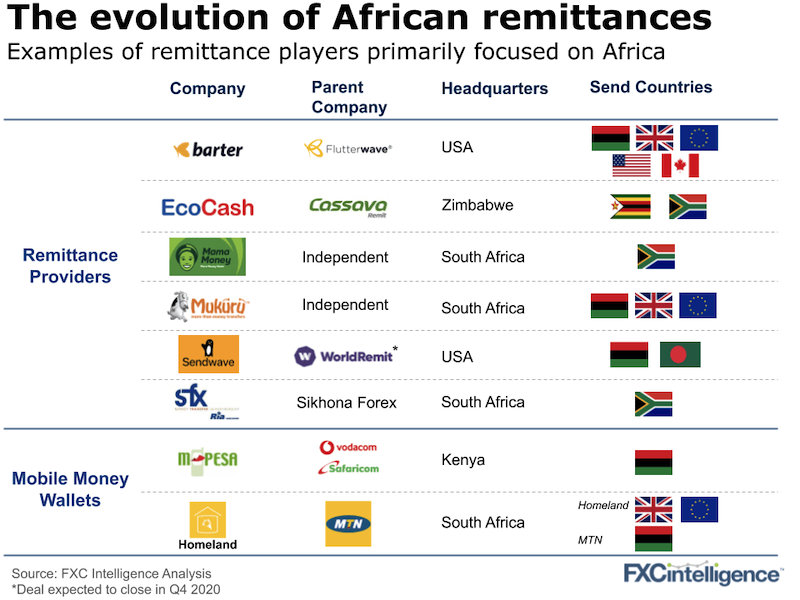

Incumbents such as Western Union, MoneyGram and Ria still dominate remittances to and within Africa and players such as WorldRemit and Azimo are fast gaining share. But many regional players have been emerging, focusing in on migrants within the continent and beyond, often just for a handful of corridors.

This week, we take a deep dive into remittance trends in Africa following a conversation with Nicolas Vonthron, Mama Money’s CEO.

Our main thoughts:

- Digital is gaining ground, but the retail channel is key

Cash pay-ins and pay-outs remain dominant in the continent. At Mama Money, for example, cash accounts for 90% of total pay-ins. This makes physical agents essential, but their role is different from those in other parts of the world. They also help to improve financial and technological literacy among African consumers, emphasising the convenience and safety of digital payment methods such as bank account-based remittances and wallets. This method is gaining ground, particularly in countries such as Tanzania and Kenya, where M-Pesa paved the way.

- Competition is becoming fierce…

Competition in the African remittances market has ramped up in the recent years. Informal channels, such as sending money through bus drivers, are still widely used by consumers, although costs are very high. However, growing competition in formal channels, including the players in our chart above, is driving down costs.

- …but incumbents and digital players are still dominating the market

Digital remittance players such as WorldRemit and Azimo are gradually expanding in Africa. This is thanks to partnerships with mobile wallet providers and a willingness to adapt to market requirements with the offer of cash payouts. Western Union, MoneyGram and Ria continue to dominate the market with their large retail networks, which can also be leveraged for pay in and pay out by regional players, and partnerships with major financial conglomerates such as ABSA.

- Improving overall financial inclusion

Although regional differences exist, a high proportion of Africa’s population remains unbanked with only 33% of the adult population in Sub-Saharan Africa owning a bank account as of 2017. But new products are emerging across the region. Mama Money is building a banking product for diaspora workers, while Chipper Cash, which raised $30m in November, and Eversend have already launched digital banking products. Although not specifically focused on remittances, the latter two players will look to gain market share by focusing on intra-Africa cross-border payments as well as broader sets of financial services.

As populations across Africa become more mobile, expect the within Africa remittances opportunity to continue to grow, alongside the well-established diaspora corridors. More funding and product development will surely follow.