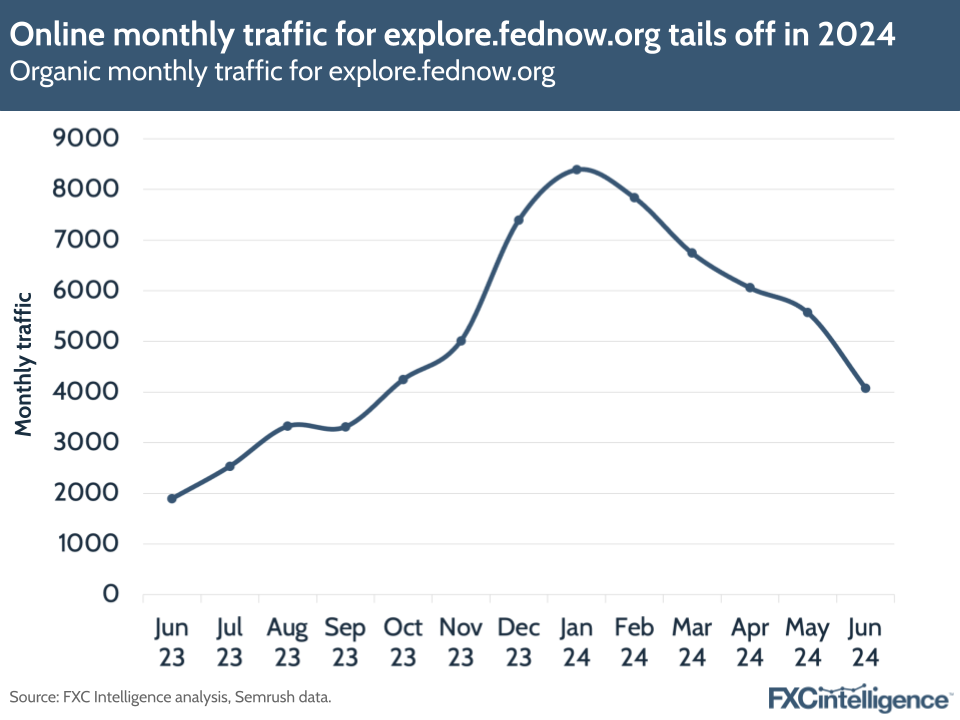

Meanwhile, monthly traffic for explore.fednow.org (which provides further details on the system) rose significantly from the month of Fednow’s launch to January 2024 this year, though it has declined since. Though this accounts for all traffic – and not just those users who might be directly involved in FedNow’s adoption – the suggestion is that the topic is not as high on the agenda for industry stakeholders as it was last year.

Unlike other countries introducing instant payments, the US has not mandated FedNow adoption and many have speculated that it is unlikely to do so. Not only could it require additional authorities to do this, but other payment methods – e.g. cash, writing cheques – are still so frequently used by so many people, using so many institutions, that it would likely be too big a shift to require the whole country to move onto the system at once.

Having said this, real-time payment usage is growing in the country, and Luhtanen says that a generational shift towards digital payments – alongside increasing adoption by financial institutions – could mean that we see a gradual decrease in cash and cheque usage over time, in turn spurring the use of services like FedNow.

On the Fed’s end, the goal will be more about incentivising adoption, through pricing promotions for example. In March 2024, the central bank also introduced the FedNow User Group, which it hopes will promote collaboration among institutions on the network – with one of the goals being to grow the network and identify in-demand use cases for instant payments.

How does the US’ real-time payments adoption compare to other countries?

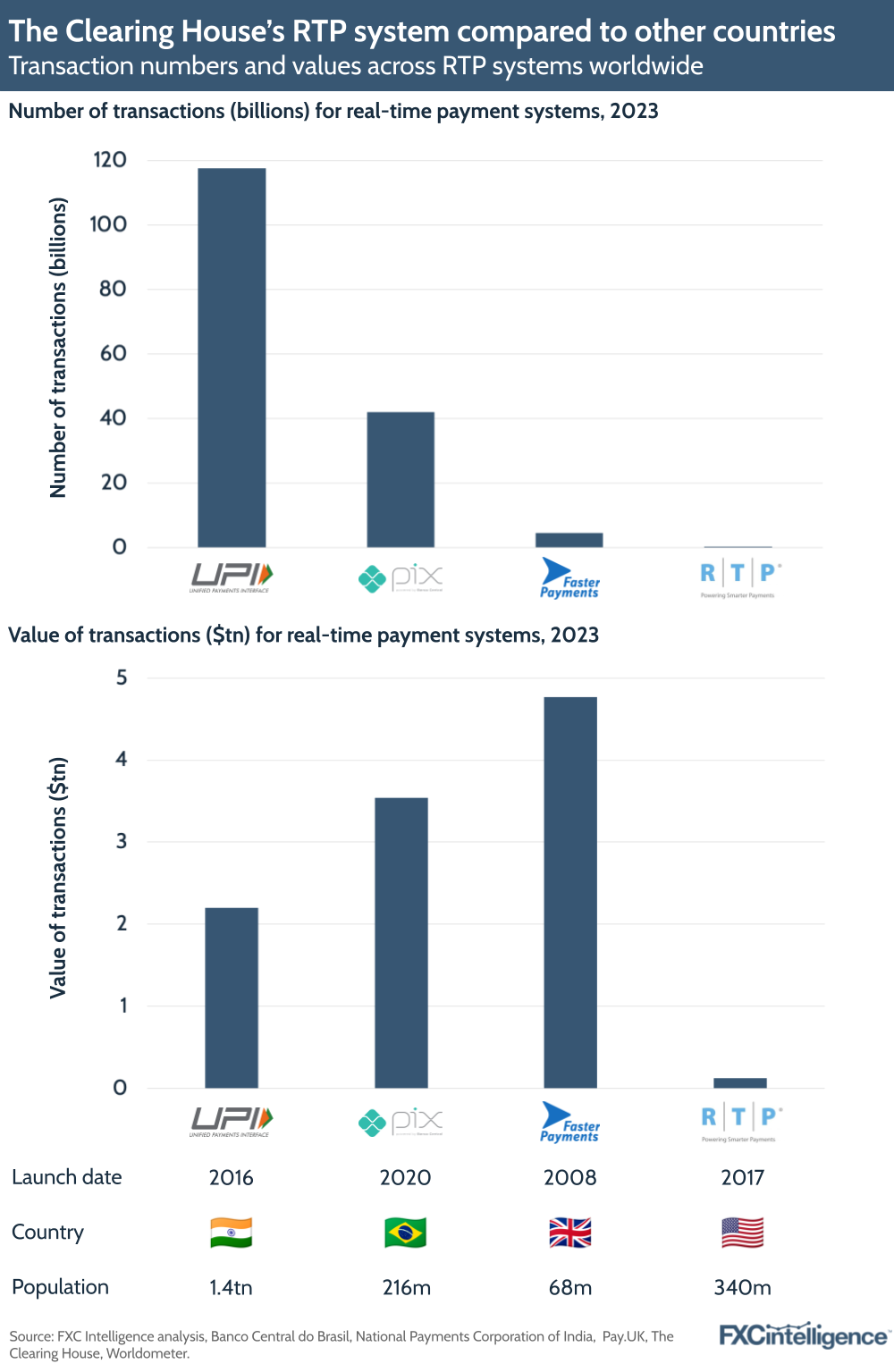

Looking at other systems worldwide shows the scale to which FedNow and RTP are seeing adoption compared to other countries. However, its important to note that different regions have different populations, different numbers of financial institutions, and have also launched at different times.

While FedNow is not currently sharing volumes and transactions data, comparing RTP’s progress with real-time players worldwide presents a picture.

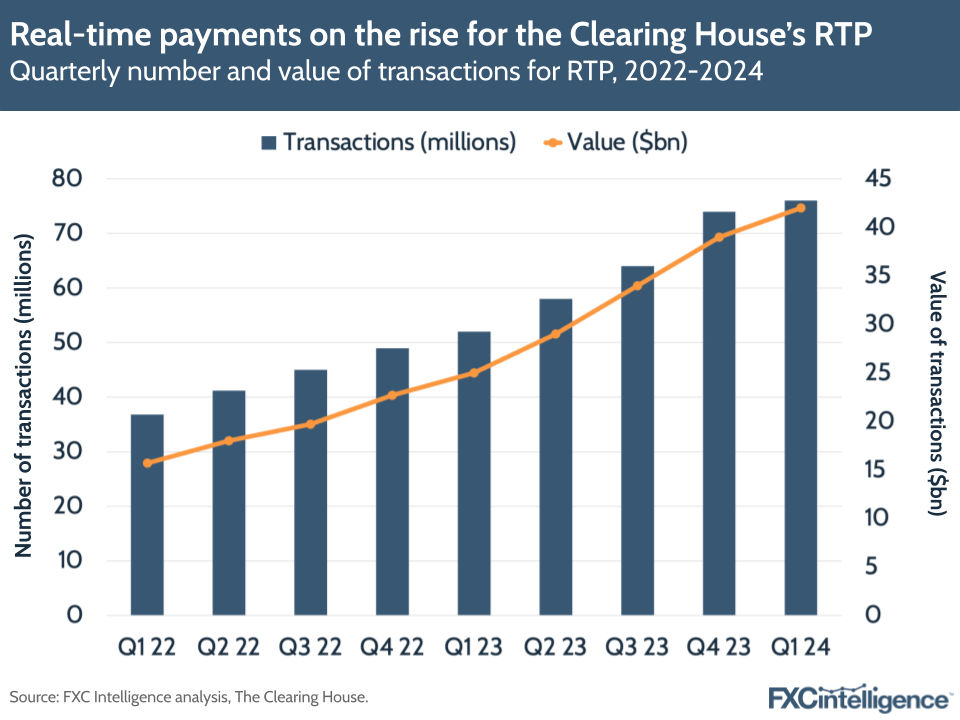

Looking at the basic picture, RTP is seeing significant growth in its volumes, but it’s important to remember this within the context of ACH being the de facto payment rail in the US.

In 2023, the ACH Network securely handled 31.5 billion payments (a 4.8% rise YoY), valued at $80.1tn – a 4.4% YoY increase in payment values. Meanwhile, same-day ACH transaction volumes grew 22.3% YoY to 853.4 million payments, while overall transaction values rose 41.2% YoY to $2.4tn.

By comparison, there were 248 million instant RTP transactions for the year, worth $127bn. However, the system did achieve volume growth of 44% and value growth of 67% in 2023, showing that instant payments on this system are growing faster than the incumbent network.

The same is observed when comparing RTP to other systems worldwide. The real-time payments systems in India (UPI), Brazil (Pix) and the UK (Faster Payments) all process a considerably higher number of transactions. This indicates the extent to which these systems have become embedded in these countries.

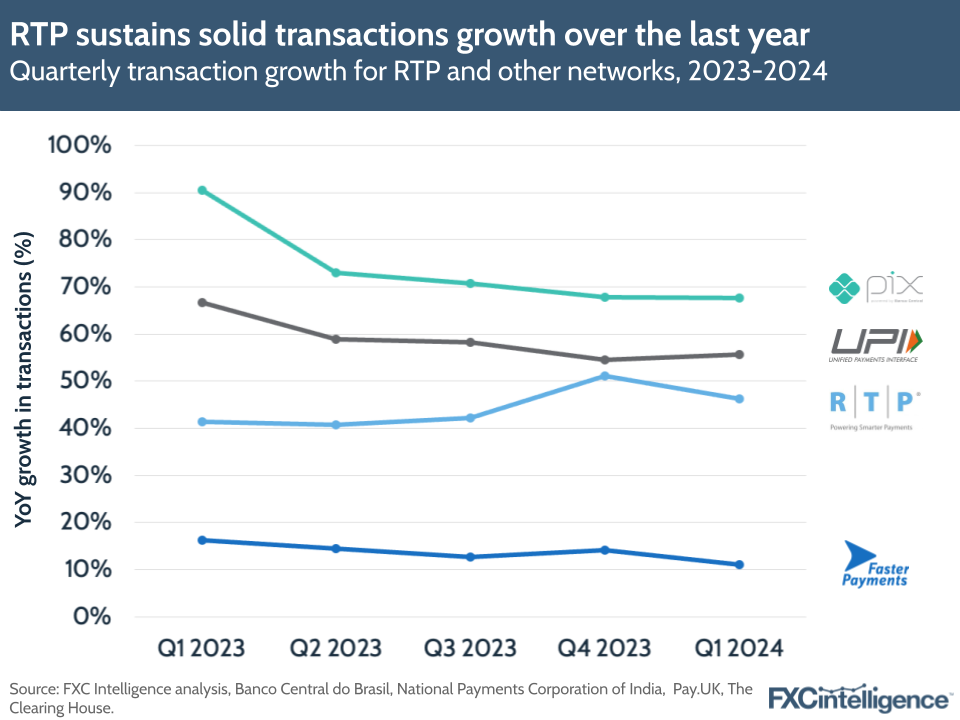

Nevertheless, despite the massive difference in volumes and values, comparing these same systems based on quarterly growth indicates that RTP is being adopted at a pace in line with the rest of the market. The number of RTP payments made in Q1 2024 grew 46% YoY, substantially ahead of the UK’s Faster Payments at 11% (though this system has been around since 2008), though behind UPI at 56% and Pix at 68%.

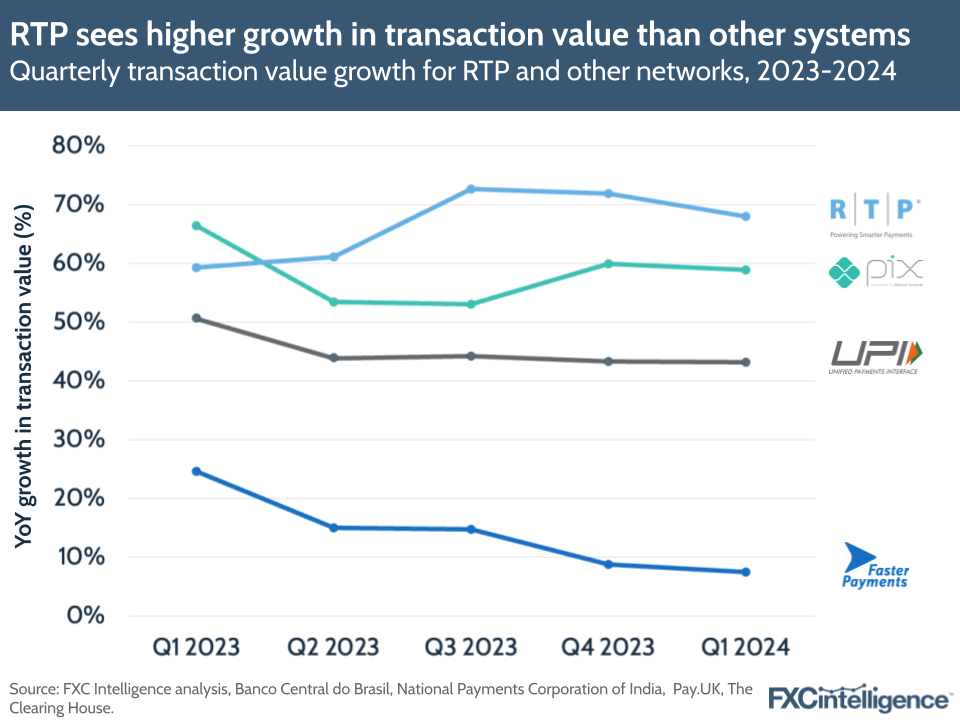

Meanwhile, on value growth, RTP saw the highest growth amongst the rails compared here in Q1 at 68%, followed by Pix at 59%, UPI at 43% and Faster Payments at 8%.

The crux of this is that – in tandem with the initial spurt of growth on FedNow – growing adoption amongst institutions indicates that there is appetite for real-time payments in the US and that this is continuing to grow over time.

Will FedNow be used for cross-border payments?

The conversation on FedNow has revolved around domestic US-based payments, but there have been several launches of cross-border interlinkages between instant payments in other regions of the world; for example, a number of Southeast Asian nations have already synced up their systems to facilitate instant remittances across borders.

The Clearing House itself has already been part of an initiative with EBA Clearing and Swift to connect RTP and pan-European instant payment system RT1 to enable a similar link between the UK and the US.

When asked about FedNow’s cross-border potential a year after the launch, the response from experts was either that it’s too early in the process, or that the current trajectory doesn’t suggest the Fed will move in this direction – given that other systems exist to fulfil this purpose.

“The demand is already satisfied by existing systems like Fed New York and other international correspondent banking relationships,” said the spokesperson from Arf. “Therefore, we don’t foresee FedNow incorporating cross-border functionality as it doesn’t make sense given the current landscape.”

Luhtanen adds that the vast majority of transactions in the US are domestic, and given the spectrum of financial institutions that exist in the US, there is a lot of work to be done first on the domestic side.

“The Clearing House has already proven technically that they can facilitate cross-border transactions into Europe,” says Luhtanen. “It’s not that there isn’t enough interest or demand for cross-border payments. There is definitely demand there, and it will be something that gets done. The point is there is a lot of work to advance adoption and usage domestically that is appropriately being prioritised right now.”

On the other hand, Hall says that the US will “undoubtedly” participate in cross-border real-time payments as FedNow and RTP mature and grow in adoption. “Cross-border payments via non real-time rails are strongly used today,” she says. “Pairing existing use cases, as well as enabling new use cases, with the benefits of real-time payments for added value should be considered as modernisation of payments is discussed and prioritised.”

While he believes that the Federal Reserve is “laser-focused” on encouraging and supporting domestic adoption, Anchin said that demand is there to make cross-border payments faster, safer and more efficient, and has in fact been a Federal Reserve strategic objective since 2015.

“FedNow has the technical underpinnings to enable cross-border instant payments, including support for the ISO 20022 messaging standard, so I imagine cross-border capabilities are on the long-term roadmap.”

As it stands, the continued adoption of FedNow may not have a direct bearing on international payments as it finds its feet within the domestic space. While some are praising the speed of adoption over the course of the year, looking at the wider payments landscape indicates there is still some way to go on this and while the benefits are being seen in some areas, it’s unlikely that in another year’s time the US’ payments landscape will look vastly different from it looks now.

While some experts we spoke to said adoption was progressing well, others have been less positive about the rate of adoption.

“Regarding FedNow adoption, it’s not moving very fast,” said the spokesperson from Arf. “Many banks currently profit from ACH transactions and are hesitant to shift to FedNow due to potential revenue loss from overnight deposits and related charges.”

“While some major banks have started offering FedNow, it is not yet a priority for smaller banks. We estimate that widespread adoption across all 8,000 banks might take another three to six years. Thus, we shouldn’t expect immediate, universal implementation.”