Open banking (the ability to connect directly to a customer’s bank account) has taken time to get going.

Before 2016, it was hardly talked about. With PSD2 and other similar regulations entering into force, open banking now appears to be a predictor of where finance and payments are heading as it democratises access to customers and their data. This has spawned some interesting developments in the international payments space.

Some takeaways:

- Financial services are becoming more accessible. New apps and products increase financial literacy and provide the opportunity to recommend products.

- Data, previously the right of just the customers’ bank, is now freely available (with the customer’s permission). This shifting of data rights provides opportunities for non-bank institutions and other companies to build new products based on this insight.

- A need for cross-border payments can now be easily identified for customers who allow access to their data. An alternative option (usually cheaper and faster) can be offered, taking the cross-border business away from the banking incumbents.

- Fewer and fewer payments will have to be initiated directly from banks. This is good news for payment companies, less so for the banks. Some forward thinking banks such as Barclays and Lloyds already offer account aggregation services to pull funds from competitor accounts.

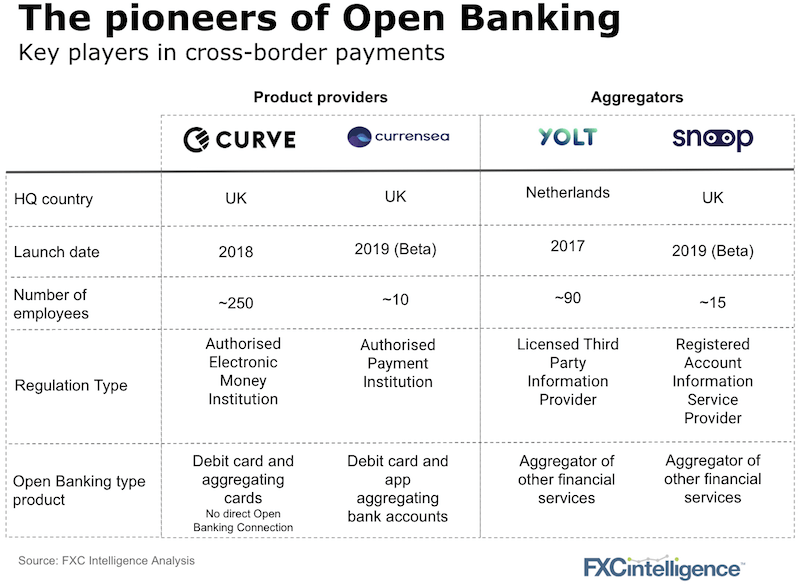

- Some players such as Currensea have a direct connection via open banking sharing data. Others such as Curve do not have connections but are building similar banking aggregation products.

2019 was very much a year of transition from competition between banks and fintechs to partnerships. Open banking knocks down one more barrier and means a fintech no longer needs to setup a formal relationship with a bank to partner with them. This will massively speed up product development and means the rate of change in this decade is likely to come even faster than before.

[fxci_space class=”tailor-63341c4f3330g”][/fxci_space]