Digital banks are the latest competition

Whilst the new digital banks (Monzo, Starling, N26 and others) have been grabbing the headlines with their top line growth, they have also been putting formidable payment offerings in place. Backed by venture money and a target to simply grow, they have made it into our market share data and therefore onto our radar.

These new digital banks accounted for 5% of UK consumer money transfer in 2018, according to research we provided for the FCA last year. A year before, they didn’t even register.

What makes the digital banks such formidable competitors

- Banks own the customer, but digital banks now own millions of customers too.

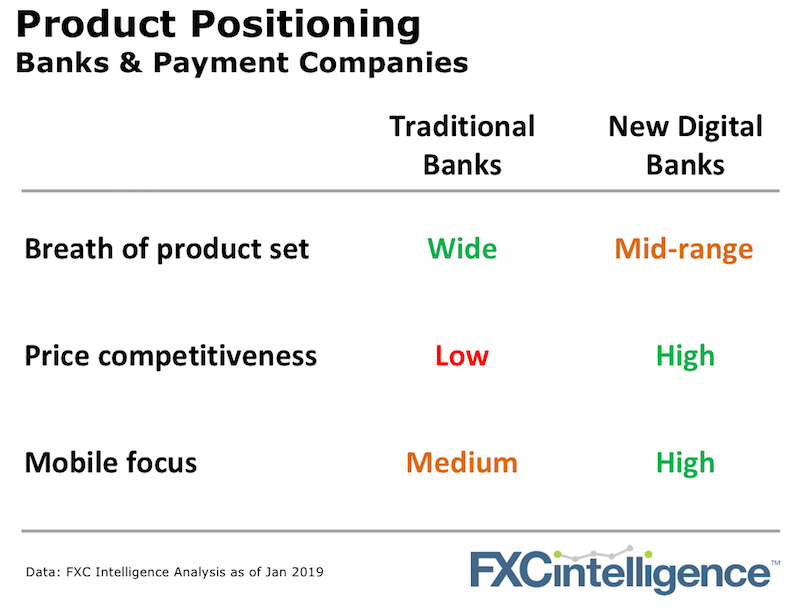

- Digital banks are still focused on customers not revenue, so pricing can be very aggressive. Monzo and N26 have simply plugged TransferWise into their product with no additional markups. Starling Bank, after flirting with TransferWise, decided to build its own payment product, albeit with a similar pricing structure.

- Traditional banks still have the widest range of services but the new digital banks have their own customer hooks. Deposit or savings accounts, loans and mortgages are currently enough to pull millions of new customers in.

- Since digital banks are the newest kids on the block, they are unencumbered by historical tech debt and are inherently more mobile friendly and tech forward. That only helps when it comes to user experience.

So how do these new banks fit alongside the dedicated payment companies?

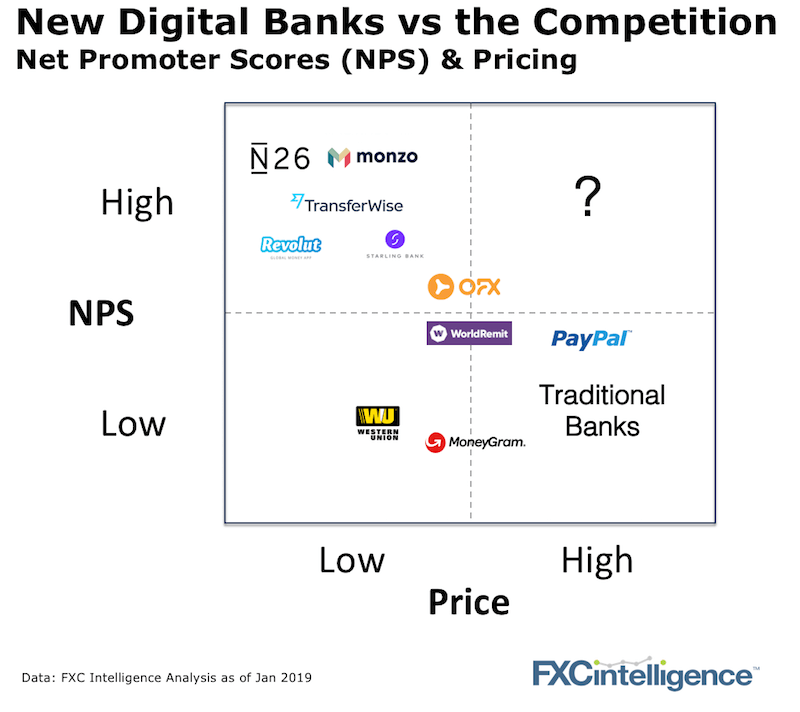

Does a low price = a high customer rating?

The only players in the market that have Net Promoter Scores close to fintechs like TransferWise and Revolut are the new digital banks. Monzo claims to have an NPS above 80, which would be in line with TransferWise and Revolut (according to our NPS data).

Is it possible to have a service loved by customers and charge a premium? For commodity products like international payments, the positioning of key players in the market suggest that if it is possible, no one has yet figured out how.

Some groups such as OFX (make sure to read our recent CEO interview) and WorldRemit are maintaining relatively high prices and strong but not top-end NPS scores. The question is where they go from there.

The big brands (PayPal, major banks) leverage their trust and awareness to price at a premium level. And interestingly, will Western Union, which is becoming much more price competitive, see a bump in its customer love or does it retain too much historical baggage?

[fxci_space class=”tailor-6331b744d2e26″][/fxci_space]