Last week, we looked at the impact of big tech on cross-border payments. This week, we zoom out and analyse some of the macro trends driving the sector, focusing on cross-border card and e-wallet payments. We also look at Ripple’s additional $20m investment into MoneyGram.

What’s driving cross-border card payments?

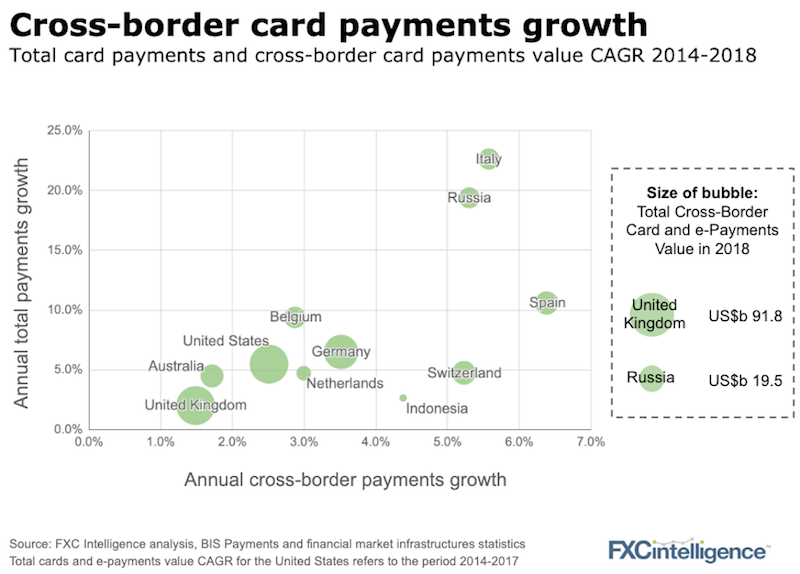

Payments by cash and bank transfer is one side of the cross-border money transfer market. The other is card and electronic wallet payments. Our insights below are for the largest economies where consistent, comparative data is available.

There are many payment companies entering the space and others launching new products to better serve the cross-border needs for card and e-wallet transactions.

What’s driving the sector?

Overall growth in card payments is driven by the general shift away from cash especially in Southern and Eastern Europe (e.g. Italy, Russia and Spain are very cash-reliant economies) and developing countries (e.g. Indonesia). In countries such as the UK and the Netherlands, card usage is reaching a more mature stage.

Why is cross-border payments growth slower than overall card payments growth?

We see a number of factors:

- The relatively high costs of using a card internationally versus domestically, driven by a range of FX and cross-border fees (with a large variances in these costs across cards, issuers and countries).

- As the acquiring market is highly fragmented, it is difficult for customers and merchants to have fast and broad access to international payment systems.

- Cross-border card payments is also highly linked to e-commerce growth – slow growing e-commerce markets have slower growth in cross-border card payments.

What are the implications?

- Regulations that help to reduce the cost of card payments abroad may make card usage more transparent and faster and this may drive growth (e.g. the EU Cross-Border services law) .

- We’d expect to see more investment by fintech players into the high-growth markets such as Spain, Italy and Russia to serve the growing demand.

- There are network effects from digital payment/wallet adoption. Venmo in the US has over 40 million users and as scale and options grow in other markets (e.g. Revolut), the usage of these payment methods will grow.

The latest investment in MoneyGram

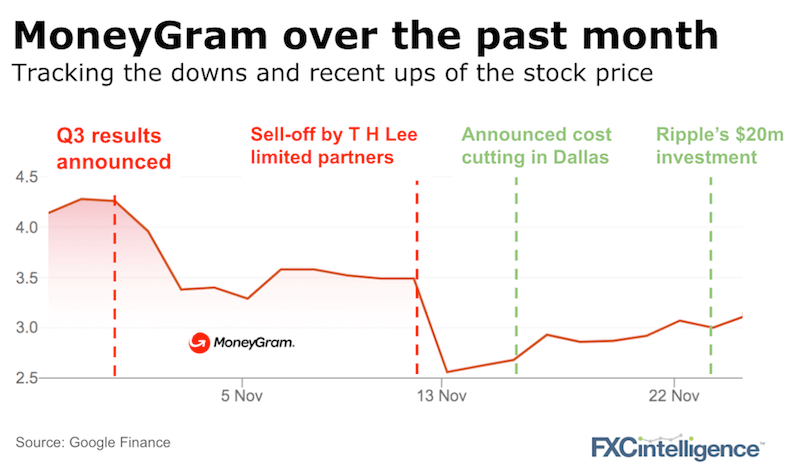

We recently analysed the most volatile public company payment stocks. Top of the list was MoneyGram.

This past week, Ripple invested a further $20m into MoneyGram completing its planned $50m investment. Ripple now owns just under 10% of MoneyGram.

Although the price of Ripple’s investment per share was just over $4, the market, which keeps changing its mind on MoneyGram, doesn’t agree with this value yet. Recent news has been more positively received for MoneyGram with the stock picking up – will this continue?

We track the pricing of many thousands of cross-border payment cards across the globe. To use this data to drive your strategy and pricing get in touch.

[fxci_space class=”tailor-6333128234742″][/fxci_space]