Will MoneyGram survive? Will Ripple save MoneyGram or MoneyGram launch Ripple? MoneyGram’s Q4 earnings, released on 25 February, shed new light on the operations of both companies. We do a deep dive on both of them below.

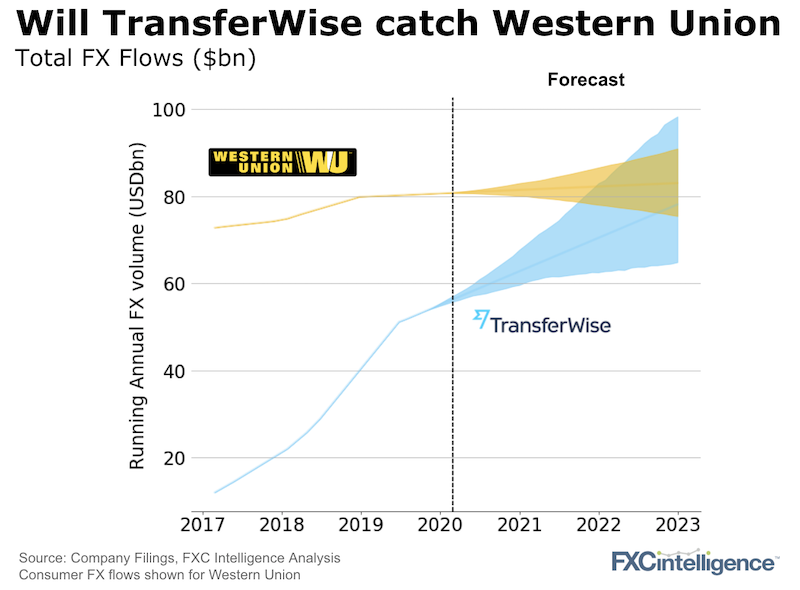

With clarity as to Western Union’s 2019 numbers, we can ask the question how long until the fastest growing competitor – TransferWise – catches them?

MoneyGram and Ripple – who needs who?

Sometimes it just takes a small accounting mistake. It may have been a small error by MoneyGram in how they classified the payments they received from Ripple but that has now forced MoneyGram to shed a lot more light on the operations of both businesses.

Let’s first detail what we now know in six brief points:

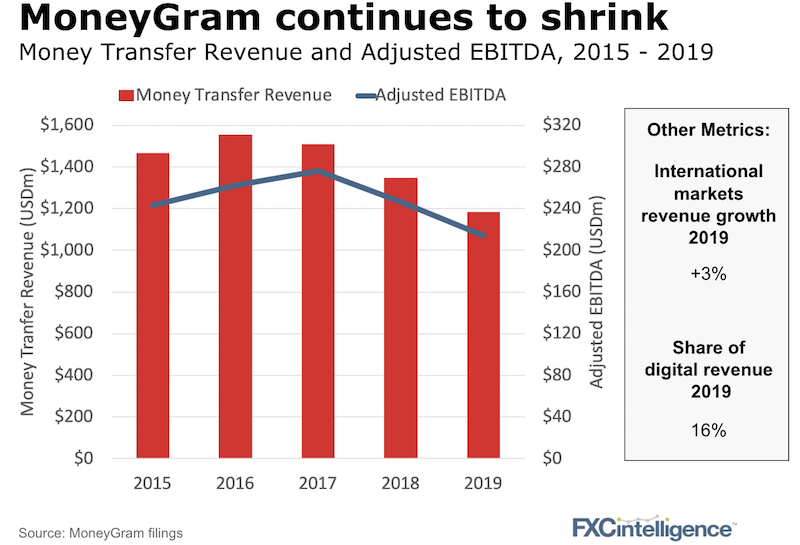

1) MoneyGram is having a hard time

Since the US government stopped Ant Financial from buying MoneyGram in 2017, MoneyGram’s share price has gone from a high of nearly $18 to a low of just over $2 today. Its financials have continued to decline.

2) Ripple’s relationship with MoneyGram

Ripple currently owns just under 10% of MoneyGram, having invested $50m in two tranches in June 2019 and November 2019 (at a price of $4.1/share). In the documents filed by MoneyGram this week, they showed that Ripple paid them $2.4m in Q3 of 2019 and $8.9m in Q4 of 2019. These payments, which were initially classified as revenue, had to be re-classified as a “contra expense” under the SEC’s guidance, becoming pretty much free cash flow for MoneyGram.

3) MoneyGram’s free cash flow

In Q4 of 2019, MoneyGram as a business generated $19.8m of free cash flow. (Generating free cash flow is what my old business school corporate finance professor called the core purpose of a business). Ripple accounted for 45% of this free cash flow.

4) Ripple’s ongoing support of MoneyGram

In 2020, MoneyGram expects a slight increase in the run-rate of Ripple’s payments, which are proportional to the amount of FX flow MoneyGram uses Ripple’s XRP on-demand liquidity product for (right now this is predominantly the US to Mexico corridor).

We estimate the 2020 contribution from Ripple will be around $40-50m. The contract for these payments currently lasts until 2023 – a date that was shared by MoneyGram’s CEO in their earning call (yes, we do read these 10,000 word transcripts so you don’t have to).

5) What will happen to MoneyGram’s Walmart business?

MoneyGram expects to lose a significant share of its Walmart business. Walmart opened up its platform to competition last year and MoneyGram’s Walmart2World product accounts for around 9% of MoneyGram’s total revenue. So significant and uncertain is the impact of this potential loss that MoneyGram is now only able to give stock market guidance on a quarterly basis as opposed to annually.

6) MoneyGram’s Deferred Prosecution Agreement extension

MoneyGram further announced this week that it pushed back by six months the $55m payment it still owes the US government as part of its Deferred Prosecution Agreement (DPA) and is negotiating for a further extension and reduction. One of the reasons stated by MoneyGram is simply that the company might not be able to afford to make the payment.

How did the markets react to all this?

- Although MoneyGram is one of the most volatile payment stocks, Tuesday’s releases still knocked around 20% off its share price.

- The value of XRP to the USD (also highly volatile) is down 15% since Tuesday.

What questions does this leave us?

- Will MoneyGram survive? Or will it survive long enough to exit the DPA and find a buyer? Is the business worth its current enterprise value of $1bn, which includes $850m of debt?

- What is the MoneyGram brand worth? Our own research suggests that whilst awareness is well below Western Union, MoneyGram is still a widely recognised financial brand, far above most other competitors.

- How should we read Ripple? Is paying your customers to use your service a reasonable path to growth? In 2019, Ripple raised $200m from investors and sold a further c.$500m of XRP. Ripple also still sits on more than $10bn of XRP so paying MoneyGram perhaps $200m over the next four years is clearly not a financial constraint.

Steady on TransferWise

When it comes to total FX flow, Western Union had a flat-ish 2019. If TransferWise is going to catch up, this surely helps.

Although still among the most impressive in the industry, TransferWise’s growth rates have slowed and 2019 looks to be an inflection point. What was once triple digit growth is now high single digit growth.

New white-label deals will help but, so far, the deals have mostly been with new digital banks. These banks may have large customer numbers but they also have much smaller wallet share and relatively small cross-border payment flows.

And don’t forget that when it comes to revenue, Western Union is still far ahead of TransferWise, driven by a much higher take-rate (pricing).

[fxci_space class=”tailor-63342fde3d46h”][/fxci_space]